|

시장보고서

상품코드

1683460

광트랜시버 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Optical Transceiver - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

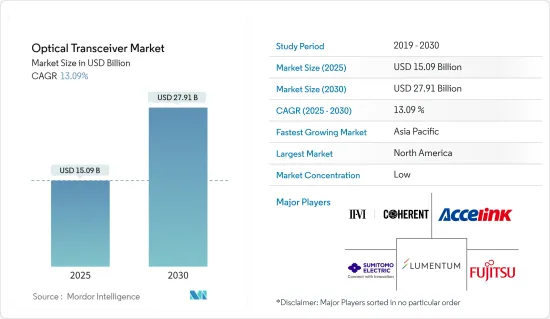

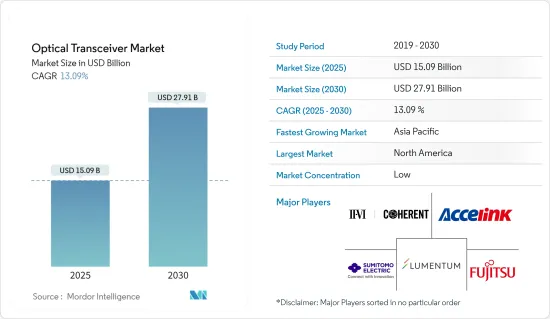

광트랜시버 시장 규모는 2025년에 150억 9,000만 달러에 달하고, 2030년에는 279억 1,000만 달러에 이를 것으로 예측되며, 시장 추정 및 예측 기간(2025-2030년)의 CAGR은 13.09%를 나타낼 것으로 예상됩니다.

광트랜시버는 광섬유 트랜시버라고도 하며, 광섬유 네트워크에서 데이터를 송수신하는 데 사용되는 상호 연결 구성요소입니다. 송신기와 수신기의 두 가지 주요 부품으로 구성됩니다. 송신기는 전기 신호를 광 신호로 변환하고 광섬유 케이블을 통해 전송합니다. 한편, 수신기는 광 신호를 수신하여 전기 신호로 변환합니다.

주요 하이라이트

- 광트랜시버는 장거리 고속 데이터 전송을 가능하게 합니다. 비디오 스트리밍, 클라우드 컴퓨팅, 데이터센터와 같은 고대역폭 용도을 지원할 수 있습니다. 광트랜시버는 신호의 상당한 열화 없이 장거리 데이터 전송이 가능합니다. 광섬유 케이블로 수 킬로미터의 데이터 전송이 필요한 통신 및 네트워킹 용도에 일반적으로 사용됩니다.

- 몇 가지 요인으로 인해 전기통신 업계는 첨단 통신에 대한 요구가 커지고 있습니다. 이러한 요인으로는 에너지 효율의 요구, 고도의 접속성 제공에 대한 주력, 사물인터넷(IoT)과 인공지능(AI) 등 신기술의 등장 등이 있습니다. 통신 사업자는 고객에게 높은 연결성과 높은 성능을 제공하기 위해 노력하고 있습니다. 여기에는 5G, 에지 컴퓨팅, 네트워크 인프라 개선 등의 기술 도입이 포함됩니다. 이러한 발전으로 보다 빠르고 안정적인 통신 서비스가 가능합니다. 베어러 네트워크의 첨단 개발과 업그레이드로 5G 기술의 발전과 기지국의 발전에 따라 광통신 네트워크 장비에 대한 수요가 증가할 것으로 예측됩니다.

- 클라우드 기반 서비스는 최근 수요가 크게 증가하고 있습니다. 클라우드 컴퓨팅은 온프레미스 서버 및 하드웨어를 필요로 하지 않아 기업의 IT 인프라 비용을 절감할 수 있습니다. 대신 기업은 온디맨드로 컴퓨팅 리소스와 서비스에 액세스할 수 있으며 사용한 만큼만 요금을 지불할 수 있습니다. 또한 클라우드 서비스는 수요에 따라 리소스를 늘리거나 줄일 수 있습니다. 그 큰 이점으로부터 클라우드 서비스의 채용이 늘어나면, 고급 통신 인프라에 대한 대규모 수요가 생겨 광트랜시버 시장을 견인하게 됩니다.

- 데이터센터와 같은 광트랜시버는 대용량 데이터 전송 네트워크에 필수적입니다. 최근, 광트랜시버의 네트워크 복잡화가 진행되고 있습니다. 최신 네트워크에서는 높은 데이터 속도가 요구되므로 1G에서 400G까지의 속도로 데이터를 전송할 수 있는 광트랜시버가 개발되었습니다. 데이터 속도가 높을수록 신뢰성이 높고 효율적인 데이터 전송을 보장하기 위해 보다 정교한 설계와 기술이 필요합니다.

- COVID-19의 발생은 데이터 이용을 증가시켰습니다. 중국에서 혁신적인 인터넷을 이용한 엔터테인먼트 서비스를 제공하는 대기업 플랫폼, Maoyan Entertainment에 의한 COVID-19의 유행이 중국의 엔터테인먼트 업계에 미친 영향에 관한 보고서에 따르면, 영화 업계는 유행에 의해 심각한 타격을 받았지만, TV나 스트리밍 플랫폼을 포함한 온라인 엔터테인먼트 시장은 호황을 누리고 있었습니다. 이는 시장의 성장으로 이어졌습니다.

광트랜시버 시장 동향

데이터센터가 광트랜시버의 급성장 용도에

- 현대 디지털 서비스의 백본 역할을 하는 데이터센터의 급증으로 효율적이고 안정적인 연결 솔루션이 필요합니다. 광트랜시버는 이러한 데이터센터 내에서 중단 없는 데이터 흐름을 유지하는 데 필요한 속도, 용량 및 확장성을 제공합니다.

- 데이터센터는 조사한 시장의 중요한 촉진요인으로 부상하고 있습니다. AI 및 고성능 컴퓨팅(HPC)과 같은 데이터 및 기술이 보급됨에 따라 데이터센터 자산을 빠르고 안정적이고 비용 효율적으로 연결할 필요성이 크게 증가하고 있습니다. 처리량, 지연, 운영 간소화, 유지 보수, 인텔리전스 및 보안은 데이터센터 공급업체에게 중요한 우선순위가 되고 있습니다.

- 데이터센터 네트워크는 광섬유 기술을 빠르게 채택하고 있습니다. 데이터센터용 광섬유 기반 네트워크는 다수의 광섬유 장비를 결합하여 구축됩니다. 이러한 대용량 네트워크에서는 광트랜시버가 중요한 역할을 합니다. 현재 최신 데이터센터 네트워크의 대부분은 대용량 데이터 전송이 필요합니다.

- 미국에 본사를 두고 있는 Inphi는 데이터센터 애플리케이션을 점점 더 목표로 삼고 있으며 실리콘 포토닉스와 DSP 기술을 활용한 400G 데이터센터 인터커넥트 광모듈 등 첨단 제품으로 시장을 확장하고 있습니다. Cloudscene에 따르면 2023년 9월 현재 미국에는 5,375개의 데이터센터가 있으며 세계 어느 나라보다 많습니다. 또한 522곳이 독일에, 517곳이 영국에 있습니다.

- 클라우드 애플리케이션, AI, 빅 데이터의 도입이 진행됨에 따라 다양한 지역에서 데이터센터 건설에 대한 수요가 증가하고 있습니다. 더 많은 조직이 운영을 클라우드로 전환함에 따라, 그들의 요구를 지원하기 위한 보다 고급 데이터센터가 필요합니다. 예를 들어, 메트로 엣지는 2023년 1월 데이터센터 시설의 설계 및 건설에 대해 크룬 건설 및 기타 건설 회사와 최종 합의했습니다. 이 프로젝트는 향후 몇 개월 이내에 완전한 권리를 취득하고 곧 착공할 예정입니다.

- Microsoft는 2023년 11월 퀘벡 주에서 클라우드 컴퓨팅과 AI 인프라를 확대하기 위해 향후 2년간 5억 달러를 투자할 것이라고 발표했습니다. 이 발표에서는 L'Ancienne-Lorette, Donnacona, Saint-Augustin-de-Desmaures 및 Levis의 미래 데이터센터 위치가 언급되어 착공예정입니다.

북미가 가장 큰 시장 점유율을 차지

- 북미는 통신환경 확대와 인터넷 보급으로 광트랜시버 시장 개척에 크게 기여하고 있는 국가 중 하나입니다. 이러한 동향은 접속성의 향상을 요구해, 북미의 광트랜시버 수요를 증대시키고 있습니다. 서비스형 소프트웨어 솔루션 기업이자 온라인 미디어 모니터링 기업인 Meltwater에 따르면 2023년 10월 현재 미국의 인터넷 보급률은 91.8%입니다.

- 미국에서는 인터넷의 보급률이 높고, AI, 5G, IoT, 고성능 컴퓨팅 등의 첨단 기술이 도입되고 있기 때문에 높은 데이터 전송 속도가 요구되고 있으며, 이것이 시장의 성장을 뒷받침하고 있습니다.

- 데이터 트래픽 증가는 기업과 소비자가 생성하는 데이터를 지원하는 많은 데이터센터를 개발하는 추가 수요를 창출하고 있습니다. 미국에서는 클라우드 컴퓨팅 서비스와 용도의 이용도 확대될 전망으로 대규모 하이퍼스케일 클라우드 기반 데이터센터의 개발로 이어지고 있습니다.

- 구글(미국), 마이크로소프트(미국), 아마존(미국) 등 주요 데이터센터 기업의 존재도 북미 광트랜시버 시장의 성장에 크게 기여하고 있습니다. Google 및 Microsoft와 같은 클라우드 서비스 제공업체는 데이터센터에 높은 데이터 속도 광트랜시버를 도입하고 있습니다.

- 데이터가 급증하고 AI 및 고성능 컴퓨팅(HPC)과 같은 기술이 확대됨에 따라 데이터센터 자산을 신속하고 안정적이고 비용 효율적으로 연결할 필요성이 크게 증가하고 있습니다. 처리량, 대기 시간, 운영 및 유지 관리 간소화, 인텔리전스 및 보안과 같은 요소는 지역 데이터센터 공급업체의 주요 우선순위가 되고 있습니다. 미국은 5G 전개에 대한 투자율이 높기 때문에 5G 시장의 주요 혁신가이자 투자자 중 하나입니다.

광트랜시버 시장 개요

광트랜시버 시장은 Coherent Corp.(II-VI Incorporated), Accelink Technologies(Accelink Technologies), Lumentum Operations LLC (Lumentum Holdings), Sumitomo Electric Industries Ltd, Fujitsu Optical Components Limited (Fujitsu Ltd) 등 있습니다. 시장 기업은 제품 라인업을 강화하고 지속 가능한 경쟁 우위를 얻기 위해 제휴 및 인수와 같은 전략을 채택하고 있습니다.

- 2023년 12월 II-VI Incorporated는 광통신 네트워크용 초소형 QSFP-DD 및 OSFP 폼 팩터인 800G ZR/ZR 트랜시버를 발표했습니다. 코히런트의 800G ZR/ZR 트랜시버는 IP 라우터의 QSFP-DD 및 OSFP 트랜시버 슬롯에 직접 연결할 수 있는 세계 최초의 디지털 코히런트 옵틱스(DCO)입니다.

- 2023년 10월 소스 포토닉스는 스코틀랜드 글래스고에서 개최된 ECOC 2023에서 AI 클러스터 연결을 위한 800Gbps 쇼트 리치 멀티 모드(MMF) 트랜시버와 액티브 케이블 제공을 발표했습니다. 이를 통해 짧은 도달범위의 광 플러그 가능 모듈과 액티브 케이블 용도을 통해 AI 데이터센터 인프라를 획기적으로 가속화할 수 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업 밸류체인 분석

- 업계의 매력도 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- COVID-19의 영향과 기타 거시 경제 요인이 시장에 미치는 영향

제5장 시장 역학

- 시장 성장 촉진요인

- 고도 통신에 대한 요구 증가

- 클라우드 기반 서비스에 대한 수요 증가

- 시장 성장 억제요인

- 네트워크의 복잡화

제6장 시장 세분화

- 프로토콜별

- 이더넷

- 파이버 채널

- CWDM/DWDM

- FTTX

- 기타 프로토콜

- 데이터 레이트별

- 10Gbps 미만

- 10Gbps-40Gbps

- 100Gbps

- 100Gbps 이상

- 용도별

- 데이터센터

- 통신

- 지역별

- 북미

- 유럽

- 아시아

- 호주 및 뉴질랜드

- 라틴아메리카

- 중동 및 아프리카

제7장 경쟁 구도

- 기업 프로파일

- Coherent Corp.(II-VI Incorporated)

- Accelink Technologies

- Lumentum Operations LLC(Lumentum Holdings)

- Sumitomo Electric Industries Ltd

- Fujitsu Optical Components Limited(Fujitsu Ltd)

- Smiths Interconnect(Reflex Photonics Inc.)

- Source Photonics(Redview Capital)

- Huawei Technologies Co. Ltd

- Broadcom Inc.

- HUBER SUHNER Cube Optics

제8장 투자 분석

제9장 시장 기회와 앞으로의 동향

SHW 25.03.28The Optical Transceiver Market size is estimated at USD 15.09 billion in 2025, and is expected to reach USD 27.91 billion by 2030, at a CAGR of 13.09% during the forecast period (2025-2030).

An optical transceiver, also known as a fiber optic transceiver, is an interconnect component used to transmit and receive data in a fiber-optic network. It consists of two main parts: a transmitter and a receiver. The transmitter converts electrical signals into light signals, which are transmitted through fiber optic cables. The receiver, on the other hand, receives light signals and converts them back into electrical signals.

Key Highlights

- Optical transceivers enable high-speed data transmission over long distances. They can support high bandwidth applications like video streaming, cloud computing, and data centers. They can transmit data over long distances without significant signal degradation. They are commonly used in telecommunications and networking applications that require data transmission over kilometers of fiber optic cables.

- Due to several factors, the telecom industry is experiencing an increasing need for advanced communication. These factors include the demand for energy efficiency, the focus on delivering advanced connectivity, and the rise of new technologies such as the Internet of Things (IoT) and artificial intelligence (AI). Telecom companies strive to deliver advanced connectivity and higher performance to their customers. This includes deploying technologies like 5G, edge computing, and improved network infrastructure. These advancements enable faster and more reliable communication services. The advanced development and upgrade of the bearer network is anticipated to drive the demand for optical communication network equipment to increase as 5G technology progresses and base stations are deployed.

- Cloud-based services have experienced a significant increase in demand in recent years. Cloud computing allows businesses to reduce their IT infrastructure costs by eliminating the need for on-premises servers and hardware. Instead, companies can access computing resources and services on demand, paying only for what they use. Cloud services also offer the ability to scale resources up or down based on demand. The increasing adoption of cloud services owing to their significant advantages would create massive demand for advanced communication infrastructure, thereby driving the optical transceivers market.

- Optical transceivers, such as data centers, are critical in high-capacity data transmission networks. In recent years, there has been an increase in network complexity in optical transceivers. The demand for high data rates in modern networks has led to the development of optical transceivers capable of transmitting data at speeds ranging from 1G to 400 G. The higher data rates require more sophisticated designs and technologies to ensure reliable and efficient data transmission.

- The outbreak of COVID-19 increased the usage of data. According to a report on the impact of the COVID-19 pandemic on China's entertainment industry by Maoyan Entertainment, a leading platform providing innovative Internet-empowered entertainment services in China, the movie industry was severely hit by the pandemic, whereas the online entertainment market, including TV and streaming platforms, were booming as people were confined to their homes. This has led to the growth of the market.

Optical Transceiver Market Trends

Data Centers to the Fastest Growing Application for Optical Transceivers

- The proliferation of data centers, which serve as the backbone of modern digital services, requires efficient and reliable connectivity solutions. Optical transceivers offer the speed, capacity, and scalability required to maintain the uninterrupted data flow within these data centers.

- Data centers are emerging as significant drivers in the market studied. With the proliferation of data and technologies, like AI and high-performance computing (HPC), the need to connect data center assets quickly, reliably, and cost-effectively is growing significantly. Throughput, latency, simplified operations, maintenance, intelligence, and security are becoming significant priorities for data center vendors.

- Data center networks are rapidly adopting fiber optics technology. A fiber-based network for data centers is built by combining many fiber optic devices. In these high-capacity networks, optical transceivers play a significant role. The majority of modern data center networks currently necessitate high-capacity data transmission.

- US-based Inphi is increasingly targeting data center applications and extending its marketplace with advanced products, including 400G data center interconnect optical modules, which leverage their silicon photonics and DSP technologies. According to Cloudscene, as of September 2023, there were 5,375 data centers in the United States, the most of any country worldwide. A further 522 were in Germany, while 517 were in the United Kingdom.

- The growing adoption of cloud applications, AI, and big data drives the demand for data center construction across various regions. As more organizations shift their operations to the cloud, they require more advanced data centers to support their needs. For instance, in January 2023, Metro Edge finalized agreements with Clune Construction and other construction firms to design and build the data center facility. The project is expected to have full entitlements within the next few months and break ground shortly after.

- In November 2023, Microsoft announced it would invest USD 500 million in expanding its cloud computing and AI infrastructure in Quebec over the next two years. The announcement references future data center locations in L'Ancienne-Lorette, Donnacona, Saint-Augustin-de-Desmaures, and Levis, with construction starting soon.

North America Holds Largest Market Share

- North America is one of the significant contributors to the optical transceiver market's development due to the growing communication landscape and the massive internet penetration. These trends demand improved connectivity, increasing the demand for optical transceivers in North America. According to Meltwater, a software-as-a-service solution company and an online media monitoring company, as of October 2023, the internet penetration rate as of October 2023 in the United States was 91.8%.

- The high adoption of the Internet and advanced technologies like AI, 5G, IoT, and high-performance computing in the United States is driving the need for a high data transmission rate, which drives the market's growth.

- Increasing data traffic has created additional demand for developing many data centers that support data generated by businesses and consumers. The use of cloud-computing services and applications is also expected to grow in the United States, leading to the development of large hyperscale cloud-based data centers.

- The presence of some of the key data center companies like Google (US), Microsoft (US), and Amazon (US) has also contributed significantly to the growth of the optical transceiver market in North America. Cloud service providers like Google and Microsoft are implementing high-data-rate optical transceivers in their data centers.

- With the proliferation of data and expansion of technologies like AI and high-performance computing (HPC), the need to connect data center assets quickly, reliably, and cost-effectively is growing significantly. Factors such as throughput, latency, simplified operations and maintenance, intelligence, and security are becoming major priorities for regional data center vendors. The United States is one of the major innovators and investors in the 5G market, owing to a high investment rate for 5G deployment.

Optical Transceiver Market Overview

The optical transceiver market is highly fragmented, with the presence of major players like Coherent Corp. (II-VI Incorporated), Accelink Technologies, Lumentum Operations LLC (Lumentum Holdings), Sumitomo Electric Industries Ltd, and Fujitsu Optical Components Limited (Fujitsu Ltd). Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- December 2023: II-VI Incorporated introduced its 800G ZR/ZR+ transceiver in ultracompact QSFP-DD and OSFP form factors for optical communications networks. The 800G ZR/ZR+ transceivers from Coherent are the world's first digital coherent optics (DCO) that can plug directly into QSFP-DD and OSFP transceiver slots on IP routers.

- October 2023: Source Photonics announced the availability of 800 Gbps short-reach multimode (MMF) transceivers and active cables for AI cluster connectivity at ECOC 2023 in Glasgow, Scotland, that enables AI data center infrastructure to achieve dramatically higher speeds for short-reach optical pluggable modules and active cable applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Need for Advanced Communication

- 5.1.2 Increasing Demand for Cloud-based Services

- 5.2 Market Restraints

- 5.2.1 Increase in Network Complexity

6 MARKET SEGMENTATION

- 6.1 By Protocol

- 6.1.1 Ethernet

- 6.1.2 Fiber Channel

- 6.1.3 CWDM/DWDM

- 6.1.4 FTTX

- 6.1.5 Other Protocols

- 6.2 By Data Rate

- 6.2.1 Less than 10 Gbps

- 6.2.2 10 Gbps to 40 Gbps

- 6.2.3 100 Gbps

- 6.2.4 Greater than 100 Gbps

- 6.3 By Application

- 6.3.1 Data Center

- 6.3.2 Telecommunication

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Coherent Corp. (II-VI Incorporated)

- 7.1.2 Accelink Technologies

- 7.1.3 Lumentum Operations LLC (Lumentum Holdings)

- 7.1.4 Sumitomo Electric Industries Ltd

- 7.1.5 Fujitsu Optical Components Limited (Fujitsu Ltd)

- 7.1.6 Smiths Interconnect (Reflex Photonics Inc.)

- 7.1.7 Source Photonics (Redview Capital)

- 7.1.8 Huawei Technologies Co. Ltd

- 7.1.9 Broadcom Inc.

- 7.1.10 HUBER+SUHNER Cube Optics