|

시장보고서

상품코드

1683986

유럽의 제초제 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Europe Herbicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

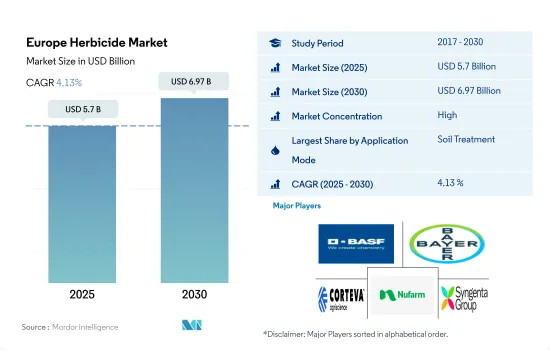

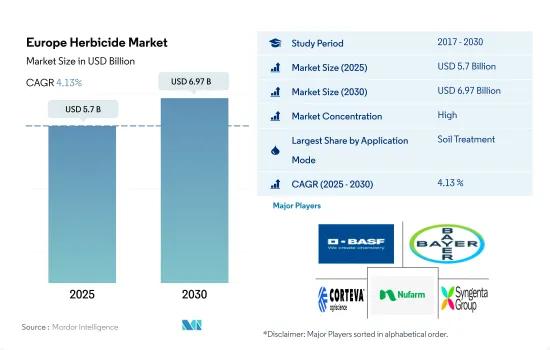

유럽의 제초제 시장 규모는 2025년에 57억 달러로 추정되고, 2030년에는 69억 7,000만 달러에 이를 것으로 예측되며, 예측 기간 중 2025년부터 2030년까지 CAGR 4.13%로 성장할 전망입니다.

유럽에서는 토양 처리가 제초제 살포의 주요 수단으로 가장 중요합니다.

- 유럽에서는 농업에서 잡초를 효율적으로 관리하기 위해 다양한 제초제 살포 방법이 채택되었습니다. 적절한 살포 방법을 선택함으로써 농부는 비용 효율적인 솔루션을 실현하고 대상 지역을 정확하게 커버하며 낭비를 최소화할 수 있습니다. 이 효율성 향상은 제초제 사용량을 최적화하여 궁극적으로 농부의 투입 비용을 절감합니다.

- 농업 관행에서는 토양 살포가 제초제 사용의 우세한 모드로 두드러졌으며, 2022년에는 제초제 살포 부문 전체의 48.2%를 차지했습니다. 이 방법은 주로 곡물 및 곡류의 재배로 채용되고 있어 62.0%로 최대 시장 점유율을 차지하고 있습니다. 제초제의 토양 처리가 선호되는 이유는 잡초의 성장을 방지하거나 최소화함으로써 곡류 및 곡물의 품질을 보호하는 효과가 있기 때문입니다. 이 제초제는 잡초가 발생하기 전이나 재배 초기 단계에서 잡초를 방제하는 데 효과적입니다.

- 또한 엽면 살포법은 금액 기준으로 2위 시장 점유율을 확보했으며 2022년에는 30.6%를 차지했습니다. 이 살포 기술은 잡초 방제에 유리한 것으로 입증되었으며, 특히 정확한 타겟팅이 필요한 작물, 예를 들어 대상 식물의 잎에 직접 살포하는 경우에 유리합니다. 이 방법은 출처 후 잡초를 방제하는 데 효과적이며 많은 농작물에서 일반적으로 사용됩니다.

- 유럽의 농업 부문에서 제초제 사용은 작물 생산성을 최적화하고 전반적인 수익성을 높이는 데 중점을 둡니다. 미국 제초제 시장 점유율의 CAGR은 4.1%로 예측되고 있으며, 시장은 큰 성장이 예상되고 있습니다.

밀, 옥수수, 사탕무 등의 주요 작물에서 잡초의 확산이 확대되고, 이러한 작물의 재배 면적이 확대되고 있다는 것이 시장을 견인할 가능성이 있습니다.

- 곰팡이병과 해충과는 별도로, 잡초는 유럽 농업 부문의 위협이 되고 있으며, 이 지역 주요 작물에 심각한 피해를 초래하고 있습니다. 이 지역의 제초제 소비는 시장 점유율의 대부분을 차지했으며 유럽 작물 보호 화학 시장의 34.7%를 차지했으며 2022년 시장 가치는 49억 3,000만 달러였습니다.

- 2022년 시장 점유율은 61.7%로 곡물 및 곡류가 유럽의 제초제 시장을 독점했습니다. 이러한 이점은 이러한 작물에서 재배 면적 증가와 잡초 감염 증가에 기인합니다. 작물의 손실을 일으키는 잡초가 많이 있습니다. 실시한 실험에 따르면, 연구자들은 프랑스 밀 재배에서 108종의 잡초를 발견했고, 유럽 5개국의 밀 재배(덴마크, 핀란드, 독일, 라트비아, 스웨덴)에서는 197종의 잡초를 발견했습니다. 이러한 잡초종 증가는 밀, 옥수수, 사탕무 등의 주요 작물에 피해를 끼쳤습니다. 매년 평균적으로 잡초가 통제되지 않기 때문에 밀의 수확 손실은 25-30%, 옥수수의 수확 손실은 60-85%, 사탕무의 수확 손실은 90-95%에 달할 전망입니다.

- 유럽 국가에서는 토양 처리에 의한 제초제 치료가 인기를 끌고 있습니다. 이 적용 형태는 2022년에 48.2%의 주요 시장 점유율을 차지했습니다. 이 이점은 초기 성장 단계에서 잡초의 방제 효과와 크게 관련되어 작물의 발아가 빨라지고 나중 단계에서 제초제의 필요성이 감소합니다. 이러한 이점으로부터, 이 적용 모드는 성장할 것으로 예측되며, 예측 기간 중의 추정 CAGR은 4.1%로 전망됩니다.

- 유럽의 제초제 시장은 주요 작물에서 잡초 만연 증가에 견인되어 예측 기간 동안 CAGR 4.0%를 기록하여 성장할 것으로 예측됩니다.

유럽의 제초제 시장 동향

농부들은 잡초 문제를 관리하는 중요한 도구로 제초제에 대한 의존도를 높일 것으로 예상됩니다.

- 유럽에서는 주로 다양한 요인으로 제초제 소비가 크게 증가하고 있습니다. 중요한 요인 중 하나는 수백만 명의 사람들이 농촌에서 도시로 이주했기 때문에 수작업으로 제초할 수 있는 노동자가 부족하다는 것입니다. 그 결과, 제초제의 사용은 작물의 수확량과 양을 모두 높이는 효과적이고 비용 효율적인 방법으로 부상했습니다. 이 동향은 2019년부터 2022년에 걸쳐 특히 두드러졌으며, 이 지역의 제초제 소비량은 31.4% 증가했습니다.

- 유럽 국가들 중 독일과 프랑스는 이 지역의 기타 국가에 비해 제초제 사용률이 높습니다. 2022년 독일은 1헥타르당 3,100의 사용률을 기록했고, 프랑스는 2,800으로 약간 차이가 났습니다. 이 나라들은 농업 생산의 안정성, 양, 식량 안보를 보장하기 위해 제초제를 포함한 화학 농약의 살포에 크게 의존합니다. 잡초의 지속성과 적응성으로 인해 이 지역에서는 제초제의 살포율을 높여야 합니다.

- 또한 유럽의 인구 증가로 향후 30년간 식량 수요가 급증할 것으로 예상됩니다. 그 결과, 수확량을 늘리고, 작물을 유해한 잡초로부터 지키는 것으로, 식량 생산에 대한 요구의 고조에 대응하기 위해, 제초제 수요도 높아질 것으로 예상됩니다.

- 따라서 식량 수요 증가, 노동력 부족, 기후 변화가 예측 기간(2023-2029년)에 있어서 제초제의 소비를 촉진할 것으로 예상됩니다. 농부들은 앞으로 수년간 이러한 과제를 해결하고, 증가하는 식량 수요를 충족하고 지속 가능한 농업 생산성을 확보하기 위한 중요한 수단으로 제초제에 대한 의존도를 높여 나갈 것으로 보입니다.

유럽 국가 중 2022년 글리포세이트 가격은 독일과 프랑스가 가장 높았으며 톤당 1,150달러였습니다.

- 2022년 메트리부진은 1톤당 16,700달러로 평가되었습니다. 메트리부진은 특정 활엽 잡초 및 쌀과 잡초를 선택적으로 방제하는 제초제로 널리 사용되는 유기 합성 화합물입니다. 메트리부진의 용도는 야채와 밭작물, 레크리에이션 지역의 잔디, 비 농경지에 사용됩니다. 제제로는 습윤성 분말, 유화성 농축제, 수분산성 입자(건조 유동성), 유동성 농축제 등이 있습니다. 메트리부진의 살포에는 공중 살포, 화학 살포, 지상 살포 등 다양한 방법이 이용됩니다.

- 펜디메탈린 펜디메탈린은 잔류활성을 가진 출아 전 제초제로 원예, 잔디, 임업 등 다양한 작물의 일년생초와 활엽 잡초에 대해 폭넓은 방제효과를 발휘합니다. 주요 작용 메커니즘은 영향을 받기 쉬운 잡초의 세포 분열과 신장을 억제하고 뿌리와 싹의 성장을 방해하는 것입니다. 2022년 이 제초제의 가격은 톤당 3,300달러였습니다.

- 글리포세이트계 제초제는 유럽에서 가장 널리 사용되고 있는 제초제로서의 지위를 유지하고 있으며 EU 제초제 시장의 33%를 차지하고 있습니다. 2022년 글리포세이트 제초제의 가격은 톤당 1,200달러였습니다. 글리포세이트계 제초제의 사용량은 급격히 증가하고 있으며, 유럽, 특히 EU의 대규모 농업 회원국에서의 판매량은 여전히 큽니다. Farm Accountancy Data Network(FADN)의 데이터는 농부의 농약에 대한 지출이 전반적으로 증가하고 있음을 보여줍니다.

- EU 국가 중 2022년 글리포세이트의 가격은 독일과 프랑스가 가장 높았으며 각각 1톤당 1,150달러, 영국은 1톤당 1,140달러였습니다.

유럽의 제초제 산업 개요

유럽의 제초제 시장은 상당히 통합되어 있으며 상위 5곳에서 65.24%를 차지합니다. 이 시장 주요 기업은 다음과 같습니다. BASF SE, Bayer AG, Corteva Agriscience, Nufarm Ltd 및 Syngenta Group(알파벳순 정렬).

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약 및 주요 조사 결과

제2장 보고서 제안

제3장 서문

- 조사 전제조건 및 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 1헥타르당 농약 소비량

- 유효성분의 가격 분석

- 규제 프레임워크

- 프랑스

- 독일

- 이탈리아

- 네덜란드

- 러시아

- 스페인

- 우크라이나

- 영국

- 밸류체인 및 유통채널 분석

제5장 시장 세분화

- 적용 모드별

- 화학 관개

- 잎면 살포

- 훈증

- 토양 치료

- 작물 유형별

- 상업 작물

- 과일 및 야채

- 곡물

- 콩류 및 지방종자

- 잔디 및 관상용

- 국가별

- 프랑스

- 독일

- 이탈리아

- 네덜란드

- 러시아

- 스페인

- 우크라이나

- 영국

- 기타 유럽

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일(세계 수준 개요, 시장 수준 개요, 주요 사업 부문, 재무, 직원 수, 주요 정보, 시장 순위, 시장 점유율, 제품 및 서비스, 최근 동향 분석 포함)

- ADAMA Agricultural Solutions Ltd.

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Nufarm Ltd

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

- Wynca Group(Wynca Chemicals)

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계의 개요

- 개요

- Porter's Five Forces 분석 프레임워크

- 세계 밸류체인 분석

- 시장 역학(DROs)

- 정보원 및 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Europe Herbicide Market size is estimated at 5.7 billion USD in 2025, and is expected to reach 6.97 billion USD by 2030, growing at a CAGR of 4.13% during the forecast period (2025-2030).

In Europe, soil treatment holds the utmost importance as the primary mode of herbicide application

- In Europe, various modes of herbicide application are employed to efficiently manage weeds in agriculture. By selecting appropriate application methods, farmers can achieve cost-effective solutions, ensuring precise coverage of targeted areas and minimizing wastage. This enhanced efficiency optimizes herbicide usage, ultimately leading to reduced input costs for farmers.

- In agricultural practices, soil application stands out as the predominant mode of herbicide usage, which represented 48.2% of the total herbicide application segment in 2022. This method is majorly employed in the cultivation of grains and cereals, which holds the largest market share at 62.0%. The preference for soil treatment of herbicides is driven by their efficacy in protecting the quality of grains and cereals by preventing or minimizing weed growth. They are effective in controlling weeds during their pre-emergent and early growth stages.

- Furthermore, the foliar application method secured the second-largest market share by value, which accounted for 30.6% in 2022. This application technique has proven to be advantageous for weed control, particularly in crops that require accurate targeting, for instance, when applied directly onto the leaves of target plants. This method is effective for controlling post-emergence weeds and is commonly used in many agricultural crops.

- In the European agricultural sector, herbicide usage is focused on optimizing crop productivity and enhancing overall profitability. The market is expected to witness significant growth, with a projected CAGR of 4.1% in terms of the US herbicide market share.

Growing weed infestations in major crops like wheat, maize, and sugar beet and extending cultivation area under this crops may drive the market

- Apart from fungal diseases and insect pests, weeds are becoming a threat to the European agriculture sector, causing huge damage to the major crops in the region. The consumption of herbicides in the region occupied a majority market share, which accounted for 34.7% of the European crop protection chemical market, with a market value of USD 4.93 billion in 2022.

- Grains and cereal crops dominated the European herbicide market with a 61.7% market share in 2022. This dominance was attributed to the higher cultivation area and increased weed infections in these crops. There are numerous weed species causing crop losses. According to an experiment conducted, researchers found 108 weed species in France's wheat crops, and 197 weed species were found in five European countries' wheat cultivations (Denmark, Finland, Germany, Latvia, and Sweden). These increased weed species caused damage to major crops such as wheat, maize, sugar beet, and other crops. On average, every year, uncontrolled weeds cause wheat crop loss of 25-30%, maize crop loss of 60-85%, and sugar beet crop loss of 90-95%.

- The application of herbicide products through soil treatment is gaining popularity in European countries. This application mode occupied a major market share of 48.2% in 2022. The dominance is majorly related to the effectiveness of controlling weeds in the early growth stage, which could give more strength to the crops for faster germination, reducing the herbicide's necessity in the later stages. Due to these benefits, the application mode is projected to grow, registering an estimated CAGR of 4.1% during the forecast period.

- The European herbicides market is anticipated to grow, registering a CAGR of 4.0% during the forecast, driven by increased weed infestations in major crops.

Europe Herbicide Market Trends

Farmers are expected to increasingly rely on herbicides as a key tool to manage weed challenges

- Europe has experienced substantial growth in the consumption of herbicides, primarily driven by various factors. One significant factor is the shortage of workers available for manual weeding, as millions of people have migrated from rural to urban areas. As a result, herbicide usage has emerged as an effective and cost-efficient method to enhance both the quality and quantity of crop yields. This trend was particularly notable from 2019 to 2022, with herbicide consumption in the region increasing by 31.4%.

- Among European countries, Germany and France have high herbicide usage rates compared to others in the region. In 2022, Germany recorded a usage rate of 3.1 thousand per hectare, while France followed closely with 2.8 thousand per hectare. These countries heavily rely on the application of chemical pesticides, including herbicides, to ensure the stability, quantity, and food security of their agricultural production. The persistence and adaptability of weeds have necessitated higher rates of herbicide application in these regions.

- Furthermore, the increasing European population has projected a rapid growth in food demand over the next three decades. Consequently, the demand for herbicides is also expected to rise to meet the increasing need for food production by increasing the yield and protecting crops from harmful weeds.

- Therefore, the rising demand for food, labor shortages, and climate change are expected to drive the consumption of herbicides during the forecast period (2023-2029). Farmers will increasingly rely on herbicides as a key tool over the coming years to address these challenges and meet the increasing food demand, ensuring sustainable agricultural productivity.

Among countries in Europe, the price of glyphosate in 2022 was highest in Germany and France, priced at USD 1.15 thousand per metric ton

- In 2022, Metribuzin was valued at USD 16.7 thousand per metric ton. It represents a synthetic organic compound widely utilized as a herbicide with selective control over specific broadleaf weeds and grassy weed species. The applications of Metribuzin are used in vegetable and field crops, turf grasses in recreational areas, and non-crop areas. Its available formulations include wettable powder, emulsifiable concentrate, water-dispersible granules (dry flowable), and flowable concentrate. Various methods, such as aerial, chemigation, and ground application, are employed for Metribuzin's application.

- Pendimethalin is a pre-emergence herbicide with residual activities that deliver broad-spectrum control against annual grasses and broadleaf weeds across different crops, including horticultural, turf, and forestry. Its primary mode of action involves inhibiting cell division and elongation in susceptible weeds, thus impeding root and shoot growth. In 2022, this herbicide was priced at USD 3.3 thousand per metric ton.

- Glyphosate-based herbicides maintain their position as the most widely used herbicide in Europe, which accounts for 33% of the EU herbicide market. In 2022, the price of glyphosate-based herbicides stood at USD 1.2 thousand per metric ton. The usage of glyphosate-based herbicides continues to witness significant growth, while sales in Europe, especially in larger agricultural member states of the European Union, remain substantial. Data from the Farm Accountancy Data Network (FADN) indicates a general increase in farmers' spending on pesticides.

- Among EU countries, the price of glyphosate in 2022 was highest in Germany and France, each priced at USD 1.15 thousand per metric ton, followed by the United Kingdom at USD 1.14 thousand per metric ton.

Europe Herbicide Industry Overview

The Europe Herbicide Market is fairly consolidated, with the top five companies occupying 65.24%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, Nufarm Ltd and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 France

- 4.3.2 Germany

- 4.3.3 Italy

- 4.3.4 Netherlands

- 4.3.5 Russia

- 4.3.6 Spain

- 4.3.7 Ukraine

- 4.3.8 United Kingdom

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Netherlands

- 5.3.5 Russia

- 5.3.6 Spain

- 5.3.7 Ukraine

- 5.3.8 United Kingdom

- 5.3.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd.

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Nufarm Ltd

- 6.4.7 Sumitomo Chemical Co. Ltd

- 6.4.8 Syngenta Group

- 6.4.9 UPL Limited

- 6.4.10 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

샘플 요청 목록