|

시장보고서

상품코드

1683991

인도의 제초제 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)India Herbicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

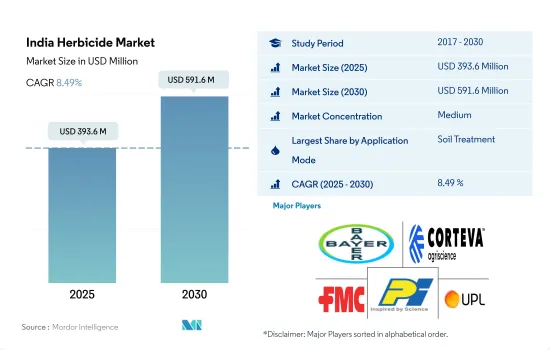

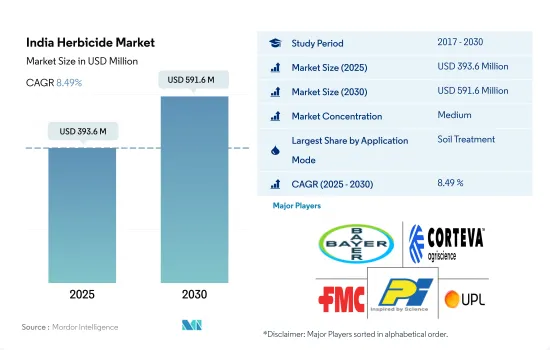

인도의 제초제 시장 규모는 2025년에 3억 9,360만 달러로 추정되고, 2030년에는 5억 9,160만 달러에 이를 것으로 예측되며, 예측 기간 중 2025년부터 2030년까지 CAGR 8.49%로 성장할 전망입니다.

가장 중요한 제초제 살포의 주요 모드는 토양 처리 살포입니다.

- 잡초는 인도의 농업 부문에 큰 위협을 가져오며 연간 약 45.0%의 상당한 작물 손실을 초래합니다. 농부는 윤작, 문화 관행, 수작업 제초, 화학 제초제 살포 등 다양한 전략을 실시하여 잡초를 방제하고 있습니다.

- 그러나 대체 방법에 따른 생산비용 상승으로 농작물 잡초에 대처하기 위해 화학제초제를 채용하는 농가가 늘고 있습니다. 농부는 제초제를 살포하여 잡초의 성장을 효율적으로 제어하고 농업 수율에 대한 악영향을 최소화할 수 있습니다.

- 잡초 방제에는 다양한 살포 방법이 있습니다. 제초제를 이용한 토양 처리는 잡초의 성장 초기 단계에서 관리에 효과적이기 때문에 큰 점유율을 차지합니다. 이 살포 방법은 이삭 이전의 잡초를 방제하는 데 유리하기 때문에 곡류 및 곡물을 재배하는 농가들 사이에서 인기를 얻고 있습니다.

- 토양 처리는 제초제를 토양에 직접 살포하는 것으로, 잡초의 씨앗이나 자라기 시작한 모종을 효과적으로 노려, 그 성장과 정착을 저해할 수 있습니다. 토양 처리를 통해 농부는 잡초 문제를 적극적으로 해결하고 중요한 초기 단계에서 작물의 건강한 성장을 가속할 수 있습니다.

- 토양 처리에 이어 엽면 살포나 화학적 살포 등의 다른 살포 방법도 국내에서는 잡초 방제를 위해 인기가 급상승하고 있습니다. 이러한 모드는 그 효과를 입증하고 작물의 생산성 향상에 다양한 이점을 제공합니다. 2022년에는 엽면 살포가 33.2%, 화학 살포가 18.7%로 큰 시장 점유율을 기록했습니다.

인도의 제초제 시장 동향

작물의 손실 확대로 인한 잡초 과제를 관리하기 위해 제초제의 소비 확대가 예상됩니다.

- 기계화된 화학 기반 잡초 방제 접근법은 기존의 수작업에 의한 제초 방법을 빠르게 대체합니다. 농부는 소규모 및 대규모 농업에서 잡초를 관리하는 비용 효과적이고 효율적인 방법으로 제초제를 사용합니다.

- 인도에서는 농작물의 생산성을 향상시킬 목적으로 농가가 작년 주기를 1년 이내에 여러 번 반복하는 작물 집약화를 실천하고 있습니다. 이 작물 집약화에 의해 잡초압이 높아지는 경우가 많고, 작물의 생산성을 유지하기 위해 제초제의 살포가 필요합니다. 헥타르당 제초제 소비량은 평균 49.7g/ha였습니다.

- 헥타르당 제초제 소비량은 작물 유형, 잡초 침입 수준, 농업 관행, 잡초 관리 전략 등 여러 측면에 따라 달라집니다. 인도의 헥타르당 제초제 소비량은 2017년부터 2022년까지 6.0% 증가했습니다. 인도의 1인당 제초제 사용량이 증가하여 헥타르당 평균 농업 생산량을 높였습니다. 제초제의 장점에 대한 농가의 의식 증가와 더불어, 광범위한 제초제가 시장에 나와 있는 것이 사용량 증가에 기여하고 있습니다.

- 제초제 내성면(Bt면)과 같은 제초제 내성의 특성을 가지는 유전자 변형(GM) 작물의 이용, 유전자 변형을 위한 '버나제 및 버스터' 기술을 이용한 DMH-11과 같은 하이브리드 머스타드의 개발에 의해 농가는 잡초 관리에 의해 폭넓게 제초제를 사용할 수 있게 되었습니다. 이러한 개선 작물은 특정 제초제를 견딜 수 있도록 설계되었으며, 농부들은 효과적인 잡초 방제를 위해 제초제를 더 많이 사용할 수 있습니다.

아트라진, 파라코트, 글리포세이트는 인도에서 사용되는 주요 제초제입니다.

- 인도에는 다양한 농업 기후와 토양이 있습니다. 다양성이 높은 농업과 농업 시스템은 다양한 유형의 잡초 문제로 고통받고 있습니다. 잡초는 제품의 품질을 손상시키고 건강과 환경에 해를 끼칠 뿐만 아니라 10%에서 80%의 작물 수율 손실을 유발합니다. 아트라진, 파라코트, 글리포세이트가 국내에서 사용되는 주요 제초제입니다.

- 아트라진은 인도의 옥수수와 벼농사에서 에키노크로아, 엘신속, 아마란사스빌리지스 등의 활엽잡초나 벼과 잡초의 방제에 널리 사용되는 제초제입니다. 제초제는 2022년에 13,500달러로 평가되었습니다. 인도는 세계에서 가장 큰 아트라진 기술 수입국이며 주로 중국, 이탈리아, 이스라엘에서 수입하고 있습니다.

- 파라코트는 광범위한 접촉형 제초제로 2022년에는 4,600달러를 차지했습니다. 인도에서는 총 14유형의 파라코트 디클로라이드의 상품명이 판매되고 있습니다. 곡물, 콩류, 기름씨, 야채, 환금작물 등 약 25개의 작물에 사용되고 있습니다. 그러나 중앙 살충제 위원회 및 등록 위원회(CIBRC)가 사용을 승인하고 있는 것은 9작물뿐입니다.

- 글리포세이트는 비선택성 제초제로 Cynodon dactylon, Imperata cylindrica, Arundinella bengalensis와 같은 잡초를 방제하는 데 사용됩니다. 2022년 9월 인도 정부가 발행한 통지에 따르면, 글리포세이트는 다원과 비농경지에서만 사용할 수 있습니다. 2022년에는 1,100달러로 평가되었습니다.

- 인도 정부는 농촌 경제를 활성화하고 농부의 수입을 늘리기 위해 지속적으로 예산을 지원해 왔습니다. 22년도 예산에서는 농업 분야와 농촌 경제의 개선을 위해, 많은 시책이나 대처가 제안 및 발표되었습니다. 이것은 이 나라의 제초제 가격에 추가적인 영향을 미칠 것으로 예상됩니다.

인도의 제초제 산업 개요

인도의 제초제 시장은 적당히 통합되어 있으며 상위 5곳에서 61.28%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. Bayer AG, Corteva Agriscience, FMC Corporation, PI Industries 및 UPL Limited(알파벳순 정렬).

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약 및 주요 조사 결과

제2장 보고서 제안

제3장 서문

- 조사 전제조건 및 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 1헥타르당 농약 소비량

- 유효성분의 가격 분석

- 규제 프레임워크

- 인도

- 밸류체인 및 유통채널 분석

제5장 시장 세분화

- 적용 모드별

- 화학 관개

- 엽면 살포

- 훈증

- 토양 치료

- 작물 유형별

- 상업 작물

- 과일 및 야채

- 곡물

- 콩류 및 지방종자

- 잔디 및 관상용

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일(세계 수준 개요, 시장 수준 개요, 주요 사업 부문, 재무, 직원 수, 주요 정보, 시장 순위, 시장 점유율, 제품 및 서비스, 최근 동향 분석 포함)

- ADAMA Agricultural Solutions Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Gharda Chemicals Ltd

- PI Industries

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계의 개요

- 개요

- Porter's Five Forces 분석 프레임워크

- 세계 밸류체인 분석

- 시장 역학(DROs)

- 정보원 및 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The India Herbicide Market size is estimated at 393.6 million USD in 2025, and is expected to reach 591.6 million USD by 2030, growing at a CAGR of 8.49% during the forecast period (2025-2030).

The primary mode of herbicide application of utmost significance is the soil treatment application

- Weeds pose a significant threat to the agricultural sector in India, resulting in substantial annual crop losses of around 45.0%. Farmers are implementing various strategies, including crop rotation, cultural practices, manual weeding, and spraying chemical herbicides to control weeds.

- However, due to rising production costs associated with alternative methods, more farmers are adopting chemical herbicides to tackle weeds in their crops. Farmers can efficiently control weed growth and minimize the detrimental effects on their agricultural yield by spraying herbicides.

- There are various application modes for weed control. Soil treatment using herbicides holds a prominent share due to its effectiveness in managing weeds during their early growth stages. This application method has gained popularity among farmers cultivating grain and cereal crops due to its advantageous effects in controlling pre-emergence weeds.

- Soil treatment involves applying herbicides directly to the soil, where they can effectively target weed seeds and emerging seedlings, inhibiting their growth and establishment. By employing soil treatment applications, farmers can proactively address weed issues and promote healthier crop growth in the crucial early stages.

- Following the soil treatment mode, other application modes such as foliar and chemigation have witnessed a surge in popularity for weed control in the country. These modes have demonstrated their effectiveness and offered various benefits in enhancing crop productivity. In 2022, foliar and chemigation registered a significant market share of 33.2% and 18.7%, respectively.

India Herbicide Market Trends

Herbicide consumption is anticipated to expand to manage the weed challenges due to growing losses of crops

- Mechanized and chemical-based weed control approaches are rapidly replacing traditional manual weeding methods. Farmers use herbicides as a cost-effective and efficient way to manage weeds in small-scale and large-scale farming operations.

- With the aim of increasing crop productivity, farmers in India have been practicing crop intensification, which involves repeated cropping cycles within a year. This intensification frequently results in increased weed pressure, necessitating the application of herbicides to maintain crop productivity. The average herbicide consumption per hectare accounted for 49.7 g/ha.

- Herbicide consumption per hectare can vary based on numerous aspects such as crop type, weed infestation level, agricultural practices, and weed management strategies. The consumption of herbicides in India per hectare increased by 6.0% from 2017 to 2022. Herbicide usage per capita in India increased to boost the average agricultural output per hectare. Farmers' growing awareness of the advantages of herbicides, along with the availability of a wide range of herbicides on the market, has contributed to their increased usage.

- The utilization of genetically modified (GM) crops that possess herbicide-tolerant characteristics, like herbicide-tolerant cotton (Bt cotton), and the development of hybridized mustard such as DMH-11 using the "barnase/barstar" technique for genetic modification has enabled farmers to employ herbicides more extensively in weed management. These modified crops are designed to endure specific herbicides, empowering farmers to utilize herbicides to a greater extent for effective weed control.

Atrazine, paraquat, and glyphosate are major herbicides used in the country

- India has a wide range of agroclimates and soil types. The highly diverse agriculture and farming systems are beset with different types of weed problems. Weeds cause 10% to 80% crop yield losses, besides impairing product quality and causing health and environmental hazards. Atrazine, paraquat, and glyphosate are major herbicides used in the country.

- Atrazine is an herbicide widely used to control broadleaf and grassy weeds like Echinocloa, Elusine spp, and Amaranthus viridis in maize and rice crops in India. The herbicide was valued at USD 13.5 thousand in 2022. India is the world's largest importer of Atrazine technical and imports majorly from China, Italy, and Israel.

- Paraquat is a broad-spectrum contact herbicide, accounting for USD 4.6 thousand in 2022. A total of 14 commercial names of paraquat dichloride are sold in India. It is used in about 25 crops, including cereals, pulses, oil seeds, vegetables, and cash crops. However, the Central Insecticide Board & Registration Committee (CIBRC) has approved its use in only nine crops.

- Glyphosate is a non-selective herbicide used to control weeds like Cynodon dactylon, Imperata cylindrica, and Arundinella bengalensis. As per the notice issued by the Government of India in September 2022, glyphosate can be used only in tea gardens and non-crop areas. It was valued at USD 1.1 thousand in 2022.

- The Government of India has continuously provided budgetary support to revive the rural economy and increase farmers' income. A number of measures and initiatives were proposed and announced during the FY22 budget for the improvement of the agriculture sector and the rural economy. This is expected to influence the prices of herbicides in the country further.

India Herbicide Industry Overview

The India Herbicide Market is moderately consolidated, with the top five companies occupying 61.28%. The major players in this market are Bayer AG, Corteva Agriscience, FMC Corporation, PI Industries and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 India

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Gharda Chemicals Ltd

- 6.4.7 PI Industries

- 6.4.8 Sumitomo Chemical Co. Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

샘플 요청 목록