|

시장보고서

상품코드

1683488

전신 마취제 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Global General Anesthesia Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

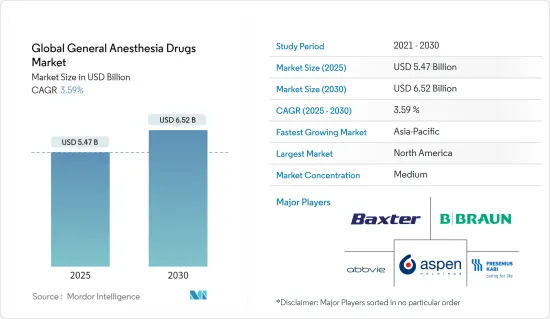

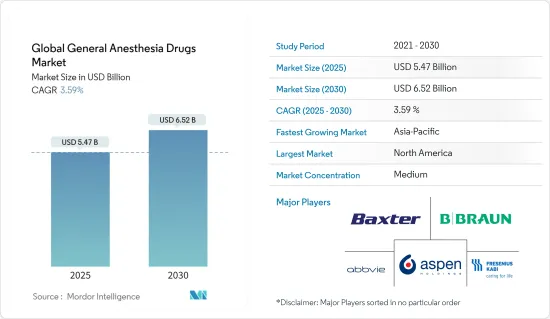

세계의 전신 마취제 시장 규모는 2025년에 54억 7,000만 달러로 추계되어 예측 기간(2025-2030년)의 CAGR은 3.59%로, 2030년에는 65억 2,000만 달러에 달할 것으로 예측되고 있습니다.

전신 마취의 주요 목표는 수술 과정에서 환자의 의식을 잃게 하고 통증을 느끼지 않게 하는 것입니다. 암, 심혈관 질환, 관절염 등과 같은 질병의 유병률이 증가함에 따라 약물, 물리 치료 및 수술을 통한 효과적인 질병 관리의 필요성이 높아지고 있으며, 이는 수술 중 자율 반사를 제어하면서 환자의 의식을 잃고 고통스러운 자극을 느끼지 못하게 하는 전신 마취제에 대한 수요를 촉진하고 있습니다.

인구의 암 부담이 증가함에 따라 영향을받는 암세포와 림프절을 제거하는 외과 적 개입을 통한 치료에 대한 수요가 증가합니다. 따라서 이러한 절차에 사용되는 전신 마취제의 시장 성장은 예측 기간 동안 증가 할 것으로 예상됩니다. 예를 들어, 미국 암 협회가 발표한 2024년 통계에 따르면 2024년 미국에서 약 200만 건의 새로운 암 사례가 진단될 것으로 예상되는데, 이는 2023년의 192만 건에 비해 크게 증가한 수치입니다.

게다가, 전미 성인 심장 수술 감사 보고 2023에 의하면, 2022년의 성인 심장 수술 건수는 24,807건이었지만, 2021년은 19,333건이었습니다. 이것은 예측 기간 동안 이러한 수술에 사용되는 전신 마취제 수요를 촉진할 것으로 예상됩니다. 게다가 세계보건기구(WHO)에 따르면 2022년에는 2030년까지 세계 6명 중 1명이 60세가 되었고, 2050년까지 60세 이상의 세계 인구는 21억명으로 두배로 늘어난다고 합니다. 따라서 노인 인구가 다양한 만성 질환에 걸리기 쉬워지고 수술이 증가함에 따라 전신 마취제의 요구가 커지고 예측 기간 동안 시장 성장으로 이어집니다.

또한 미국 식품의 약국 (FDA), 브라질 보건 규제 기관 (ANVISA), 유럽 의약품 국 (EMA), 치료 용품 국 (TGA)과 같은 규제 기관의 고급 전신 마취 제품 출시 및 파이프 라인 제품 승인이 증가하여 예측 기간 동안 시장 성장을 촉진 할 것으로 예상됩니다. 예를 들어, 2022년 10월, Hikma는 전신 마취를 위해 병원에서 기관 삽관을 용이하게 하고 수술 또는 기계 환기 중 근육 이완을 제공하는 데 사용되는 중요한 의약품인 숙시닐콜린 클로라이드를 미국에서 프리필드 주사기 형태의 주사제 형태로 출시했습니다.

따라서 만성 질환에 대한 수술 건수 증가와 같은 요인은 전신 마취제에 대한 수요를 증가시켜 예측 기간 동안 시장의 성장을 주도합니다. 그러나 소아 환자 및 임산부의 전신 마취와 관련된 위험은 시장 성장을 저해 할 수 있습니다.

전신 마취제 시장 동향

프로포폴 부문은 예측 기간 동안 주목할만한 성장을 보일 것으로 예상

프로포폴은 전신 마취의 유도 및 유지에 사용되는 정맥 마취제입니다. 프로포폴의 정맥 (IV) 투여는 무의식을 유도하는 데 사용되며, 그 후 약물의 조합을 사용하여 마취를 유지할 수 있습니다. 프로포폴은 마취의 유도 유지와 난치성 간질 상태의 관리에 사용됩니다. 이 약물은 마취가 필요한 다양한 수술 절차에 항상 사용되어 왔습니다.

약물은 마취가 필요한 다양한 수술 절차에 항상 사용되어 왔습니다. 응급 수술의 발생률 증가, 노인 인구 증가, 약물의 광범위한 사용, 단기 작용 특성 및 전 세계적으로 증가하는 수술 절차가이 부문의 성장을 촉진하는 주요 요인입니다. 예를 들어, 세계보건기구 2023 보고서에 따르면 외상성 부상, 암, 심혈관 질환의 발생률이 계속 증가하고 있으며 외과적 개입이 공중 보건 시스템에 미치는 영향은 전 세계적으로 계속 증가할 수 있습니다. 수술은 장애를 완화하고 일반적인 질환으로 인한 사망 위험을 줄일 수 있는 유일한 치료법입니다. 매년 많은 사람들이 외과적 치료를 받고 있으며, 수술적 개입은 세계의 장애조정 생존연수의 13%를 차지할 것으로 추정됩니다. 예를 들어 미국 질병통제예방센터의 2023년 11월 업데이트에 따르면 지난 2년간 미국에서 의도하지 않은 부상으로 인해 응급실을 방문한 건수는 약 2,500만 건에 달했습니다. 같은 자료에 따르면 2023년 마지막 3개월 동안 활동 제한 부상을 입은 18세 이상 성인의 비율은 5.9%였습니다. 따라서 부상 및 관련 수술의 증가는 프로포폴의 채택을 강화하여 예측 기간 동안 이 부분의 성장으로 이어질 것으로 예상됩니다.

또한 주요 시장 기업와 제품 출시 및 협업과 같은 전략적 활동은 예측 기간 동안 세그먼트의 성장에 유리할 것으로 예상됩니다. 예를 들어, 2022년 8월, 급성 및 중환자 치료 의약품 혁신에 주력하는 제약 회사 인 Genixus는 연례 전국 약국 구매 협회 컨퍼런스에서 RTA 주사기 제품의 KinetiX 플랫폼 내 첫 번째 제품으로 프로포폴을 제공한다고보고했습니다. 새로운 프로포폴 실린지는 워크플로우를 간소화하고 효과적인 치료 제공을 지원하기 위해 설계된 Kinetix RTA 플랫폼에서 사용할 수 있는 첫 번째 제품 중 하나입니다. 이와 마찬가지로, 2022년 4월에는 미국 식품의약국(FDA)의 약식 신약 신청 승인을 받은 디프리반(프로포폴) 주사용 에멀젼 USP의 AB 등급 제네릭 제품인 프로포폴 주사용 에멀젼, USP 10 mg/mL(20, 50 및 100ml 단일 환자 사용 바이알)을 출시했습니다.

따라서 프로포폴의 이점, 새로운 개발 및 외과적 개입의 필요성으로 인해이 부문은 예측 기간 동안 상당한 성장을 목격 할 것으로 예상됩니다.

북미는 예측기간 중 상당한 성장이 예상

북미는 지역의 만성 질환 위험 증가와 유리한 의료 인프라로 인해 예측 기간 동안 상당한 성장을 목격 할 것으로 예상됩니다. 또한 고령화 인구의 증가와 수술에 대한 수요도 북미 시장의 성장에 기여하고 있습니다.

예를 들어, 심혈관 질환의 위험 증가는 환자를 치료하기 위한 다양한 전신 마취제의 필요성을 증가시킵니다. 미국 질병 예방 관리 센터(Centers for Disease Control and Prevention)에 따르면, 2022년에는 미국에서는 매년 약 80만 5,000명이 심장 발작을 일으키며, 그 중 60만 5,000명이 최초의 심장 발작을 일으키고, 약 20만명이 이미 심장 발작을 일으키고 있다고 발표했습니다. 따라서 이러한 요인이 시장의 성장을 높이고 있습니다. 또한 전신 마취는 무릎 교체술이나 개심술과 같은 주요 수술에 일반적으로 사용됩니다. 예를 들어, 2023년 8월 미국 국립의학도서관에 발표된 논문 업데이트에 따르면 매년 약 40만 건의 관상동맥우회술(CABG) 수술이 시행되고 있으며, 이는 미국에서 가장 많이 시행되는 주요 수술입니다. 따라서 미국 전역에서 심장 수술 절차의 높은 유병률은 전신 마취제에 대한 수요를 창출하여 예측 기간 동안 시장의 성장을 촉진 할 수 있습니다.

게다가 인구통계학적 전망(CBO)이 발표한 인구 통계 전망에 따르면 2024년에는 25-64세 인구와 65세 이상 인구의 비율이 2.9대 1이 될 것으로 CBO는 예상합니다. 2054년에는 2.2대 1이 될 것으로 예상됩니다. 고령 인구의 증가로 인해 심혈관 및 신경 질환과 같은 노년층의 만성 질환이 급격히 증가하면서 마취제에 대한 수요가 증가했습니다.

또한, 전신 마취제에 대한 제품 출시, 규제 승인 및 임상 시험 연구의 증가는 예측 기간 동안 미국 시장의 성장을 더욱 촉진 할 것으로 예상됩니다.예를 들어, 2022년 4월 세다나 메디컬은 미국에서 중환자실(ICU)에서 기계식 인공호흡기 환자의 진정을 위해 정맥 프로포폴과 세다콘다 ACD-S 장치 시스템을 통해 투여된 흡입 이소플루란의 안전성과 효능을 비교하기 위한 임상 시험을 실시했습니다. 따라서 이러한 결과와 전신 마취제가 제공하는 추가 혜택은 북미에서 채택을 증가시켜 예측 기간 동안 시장 성장으로 이어질 것입니다.

따라서 수술 절차의 증가, 마취제의 효능을 입증하기위한 임상 연구의 증가, 제품 출시와 같은 전략적 활동과 결합 된 주요 시장 기업의 존재로 인해 시장은 북미에서 주목할만한 성장을 목격 할 것으로 예상됩니다.

전신 마취제 산업 개요

전신 마취제 시장은 여러 주요 시장 기업의 존재로 인해 본질적으로 반 통합되어 있습니다. 시장 기업은 전 세계적으로 제품 포트폴리오를 개선하기 위해 합병, 인수, 제품 출시, R&D 활동 등 다양한 전략적 활동을 지속적으로 추진하고 있습니다. 시장의 주요 기업은 AbbVie Inc., Paion AG, Aspen Holdings, Baxter International Inc., Fresenius SE & Co.KGaA 등입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 수술 건수 증가

- 신약 승인 및 출시

- 시장 성장 억제요인

- 전신 마취제의 부작용

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자, 소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 약제 유형별

- 세보플루란

- 데스플루란

- 이소플루란

- 아산화질소

- 프로포폴

- 기타 약

- 투여 경로별

- 흡입

- 정맥내 투여

- 수술 유형별

- 일반 외과

- 암 수술

- 심장 수술

- 인공 슬관절 치환술

- 기타 수술

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 기업 프로파일

- Aspen Holdings

- Paion AG

- AbbVie Inc.

- Endo International plc(Par Pharmaceutical Inc.)

- Baxter International Inc.

- Safeline pharmaceuticals

- Fresenius SE & Co. KGaA

- Hikma Pharmaceuticals plc

- Pfizer Inc.

- Piramal Critical Care

- AVET Pharmaceuticals Inc.

제7장 시장 기회와 앞으로의 동향

HBR 25.04.01The Global General Anesthesia Drugs Market size is estimated at USD 5.47 billion in 2025, and is expected to reach USD 6.52 billion by 2030, at a CAGR of 3.59% during the forecast period (2025-2030).

The primary goal of general anesthesia is to make a patient unconscious and not feel pain during the surgical procedure. The increasing prevalence of diseases such as cancer, cardiovascular diseases, arthritis, and others among the population raises the need for effective management of the disease through pharmaceuticals, physical therapy, and surgeries, which in turn fuel the demand for general anesthesia drugs to render a patient unconscious and unable to feel painful stimuli while controlling autonomic reflexes during surgeries.

The increasing burden of cancer among the population raises the demand for treatment through a surgical intervention that involves removing cancer cells and lymph nodes that are affected. Hence, the market growth of general anesthesia drugs used in such procedures is anticipated to augment over the forecast period. For instance, according to 2024 statistics published by the American Cancer Society, about 2 million new cancer cases are expected to be diagnosed in the United States in 2024, compared to 1.92 million new cancer cases in 2023.

Furthermore, according to the National Adult Cardiac Surgery Audit Report 2023, the number of adult heart operations in 2022 was 24,807 compared to 19,333 in 2021. This, in turn, is expected to fuel the demand for general anesthesia drugs used in such procedures over the forecast period. Moreover, according to the World Health Organization, in 2022, it was mentioned that by 2030, one in six people in the world would be aged 60 years, and by 2050, the world's population of people aged 60 years and older would double to 2.1 billion. Therefore, as the senior population is more prone to various chronic diseases and further surgeries, the need for general anesthesia drugs elevates, leading to market growth over the forecast period.

Moreover, increase in advanced general anesthesia product launches and the approvals of pipeline products by regulatory agencies such as the US Food and Drug Administration (FDA), Brazilian Health Regulatory Agency (ANVISA), European Medicines Agency (EMA), Therapeutic Goods Administration (TGA) among others, are expected to fuel the market's growth over the forecast period. For instance, in October 2022, Hikma launched Succinylcholine Chloride, an important medicine used in hospitals for general anesthesia, to facilitate tracheal intubation, and to provide muscle relaxation during surgery or mechanical ventilation in the form of an injection in a prefilled syringe form in the United States.

Therefore, factors such as the rising number of surgeries for chronic diseases raise the demand for general anesthesia drugs, driving the market's growth during the forecast period. However, risks associated with general anesthesia in pediatric patients and pregnant women may likely impede market growth.

General Anesthesia Drugs Market Trends

Propofol Segment is Expected to Witness a Notable Growth Over the Forecast Period

Propofol is an intravenous anesthetic agent used for the induction and maintenance of general anesthesia. Intravenous (IV) administration of Propofol is used to induce unconsciousness, after which anesthesia may be maintained using a combination of medications. Propofol is used for the induction maintenance of anesthesia and the management of refractory status epilepticus. The drug has always been used for various surgical procedures requiring anesthesia.

The increasing incidences of emergency surgeries, a growing senior population, extensive usage of the drug, short-acting characteristics, and a growing number of surgical procedures worldwide are the major factors propelling the segment's growth. For instance, as per the World Health Organization 2023 report, the incidences of traumatic injuries, cancers, and cardiovascular disease continue to rise, and the impact of surgical intervention on public health systems may continue to grow globally. Surgery is the only therapy that can alleviate disabilities and reduce the risk of death from common conditions. Each year, many people undergo surgical treatment, and surgical interventions account for an estimated 13% of the world's total disability-adjusted life years. For instance, as per the November 2023 update by the Centers for Disease Control and Prevention, about 25 million emergency department visits for unintentional injuries were reported in the United States in the past two years. As per the same source, the share of adults age 18 and older who had an activity-limiting injury during the last three months of 2023 was 5.9%. Hence, an increase in cases of injuries and related surgeries is expected to bolster the adoption of Propofol, leading to segment growth over the forecast period.

Furthermore, key market players and their strategic activities, such as product launches and collaborations, are expected to favor the segment's growth over the forecast period. For instance, in August 2022, Genixus, a pharmaceutical company focused on transforming acute and critical care medicines, reported offering Propofol as the first product within its KinetiX platform of RTA syringe products at the Annual National Pharmacy Purchasing Association Conference. The new Propofol Syringe is one of the first products available within the Kinetix RTA platform, designed to simplify workflow and support effective care delivery. Similarly, in April 2022, Avet Pharmaceuticals Inc. launched its Propofol Injectable Emulsion, USP 10 mg/mL, in 20, 50, and 100-ml Single Patient-Use Vials, an AB-rated generic equivalent of DIPRIVAN (Propofol) Injectable Emulsion USP, following its abbreviated new drug application approval from the Food and Drug Administration (FDA).

Hence, owing to the benefits of Propofol, the new developments, and the need for surgical interventions, the segment is believed to witness considerable growth during the forecast period.

North America is Expected to Witness a Significant Growth Over the Forecast Period

North America is expected to witness significant growth over the forecast period due to the region's increased risk of chronic diseases and favorable healthcare infrastructure. Furthermore, an increase in the aging population, along with the demand for surgical procedures, also contributes to the growth of the market in North America.

For instance, the increased risk of cardiovascular diseases is elevating the need for various general anesthesia drugs to treat patients. According to the Centers for Disease Control and Prevention, in 2022, it was stated that every year, around 805,000 people in the United States have a heart attack, out of which 605,000 have a first heart attack and about 200,000 people have already had a heart attack have a second attack. Hence, this factor is elevating the growth of the market. Additionally, general anesthesia is commonly used for major operations, such as knee replacement or open-heart surgery. For instance, according to the article update published in August 2023 in the National Library of Medicine, approximately 400,000 coronary artery bypass grafting (CABG) surgeries are performed yearly, making it the most performed major surgical procedure in the United States. Thus, a high prevalence of cardiac surgery procedures across the United States may create a demand for general anesthetic drugs, fueling the market's growth over the forecast period.

Moreover, according to the Demographic Outlook: 2024 to 2054 published by the Congressional Budget Office (CBO), in 2024, the ratio of people aged 25 to 64 to 65 or older maybe 2.9 to 1, CBO projects. By 2054, it may be 2.2 to 1. Growth in the aged population resulted in a sharp increase in the number of chronic conditions among older people, such as cardiovascular and neurological ailments, driving up demand for anesthetic medicines.

Furthermore, increased product launches, regulatory approvals, and clinical trial studies for general anesthetic drugs are further expected to fuel the US market's growth over the forecast period. For instance, in April 2022, Sedana Medical conducted a clinical trial in the United States to compare the safety and efficacy of inhaled isoflurane administered via the Sedaconda ACD-S device system versus intravenous propofol for sedation of mechanically ventilated patients in the Intensive Care Unit (ICU). Hence, such results and further benefits offered by general anesthetic drugs will likely increase their adoption in North America, leading to market growth over the forecast period.

Hence, due to the increase in surgical procedures, the rise in clinical studies to demonstrate the efficacy of anesthesia drugs, and the presence of major market players coupled with their strategic activities, such as product launches, the market is expected to witness notable growth in North America.

General Anesthesia Drugs Industry Overview

The general anesthesia drugs market is semi-consolidated in nature due to the presence of several key market players. The market players are continuously involved in various strategic activities such as mergers, acquisitions, product launches, and research and development activities to improve their product portfolio across the globe. Some of the key players in the market include AbbVie Inc., Paion AG, Aspen Holdings, Baxter International Inc., and Fresenius SE & Co. KGaA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Number of Surgeries

- 4.2.2 New Drug Approvals and Launches

- 4.3 Market Restraints

- 4.3.1 Side Effects of General Anesthetics

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Type of Drugs

- 5.1.1 Sevoflurane

- 5.1.2 Desflurane

- 5.1.3 Isoflurane

- 5.1.4 Nitrous Oxide

- 5.1.5 Propofol

- 5.1.6 Other Drugs

- 5.2 By Route of Administration

- 5.2.1 Inhalation

- 5.2.2 Intravenous

- 5.3 By Surgery Type

- 5.3.1 General Surgery

- 5.3.2 Cancer Surgery

- 5.3.3 Heart Surgery

- 5.3.4 Knee and Hip Replacements

- 5.3.5 Other Surgery Types

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Other End Users

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Aspen Holdings

- 6.1.2 Paion AG

- 6.1.3 AbbVie Inc.

- 6.1.4 Endo International plc (Par Pharmaceutical Inc.)

- 6.1.5 Baxter International Inc.

- 6.1.6 Safeline pharmaceuticals

- 6.1.7 Fresenius SE & Co. KGaA

- 6.1.8 Hikma Pharmaceuticals plc

- 6.1.9 Pfizer Inc.

- 6.1.10 Piramal Critical Care

- 6.1.11 AVET Pharmaceuticals Inc.