|

시장보고서

상품코드

1683984

중국의 제초제 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)China Herbicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

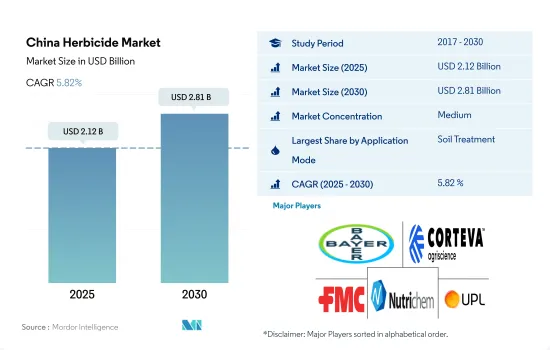

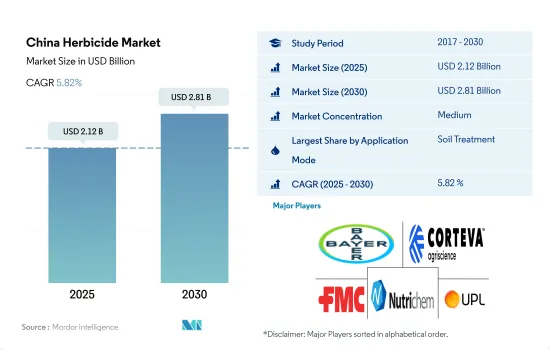

중국의 제초제 시장 규모는 2025년에 21억 2,000만 달러로 추정되고, 2030년에는 28억 1,000만 달러에 이를 것으로 예측되며, 예측 기간 2025년부터 2030년까지 CAGR 5.82%로 성장할 것으로 예측됩니다.

시장을 견인하는 것은 제초제의 효과적인 통제에 대한 요구입니다.

- 중국 농부는 제초제 살포에 다양한 방법을 채택하고 있습니다. 이 모든 방법의 시장 규모는 2022년에 17억 8,000만 달러에 달했습니다.

- 2022년 토양 처리법은 8억 4,150만 달러로 가장 높은 시장 점유율을 차지하며 제초제 시장 전체의 47.2%를 차지했습니다. 토양 처리의 인기는 특히 잡초 종자를 표적화하고 작물 파종 전에 발아를 억제하는 이삭 전 제초제의 사용에서의 효능 때문입니다. 2022년 시장 점유율은 31.9%로, 제초제의 엽면 살포는 잡초 방제에 많은 이점을 가져옵니다. 제초제가 잡초 잎과 직접 접촉하여 엽면으로부터의 흡수가 촉진되므로 정확한 표적을 정할 수 있습니다.

- 화학 관개법은 2017년 1억 9,940만 달러에서 2022년에는 3억 3,980만 달러로 성장했습니다. 2022년에는 곡물 및 곡류 분야에서 주로 사용되어 시장 점유율의 52.3%를 차지했습니다. 이는 이러한 작물에서 마이크로 관개 시스템이 보급되어 화학 관개에 적합하기 때문입니다.

- 엽면 살포는 잡초 방제에 몇 가지 장점이 있습니다. 엽면 살포는 제초제가 잡초의 잎에 직접 접촉하기 때문에 적을 좁힌 작용을 얻을 수 있습니다.

- 훈증에 의한 잡초 방제는 그 높은 특이성 및 환경에 대한 배려로부터, 적용 범위가 한정되기 때문에 다른 살포 방법에 비해 일반적이라고는 말할 수 없습니다. 그러나 다른 방법으로는 방제할 수 없는 엄청난 잡초를 효과적으로 방제할 수 있습니다.

- 농민들에게 각 적용 방법의 유효성, 특이성 및 필수성을 고려하면 제초제 시장은 2023년부터 2029년까지의 예측 기간 동안 CAGR 6.1%를 나타낼 것으로 예측됩니다.

중국의 제초제 시장 동향

윤작과 같은 대체 방법의 채택 및 제초제 살포의 기술적 진보-제초제 살포의 제어는 헥타르 당 소비량 감소에 기여

- 중국에서 제초제의 사용량은 몇 가지 중요한 요인에 의해 크게 감소했습니다. 그 원인으로는 윤작과 생물적 방제가 농업, 원예, 조경 등 다양한 분야에서 효과적인 잡초 관리에 빠뜨릴 수 없는 툴로 인식되어 채용되게 된 것을 들 수 있습니다.

- 윤작은 같은 땅에서 다른 작물을 특정 순서로 장기간에 걸쳐 재배하는 것입니다. 작물에 따라 성장 패턴과 필요한 영양이 다르기 때문에 잡초의 수명주기를 차단하는 데 도움이 됩니다. 작물을 번갈아 재배함으로써 중국 농부는 잡초의 성장주기를 방해하고 잡초의 개체수를 줄이고 제초제를 대량으로 사용할 필요성을 최소화합니다.

- 중국의 농가들은 다양한 작물의 잡초를 효과적으로 관리하기 위해 생물학적 방제제를 능숙하게 이용하여 제초제의 사용량을 현저하게 줄이고 있습니다. 이러한 생물학적 방제제의 도입은 매우 유익하며, 그 결과 다양한 농업 관행을 통해 제초제 살포에 대한 의존도가 감소하고 있습니다.

- 중국 농부들은 잡초 관리를 강화하기 위해 무인 항공 시스템(UAS)의 이미지 분석과 컴퓨터 비전 기술을 활용합니다. 이 접근법을 채택함으로써, 잡초가 발생하는 이랑을 확인하고, 잡초가 발생하지 않은 이랑은 그대로 두고 선택적으로 제초제를 정확하게 살포합니다. 이 혁신적인 방법은 불필요한 살포를 피함으로써 제초제 낭비를 효과적으로 최소화하고 헥타르 당 제초제 소비를 전반적으로 줄입니다.

- 농부는 유전자 변형 작물을 채택하여 추가 투자의 필요성을 최소화하고 헥타르 당 제초제 소비를 크게 줄입니다.

중국은 세계 최대의 글리포세이트 생산 및 수출국입니다.

- 잡초는 중국의 식량 안보에 중요한 작물 생산에 큰 제약이 되었습니다. 500종 이상의 침략적 잡초가 중국의 농업 생산과 생태계에 대한 위협이 되고 있습니다. 아트라진, 파라코트, 글리포세이트는 중국에서 일반적으로 사용되는 제초제입니다.

- 아트라진은 다양한 잎 잡초와 쌀과 식물의 방제에 널리 사용되는 제초제입니다. 중국에서는 연간 1만 6,000톤 이상(기술적으로 97%)의 아틀라진이 소비되고 있습니다. 아트라진은 주로 옥수수와 사탕수수 밭의 연간 잡초를 방제하는 데 사용됩니다. 중국은 세계 아트라진의 주요 공급국 중 하나입니다. 2022년 가격은 톤당 1만 3,700달러였습니다.

- 파라코트는 그라목슨의 유효 성분으로 잡초와 쌀 및 식물을 방제합니다. 또한 수확 전 면화와 같은 작물 건조에도 사용됩니다. 파라코트는 2022년에 1톤당 4,600달러로 평가되었습니다. 중국은 파라코트 수출 대국으로 파라코트 생산량의 80% 이상이 세계 각국에 수출되고 있습니다.

- 글리포세이트는 유기 인계 광역 스펙트럼 침투성 제초제이며 작물 건조제이기도 합니다. 2022년 가격은 톤당 1,100달러였습니다. 글리포세이트는 주로 쌀과, 수염과, 활엽수와 같은 잡초의 방제에 사용됩니다. 중국은 세계 최대의 글리포세이트 생산 및 수출국입니다. 중국에서의 글리포세이트 생산량은 2010년 31만 6,000톤에서 2017년 약 50만 5,000톤으로 증가했습니다. 2017년 중국은 30만 톤 이상의 글리포세이트 기술을 수출하여 세계 글리포세이트 수요의 절반 이상을 충족했습니다.

- 국내 날씨, 잡초 만연, 에너지 가격, 인건비 등의 요인이 유효 성분의 가격에 크게 영향을 미치고 있습니다.

중국의 제초제 산업 개요

중국의 제초제 시장은 적당히 통합되어 있으며 상위 5개사에서 64.14%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. Bayer AG, Corteva Agriscience, FMC Corporation, Nutrichem 및 UPL Limited(알파벳순 정렬).

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약 및 주요 조사 결과

제2장 보고서 제안

제3장 서문

- 조사의 전제조건 및 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 1헥타르당 농약 소비량

- 유효성분의 가격 분석

- 규제 프레임워크

- 중국

- 밸류체인 및 유통채널 분석

제5장 시장 세분화

- 적용 모드별

- 약제 살포

- 엽면 살포

- 훈증

- 토양 치료

- 작물 유형

- 상업 작물

- 과일 및 야채

- 곡물

- 콩류 및 지방종자

- 잔디 및 관상용

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일(세계 수준 개요, 시장 수준 개요, 주요 사업 부문, 재무, 직원 수, 주요 정보, 시장 순위, 시장 점유율, 제품 및 서비스, 최근 동향 분석 포함)

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Jiangsu Yangnong Chemical Co. Ltd

- Lianyungang Liben Crop Technology Co. Ltd

- Nutrichem Co. Ltd

- Rainbow Agro

- UPL Limited

- Wynca Group(Wynca Chemicals)

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계의 개요

- 개요

- Porter's Five Forces 분석 프레임워크

- 세계 밸류체인 분석

- 시장 역학(DROs)

- 정보원 및 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The China Herbicide Market size is estimated at 2.12 billion USD in 2025, and is expected to reach 2.81 billion USD by 2030, growing at a CAGR of 5.82% during the forecast period (2025-2030).

The market is driven by the need for effective control of herbicides

- Farmers in China employ various methods of herbicide application. The market for all these methods was valued at USD 1.78 billion in 2022.

- In 2022, the soil treatment method had the highest market share of USD 841.5 million, accounting for 47.2% of the total herbicide market. The popularity of soil treatment is due to its efficacy in utilizing pre-emergent herbicides, specifically targeting weed seeds, inhibiting their germination before crop sowing. With a market share of 31.9% in 2022, foliar application of herbicides offers numerous benefits in weed control. It provides precise targeting as the herbicides directly contact the weed's foliage, facilitating absorption through the leaf surfaces.

- The chemigation method grew from USD 199.4 million in 2017 to USD 339.8 million in 2022. In 2022, it was predominantly used in the grains and cereals segment, representing 52.3% of the market share. This is due to the prevalence of micro-irrigation systems in these crops, making them well-suited for chemigation.

- The foliar application offers several advantages in weed control. It provides targeted action, as the herbicides come into direct contact with the weed's foliage.

- The fumigation method of weed control is less common than other application methods due to its limited applicability attributed to its high specificity of usage and environmental concerns. However, it effectively controls a few tough weeds that other methods cannot.

- Considering the effectiveness, specificity, and essentiality of each application method for farmers, the market for herbicides is projected to register a CAGR of 6.1% during the forecast period from 2023 to 2029.

China Herbicide Market Trends

Adoption of alternative methods like crop rotation and technical advancements in herbicide application-controlled herbicide application contributes to lower consumption per hectare

- The usage of herbicides in China has reduced significantly due to several key factors. Some factors contributing to this are the growing recognition and adoption of crop rotation and biological controls as essential tools for effective weed management in various sectors, such as agriculture, horticulture, and landscaping.

- Crop rotation is a practice where different crops are grown in a specific sequence on the same land over time. This helps break the lifecycle of weeds, as different crops have different growth patterns and nutritional needs. By alternating crops, Chinese farmers have disrupted weed growth cycles, reduced weed populations, and minimized the need for higher use of herbicides.

- Chinese farmers skillfully employ biocontrol agents to effectively manage weeds in a wide array of crops, thereby leading to a notable decrease in the usage of herbicides. The implementation of these biocontrol agents is highly beneficial, resulting in reduced reliance on herbicide applications throughout various agricultural practices.

- Chinese farmers use unmanned aerial systems (UAS) imagery analysis and computer vision techniques to enhance weed management practices. By employing this approach, they identify weed-infested rows and selectively apply herbicides accurately, leaving non-weed-infested rows untouched. This innovative method effectively minimizes the wastage of herbicides by avoiding unnecessary applications and reducing overall herbicide consumption per hectare.

- Farmers adopt genetically modified organism (GMO) crops to minimize additional investment requirements, resulting in a significant reduction in herbicide consumption per hectare.

China is the world's largest producer and exporter of glyphosate

- Weeds are a major constraint to crop production, which is crucial for food security in China. Over 500 invasive weeds are an increasing threat to agricultural production and ecosystems in China. Atrazine, paraquat, and glyphosate are commonly used herbicides in China.

- Atrazine is an herbicide widely used to control various broadleaved weeds and grasses. China consumes more than 16,000 ton (97% technical) of atrazine annually. Atrazine is mainly used to control annual weeds in corn or sugarcane fields. China is one of the major suppliers of atrazine worldwide. It was priced at USD 13.7 thousand per metric ton in 2022.

- Paraquat is the active ingredient of gramoxone, which controls weeds and grasses. It is also used for desiccating crops, like cotton, before harvest. Paraquat was valued at USD 4.6 thousand per metric ton in 2022. China is a major paraquat export country, and over 80% of its paraquat output is exported to countries worldwide.

- Glyphosate is an organophosphorus broad-spectrum systemic herbicide and crop desiccant. It was priced at USD 1.1 thousand per metric ton in 2022. Glyphosate is mainly used to control weeds like grasses, sedges, and broadleaves. China is the world's largest producer and exporter of glyphosate in the world. The output of glyphosate in China increased from 316,000 ton in 2010 to about 505,000 ton in 2017. In 2017, China exported over 300,000 ton of glyphosate technical, which satisfied more than half of the global glyphosate demand.

- Factors like weather conditions, weed infestation, energy prices, and labor costs in the country majorly influence the prices of active ingredients.

China Herbicide Industry Overview

The China Herbicide Market is moderately consolidated, with the top five companies occupying 64.14%. The major players in this market are Bayer AG, Corteva Agriscience, FMC Corporation, Nutrichem Co. Ltd and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 China

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Bayer AG

- 6.4.3 Corteva Agriscience

- 6.4.4 FMC Corporation

- 6.4.5 Jiangsu Yangnong Chemical Co. Ltd

- 6.4.6 Lianyungang Liben Crop Technology Co. Ltd

- 6.4.7 Nutrichem Co. Ltd

- 6.4.8 Rainbow Agro

- 6.4.9 UPL Limited

- 6.4.10 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

샘플 요청 목록