|

시장보고서

상품코드

1684002

남미의 제초제 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)South America Herbicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

남미의 제초제 시장 규모는 2025년에 154억 7,000만 달러로 추정되고, 2030년에는 196억 4,000만 달러에 이를것으로 예측되며, 예측 기간(2025-2030년)의 CAGR은 4.89%를 나타낼 것으로 전망됩니다.

농산물에 대한 수요 증가와 잡초의 효과적인 관리에 대한 관심이 시장의 성장을 강화하고 있습니다.

- 화학 처리는 2022년 시장 가치의 19.7%를 차지했습니다. 관개 인프라가 잘 발달된 지역에서 인기가 높습니다. 점적 관개 시스템의 채택이 증가함에 따라 향후 몇 년 동안 시장의 성장을 촉진할 것으로 예상됩니다.

- 잎 표면 살포는 두 번째로 큰 점유율을 차지하고 있으며 예측 기간(2023-2029년) 동안 5.1%의 연평균 성장률을 나타낼 것으로 예상됩니다. 제초제는 식물의 잎에 직접 적용되어 식물 전체에 흡수되고 이동하여 원치 않는 식물을 제어합니다. 제초제 사용량을 최소화하면서 잡초를 표적화하여 효율적으로 방제할 수 있어 농업 분야에서 널리 사용되고 있습니다.

- 훈증은 2023년부터 2029년 사이에 7,830만 달러의 성장이 예상됩니다. 이 방법은 토양이나 온실과 같은 폐쇄 공간에서 해충과 잡초를 제거하기 위해 가스 형태의 제초제를 사용합니다. 이 방법은 기체 제초제를 사용하여 토양이나 온실과 같은 밀폐된 공간에서 해충과 잡초를 방제하는 것입니다. 일반적으로 넓은 지역을 처리하는 데 사용되며 특히 토양 매개 해충에 효과적입니다.

- 토양처리 분야는 예측 기간(2023-2029년) 동안 5.4%의 연평균 성장률을 나타낼 것으로 예상됩니다. 이 방법은 지속적인 잡초 문제를 심거나 관리하기 전에 잡초를 방제하기 위해 제초제를 토양에 직접 적용하는 것을 포함합니다. 토양 처리는 작물의 생육과 성장에 유리한 환경을 조성하는 데 도움이 될 수 있습니다.

- 남미의 제초제 시장은 예측기간 중(2023-2029년) 50억 4,000만 달러의 성장이 예상됩니다. 남미에서 제초제에 대한 수요는 잡초 성장을 효과적으로 제어하고 작물 수확량을 극대화하기 위해 이러한 적용 방법을 채택하는 데 영향을 받습니다. 변화하는 농업 관행, 작물 유형, 잡초 압력 및 해충 관리 전략이 제초제 제품에 대한 수요를 주도하고 있습니다.

잡초 방제의 이점과 수확량에 미치는 영향에 대한 인식이 높아지면서 성장세를 주도했습니다.

- 남미는 2022년 전 세계 제초제 시장의 35.5%를 차지했습니다. 남미의 제초제 시장은 아르헨티나, 브라질, 칠레 및 기타 남미 지역을 포함한 다양한 지역에서 성장하고 있습니다. 이들 국가는 광활한 농지를 보유한 주요 농업 생산국으로, 잡초 개체군을 관리하고 최적의 작물 수확량을 확보하기 위해 제초제 사용이 필수적입니다.

- 브라질은 이 시장에서 53.6%의 주요 점유율을 차지하고 있으며, 이 기간 동안 5.2%의 연평균 성장률을 나타낼 것으로 예상됩니다. 브라질의 농부들은 잡초 방제의 이점과 잡초가 농작물 수확량에 미치는 영향에 대해 점점 더 많이 인식하고 있습니다. 잡초로 인한 농작물 손실이 증가하면 제초제 사용률이 높아질 수 있습니다.

- 2022년 아르헨티나는 남미의 제초제 시장에서 35.1%의 점유율을 차지하며 다른 국가에 비해 가장 빠른 5.6%의 연평균 성장률(CAGR)을 기록했습니다. 식량 및 농산물에 대한 수요가 증가함에 따라 아르헨티나의 농부들은 재배 면적을 확대하고 작물 생산을 강화하여 잡초 방제를 위한 제초제의 필요성이 더욱 커질 수 있습니다.

- 특정 제초제에 대한 잡초의 내성은 농부들에게 큰 도전이 될 수 있습니다. 그 결과 새로운 제초제 제형이나 작용 방식으로 전환하여 이러한 대안에 대한 수요가 증가할 수 있습니다. 이러한 요인들로부터 제초제 소비량은 기간 동안 19만 1,900톤 증가할 것으로 예상됩니다.

- 남미의 제초제 시장은 예측 기간(2023-2029년) 동안 5.2%의 연평균 성장률을 나타낼 것으로 예상됩니다. 농작물 손실 증가, 농작물 보호의 필요성, 잡초 방제에 대한 인식 증가, 농산물 수요 증가가 시장의 성장을 견인하고 있습니다.

남미의 제초제 시장 동향

아르헨티나는 잡초 발생에 유리한 토양 조건으로 인해 제초제 소비량에서 남미를 압도하고 있습니다.

- 잡초는 토지 및 수자원의 활용을 방해하여 작물 수확량에 악영향을 미치는 원치 않는 바람직하지 않은 식물입니다. 잡초로 인한 작물의 수확량 손실은 잡초의 출현 시기, 잡초의 종류, 작물 유형 등 여러 요인에 따라 달라집니다. 잡초를 방제하지 않으면 100%의 수확량 손실이 발생할 수 있습니다. 제초제는 원치 않는 잡초를 조작하거나 방제하는 데 사용되는 화학 물질입니다. 제초제는 잡초를 효과적으로 방제할 수 있는 도구로, 기계적인 방법보다 적은 에너지로 효율적으로 수확량을 달성할 수 있습니다.

- 아르헨티나는 2022년 7.4kg/ha의 제초제 소비량으로 남미에서 제초제 소비량 1위를 차지했습니다. 아르헨티나는 팜파스 지역의 비옥한 토양부터 건조한 지역의 모래와 양토 토양에 이르기까지 다양한 토양 유형을 가지고 있습니다. 각기 다른 잡초 종은 특정 토양 조건에 적응하여 아르헨티나의 여러 지역에서 번성하고 확산될 수 있습니다. 플랩베인, 돼지풀, 존송그라스, 핑거그라스, 구스그라스, 헛간풀, 라이그라스 등이 가장 중요한 잡초로 꼽힙니다.

- 브라질은 2022년 제초제 소비량이 5.3kg/ha로 두 번째로 높습니다. 브라질은 열대 기후가 주를 이루며 대부분의 지역에서 일 년 내내 따뜻한 기온을 보입니다. 높은 기온은 많은 잡초 종의 발아, 성장, 번식을 촉진하기 때문에 잡초 성장에 유리한 조건을 제공합니다. 브라질에서 발견되는 주요 잡초 종으로는 물달개비, 코니자, 사이페루스, 비덴스 필로사, 수수 할레펜스 등이 있습니다.

- 남미에는 특히 브라질과 아르헨티나와 같은 국가에 광대한 경작지가 있어 제초제 수요가 많습니다. 대규모 농작물 재배를 위한 토지 개간은 효과적인 잡초 방제의 필요성을 증가시켜 제초제에 대한 수요를 증가시킵니다.

다양한 제초제 방제 효과와 다른 국가로부터의 수입 의존도는 이 지역의 아트라진 제초제 가격을 상승시킬 수 있습니다.

- 아트라진은 트리아진 계열의 화학물질에 속하는 제초제로 다양한 작물의 활엽수 및 풀 잡초를 방제하는 데 널리 사용됩니다. 남미의 아트라진 가격은 2022년 1만 3,810달러였습니다. 제초제로서 아트라진의 작용 방식은 식물의 광합성 과정을 억제하는 것입니다. 특히 엽록체의 광합성 시스템 II(PSII) 단백질 복합체를 표적으로 삼아 광합성 과정에서 빛 에너지를 화학 에너지로 전환하는 식물의 능력을 방해합니다. 이로 인해 독성 부산물이 축적되고 궁극적으로 표적이 된 잡초가 죽게 됩니다.

- 파라코트는 비피리딜륨 화합물 계열의 화학 물질에 속하는 널리 사용되는 제초제입니다. 주로 농업 및 비농업 환경에서 다양한 활엽수 및 풀 잡초를 방제합니다. 빠른 작용과 비선택적 특성으로 인해 파라코트는 일반적으로 작물이 나오기 전에 잡초를 방제하기 위한 식전 또는 발아 전 제초제로 사용됩니다. 면화, 옥수수, 대두, 사탕수수 및 기타 다양한 작물을 포함한 광범위한 작물에 효과적입니다. 파라코트는 2022년 남미에서 가격이 4,600달러였습니다.

- 글리포세이트는 유기포스포네이트 계열의 화학물질에 속하는 널리 사용되는 제초제입니다. 비선택성 전신 제초제로서 다양한 작물의 광범위한 잡초를 효과적으로 방제할 수 있습니다. 남미의 글리포세이트 가격은 2022년 1,100달러였습니다. 글리포세이트의 효과와 광범위한 활성, 상대적으로 저렴한 비용으로 인해 이 지역 농부들은 잡초 방제를 위해 글리포세이트를 많이 선택했습니다. 그러나 잠재적인 건강 및 환경 영향에 대한 우려로 인해 그 사용에 대한 논란이 있어 왔습니다.

남미의 제초제 산업 개요

남미의 제초제 시장은 적당히 통합되어 상위 5개사에서 48.24%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. ADAMA Agricultural Solutions Ltd, BASF SE, Bayer AG, Corteva Agriscience and Syngenta Group.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 헥타르당 농약 소비량

- 유효성분의 가격 분석

- 규제 프레임워크

- 아르헨티나

- 브라질

- 칠레

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 적용 모드

- 화학 처리

- 잎 표면 살포

- 훈증

- 토양 처리

- 작물 유형

- 상업 작물

- 과일 및 채소

- 곡물

- 콩류 및 유지 종자

- 잔디 및 관상용

- 생산국

- 아르헨티나

- 브라질

- 칠레

- 기타 남미

제6장 경쟁 구도

- 주요 전략적 움직임

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일(세계 수준 개요, 시장 수준 개요, 주요 사업 부문, 재무, 직원 수, 주요 정보, 시장 순위, 시장 점유율, 제품 및 서비스, 최근 동향 분석 포함)

- ADAMA Agricultural Solutions Ltd

- American Vanguard Corporation

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Rainbow Agro

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계의 개요

- 개요

- Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 출처 및 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

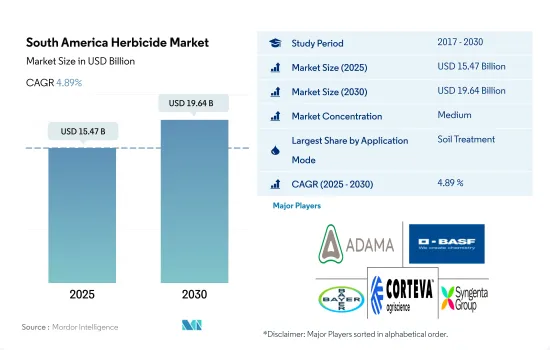

The South America Herbicide Market size is estimated at 15.47 billion USD in 2025, and is expected to reach 19.64 billion USD by 2030, growing at a CAGR of 4.89% during the forecast period (2025-2030).

The rising demand for agricultural products and a focus on managing weed effectively are strengthening the market's growth

- Chemigation accounted for 19.7% of market value in 2022. It is a popular choice in areas with well-developed irrigation infrastructure. The rising adoption of drip irrigation systems is expected to fuel the market's growth in the coming years.

- Foliar holds the second major share and is expected to record a CAGR of 5.1% during the forecast period (2023-2029). Herbicides are applied directly to the leaves of plants, where they are absorbed and translocated throughout the plant to control unwanted vegetation. It is common practice in agriculture, allowing for targeted and efficient weed control while minimizing herbicide usage.

- The fumigation method is anticipated to witness a growth of USD 78.3 million between 2023 and 2029. This method involves using gaseous herbicides to control pests and weeds in soil or enclosed spaces, such as greenhouses. It is commonly used to treat large areas and is especially effective against soil-borne pests.

- The soil treatment segment is expected to record a CAGR of 5.4% during the forecast period (2023-2029). This method involves applying herbicide directly to the soil to control weeds before planting or managing persistent weed issues. Soil treatment can help create a favorable environment for crop establishment and growth.

- The South American herbicide market is expected to grow by a value of USD 5.04 billion during the forecast period (2023-2029). The demand for herbicides in South America is influenced by the adoption of these application methods to control weed growth effectively and maximize crop yield. Changing agricultural practices, crop types, weed pressure, and pest management strategies are driving the demand for herbicide products.

The growth was driven by rising awareness about the benefits of weed control and its impact on yield

- South America accounted for 35.5% of the total global herbicide market in 2022. The herbicide market in South America is experiencing growth in various regions, including Argentina, Brazil, Chile, and the Rest of South America. These countries are major agricultural producers with vast expanses of farmland; therefore, the use of herbicides becomes crucial to manage weed populations and ensure optimal crop yields.

- Brazil held a major share of 53.6% in the market and is expected to register a CAGR of 5.2% during the period. Farmers in the country are becoming increasingly aware of the benefits of weed control and the impact of weeds on crop yields. Rising crop losses due to weeds may lead to higher adoption of herbicides.

- In 2022, Argentina held a 35.1% share of the South American herbicide market, registering a CAGR of 5.6%, which was the fastest compared to other countries. With the rising demand for food and agricultural products, farmers in Argentina may expand their cultivation areas and intensify crop production, leading to a greater need for herbicides to control weeds.

- Weed resistance to certain herbicides can be a significant challenge for farmers. As a result, they may switch to newer herbicide formulations or modes of action, driving demand for these alternatives. Due to these factors, the consumption of herbicide is expected to increase by 191.9 thousand metric ton during the period.

- The South American herbicide market is projected to record a CAGR of 5.2% during the forecast period (2023-2029). The rising crop losses, the need to protect crops, and increasing awareness of weed control, coupled with rising demand for agriculture products, are driving the growth of the market.

South America Herbicide Market Trends

Argentina dominated South America in the consumption of herbicides due to the favorable soil conditions for weed infestation

- Weeds are unwanted and undesirable plants that interfere with the utilization of land and water resources and thus adversely affect crop yields. Yield losses in crops due to weeds depend on several factors, such as weed emergence time, type of weeds, and crop type. Weeds can result in 100% yield loss if left uncontrolled. Herbicides are chemicals used to manipulate or control undesirable weeds. Herbicides are effective and operative tools to control weeds, allowing yields to be achieved efficiently with less energy than mechanical practices.

- Argentina dominated South America in consumption of herbicides at a rate of 7.4 kg/ha in 2022. Argentina has diverse soil types, ranging from fertile soils in the Pampas region to sandy and loamy soils in the arid areas. Different weed species are adapted to specific soil conditions, allowing them to thrive and spread in different areas of the country. Fleabane, pigweed, johnsongrass, fingergrass, goosegrass, barnyard grass, and ryegrass are considered the most important weeds.

- Brazil has the second-highest herbicide consumption rate of 5.3 kg/ha in 2022. Brazil has a predominantly tropical climate, with warm temperatures throughout the year in most regions. High temperatures provide favorable conditions for weed growth, as they accelerate the germination, growth, and reproduction of many weed species. Commelina benghalensis, Conyza spp., Cyperus spp., Bidens pilosa, and Sorghum halepense are some of the major weed species found in Brazil.

- South America has vast areas of arable land, particularly in countries like Brazil and Argentina, which drives the demand for herbicides. The clearing of land for cultivating large-scale crops contributes to the need for effective weed control, thereby increasing the demand for herbicides.

effectiveness in controlling various herbicides and dependency on imports from other countries may raise the price of Atrazine herbicides in the region.

- Atrazine is a herbicide belonging to the chemical class of triazines and is widely used to control broadleaf and grassy weeds in various crops. The price of atrazine in South America was USD 13.81 thousand in 2022. Atrazine's mode of action as a herbicide involves inhibiting the photosynthesis process in plants. It specifically targets the photosystem II (PSII) protein complex in chloroplasts, disrupting the plants' ability to convert light energy into chemical energy during photosynthesis. This leads to the accumulation of toxic byproducts and, ultimately, the death of the targeted weeds.

- Paraquat is a widely used herbicide belonging to the chemical class of bipyridylium compounds. It primarily controls various broadleaf and grassy weeds in agricultural and non-agricultural settings. Due to its rapid action and non-selective nature, paraquat is commonly used as a pre-plant or pre-emergence herbicide to control weeds before crops emerge. It is effective in a wide range of crops, including cotton, corn, soybeans, sugarcane, and various other crops. Paraquat was priced at USD 4.6 thousand in South America in 2022.

- Glyphosate is a widely used herbicide belonging to the chemical class of organophosphonates. It is a non-selective systemic herbicide, meaning it can effectively control a broad range of weeds in various crops. The price of glyphosate in South America was USD 1.1 thousand in 2022. Glyphosate's effectiveness, broad-spectrum activity, and relatively low cost have made it a popular choice for weed control for farmers in the region. However, its use has been controversial due to concerns about potential health and environmental impacts.

South America Herbicide Industry Overview

The South America Herbicide Market is moderately consolidated, with the top five companies occupying 48.24%. The major players in this market are ADAMA Agricultural Solutions Ltd, BASF SE, Bayer AG, Corteva Agriscience and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Brazil

- 4.3.3 Chile

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Chile

- 5.3.4 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 American Vanguard Corporation

- 6.4.3 BASF SE

- 6.4.4 Bayer AG

- 6.4.5 Corteva Agriscience

- 6.4.6 FMC Corporation

- 6.4.7 Rainbow Agro

- 6.4.8 Sumitomo Chemical Co. Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms