|

시장보고서

상품코드

1683980

아시아태평양의 살충제 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Asia Pacific Insecticide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

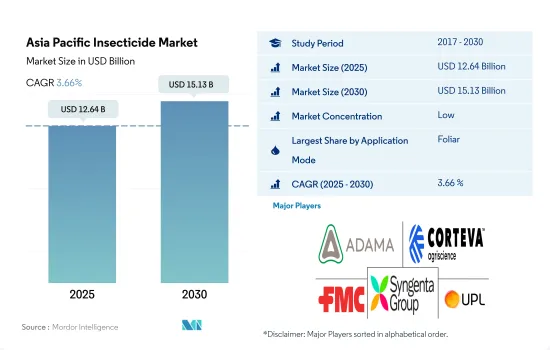

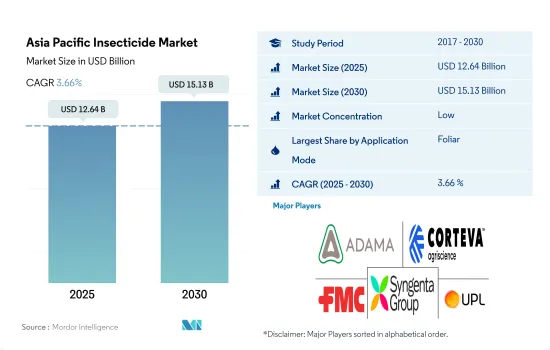

아시아태평양의 살충제 시장 규모는 2025년 126억 4,000만 달러로 추정되며, 2030년에는 151억 3,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2025-2030년) CAGR 3.66%로 성장할 것으로 예측됩니다.

시장을 견인하고 있는 것은 병해충의 만연에 의한 수량 감소의 증대입니다.

- 이 지역 대부분의 국가에서 농업은 중요한 역할을 하며 GDP에 크게 기여하고 있습니다. 그럼에도 불구하고 해충의 만연으로 인한 농작물 생산 위험은 크고 수율 감소, 농부의 경제적 손실, 식량 안보에 대한 우려로 이어집니다. 아시아태평양은 기후와 토양이 다양하기 때문에 다양한 작물을 재배 할 수 있습니다.

- 이 지역에서는 충해를 관리하기 위해 다양한 살포 방법이 채택되었습니다. 2022년에는 엽면 살포법이 금액 기준으로 57.0%로 가장 높은 점유율을 차지했습니다. 이 지역에서는 종합 해충 관리 전략의 일환으로 클로란트라닐리프롤, 엠마멕틴 벤조산염 및 스피네트람에 의한 엽면 살포가 상당히 효과적임이 확인되었습니다.

- 토양 처리법은 2022년 금액 기준으로 9.9%로 세 번째로 높은 점유율을 차지했습니다. 토양에 살충제 살포는 곤충을 방제하는 가장 쉽고 안전하고 효율적인 방법임이 확인되었습니다. 농업 해충의 경우, 약 95%가 일생 중 일부를 흙 속에서 보내고 있기 때문에 이미 말했듯이, 흙 속에 가두어 두는 것이 불가결합니다.

- 그럼에도 불구하고 잎 표면 살포 농약의 사용에는 소비자, 노동자 및 환경 건강에 몇 가지 단점이 있습니다. 화학 관개는 점적 관개 시스템을 사용하여 토양의 살충제를 사용하는 것으로, 잎 표면 살포 살충제에 공통적 인 몇 가지 단점을 제거 할 수 있습니다. 화학 관개는 2022년 금액 기준으로 7.4%의 점유율을 차지했습니다.

- 가장 안전하고 효과적인 살포 방법을 만드는 것을 목표로 하는 연구와 기술 혁신 증가로 시장은 예측 기간(2023-2029년)에 CAGR 3.9%를 나타낼 것으로 예상됩니다.

기후 변화로 인한 해충 위협 증가가 시장 성장에 기여

- 2022년 살충제 세계 시장 점유율은 아시아태평양이 34.8%를 차지했습니다. 아시아태평양은 농업 부문이 크고 해충이 많기 때문에 살충제의 중요한 시장 중 하나입니다. 이 지역에서 살충제는 곤충과 해충으로부터 작물을 보호하고 높은 수율을 보장하기 위해 널리 사용됩니다.

- 인도, 중국, 일본, 호주 등의 국가들은 농작물을 보호하기 위해 살충제를 널리 채용하고 있으며, 작물의 수율과 생산성에 대한 곤충의 영향에 대한 인식이 높아지고 있기 때문에 시장에서 큰 점유율을 차지하고 있습니다.

- 현대적인 농업 관행의 도입과 경작 면적 증가 등 농업 활동의 확대가 시장 성장에 기여하고 있습니다. 이 지역의 경작 면적은 2019년 6억 2,450만 헥타르에서 2022년 6억 6,220만 헥타르로 증가했습니다. 농업이 증가함에 따라 해충으로부터 작물을 보호하는 효과적인 솔루션이 필요합니다.

- 기후 변화는 작물에 피해를 주는 해충의 만연으로 이어집니다. 이러한 이유로 살충제 수요는 향후 몇 년동안 증가할 수 있습니다.

- 중국은 해충 위협 증가와 농작물 손실 증가로 인한 농민들이 살충제 사용량을 늘릴 것으로 예상되기 때문에 예측기간(2023-2029년)의 CAGR은 5.7%로, 이 지역에서 가장 급성장할 것으로 전망되고 있습니다.

- 아시아태평양의 살충제 시장은 농업 부문 확대, 작물 보호 필요성 증가, 기후 변화로 인한 살충제 수요 증가로 2023년부터 2029년까지 연평균 복합 성장률(CAGR) 3.9%를 나타낼 것으로 예측됩니다.

아시아태평양의 살충제 시장 동향

기온 상승은 노린재 같은 다양한 해충의 성장을 가속하고 헥타르 당 살충제 소비를 증가시킵니다.

- 아시아태평양에서는 일본의 1헥타르당 살충제 소비량이 높아 2017년부터 2022년까지 약 7% 증가했습니다. 이 증가는 해충의 개체수가 크게 증가했기 때문일 수 있습니다. 농림수산부의 보고에 따르면 농작물에 심각한 위협을 일으키는 노린재는 최근 점점 더 확산되고 있습니다. 전문가에 따르면, 노린재를 비롯한 해충 증식의 주요 요인은 지구 온난화에 있다고합니다. 노린재 및 기타 해충의 만연을 관리하는 주요 방법은 화학 살충제의 사용이며, 살포의 빈도와 양이 증가하는 것이 베트남에서 헥타르 당 살충제의 소비량이 증가하는 주요 요인입니다.

- 베트남은 헥타르당 살충제 사용량 이 지역에서 두 번째로 많은 국가입니다. 헥타르당 살충제 사용량은 2017년 750g에서 2022년 1,200g으로 크게 증가했습니다. 이 증가는 생산성 향상과 해충 방제를 목적으로 한 집약적 작물 생산 기술의 채용으로 인한 것으로 예상됩니다. 고온, 다습, 빈번한 강우를 특징으로하는 베트남의 열대 기후는 농업에 좋은 조건을 제공하지만 동시에 해충의 급속한 성장을 가속합니다. 그 결과, 이 나라에서는 헥타르당 살충제 소비량이 증가하고 있습니다.

- 전반적으로 아시아태평양의 기타 국가에서도 헥타르 당 살충제 소비량이 전년 대비 증가하고 있습니다. 해충 발생 수 증가로 이어지는 기후 변화가이 추세의 주된 이유입니다.

사탕수수, 면화, 과일, 야채 등 주요 작물에서 살충제 수요 증가는 유효 성분의 가격 상승에 유리합니다.

- 기후 변화 외에도 해충은 이 지역의 농업 부문에 큰 위협을 가하고 있으며 평균 73%-100%의 수율 손실을 초래합니다. 이러한 해충과 효과적으로 싸우기 위해 농부는 화학 살충제에 크게 의존합니다.

- 이 지역에서 가장 널리 사용되는 살충제는 시페르메트린으로, 비늘눈, 외초목, 쌍둥이눈, 반선목 등 다양한 해충을 효과적으로 구제하는 합성 피레스로이드계의 특성으로 알려져 있습니다. 인도, 중국, 베트남 등의 국가에서는 주로 시펠 메트린이 다양한 작물의 해충 방제에 사용됩니다. 중국과 베트남은 시펠 메트린의 주요 수입국입니다. 2022년 현재 유효성분 가격은 1톤당 21,037.7달러로 상승했으며 2017년 이후 21.1%의 상당한 상승을 반영하고 있습니다. 이 현저한 가격 상승은 주로 사탕수수, 면화, 과일, 야채 등의 작물에 있어서의 시펠메트린 수요 증가에 기인합니다.

- 네오니코티노이드계 살충제인 이미다클로프리드는 면화, 벼, 지방종자, 과일, 야채, 차, 커피, 카다몬 등의 농장 작물 등 다양한 작물의 종자 코팅제, 토양 처리제, 엽면 처리제로 사용되고 있습니다. 그 주요 목적은 흡즙성 해충의 치료입니다. 중국은 이미다클로프리드의 주요 수출국이고 인도와 베트남은 이 살충제의 주요 수입국입니다. 유효성분의 가격은 톤당 17,105.7달러로 2017년에 비해 21.2%의 대폭 상승했습니다.

- 수요 증가, 수입 관세, 환율 변동 등 다양한 요인이 유효 성분의 가격 변동에 기여하고 있습니다.

아시아태평양 살충제 산업 개요

아시아태평양 살충제 시장은 세분화되어 상위 5개사에서 21.92%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. ADAMA Agricultural Solutions Ltd, Corteva Agriscience, FMC Corporation, Syngenta Group, UPL Limited(알파벳순).

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 1헥타르당 농약 소비량

- 유효성분의 가격 분석

- 규제 프레임워크

- 호주

- 중국

- 인도

- 인도네시아

- 일본

- 미얀마

- 파키스탄

- 필리핀

- 태국

- 베트남

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 사용 방법

- 화학 관개

- 잎면 살포

- 훈증

- 종자 처리

- 토양처리

- 작물 유형

- 상업 작물

- 과일·야채

- 곡물

- 콩류 및 유량씨

- 잔디 및 관상용

- 국가

- 호주

- 중국

- 인도

- 인도네시아

- 일본

- 미얀마

- 파키스탄

- 필리핀

- 태국

- 베트남

- 기타 아시아태평양 지역

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일(세계 수준 개요, 시장 수준 개요, 주요 사업 부문, 재무, 직원 수, 주요 정보, 시장 순위, 시장 점유율, 제품 및 서비스, 최근 동향 분석 포함)

- ADAMA Agricultural Solutions Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Jiangsu Yangnong Chemical Co. Ltd

- Nufarm Ltd

- Rainbow Agro

- Syngenta Group

- UPL Limited

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계의 개요

- 개요

- Porter's Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Asia Pacific Insecticide Market size is estimated at 12.64 billion USD in 2025, and is expected to reach 15.13 billion USD by 2030, growing at a CAGR of 3.66% during the forecast period (2025-2030).

The market is being driven by growing yield losses due to increasing pest infestations

- In most of the countries in the region, agriculture has a key role to play and contributes substantially to GDP. Nevertheless, there is a significant risk to crop production due to the infestations of insects that result in reduced yields, financial losses for farmers, and concerns about food security. The diversity of climate and soil in Asia-Pacific allows for the cultivation of different crops.

- Various application methods are adopted in the region to manage insect infestation. The foliar application method occupied the highest share of 57.0% by value in 2022. It has been observed that the use of foliar spraying with chlorantraniliprole, emamectin benzoate, and spinetoram as part of an integrated pest management strategy has been quite effective in the region.

- The soil treatment method occupied the third highest share of 9.9% by value in 2022. It has been observed that insecticide application on soil appeared to be the easiest, safest, and most efficient way of controlling insects. In terms of agricultural pests, approximately 95% have passed some portion of their lives in the soil, and therefore, it is essential for them to be held underground, as already mentioned.

- Nevertheless, there are several drawbacks to the health of consumers, workers, and the environment from using foliar pesticides. Chemigation uses pesticides in soil with drip irrigation systems and may remove several drawbacks common to foliar insecticide applications. Chemigation occupied a share of 7.4% by value in 2022.

- Owing to the increase in research and innovation, which are aimed to bring out the safest and most effective method of application, the market is anticipated to register a CAGR of 3.9% during the forecast period (2023-2029).

The rising threat of pests with changing climate is contributing to the growth of the market

- Asia-Pacific accounted for 34.8% of the market share of the global insecticide market in 2022. Asia-Pacific is one of the important markets for insecticides due to its large agricultural sector and the prevalence of pests in the region. Insecticides are widely used in the region to protect crops from insects and pests, ensuring higher yields.

- Countries such as India, China, Japan, and Australia hold a substantial share of the market due to the wide adoption of insecticides to protect crops and the rise in awareness about the effects of insects on crop yield and productivity.

- The expansion of agriculture activities, such as adapting modern agriculture practices and increasing the area under agricultural cultivation, contributes to the market's growth. The region witnessed an increase in acreage under cultivation to 662.2 million hectares in 2022 from 624.5 million hectares in 2019. As agriculture increases, effective solutions are needed to protect crops from pests.

- The changing climate is leading to the spread of insect pests that can damage crops. Due to this, the demand for insecticides may increase in the coming years.

- China is expected to grow fastest in the region at a CAGR of 5.7% during the forecast period (2023-2029) because the farmers in the country are expected to increase the usage of insecticide owing to the rising threat of pests and increasing crop losses.

- The Asia-Pacific insecticide market is forecasted to record a CAGR of 3.9% during 2023-2029 due to the increasing demand for insecticides due to the expansion of the agriculture sector, the rising need to protect crops, and the changing climate.

Asia Pacific Insecticide Market Trends

The rise in climate temperatures favors various insect pests like stink bugs to grow, increasing insecticide consumption per hectare

- In Asia-Pacific, Japan exhibits higher per-hectare consumption of insecticide, which witnessed approximately a 7% increase from 2017 to 2022. This rise may be attributed to the substantial growth in the population of insect pests. The Ministry of Agriculture, Forestry, and Fisheries reports that stink bugs, which pose significant threats to agricultural crops, have been increasingly prevalent in recent years. According to experts, the primary factor driving the proliferation of stink bugs and other pests is attributed to global warming. The principal approach to managing infestations of stink bugs and other pests involves the use of chemical insecticides, with the intensified frequency and dosages of the application being the primary factors contributing to the augmented consumption of insecticides per hectare in the country.

- Vietnam is the second country in the region in terms of insecticide usage per hectare. The amount of insecticide used per hectare significantly increased from 750 g in 2017 to 1,200 g in 2022. This rise may be attributed to the adoption of intensive crop production techniques aimed at improving productivity and pest control. Vietnam's tropical climate, characterized by high temperatures, humidity, and frequent rainfall, provides favorable conditions for agriculture but also promotes the rapid proliferation of insect pests. As a result, insecticide consumption per hectare has increased in the country.

- In overall, other countries in Asia-Pacific are also experiencing a YoY increase in insecticide consumption per hectare. Climate changes leading to an increase in the population of insect pests' infestations are primary reasons for this trend.

Increased demand for insecticides in major crops like sugarcane, cotton, and fruits and vegetables favors the active ingredient price growth

- In addition to climate changes, insect pests present a significant threat to the agriculture sector in the region, causing average yield losses of up to 73% to 100%. To combat these insect pests effectively, farmers are heavily relying on chemical insecticides.

- Cypermethrin holds a dominant position as the most widely used insecticide in the region, known for its synthetic pyrethroid properties that effectively control various insect pests, including Lepidoptera, Coleoptera, Diptera, and Hemiptera. Countries like India, China, and Vietnam predominantly rely on cypermethrin for pest control across various crops. China and Vietnam are the primary importers of cypermethrin. As of 2022, the price of the active ingredient increased to USD 21,037.7 per metric ton, reflecting a significant rise of 21.1% since 2017. This notable price increase was primarily attributed to the escalating demand for cypermethrin in crops such as sugarcane, cotton, and fruits and vegetables.

- Imidacloprid, a neonicotinoid insecticide, finds application as a seed dressing, soil treatment, and foliar treatment in various crops, including cotton, rice, oilseeds, fruits, and vegetables, and plantation crops like tea, coffee, and cardamom. Its primary purpose is to control sucking insect pests. China serves as the major exporter of Imidacloprid, while India and Vietnam are the main importing countries for this insecticide. The price of the active ingredient stood at USD 17,105.7 per metric ton, representing a significant increase of 21.2% compared to 2017.

- Various factors, such as rising demand, import tariffs, and fluctuations in exchange rates, contribute to the fluctuation in the price of the active ingredients.

Asia Pacific Insecticide Industry Overview

The Asia Pacific Insecticide Market is fragmented, with the top five companies occupying 21.92%. The major players in this market are ADAMA Agricultural Solutions Ltd, Corteva Agriscience, FMC Corporation, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Indonesia

- 4.3.5 Japan

- 4.3.6 Myanmar

- 4.3.7 Pakistan

- 4.3.8 Philippines

- 4.3.9 Thailand

- 4.3.10 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Myanmar

- 5.3.7 Pakistan

- 5.3.8 Philippines

- 5.3.9 Thailand

- 5.3.10 Vietnam

- 5.3.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Jiangsu Yangnong Chemical Co. Ltd

- 6.4.7 Nufarm Ltd

- 6.4.8 Rainbow Agro

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms