|

시장보고서

상품코드

1683221

저장 곡물용 살충제 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Stored Grain Insecticides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

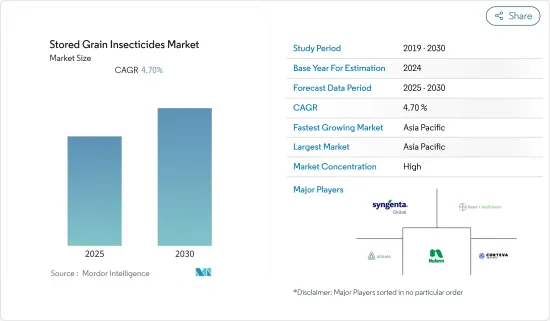

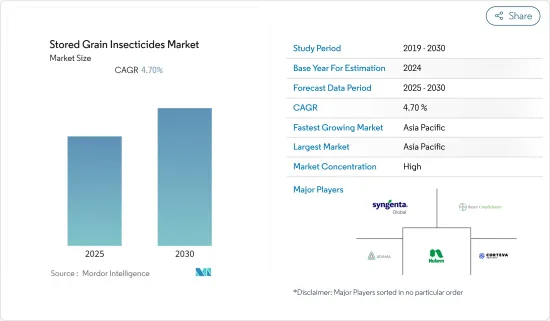

저장 곡물용 살충제 시장은 예측 기간 동안 CAGR 4.7%를 나타낼 것으로 예상됩니다.

수확 후 더 나은 가격을 요구하는 시장 압력이 지속되고 수확 후 손실 감소에 대한 관심이 높아지는 것이 시장 성장을 가속하는 주요 요인입니다. 각국의 많은 소규모 농가들은 저장시설이 부족하여 잉여 곡물을 저장할 수 없어 수확 후 손실이 증가하고 있습니다. 또한 각국 정부는 다가오는 식량 저장 위기에 대응하기 위해 점점 더 많은 노력을 기울이고 있으며, 첨단 곡물 저장 사일로 건설에 대한 기여도가 증가하고 있습니다. 이는 곤충용 곡물 보호제에 대한 수요를 증가시킬 가능성이 높습니다. 전 세계적으로 확산되고 있는 팬데믹은 공급망의 혼란으로 인해 곡물 재고와 저장량이 증가하고 있습니다. 농부들은 저장 곡물을 해충의 침입으로부터 보호하기 위해 저장 곡물용 살충제에 대한 수요를 늘리는 경향이 있습니다. 따라서 물류 분야를 제외하고 코로나19의 영향이 2021년 3분기까지 확대될 경우, 시장은 전 세계적으로 더욱 성장할 것으로 예상됩니다.

저장곡물용 살충제 시장 동향

저장 곡물 해충 - 1인당 손실

해충, 진드기, 설치류, 조류의 침입으로 인해 연간 약 13억 톤의 식용 곡물이 폐기되고 있습니다. 살충제의 사용은 사일로, 곡물 상자, 창고 내의 곤충과 해충을 방제하는 매우 효과적인 방법입니다. 유엔식량농업기구(FAO)에 따르면 수확 후 농산물의 평균 생산 손실은 선진국에서 연간 약 5%, 선진국에서 연간 약 7%, 개발도상국에서 연간 약 7%로 추정됩니다. 특히 인도, 중국 등 신흥 경제국에서는 수확 후 손실 감소에 대한 관심이 높아지고 있어 조사 기간 동안 창고용 살충제 판매를 강화할 수 있는 기회가 될 것으로 보입니다. 살충제는 무역 과정에서 필수적이며, 검역 과정에서도 중요한 역할을 합니다. 왜냐하면 몇 가지 작물, 특히 원예작물에서 유해물질을 제거하는 것은 수출 시장에서 농산물의 품질을 향상시키는 데 필수적이기 때문입니다. 이러한 경우, 살충제를 이용한 화학적 처리는 높은 효율로 작동하는 유일한 기술입니다.

아시아태평양이 시장을 독점

FAO의 보고에 따르면 인도의 온대 작물 재배 지역에서는 기온이 상승함에 따라 곤충의 활동이 활발해지고 있습니다. 이로 인해 쌀, 옥수수, 밀 등의 작물 재배에서 평균 기온이 1℃ 상승할 때마다 전국적으로 약 10-25%의 손실이 발생하고 있습니다. 인도에서 곡물 저장에 피해를 주는 가장 흔한 곤충은 벼멸구, 카프라 딱정벌레, 곡물 나방, 레서 그레인/푸드 그레인/패디 볼러(Food Grain/Paddy Borer)입니다. 이들은 쌀, 밀, 옥수수, 조, 보리, 기타 곡물에 이르기까지 많은 저장곡물에 영향을 미치고 있습니다. 이러한 곤충의 저장곡물 침입이 증가함에 따라 국내 저장곡물용 살충제 시장은 더욱 확대되고 있습니다. 그러나 IRRI의 보고서에 따르면 인도에서 저장곡물용 살충제의 과도한 사용과 오용은 쌀과 다른 곡물의 자연적 방제 메커니즘을 파괴하고 있기 때문에 FSSAI는 이러한 살충제 사용에 대한 규제 상한선을 설정하고 있습니다. 따라서 FSSAI는 이러한 살충제 사용에 대한 규제 상한선을 설정하고 있습니다. 이는 예측 기간 동안 시장 성장을 어느 정도 억제할 것으로 예상됩니다.

저장곡물용 살충제 산업 개요

저장곡물용 살충제 시장은 경쟁이 치열하고 다양한 중소기업이 세계에서 상당한 점유율을 차지하고 있습니다. 따라서 매우 치열한 경쟁이 발생하고 있습니다. 전 세계 주요 기업들의 인수합병 활동이 활발하게 진행되고 있는 것도 시장이 통합되고 있는 주요 요인 중 하나입니다. 북미와 아시아태평양은 경쟁 활동이 가장 활발한 지역입니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 성과

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 시장 성장 억제요인

- 업계의 매력 - Porter의 Five Forces 분석

- 공급 기업의 교섭력

- 바이어의 교섭력

- 신규 진출업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 세분화

- 제품 유형별

- 유기 인산염

- 피레스로이드

- 바이오 살충제

- 기타

- 용도별

- 농장 내

- 농장 외

- 수출

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 기타 북미

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 러시아

- 기타 유럽

- 아시아태평양

- 인도

- 중국

- 일본

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 기타 남미

- 아프리카

- 남아프리카공화국

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 가장 채택 된 전략

- 시장 점유율 분석

- 기업 개요

- Bayer CropScience AG

- Degesch America Inc.

- Syngenta AG

- Corteva AgriScience

- Nufarm Ltd

- Douglas Products

- Adama Agricultural Solutions Ltd.

- UPL Limited

제7장 시장 기회와 향후 동향

제8장 COVID-19의 영향 평가

LSH 25.03.27The Stored Grain Insecticides Market is expected to register a CAGR of 4.7% during the forecast period.

Sustaining market pressure for better prices during the post-harvest stage and increasing focus on the reduction of post-harvest losses are the major factors driving the market growth. Lack of storage facilities in many small scale farms across various countries led to the inability to store surplus grains resulting in increased post harvest losses. Additionally, the respective governments are increasingly focusing toward keeping pace with its looming food storage crises and has increased the contribution toward the construction of high-tech grain storage silos. This is likely to augment the demand for insect grain protectants. The prevailing pandemic across the globe has resulted in increased stocking and storage of grains due to the disruption of supply chain. In order to protect the stored grains from pest infestation, farmers tend to demand the stored grains insecticide at an increasing level. Hence apart from logistics sector, the impact of COVID-19 if extended to the third quarter of 2021,the market is further observed to grow across the globe.

Stored Grain Insecticide Market Trends

Stored grain pest- per capita loss

Owing to the infestation of pests, mites, rodents, and birds, around 1,300 million metric ton of food grains are being wasted annually. The use of insecticides is a very effective method to control insects and pests in silos, grain bins, and warehouses. According to Food and Agricultural Organization (FAO), the average production loss of the post-harvest produce is estimated to be around 5% in the developed countries, 7% in industrialized countries, and around 7% in developing countries, annually. The increasing concerns toward reducing post-harvest losses, especially from the emerging economies, such as India and China, seems to be an opportunity, which can enhance the sales of warehouse insecticides during the study period. Insecticides are mandatory for trade processes and are important for the quarantine process, as elimination of toxic substances from few crops, especially horticulture crops, is essential to increase the quality of produce in the export market. In such cases, chemical treatment with insecticides is only the technique available, which works with high efficiency.

Asia Pacific Dominates the Market

According to a report by FAO, insect activity is on the rise because of the increasing temperature in the temperate crop-growing regions of India. This, in turn, is leading to the nationwide losses in the cultivation of crops, such as rice, corn, and wheat, by about 10-25% with per degree Celsius rise in mean surface temperature. The most common insects damaging grain storages in India are the rice weevil, the khapra beetle, the grain moth, and the lesser grain/ hooded-grain/ paddy borer. These affect a host of stored grains ranging from rice, wheat, maize, jowar, barley, and other grains. The increase in infestation of stored grains by such insects is further enhancing the market for stored grain insecticides in the country. However, according to reports by IRRI, the overuse and misuse of stored grain insecticides in India is disrupting the natural control mechanisms of rice and other grains, and hence, the FSSAI has set a maximum regulatory limit to the usage of such insecticides. This is going to deter the growth of the market to some extent in the said forecast period.

Stored Grain Insecticide Industry Overview

The storage grain insecticide market is highly competitive, with various small- and medium-sized companies coining reasonable shares in the world. This has resulted in a very stiff competition. The increasing merger and acquisition activities by the major players in different parts of the world is one of the major factors for the consolidated nature of the market. North America and the Asia-Pacific are the two regions showing maximum competitor activities.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions and Market Definition

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Product Type

- 5.1.1 Organophosphate

- 5.1.2 Pyrethroids

- 5.1.3 Bio-Insecticides

- 5.1.4 Others

- 5.2 By Application type

- 5.2.1 On Farm

- 5.2.2 Off Farm

- 5.2.3 Export shipments

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Spain

- 5.3.2.5 Italy

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of South America

- 5.3.5 Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Rest of Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adapted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Bayer CropScience AG

- 6.3.2 Degesch America Inc.

- 6.3.3 Syngenta AG

- 6.3.4 Corteva AgriScience

- 6.3.5 Nufarm Ltd

- 6.3.6 Douglas Products

- 6.3.7 Adama Agricultural Solutions Ltd.

- 6.3.8 UPL Limited