|

시장보고서

상품코드

1683218

고분자 바이오소재 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Global Polymeric Biomaterials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

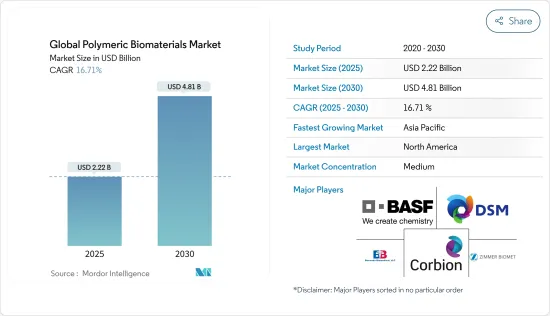

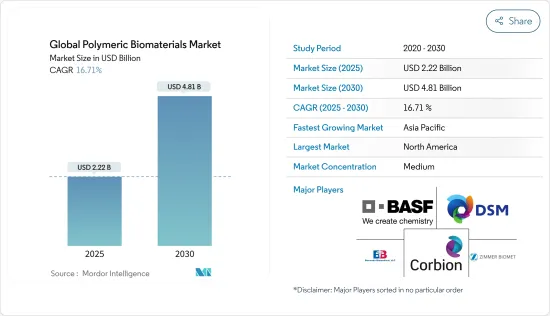

세계의 고분자 바이오소재 시장 규모는 2025년에 22억 2,000만 달러로 추정되고, 예측 기간 2025년부터 2030년까지 CAGR은 16.71%로 전망되며, 2030년에는 48억 1,000만 달러에 달할 것으로 예측됩니다.

시장 성장을 뒷받침하는 주요 요인으로는 고분자 바이오소재의 기술 혁신과 조직 공학에서 고분자 바이오소재의 용도 확대 등이 있습니다. 신경과 정형외과 수술의 수가 증가하고 있는 것은 세계 시장 성장의 주요 요인 중 하나입니다.

예를 들어, 2024년 2월에 Parkinson's United Kingdom(영국)에서 발표된 보고서에 따르면, 영국에서는 약 15만 3,000명이 파킨슨병을 앓고 있습니다. 인구 고령화와 지속적인 증가로 이 수치는 2030년까지 20% 가까이 증가하여 17만 2,000명이 될 것으로 예측됩니다. 노화에 따른 파킨슨병의 유병률 증가는 고분자 바이오소재 시장의 성장을 뒷받침하고 있습니다. 이러한 물질은 약물 전달 시스템 및 신경 임플란트와 같은 고급 치료 솔루션의 개발에 점점 더 많이 사용되고 있습니다.

게다가, 고분자 바이오소재 용도의 확산과 신제품의 투입이 함께 시장의 성장을 가속할 것으로 예상됩니다. 예를 들어, 2023년 6월, International Flavors & Fragrances(IFF)는 기존의 화석 유래 재료와 동등하거나 그 이상의 성능을 가지며 지속 가능한 이점을 제공하는 바이오소재 개발을 목적으로 하는 획기적인 DEB(Designated Enzymatic Biomaterials) 기술을 발표했습니다. 이 기술 혁신은 다양한 산업에서 지속가능하고 고성능인 대체재료에 대한 규제와 소비자의 요구 증가에 부응하여 고분자 바이오소재 시장의 성장을 가속할 것으로 기대되고 있습니다.

결론적으로 고분자 바이오소재의 기술 혁신, 용도 확대, 지속 가능한 바이오소재의 진보가 고분자 바이오소재 시장의 성장을 가속하고 있습니다. 그러나 고분자 바이오소재와 관련된 합병증은 시장 성장을 방해할 것으로 예상됩니다.

세계 고분자 바이오소재의 동향

정형외과 부문은 예측기간 동안 큰 성장이 예상됩니다.

근골격계 장애(MSD)가 증가함에 따라, MSD는 수술적 치료를 필요로 하므로 정형외과 부위가 증가할 가능성이 높습니다. 따라서, 이러한 치료를 위한 바이오소재에 대한 요구는 높습니다. 예를 들어 호주 정부가 2024년 6월 발표한 보고서에 따르면 호주는 2023년 인구의 29%에 해당하는 약 730만 명이 만성 근골격계 질환을 앓고 있는 것으로 추정됩니다. 그 중 400만 명이 요통, 370만 명이 관절염, 85만 4,000명이 골다공증 또는 골감소증입니다. 만성 근골격계 질환의 유병률이 높아 진보된 정형외과 솔루션 수요를 견인하고 있습니다. 이러한 수요 증가는 정형외과 부문의 성장을 뒷받침하고 있으며, 치료 및 수술용 모두 혁신적이고 내구성 있고 생체적합성이 있는 재료의 필요성이 부각되고 있습니다.

또한 세계 노인이 증가하고 있기 때문에 관절염, 골관절염, 류마티스 관절염 등 정형외과 질환을 앓고 있는 사람의 수가 증가할 것으로 예상됩니다. 예를 들어, 세계보건기구(WHO)가 2023년 7월 발표한 보고서에 따르면 인구 고령화가 골관절염의 급격한 증가로 이어지고 있으며, 전 세계적으로 5억 2,800만 명 이상이 앓고 있으며 대부분 55세 이상입니다. 정형외과 질환의 이환율이 높은 고령자 증가는 첨단 치료에 대한 수요를 촉진하고, 보다 효과적이고 내구성 있는 바이오소재의 정형외과 솔루션에 대한 요구를 통해 고분자 바이오소재 시장의 정형외과 부문의 성장을 가속하고 있습니다.

또한 주요 시장 진출 기업의 노력도 같은 부문의 성장을 가져오는 요인 중 하나입니다. 예를 들어, 2023년 2월, Invibio Biomaterial Solutions는 영국 리즈에 새로운 정형외과 제품 개발 시설을 개설했습니다. 이는 의료기기의 연구개발과 제조능력을 강화하기 위한 전략적 확대를 의미합니다. 이 개발로 인비비오는 선진적인 폴리에테르에테르케톤(PEEK) 폴리머제 임플란트 디바이스의 공동개발 및 출시에서 OEM 제조업체를 지원하는 능력을 강화함과 동시에 학계 및 의료 관련 기업과의 협력관계를 촉진했습니다.

결론적으로, 정형외과 부문에서의 진보, 정형외과 질환의 유병률 증가, 다양한 의료 부문에서의 용도 확대로 인해 고분자 바이오소재에 대한 수요 증가가 이 부문의 성장을 크게 촉진할 것으로 예상됩니다.

예측기간 중 북미가 시장에서 큰 점유율을 차지할 전망

북미는 고분자 바이오소재 시장에서 큰 점유율을 차지하고 있으며, 앞으로도 그 아성은 흔들리지 않을 것으로 예상됩니다. 미국에서는 여러 비공개 회사가 바이오폴리머에 대한 풍부한 전문 지식을 가지고 있으며 첨단 기술과 맞춤 합성에 액세스하고 있습니다. 정형외과 및 정형외과적 손상과 같은 수술 증가와 같은 중요한 요인이 시장 성장을 뒷받침할 것으로 예상됩니다.

예를 들어 2024년 6월에 발표된 국제미용정형외과학회 보고서에 따르면 미국은 세계에서 가장 많은 미용정형외과 수술을 실시했으며 2023년에는 610만 건을 넘어섰습니다. 이러한 수술, 특히 성형 외과 수술의 수가 많음이 고분자 바이오소재 시장의 성장을 뒷받침하고 있습니다. 이 물질은 조직 적합성을 높이고 감염 위험을 줄이고 전반적인 수술 결과를 향상시킵니다.

마찬가지로 캐나다에서 눈 질환의 유병률 상승도 시장 성장을 가속할 것으로 예상됩니다. 예를 들어, North Toronto Eye Care가 발표한 기사에 따르면, 2023년 6월에는 250만 명의 캐나다인이 백내장과 함께 생활하고 있습니다. 이 나라에서는 매년 35만 건 이상의 백내장 수술이 진행되고 있습니다. 캐나다에서는 백내장과 같은 안질환의 유병률이 증가하고 있기 때문에 선진적 외과적 개입에 대한 수요가 높아지고 있으며, 생체적합성과 안과 수술에서의 사용으로 혁신적인 고분자 바이오소재의 필요성이 가속화되고 있습니다.

이 지역에서는 성형 수술 및 기타 외과 수술의 수가 증가함에 따라 환자에게 적합한 고분자 바이오소재에 대한 수요가 급증하고 조사 기간 동안 시장 성장을 이끌어 갈 것입니다.

세계의 고분자 바이오소재 산업 개요

고분자 바이오소재 시장의 경쟁은 적당하며 여러 선도 기업들로 구성되어 있습니다. 시장 점유율 측면에서 현재 소수의 대기업이 시장을 독점하고 있습니다. 그러나 기술의 진보와 제품의 혁신에 따라 중견에서 중소 기업이 시장에서의 존재감을 높이고 있습니다. BASF SE, Bezwada Biomedical LLC, Corbion NV, Zimmer Biomet, Royal DSM과 같은 기업이 상당한 시장 점유율을 차지하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 고분자 바이오소재 부문의 새로운 혁신

- 조직 공학에 있어서 고분자 바이오소재의 용도 확대

- 시장 성장 억제요인

- 고분자 바이오소재와 관련된 합병증

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자 및 소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화(시장 규모-단위 : 달러)

- 제품 유형별

- 폴리아릴에테르케톤

- 폴리글리콜산

- 폴리유산

- 폴리테트라플루오로에틸렌 및 발포 폴리테트라플루오로에틸렌

- 폴리우레탄

- 기타

- 용도별

- 신경

- 순환기

- 정형외과

- 안과

- 상처 치료

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC 국가

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 기업 프로파일

- BASF SE

- Bezwada Biomedical LLC

- Collagen Solutions LLC

- Corbion NV

- Covestro AG

- Evonik Industries AG

- DSM-Firmenich AG

- Starch Medical Inc.

- Victrex Manufacturing Limited

- WL Gore & Associates, Inc.

- Zimmer Biomet

제7장 시장 기회 및 향후 동향

AJY 25.03.31The Global Polymeric Biomaterials Market size is estimated at USD 2.22 billion in 2025, and is expected to reach USD 4.81 billion by 2030, at a CAGR of 16.71% during the forecast period (2025-2030).

The key factors propelling the market growth include innovations in polymeric biomaterials and increasing applications of polymeric biomaterials in tissue engineering. The rising number of neurological and orthopedic procedures is one of the major contributors to the market growth worldwide.

For instance, according to a report published in Parkinson's United Kingdom (UK) in February 2024, approximately 153,000 individuals in the United Kingdom are living with Parkinson's disease. With the aging population and continued growth, this figure is projected to rise by nearly 20% to 172,000 by 2030. The increasing prevalence of Parkinson's disease, driven by an aging population, is propelling the growth of the polymer biomaterials market. These materials are increasingly used in developing advanced therapeutic solutions, including drug delivery systems and neural implants.

Furthermore, widening applications of polymeric biomaterials coupled with introducing new products are expected to propel the market growth. For instance, in June 2023, International Flavors & Fragrances (IFF) introduced its groundbreaking Designed Enzymatic Biomaterials (DEB) technology, aimed at developing biobased materials that offer sustainability benefits with performance on par with or better than traditional fossil-based materials. This innovation is expected to drive growth in the polymer biomaterials market by meeting rising regulatory and consumer demands for sustainable, high-performance alternatives across diverse industries.

In conclusion, innovations in polymeric biomaterials, increasing applications, and advancements in sustainable biomaterials are propelling the growth of the polymer biomaterials market. However, complications associated with polymeric biomaterials are expected to hinder market growth.

Global Polymeric Biomaterials Market Trends

The Orthopedic Segment is Expected to Witness Significant Growth Over the Forecast Period

With the increasing number of musculoskeletal disorders (MSDs), the orthopedic segment is likely to increase as MSDs require surgical treatment. Hence, the requirement for biomaterials for such treatments is high. For instance, according to a report published by the Australian Government in June 2024, approximately 7.3 million individuals in Australia, representing 29% of the population, were estimated to be affected by chronic musculoskeletal conditions in 2023. Among them, 4.0 million experienced back issues, 3.7 million had arthritis, and 854,000 were living with osteoporosis or osteopenia. The high prevalence of chronic musculoskeletal conditions drives the demand for advanced orthopedic solutions. This increasing demand is propelling the growth of the orthopedic segment, highlighting the necessity for innovative, durable, and biocompatible materials for both therapeutic and surgical applications.

Additionally, the growing geriatric population across the globe is expected to increase the number of people suffering from orthopedic diseases, such as arthritis, osteoarthritis, and rheumatoid arthritis, as they are more prone to develop joint-related disorders due to weaker bones. For instance, according to a report published by the World Health Organization in July 2023, aging populations are leading to a significant rise in osteoarthritis cases, with over 528 million people worldwide affected, the majority being over 55 years old. The growing geriatric population, prone to the incidence of orthopedic conditions, is propelling the demand for advanced treatments, thereby driving growth in the orthopedic segment of the polymer biomaterials market through the need for more effective and durable biomaterial orthopedic solutions.

Moreover, initiatives by the key market players are another factor responsible for the segment growth. For instance, in February 2023, Invibio Biomaterial Solutions inaugurated a new orthopedic product development facility in Leeds, United Kingdom. It marked a strategic expansion to enhance its medical device research and development and manufacturing capabilities. This development strengthens Invibio's ability to support original medical device manufacturers (OEMs) in co-developing and launching advanced polyetheretherketone (PEEK) polymer implantable devices while fostering collaboration with academia and medical businesses.

In conclusion, the growing demand for polymeric biomaterials, driven by advancements in the orthopedic segment, the rising prevalence of orthopedic conditions, and expanding applications in various medical fields, is expected to propel segment growth significantly.

North America is Expected to Hold a Significant Share in the Market Over the Forecast Period

North America holds a significant market share in the polymer biomaterials market and is expected to continue its stronghold for a few more years. In the United States, several private companies have vast expertise in biopolymers with access to advanced technology and custom synthesis. Significant factors such as increasing surgical procedures such as plastic surgery and orthopedic injuries are expected to boost the market growth.

For instance, according to the International Society of Aesthetic Plastic Surgery report published in June 2024, the United States performed the most aesthetic and surgical procedures worldwide, with over 6.1 million in 2023. The high number of these procedures, particularly in plastic surgeries, is propelling the growth of the polymer biomaterials market. These materials enhance tissue compatibility, reduce infection risks, and improve overall surgical outcomes.

Similarly, the rising prevalence of eye disorders in Canada is also expected to propel the market growth. For instance, according to an article published by North Toronto Eye Care, in June 2023, 2.5 million Canadians are living with cataracts in 2023. In the country, more than 350,000 cataract surgeries are performed each year. The rising prevalence of eye disorders in Canada, such as cataracts, drives demand for advanced surgical interventions, accelerating the need for innovative polymer biomaterials due to their biocompatibility and use in ophthalmic procedures.

As the number of plastic surgeries and other surgical procedures rises in the region, the demand for more patient-compatible polymer biomaterials is set to surge, driving the market's growth during the study period.

Global Polymeric Biomaterials Industry Overview

The polymer biomaterials market is moderately competitive and consists of several major players. In terms of market share, a small number of significant players currently dominate the market. However, with technological advancements and product innovations, mid-size to smaller companies are increasing their market presence. Companies like BASF SE, Bezwada Biomedical LLC, Corbion NV, Zimmer Biomet, and Royal DSM hold a substantial market share.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 New Innovations in the Field of Polymeric Biomaterials

- 4.2.2 Increasing Applications of Polymeric Biomaterials in Tissue Engineering

- 4.3 Market Restraints

- 4.3.1 Complications Associated with Polymeric Biomaterials

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size- in USD)

- 5.1 By Product Type

- 5.1.1 Polyaryletheretherketone

- 5.1.2 Polyglycolic Acid

- 5.1.3 Polylactic Acid

- 5.1.4 Polytetrafluoroethylene & Expanded Polytetrafluoroethylene

- 5.1.5 Polyurethanes

- 5.1.6 Other Products

- 5.2 By Application

- 5.2.1 Neurology

- 5.2.2 Cardiology

- 5.2.3 Orthopedics

- 5.2.4 Ophthalmology

- 5.2.5 Wound Care

- 5.2.6 Other Applications

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 BASF SE

- 6.1.2 Bezwada Biomedical LLC

- 6.1.3 Collagen Solutions LLC

- 6.1.4 Corbion NV

- 6.1.5 Covestro AG

- 6.1.6 Evonik Industries AG

- 6.1.7 DSM-Firmenich AG

- 6.1.8 Starch Medical Inc.

- 6.1.9 Victrex Manufacturing Limited

- 6.1.10 W. L. Gore & Associates, Inc.

- 6.1.11 Zimmer Biomet