|

시장보고서

상품코드

1684006

베트남의 제초제 시장 : 점유율 분석, 산업 동향, 성장 예측(2025-2030년)Vietnam Herbicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

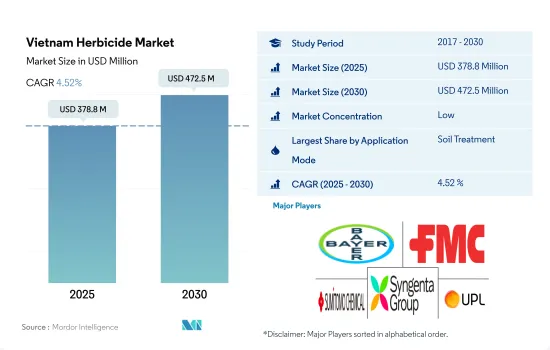

베트남의 제초제 시장 규모는 2025년에 3억 7,880만 달러로 추정되고, 2030년에는 4억 7,250만 달러에 이르고, 예측 기간(2025-2030년)의 CAGR은 4.52%를 나타낼 것으로 예측됩니다.

전통적인 제초제 토양 처리와 주요 작물의 품질을 보호하는 효과로 인해 토양 처리 채택이 증가할 수 있습니다.

- 베트남에서는 농업 현장에서 잡초를 효과적으로 방제하기 위해 다양한 방식으로 제초제를 살포합니다. 농부들은 적절한 살포 모드를 활용하여 제초제를 살포하고, 특정 지역을 효과적으로 커버하며, 낭비를 최소화함으로써 비용을 절감할 수 있습니다. 이러한 효율성 향상은 최적화된 제초제 사용으로 이어져 농가의 투입 비용을 절감할 수 있습니다.

- 2022년 농업 관행에서 가장 많이 사용되는 제초제 살포 방식은 토양 처리로 전체 제초제 살포 부문의 46.4%를 차지했습니다. 곡물 및 곡물 부문이 64.6%로 가장 큰 시장 점유율을 차지했습니다. 토양 처리 제초제에 대한 선호도는 잡초의 성장을 방지하거나 줄여 곡물과 곡물의 품질을 보호하는 데 효과적이기 때문입니다.

- 2022년에는 제초제 살포 부문에서 잎 표면 살포가 2위를 차지하며 33.2%의 시장 점유율을 나타냈습니다. 이는 잎 표면 제초제가 빠르게 작용하는 특성으로 인해 표적 잡초의 생리적 과정을 빠르게 방해할 수 있기 때문입니다. 이러한 빠른 작용은 잡초의 시들음, 황변 또는 괴사와 같은 증상을 초래합니다. 이러한 장점은 효과적으로 방제하지 않으면 작물을 빠르게 지배할 가능성이 있는 공격적이거나 경쟁적인 잡초 종을 다룰 때 유용합니다.

- 베트남 농업 부문의 제초제 활용은 작물 생산성을 극대화하고 전반적인 작물 수익성을 개선하는 데 목적이 있습니다. 제초제의 적용 방식은 시장 점유율 측면에서 4.9%의 연평균 성장률(CAGR)을 나타낼 것으로 예상됩니다.

베트남의 제초제 시장 동향

잡초로부터 작물을 보호하고 수확량을 향상시킬 필요가 있는 제초제 내성 작물의 채택은 제초제 소비를 촉진할 것으로 예상됩니다.

- 베트남의 제초제 소비는 2021년부터 2022년까지 꾸준한 상승세를 보였습니다. 이러한 증가 추세는 제초제 내성 작물의 채택, 농업 관행, 잡초 관리에 사용되는 전략 등 다양한 요인에 기인할 수 있습니다. 또한 유전자 변형(GM) 작물의 확대도 제초제 사용의 급증에 기여했습니다.

- 베트남에서는 유전자 변형 제초제 내성 옥수수(GM 옥수수)의 재배가 상당한 규모로 증가했습니다. 2019년 베트남의 농부들은 92,000에이커의 광활한 땅에서 GM 옥수수, 특히 제초제 내성 옥수수를 재배했습니다. 이는 전년도인 2018년에 비해 면적이 88% 증가한 수치입니다. GM 제초제 내성 작물의 도입 증가는 2018년과 2019년 사이 국내 제초제 소비 증가의 원인 중 하나였습니다.

