|

시장보고서

상품코드

1683874

유럽의 전기 상용차 배터리 팩 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2029년)Europe Electric Commercial Vehicle Battery Pack - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2029) |

||||||

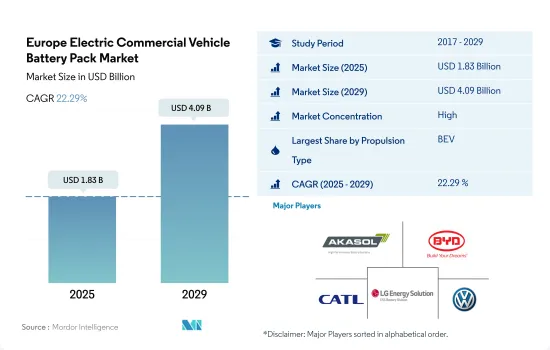

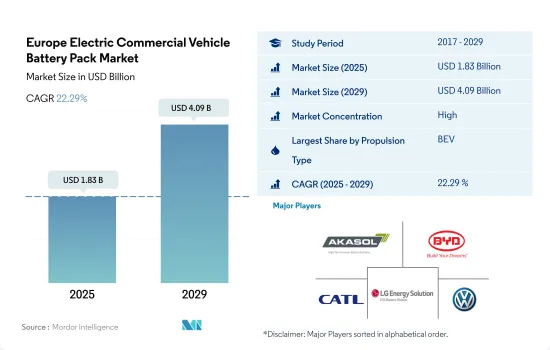

유럽의 전기 상용차 배터리 팩 시장 규모는 2025년에 18억 3,000만 달러로 추정되고, 2029년에는 40억 9,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2025-2029년)의 CAGR은 22.29%를 보일 것으로 예측됩니다.

비용 하락과 기술 발전이 유럽의 전기 상용차 시장의 배터리 팩 수요를 견인

- 유럽의 전기 상용차 배터리 팩 시장은 2017년부터 2022년까지 크게 성장했습니다. 한 보고서에 따르면 유럽은 2020년 전기 상용차 판매량이 57% 증가하여 3만 6,000대 이상이 판매되었습니다. LCV와 M & HDT가 가장 인기 있는 카테고리로 전체 판매량의 80% 이상을 차지했습니다. 전기 상용차의 도입과 보급은 규제와 인센티브에 힘입어 향후 몇 년 동안 더욱 증가할 것으로 예상됩니다.

- 전기 상용차에 대한 수요가 증가함에 따라 배터리 팩에 대한 수요도 증가했습니다. 배터리 밀도와 주행거리는 빠르게 개선되고 있으며, 전기 상용차의 평균 주행거리는 작년에만 20% 이상 증가했습니다. 하지만 배터리 팩의 가격은 여전히 전기 상용차 도입에 큰 장벽으로 작용하고 있습니다. 전기 상용차의 배터리 팩 비용은 규모의 경제와 기술 발전에 힘입어 2030년까지 56%까지 하락할 것으로 예상됩니다.

- 향후에도 유럽에서 상용차용 순수 전기 배터리 팩 시장은 지속적으로 성장할 것으로 예상됩니다. 환경 규제가 강화되고 탄소 중립 경제를 향한 움직임이 활발해지면서 많은 기업이 차량의 전기화를 모색하고 있습니다. 또한 전고체 배터리와 배터리 재활용을 포함한 배터리 기술 개발에도 상당한 기회가 있습니다. 또한, 충전 인프라의 개발은 전기 상용차의 광범위한 도입을 지원하는 데 매우 중요합니다.

정부의 지원과 투자가 유럽에서 전기자동차 채택을 촉진

- 2017년부터 2021년까지 유럽의 전기 상용차 배터리 팩 시장은 크게 성장했습니다. 이러한 성장은 환경에 대한 관심 증가, 전기자동차 도입을 촉진하는 정부 규제, 전기 상용차의 성능과 신뢰성을 향상시킨 배터리 기술의 발전 등의 요인에 의해 주도되었습니다.

- 2022년 유럽 전기 상용차 배터리 팩 시장은 긍정적인 궤적을 이어갔습니다. 이러한 성장은 전기 상용차와 관련된 장기적인 비용 절감에 대한 기업의 인식 증가, 충전 인프라의 확대, 배터리 팩의 효율성과 매력을 향상시킨 배터리 기술의 지속적인 발전 등의 요인에 의해 영향을 받았습니다.

- 2023-2029년 예측 기간 동안 유럽 전기 상용차 배터리 팩 시장은 높은 성장세를 보일 것으로 예상됩니다. 이러한 성장은 운송의 전기화를 촉진하는 정부 지원, 배터리 팩의 비용 감소, 배터리 성능 향상을 위한 지속적인 연구 개발 노력 등의 요인으로 인해 증가할 것으로 예상됩니다. 소비자 인식이 높아지고 전기자동차의 환경적 이점에 대한 관심이 높아지면서 지속 가능한 운송 수단으로의 전환이 가속화되고 있습니다. 이러한 요인들이 계속 융합되면서 전기자동차 배터리 시장은 향후 몇 년간 지속적인 성장과 발전을 거듭할 것이며, 전 세계 소비자들이 전기자동차를 매력적이고 쉽게 이용할 수 있게 될 것입니다.

유럽의 전기 상용차 배터리 팩 시장 동향

도요타 그룹이 유럽 전기자동차 시장을 주도

- 유럽 여러 국가의 전기자동차 시장은 수많은 업체들이 활동하면서 크게 성장하고 있지만, 2022년 시장의 50% 이상을 차지한 5개 주요 업체들이 주도하고 있습니다. 이러한 기업에는 도요타 그룹, 기아, 르노, 테슬라, 기아, 폭스바겐이 포함됩니다. 도요타 그룹은 유럽에서 가장 많은 전기자동차를 판매하고 있으며, 전기자동차 시장에서 약 14.84%의 점유율을 차지하고 있습니다. 이 회사는 다양한 유럽 국가의 고객 수요와 공급을 충족하는 강력한 공급 및 유통 네트워크를 보유하고 있습니다. 이 회사는 전기자동차 시장에서 광범위한 제품 포트폴리오를 제공하고 있습니다.

- 르노는 약 7.47%의 시장 점유율을 차지하며 유럽 전역에서 두 번째로 큰 전기자동차 판매 업체입니다. 이 회사는 좋은 브랜드 이미지와 탄탄한 재무 상태를 보유하고 있습니다. 이 회사는 닛산과 같은 우수한 브랜드와 제휴 및 전략적 파트너십을 맺고 있습니다. 전기자동차 판매에서 세 번째로 높은 시장 점유율인 6.71%를 기록한 기업은 테슬라입니다. 이 기업은 최첨단 혁신에 중점을 두고 있으며 배터리를 비롯한 여러 전기자동차 부품 생산업체와 견고한 전략적 제휴를 맺고 있습니다.

- 유럽의 전기자동차 판매량 4위는 기아로 약 6.26%의 시장 점유율을 차지했습니다. 이 회사는 다른 브랜드에 비해 다양한 유형의 고객을 위한 폭넓은 제품군을 보유하고 있으며, 합리적인 가격대의 다양한 옵션을 제공합니다. 유럽 전기자동차 시장에서 5번째로 큰 업체는 BMW로, 약 6.14%의 시장 점유율을 유지하고 있습니다. 유럽 여러 국가에서 전기자동차를 판매하는 다른 업체로는 현대, 메르세데스-벤츠, BMW, 아우디, 포드 등이 있습니다.

테슬라와 르노는 2022년 유럽에서 전기자동차의 광범위한 판매로 인해 배터리 팩 수요에 가장 큰 기여

- 지난 몇 년 동안 유럽의 모든 지역에서 전기자동차에 대한 수요가 급격히 증가했습니다. 이제 유럽 도로에서 전기자동차가 더 많이 보급되었습니다. 전기자동차 구매에 대한 소비자의 관심은 지역과 국가에 따라 다르지만, 유럽에서 가장 큰 두 개의 전기자동차 시장인 독일과 영국에서는 SUV가 가장 인기 있는 전기자동차 유형입니다. 편안한 이동 수단에 대한 관심이 높아지고 SUV가 세단보다 공간이 넓다는 점 때문에 여러 유럽 국가에서 전기 SUV에 대한 수요가 세단 수요를 앞지르고 있습니다.

- 유럽 전역에서 소형 SUV를 구매하는 소비자들의 수가 급격히 증가하고 있습니다. 테슬라 모델 Y는 완전 전기 모터, 별 다섯 개를 획득한 NCAP 안전 인증, 최대 7명까지 탑승 가능한 넓은 좌석, 긴 주행거리 등 다양한 기능을 제공합니다. 2022년 영국과 독일을 비롯한 여러 주요 유럽 시장에서 가장 인기 있는 모델 중 하나가 되었습니다. 르노 아르카나는 풀 하이브리드 엔진을 탑재해 연비와 가격 경쟁력으로 프랑스 등 여러 유럽 국가에서 고객들로부터 좋은 판매 반응을 얻고 있습니다.

- Captur은 하이브리드와 플러그인 하이브리드 파워트레인을 제공하며 구매자를 끌어들이는 다양한 기능으로 2022년 유럽 국가에서 르노의 베스트셀러 중 하나입니다. 유럽 전기자동차 시장에는 다양한 글로벌 브랜드의 다양한 전기 SUV와 세단도 있습니다. 대표적인 차량 중 하나는 2022년에 좋은 판매량을 기록한 도요타 야리스와 포드 쿠가입니다. 유럽 전기자동차 시장에서 경쟁하고 있는 다른 차량으로는 피아트 500과 도요타 야리스 크로스가 있습니다.

유럽의 전기 상용차 배터리 팩 산업 개요

유럽의 전기 상용차 배터리 팩 시장은 상당히 통합되어 있으며 상위 5개사에서 74.45%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. Akasol AG, BYD Company Ltd., Contemporary Amperex Technology(CATL), LG Energy Solution Ltd. and SAIC Volkswagen Power Battery(sorted alphabetically).

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 전기 상용차 판매 대수

- OEM별 전기 상용차 판매 대수

- 베스트셀러 전기 상용차 모델

- 선호되는 배터리 화학을 가진 OEM

- 배터리 팩 가격

- 배터리 재료 비용

- 다양한 배터리 화학의 가격 차트

- 누가 누구에게 공급하는지

- EV 배터리 용량 및 효율성

- 출시 된 EV 모델 수

- 규제 프레임워크

- 벨기에

- 프랑스

- 독일

- 헝가리

- 폴란드

- 영국

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 차체 유형

- 버스

- LCV

- M & HDT

- 추진 유형

- BEV

- PHEV

- 배터리 화학

- LFP

- NCA

- NCM

- NMC

- 기타

- 용량

- 15-40kWh

- 40-80kWh

- 80kWh 이상

- 15kWh 미만

- 배터리 형태

- 원통형

- 파우치형

- 프리즘형

- 방식

- 레이저

- 와이어

- 구성요소

- 양극

- 음극

- 전해질

- 분리기

- 재료 유형

- 코발트

- 리튬

- 망간

- 천연 흑연

- 니켈

- 기타 재료

- 국가명

- 프랑스

- 독일

- 헝가리

- 이탈리아

- 폴란드

- 스웨덴

- 영국

- 기타 유럽

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Akasol AG

- BMZ Batterien-Montage-Zentrum GmbH

- BYD Company Ltd.

- Contemporary Amperex Technology Co. Ltd.(CATL)

- LG Energy Solution Ltd.

- Microvast Holdings Inc

- NorthVolt AB

- Panasonic Holdings Corporation

- SAIC Volkswagen Power Battery Co. Ltd.

- Samsung SDI Co. Ltd.

- SK Innovation Co. Ltd.

- SVOLT Energy Technology Co. Ltd.(SVOLT)

- TOSHIBA Corp.

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 출처 및 참고문헌

- 도표 목록

- 주요 인사이트

- 데이터 팩

- 용어집

The Europe Electric Commercial Vehicle Battery Pack Market size is estimated at 1.83 billion USD in 2025, and is expected to reach 4.09 billion USD by 2029, growing at a CAGR of 22.29% during the forecast period (2025-2029).

Cost decline and technological advancements drive demand for battery packs in the European electric commercial vehicle market

- The European electric commercial vehicle battery pack market grew significantly from 2017 to 2022. According to a report, Europe witnessed a 57% increase in electric commercial vehicle sales in 2020, with over 36,000 units sold. LCVs and M&HDT were the most popular categories, representing over 80% of total sales. The adoption and penetration of electric commercial vehicles are expected to grow in the coming years, driven by regulations and incentives.

- The growing demand for electric commercial vehicles has also increased the demand for battery packs. Battery density and range have been improving rapidly, with the average range of electric commercial vehicles increasing by over 20% in the past year alone. However, the cost of battery packs remains a significant barrier to adoption. The cost of battery packs for electric commercial vehicles is expected to decline by 56% by 2030, driven by economies of scale and technological advancements.

- Looking toward the future, the pure electric battery pack market for commercial vehicles is expected to continue to grow in Europe. With increasing environmental regulations and a push toward a carbon-neutral economy, many companies are looking to electrify their fleets. There are also significant opportunities in the development of battery technology, including solid-state batteries and battery recycling. Additionally, the development of charging infrastructure will be critical to support the widespread adoption of electric commercial vehicles.

Government support and investments drive electric vehicle adoption in Europe

- Between 2017 and 2021, the European electric commercial vehicle battery pack market experienced significant growth. This growth was driven by factors such as rising environmental concerns, government regulations promoting electric vehicle adoption, and advancements in battery technology, which improved the performance and reliability of electric commercial vehicles.

- In 2022, the European electric commercial vehicle battery pack market continued its positive trajectory. This growth was influenced by factors such as increased awareness among businesses about long-term cost savings associated with electric commercial vehicles, the expansion of charging infrastructure, and ongoing advancements in battery technology, which enhanced the efficiency and appeal of battery packs.

- During the forecast period of 2023-2029, the European electric commercial vehicle battery pack market is expected to exhibit strong growth. This growth is expected to increase due to factors such as government initiatives promoting the electrification of transportation, decreasing costs of battery packs, and ongoing research and development efforts to improve battery performance. Heightened consumer awareness and a strong focus on the environmental advantages of electric vehicles are propelling the transition toward sustainable transportation. As these factors continue to converge, the EV battery market is poised to see continued growth and advancements in the coming years, making electric vehicles attractive and accessible for consumers worldwide.

Europe Electric Commercial Vehicle Battery Pack Market Trends

TOYOTA GROUP LEADS THE EUROPEAN EV MARKET, FOLLOWED BY RENAULT, TESLA, KIA, AND BMW

- The market for electric vehicles in various European countries is growing significantly, with numerous players operating, but it is largely driven by five major companies, which held more than 50% of the market in 2022. These companies include Toyota Group, Kia, Renault, Tesla, Kia, and Volkswagen. Toyota Group is the largest seller of electric vehicles in Europe, accounting for around 14.84% share of the electric car market. The company has a strong supply and distribution network catering to the demand and supply of customers in various European countries. The company has a wide product portfolio offering in the EV market.

- Renault holds a market share of around 7.47%, making it the second-largest seller of electric vehicles across Europe. The company has a good brand image and a strong financial position. The company has alliances and strategic partnerships with good brands such as Nissan. The 3rd highest market share, 6.71%, for electric vehicle sales was recorded by Tesla. The business focuses on cutting-edge innovations and has solid strategic alliances with producers of several EV parts, including batteries.

- The 4th largest place in European EV sales is Kia, accounting for around 6.26% of the market share. The company has wide product offerings for various types of customers with various budget-friendly options compared to other brands. The 5th largest player operating in the European EV market is BMW, maintaining its market share at around 6.14%. Some of the other players selling EVs in various European countries include Hyundai, Mercedes-Benz, BMW, Audi, and Ford.

Tesla and Renault are the largest contributors to the demand for battery packs, as a result of the widespread sale of EVs in Europe in 2022

- The demand for electric vehicles has dramatically increased during the past several years in every part of Europe. Electric vehicles are now more prevalent on European roadways. Although consumer interest in buying electric vehicles varies by area and by country, SUVs are the most popular type of electric vehicle in Germany and the United Kingdom, the region's two biggest markets for electric vehicles. The demand for electric SUVs is outpacing that for sedans in various European countries due to the increased interest in comfortable transportation and the fact that SUVs are roomier than sedans.

- The number of compact SUVs purchased by consumers has increased dramatically across Europe. The Tesla Model Y offers a fully electric motor, a 5-star NCAP safety certification, spacious seating for up to 7 passengers, a long-range, and other features. It became one of the most popular models in several major European markets, including the United Kingdom and Germany, in 2022. The Renault Arkana provides a full hybrid engine, which has received a strong sales reaction from customers in several European nations like France due to its fuel efficiency and competitive pricing.

- Captur was one of the best sellers from Renault in the European countries in 2022, owing to its offering of a hybrid and a plug-in hybrid powertrain, and is packed with lots of features attracting buyers. The European EV market also features a variety of electric SUVs and sedans from various international brands. One of the common cars is the Toyota Yaris and Ford Kuga, which recorded good sales in 2022. Other cars in the European EV market that are in the competition include the Fiat 500 and Toyota Yaris Cross.

Europe Electric Commercial Vehicle Battery Pack Industry Overview

The Europe Electric Commercial Vehicle Battery Pack Market is fairly consolidated, with the top five companies occupying 74.45%. The major players in this market are Akasol AG, BYD Company Ltd., Contemporary Amperex Technology Co. Ltd. (CATL), LG Energy Solution Ltd. and SAIC Volkswagen Power Battery Co. Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Electric Commercial Vehicle Sales

- 4.2 Electric Commercial Vehicle Sales By OEMs

- 4.3 Best-selling EV Models

- 4.4 OEMs With Preferable Battery Chemistry

- 4.5 Battery Pack Price

- 4.6 Battery Material Cost

- 4.7 Price Chart Of Different Battery Chemistry

- 4.8 Who Supply Whom

- 4.9 EV Battery Capacity And Efficiency

- 4.10 Number Of EV Models Launched

- 4.11 Regulatory Framework

- 4.11.1 Belgium

- 4.11.2 France

- 4.11.3 Germany

- 4.11.4 Hungary

- 4.11.5 Poland

- 4.11.6 UK

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Body Type

- 5.1.1 Bus

- 5.1.2 LCV

- 5.1.3 M&HDT

- 5.2 Propulsion Type

- 5.2.1 BEV

- 5.2.2 PHEV

- 5.3 Battery Chemistry

- 5.3.1 LFP

- 5.3.2 NCA

- 5.3.3 NCM

- 5.3.4 NMC

- 5.3.5 Others

- 5.4 Capacity

- 5.4.1 15 kWh to 40 kWh

- 5.4.2 40 kWh to 80 kWh

- 5.4.3 Above 80 kWh

- 5.4.4 Less than 15 kWh

- 5.5 Battery Form

- 5.5.1 Cylindrical

- 5.5.2 Pouch

- 5.5.3 Prismatic

- 5.6 Method

- 5.6.1 Laser

- 5.6.2 Wire

- 5.7 Component

- 5.7.1 Anode

- 5.7.2 Cathode

- 5.7.3 Electrolyte

- 5.7.4 Separator

- 5.8 Material Type

- 5.8.1 Cobalt

- 5.8.2 Lithium

- 5.8.3 Manganese

- 5.8.4 Natural Graphite

- 5.8.5 Nickel

- 5.8.6 Other Materials

- 5.9 Country

- 5.9.1 France

- 5.9.2 Germany

- 5.9.3 Hungary

- 5.9.4 Italy

- 5.9.5 Poland

- 5.9.6 Sweden

- 5.9.7 UK

- 5.9.8 Rest-of-Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Akasol AG

- 6.4.2 BMZ Batterien-Montage-Zentrum GmbH

- 6.4.3 BYD Company Ltd.

- 6.4.4 Contemporary Amperex Technology Co. Ltd. (CATL)

- 6.4.5 LG Energy Solution Ltd.

- 6.4.6 Microvast Holdings Inc

- 6.4.7 NorthVolt AB

- 6.4.8 Panasonic Holdings Corporation

- 6.4.9 SAIC Volkswagen Power Battery Co. Ltd.

- 6.4.10 Samsung SDI Co. Ltd.

- 6.4.11 SK Innovation Co. Ltd.

- 6.4.12 SVOLT Energy Technology Co. Ltd. (SVOLT)

- 6.4.13 TOSHIBA Corp.

7 KEY STRATEGIC QUESTIONS FOR EV BATTERY PACK CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms