|

시장보고서

상품코드

1683533

유럽의 목재 펠릿 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Europe Wood Pellet - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

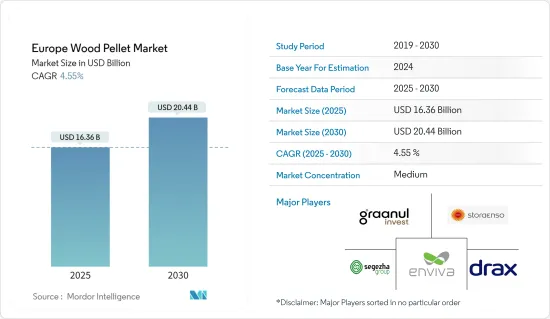

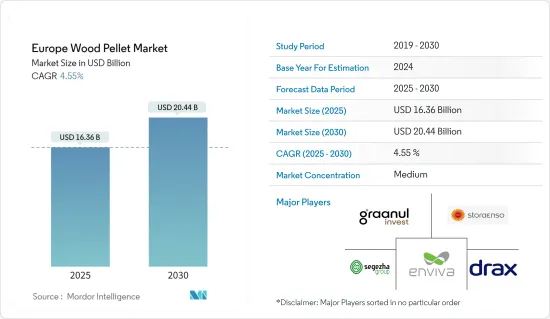

유럽의 목재 펠릿 시장 규모는 2025년에 163억 6,000만 달러로 추정되고, 예측 기간 2025년부터 2030년까지 CAGR 4.55%로 성장할 전망이며, 2030년에는 204억 4,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

- 중기적으로는 청정 에너지 발전과 열공급 용도 분야에서 목재 펠릿 수요 증가가 유럽의 목재 펠릿 시장을 견인할 것으로 보입니다.

- 한편, 대체 청정 에너지와의 경쟁 격화 및 목재 펠릿에 대한 정부의 지원 제도 종료가 예측 기간 중 시장 성장의 방해가 될 가능성이 높습니다.

- 그럼에도 불구하고 새로운 용도의 출현과 목재 펠렛 기술의 발전이 미래 시장 성장을 뒷받침할 것으로 예상됩니다.

- 다양한 용도로 목재 펠릿의 채택이 증가함에 따라 영국은 유럽의 목재 펠릿 시장을 독점할 것으로 예상됩니다.

유럽의 목재 펠렛 시장 동향

난방 용도 부문이 시장을 독점할 전망

- 난방 용도의 목재 펠릿은 주로 주거 및 상업 분야에서 식품, 요리, 그릴 및 주택에 열을 공급하는 데 사용됩니다. 이 목재 펠렛은 연결된 파이프, 보일러 및 난방 라디에이터와 함께 가정에서 난방 시스템을 구축하는 데 사용됩니다. 난방용으로는 펠렛 중앙 난방 보일러, 펠릿 스토브, 펠릿 중앙 난방 스토브 등이 있습니다.

- 유럽의 목재 펠릿 시장의 난방 용도 부문은 특히 독일과 프랑스에서 목재 펠릿의 소비가 증가하고 있기 때문에 큰 수요를 창출할 것으로 기대됩니다. 유럽은 세계에서 가장 큰 목재 펠렛 시장입니다. 2022년 이 지역의 총 목재 팔레트 소비량은 2,480만 톤(MMT)을 차지했습니다. 유럽위원회(EC)의 지침과 EU 회원국(MS)의 장려책에 따르면 2023년 수요는 2,560만 톤으로 더욱 확대될 것으로 예상됩니다.

- 주택 난방을 위한 목재 펠릿 수요 증가는 향후 시장 성장을 가속할 것으로 예상됩니다. 주거용으로는 가정용 스토브와 용량 50kW 미만의 난방 전용 보일러가 포함됩니다. 용량이 50kW를 초과하는 중소규모 업무용으로는 주택 및 공공시설에서 사용되는 열 보일러가 포함됩니다.

- 목재 펠렛은 바이오 매스 보일러와 전용 펠릿 연소 스토브로 가정용 난방 연료로 사용할 수 있습니다. 펠렛 스토브는 기존의 장작 스토브보다 연기와 그을음이 적고 깨끗하게 연소하기 때문에 뛰어납니다. 목재 펠릿은 밀도가 높고 수분 함량이 낮기 때문에(10% 이하) 스토브에서 매우 높은 연소 온도에서 연소할 수 있어 효율도 향상하고 회분도 기존 장작보다 훨씬 적습니다(2% 이하).

- 난방에 목재 펠릿을 사용하는 것은 전기 요금을 줄이는 대안입니다. 유럽 소비자들은 연료비가 상승함에 따라 대체 난방 방법을 찾고 있습니다.

- 스토브 산업 연맹에 따르면, 장작은 가정용 난방 연료 중에서 가장 저렴하며, 1kWh 당 비용은 전기 난방보다 74%, 가스 난방보다 21% 저렴합니다. 이러한 목재 펠릿의 장점은 예측 기간 동안 난방 용도 분야에 대한 수요가 증가할 것으로 예상됩니다.

- 독일, 이탈리아, 프랑스, 덴마크, 스웨덴은 난방 목적으로 목재 펠렛을 사용하는 주요 국가입니다. EPC 조사 2023에 따르면 2022년 난방용으로 목재 펠릿을 가장 많이 사용한 것은 독일에서 320만 톤을 차지했습니다.

- 독일과 이탈리아에서는 목재 펠렛에 의한 열 발생의 70% 이상이 주택 난방에 사용되었으며, 덴마크와 스웨덴에서는 펠릿이 주로 CHP 열에 사용되었습니다. 기후는 목재 펠릿 소비에 중요한 역할을 합니다. 유럽 국가의 기후는 미래에 추워질 것으로 예상되므로 예측 기간 동안 난방 목적으로 펠렛 사용이 증가할 것으로 예상됩니다.

- 따라서 예측 기간 동안 난방 분야는 시장을 독점할 것으로 예상됩니다.

영국이 시장을 독점할 전망

- 영국에서는 주택 난방, 발전소, 상업 난방, 열전 병급 플랜트 등 다양한 용도로 펠릿이 사용됩니다. 펠렛은 또한 학교와 사무실과 같은 지방 자치 단체 건물과 행정 기관 건물에서 석탄 전환 프로젝트에 진출하고 있습니다.

- 2024년 현재 혼소 발전소의 대부분은 폐쇄되거나 전환되었으며, 일부 발전소는 연료에 목재 펠릿을 100% 사용하는 방향으로 이동하고 있습니다. 그 중 가장 큰 것은 노스 요크셔에 있는 드럭스 발전소입니다. 65MWe의 발전 유닛 6기 중 4기를 목재 펠릿으로만 전환했습니다.

- 드럭스 발전소는 국내 최대의 발전소로, 2023년에는 영국 전체의 약 5%의 전력을 생산합니다. 또한 세계 최대의 바이오매스 화력발전소이기도 하며 매년 약 650만 톤(MT)의 펠릿을 받아들여, 이 나라의 연간 펠릿 수입량의 대부분을 차지하고 있습니다. 이 회사는 미국과 캐나다에도 17개의 펠렛 공장을 보유하고 있으며 발전소에 원료를 공급하고 있습니다.

- 그러나 영국 정부에 따르면 이 나라가 2023년에 수입한 목재 펠렛은 600만 톤으로, 2022년에는 752만 톤, 2021년에는 913만 톤이었습니다.

- 유엔 식량농업기관에 따르면 2022년 이 나라의 목재 펠릿 생산량은 약 32만 6,000톤이었습니다. 목재 펠렛의 생산량은 전년 대비 약 7.2%의 상당한 성장을 보였습니다.

- 영국 정부는 2035년까지 탄소 회수, 이용 및 저류(CCUS) 경쟁 시장을 개척할 계획을 내세우고, 2023년 12월 탄소 회수 및 저류를 수반하는 바이오에너지(BECCS)를 지원하는 CfD 프로그램을 확대할 계획을 발표했습니다. 이 계획은 2050년까지 영국 경제를 연간 50억 유로 밀어 올리고, 이 기술을 개척하는 국가를 기대하고 있습니다.

- 드럭스는 운영 자금으로 연간 수억 파운드의 보조금을 받고 있습니다. 2027년 영국 정부는 미연소 바이오매스 발전에 대한 지원을 중단할 예정입니다.

- 2027년 이후에 보조금이 중단되는 것을 막기 위해, 드럭스사는 목재 연소 사업에 대한 새로운 장기 보조금의 확보를 목표로 하고 있습니다. 이 회사는 계획 중인 BECCS(Bioenergy with Carbon Capture) 프로젝트를 통해 이를 달성하는 것을 목표로 하고 있습니다. 이 프로젝트는 처음에는 기존 발전 능력의 절반에 탄소 회수 저류(CCS)를 추가할 것을 제안했으며, 회사는 연간 8톤의 부정적인 배출을 창출한다고 했습니다. 목표는 전체 발전 용량에 CCS를 추가하는 것입니다.

- 2024년 1월, CfD 프로그램의 연장에 따라 영국 정부는 드럭스 발전소에 탄소 회수 기술의 도입 계획을 승인했습니다. 이 발전소에서는 목재 펠릿을 태우고 발전하는 4기의 바이오매스 유닛 중 2기로의 도입이 허가됩니다.

- 따라서 이러한 개발로 인해 예측 기간 동안 영국은 유럽의 목재 펠릿 시장을 독점할 것으로 예상됩니다.

유럽 목재 펠릿 산업 개요

유럽의 목재 펠렛 시장은 반고체화되고 있습니다. 시장의 주요 기업으로는 Store Enso Oyj, Enviva Partners LP, AS Graanul Invest, Drax Group PLC, Segezha Group PJSC 등이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 서문

- 시장 규모 및 수요 예측(-2029년)

- 최근 동향 및 개발

- 정부 규제 및 정책

- 시장 역학

- 성장 촉진요인

- 청정 에너지 발전에 있어서 목재 펠릿 수요 증가

- 열 공급 용도

- 성장 억제요인

- 대체 클린 에너지와 경쟁 격화 및 목재 펠릿에 대한 정부 지원 제도 종료

- 성장 촉진요인

- 공급망 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 용도별

- 난방

- 발전

- 지역별

- 독일

- 영국

- 프랑스

- 네덜란드

- 벨기에

- 스페인

- 러시아

- 기타 유럽

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 프로파일

- Stora Enso Oyj

- Enviva Partners LP

- AS Graanul Invest

- Drax Group PLC

- Segezha Group PJSC

- Svenska Cellulosa Aktiebolaget SCA

- German Pellets GmbH

- Pure Biofuel Ltd

- Pfeifer Group

- Erdenwerk Gregor Ziegler GmbH

- 시장 랭킹 분석

제7장 시장 기회 및 향후 동향

- 목재 펠릿 기술의 새로운 용도 및 진보

The Europe Wood Pellet Market size is estimated at USD 16.36 billion in 2025, and is expected to reach USD 20.44 billion by 2030, at a CAGR of 4.55% during the forecast period (2025-2030).

Key Highlights

- Over the medium period, the increasing demand for wood pellets in clean energy generation and heat-supply applications will likely drive the European wood pellets market.

- On the other hand, the increasing competition from alternative clean energy sources and the ending of supportive government schemes for wood pellets will likely hinder market growth during the forecast period.

- Nevertheless, the emerging applications and advancements in wood pellet technology are expected to boost the market's growth in the future.

- The United Kingdom is expected to dominate the European wood pellet market due to the increasing adoption of wood pellets for various applications.

Europe Wood Pellet Market Trends

The Heating Application Segment is Expected to Dominate the Market

- Wood pellets for heating applications are primarily used in residential and commercial sectors for food, cooking and grilling, and supplying heat to homes. These wood pellets, along with connected pipes, boilers, and heating radiators, are used to build heating systems at home. For heating proposes, several systems using wood pellets include pellet central heating boilers, pellet stoves, and pellet central heating stoves.

- The heating application segment of the European wood pellet market is expected to generate significant demand due to the rising consumption of wood pellets, especially in Germany and France. Europe is the largest global wood pallet market. In 2022, the region's total wood pallet consumption accounted for 24.8 million metric tons (MMT). According to the European Commission's (EC) mandates and incentives by EU Member States (MS), demand was expected to further expand to 25.6 MMT in 2023.

- The increasing demand for wood pellets for residential heating purposes is expected to fuel the market's growth in the future. Residential uses include domestic stoves and dedicated heat boilers with a capacity below 50 kW. Small-to-medium-scale commercial use with more than 50 kW capacity includes heat boilers used in residential and public buildings.

- Wood pellets can be used as a home heating fuel in biomass boilers or special pellet-burning stoves. Pellet stoves are better than traditional open-wood fireplaces as they burn cleaner with less smoke and soot. As the wood pellets are highly dense and contain low moisture content (lower than 10%), the pellets can burn in the stove at a very high combustion temperature with improved efficiency and much lower ash content (less than 2%) than conventional firewood.

- Using wood pellets for heating is an alternative method of reducing electricity bills. Consumers in Europe are looking for alternative ways to heat their homes following higher fuel bills.

- According to the Stove Industry Alliance, wood logs are the cheapest domestic heating fuel, costing households 74% less per kWh than electric heating and 21% less than gas heating. Such benefits of wood pellets are expected to increase their demand in heating applications during the forecast period.

- Germany, Italy, France, Denmark, and Sweden are the major countries that use wood pellets for heating purposes. According to the EPC Survey 2023, Germany used the highest amount of wood pellets for heating purposes in 2022, which accounted for 3.2 million tons.

- In Germany and Italy, more than 70% of heat generation from wood pellets was used for residential heating, while in Denmark and Sweden, pellets were used mostly for CHP heat. The climate plays an important role in the consumption of wood pellets. As the climate of European countries is expected to have colder seasons in the future, the use of pellets for heating purposes is expected to increase during the forecast period.

- Therefore, the heating application segment is expected to dominate the market during the forecast period.

The United Kingdom is Expected to Dominate the Market

- The United Kingdom uses pellets in numerous applications, such as residential heating, power plants, commercial heating, and combined heat and power plants. Pellets have also made their way into coal conversion projects in local authority buildings and public administration buildings such as schools and offices.

- As of 2024, most of the co-firing power stations have either closed or converted, with several shifting toward using 100% wood pellets for fuel. The largest of these is Drax Power Station in North Yorkshire. It has converted four of its six 65 MWe generating units to run exclusively on wood pellets.

- The Drax power plant is the country's largest, producing around 5% of the United Kingdom's total electricity in 2023. It is also the world's largest biomass-fired power station, taking in around 6.5 million metric tons (MT) of pellets each year and making up the vast majority of the country's annual pellet imports. The company also has 17 pellet plants located in the United States and Canada, which supply raw materials to its power station.

- However, according to the UK government, the country imported 6 million metric tons of wood pellets in 2023, compared to 7.52 million metric tons in 2022 and 9.13 million tons in 2021.

- According to the Food and Agriculture Organization of the United Nations, the country's wood pellet production was about 326 thousand metric tons in 2022. The production of wood pellets witnessed significant growth of about 7.2% compared to the previous year.

- In December 2023, the UK government announced its plans to extend the CfD program to support bioenergy with carbon capture and storage (BECCS) as the country set out its plan to develop a competitive market in Carbon Capture, Usage, and Storage (CCUS) by 2035. The plan is expected to boost the UK economy by EUR 5 billion a year by 2050 and make the country a pioneer in this technology.

- Drax receives hundreds of millions of pounds in annual subsidies to fund its operations. In 2027, the UK government plans to end its support for burning unabated biomass to generate electricity.

- To prevent subsidy closure after 2027, Drax is looking to secure a new long-term subsidy for its wood-burning operation. The company aims to achieve this through its planned Bioenergy with Carbon Capture (BECCS) project. This project initially proposed adding carbon capture storage (CCS) to half of its existing capacity, which the company claims will generate eight metric tons of negative emissions yearly. The aim is to add CCS to its full capacity.

- In January 2024, following the extension of the CfD program, the UK government approved Drax's plans to install carbon capture technology at Drax Power Station. The Power Station will be allowed to install the technology in two of its four biomass units, which burn wood pellets to produce electricity.

- Hence, owing to such developments, the United Kingdom is expected to dominate the European wood pellets market during the forecast period.

Europe Wood Pellet Industry Overview

The European wood pellets market is semi-consolidated. Some of the key players in the market include Stora Enso Oyj, Enviva Partners LP, AS Graanul Invest, Drax Group PLC, and Segezha Group PJSC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand for Wood Pellets in Clean Energy Generation

- 4.5.1.2 Heat-supply Applications

- 4.5.2 Restraints

- 4.5.2.1 Increasing Competition from Alternative Clean Energy Sources and Ending of Supportive Government Schemes for Wood Pellets

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Heating

- 5.1.2 Power Generation

- 5.2 Geography

- 5.2.1 Germany

- 5.2.2 United Kingdom

- 5.2.3 France

- 5.2.4 Netherlands

- 5.2.5 Belgium

- 5.2.6 Spain

- 5.2.7 Russia

- 5.2.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Stora Enso Oyj

- 6.3.2 Enviva Partners LP

- 6.3.3 AS Graanul Invest

- 6.3.4 Drax Group PLC

- 6.3.5 Segezha Group PJSC

- 6.3.6 Svenska Cellulosa Aktiebolaget SCA

- 6.3.7 German Pellets GmbH

- 6.3.8 Pure Biofuel Ltd

- 6.3.9 Pfeifer Group

- 6.3.10 Erdenwerk Gregor Ziegler GmbH

- 6.4 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Applications and Advancements in the Wood Pellet Technology

샘플 요청 목록