- 잡초의 존재는 농작물 수확량에 상당한 위협이 되어 막대한 피해를 유발합니다. 따라서 농부들은 잡초의 성장을 조절하고 수확량 손실을 최소화하기 위해 제초제에 크게 의존하고 있습니다. 이러한 요인은 제초제 시장의 성장을 더욱 강화할 것으로 예상됩니다.

- 또한, 잡초의 끈질기고 적응력이 뛰어난 특성으로 인해 제초제 살포율이 높아지고 다양한 작용 방식을 가진 여러 제초제의 활용이 필요할 것으로 예상됩니다.

- 유전자 변형 품종을 포함한 제초제 내성 작물의 채택으로 인해 잡초를 방제하고 수확량 손실을 최소화해야 할 필요성으로 인해 제초제 살포율이 높아지고 여러 제초제를 사용하게 될 것입니다.

베트남의 농업 패턴 변화로 인한 토양 황폐화 및 잡초 발생률 증가로 이어지고 있습니다.

- 베트남 고지대의 농업은 짧은 경작-긴 휴경 기간에서 짧은 경작-짧은 휴경 또는 영구 경작으로 변화하고 있습니다. 그 결과 토양이 황폐화되고 잡초가 많이 발생하는 경우가 많습니다. 쌀은 베트남의 주요 작물이며, 헛간풀(Echinochloa crus-galli)은 논에서 가장 파괴적인 잡초 중 하나입니다. 메콩 삼각주에서는 이 잡초로 인해 2021년 직접 씨를 뿌린 벼 재배 지역에서 46%의 쌀 수확량 손실이 발생했습니다.

- 메트리부진은 광합성을 억제하여 옥수수, 사탕수수, 감자, 토마토와 같은 주요 작물의 광엽 잡초를 방제하는 데 사용되는 선택적 전신 제초제입니다. 2022년에는 1톤당 16,600달러로 평가되었습니다.

- 2022년에는 일반적인 침투성 제초제인 2,4-디클로로페녹시아세트산(2,4-D)이 베트남에서 톤당 2,300달러로 평가되었습니다. 2,4-D는 잔디, 잔디, 농작물, 과채류의 활엽 잡초를 방제하는 데 사용됩니다.

- 유사하게, 펜디메탈린은 선택적 발아 전 제초제이며, 2022년에는 1톤당 3,300달러로 평가되었습니다. 감자, 담배, 수수, 쌀, 사탕수수의 일년생 풀과 광엽 잡초를 광범위하게 방제할 수 있습니다. 베트남은 2022년 인도에서 약 3,000톤의 펜디메탈린을 수입합니다.

- 다양한 기상 조건은 식물에 손상과 스트레스를 유발하여 극심한 스트레스를 견디지 못해 식물 건강에 해로울 수 있습니다. 극심한 온도, 습도, 비, 우박, 가뭄, 태풍 등의 기상 조건은 잡초의 성장을 증가시킵니다. 이는 제초제 수요 증가로 이어져 베트남의 제초제 가격 상승으로 이어질 것입니다.

베트남의 제초제 산업 개요

베트남의 제초제 시장은 세분화되어 상위 5개사에서 24.69%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. Bayer AG, FMC Corporation, Sumitomo Chemical, Syngenta Group and UPL Limited.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 헥타르당 농약 소비량

- 유효성분의 가격 분석

- 규제 프레임워크

- 베트남

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 적용 모드

- 화학 처리

- 잎 표면 살포

- 훈증

- 토양 처리

- 작물 유형

- 상업 작물

- 과일 및 채소

- 곡물

- 콩류 및 유지종자

- 잔디 및 관상용

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일(세계 수준 개요, 시장 수준 개요, 주요 사업 부문, 재무, 직원 수, 주요 정보, 시장 순위, 시장 점유율, 제품 및 서비스, 최근 동향 분석 포함)

- ADAMA Agricultural Solutions Ltd.

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Nufarm Ltd

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계의 개요

- 개요

- Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 출처 및 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Vietnam Herbicide Market size is estimated at 378.8 million USD in 2025, and is expected to reach 472.5 million USD by 2030, growing at a CAGR of 4.52% during the forecast period (2025-2030).

Traditional herbicide soil treatments and their effectiveness in protecting the quality of major crops may raise soil treatment adoption

- In Vietnam, herbicides are applied through various modes to control weeds in agricultural practices effectively. Farmers can achieve cost savings by utilizing suitable modes of application, allowing them to apply herbicides, effectively covering specific areas, and minimizing wastage. This increased efficiency leads to optimized herbicide usage, resulting in reduced input costs for farmers.

- In 2022, the dominant mode of herbicide application in agricultural practices was soil application, accounting for 46.4% of the overall herbicide application segment. The grains & cereals segment held the largest market share at 64.6%. The preference for soil treatment herbicides is attributed to their effectiveness in protecting the quality of grains and cereals by preventing or reducing weed growth.

- In 2022, foliar application was the second leading and held a market share of 33.2% in the segment of herbicide application. This is due to foliar herbicides being beneficial due to their fast-acting properties, which can rapidly disrupt the physiological processes of targeted weeds. This swift action results in symptoms like wilting, yellowing, or necrosis in the weeds. This advantage is valuable when tackling aggressive or competitive weed species that have the potential to rapidly dominate the crops if not effectively controlled.

- In the Vietnamese agricultural sector, the utilization of herbicides is aimed at maximizing crop productivity and improving overall crop profitability. The mode of application of herbicides is projected to register a CAGR of 4.9% in terms of market share.

Vietnam Herbicide Market Trends

The adoption of herbicide-tolerant crops with the need to protect the crops from weeds and improve yield is expected to drive the consumption of herbicides

- The consumption of herbicides in Vietnam witnessed a steady upward trend between 2021 and 2022. This increasing trend can be attributed to various factors, including the adoption of herbicide-tolerant crops, agricultural practices, and strategies employed for weed management. Furthermore, the expansion of genetically modified (GM) crops has contributed to the surge in herbicide usage.

- The cultivation of genetically modified herbicide-tolerant maize (GM corn) grew on a significant scale in Vietnam. In 2019, farmers in the country cultivated GM corn, specifically herbicide-tolerant maize, on an expansive 92,000 acres of land. This represented an 88% increase in acreage compared to the previous year, 2018. The increased adoption of GM herbicide-tolerant crops was one of the driving factors behind the rise in herbicide consumption in the country between 2018 and 2019.

- The presence of weeds poses a significant threat to crop yields, causing substantial damage. Consequently, farmers heavily rely on herbicides to regulate weed growth and minimize yield losses. This factor is further expected to bolster the growth of the herbicide market.

- Furthermore, the persistent and adaptable nature of weeds is expected to necessitate higher rates of herbicide application and the utilization of multiple herbicides with diverse modes of action.

- Therefore, due to the adoption of herbicide-tolerant crops, including genetically modified varieties, the need to control weeds and minimize yield losses leads to higher application rates and the use of multiple herbicides. These factors are expected to fuel the consumption of herbicides.

Changing agriculture patterns in Vietnam are leading to soil degradation and high weed infestation

- Agriculture in the uplands of Vietnam is changing from short cultivation-long fallow periods to short cultivation-short fallow periods or even permanent cropping. Soil degradation and high weed infestation are often the consequences. Rice is the major crop in Vietnam, and barnyard grass (Echinochloa crus-galli) is one of the most devastating weeds in the rice fields. In the Mekong Delta, this weed caused 46% rice yield losses in direct-seeded rice areas in 2021.

- Metribuzin is a selective and systemic herbicide that is used to control broadleaved weeds in major crops in the country, like corn, sugarcane, potatoes, and tomatoes, by inhibiting photosynthesis. In 2022, it was valued at USD 16.6 thousand per metric ton.

- In 2022, 2,4-dichlorophenoxyacetic acid (2,4-D), a common systemic herbicide, was valued at USD 2.3 thousand per metric ton in Vietnam. It is used to control broadleaf weeds in turf, lawns, field crops, and fruit and vegetable crops.

- Similarly, pendimethalin is a selective pre-emergence herbicide valued at USD 3.3 thousand per metric ton in 2022. It has broad-spectrum control of annual grasses and broadleaf weeds in potato, tobacco, sorghum, rice, and sugarcane. Vietnam imported around 3.0 thousand metric tons of pendimethalin from India in 2022.

- A variety of weather conditions can cause damage and stress to plants and thus be detrimental to plant health as they cannot survive extreme stress. These conditions, including extremes of temperature, humidity, and rain, as well as hail, drought, and typhoons, lead to increased weed growth. This will further lead to increased herbicide demand, thereby inflating the prices of active ingredients in the country.

Vietnam Herbicide Industry Overview

The Vietnam Herbicide Market is fragmented, with the top five companies occupying 24.69%. The major players in this market are Bayer AG, FMC Corporation, Sumitomo Chemical Co. Ltd, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd.

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Nufarm Ltd

- 6.4.7 Sumitomo Chemical Co. Ltd

- 6.4.8 Syngenta Group

- 6.4.9 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms