|

시장보고서

상품코드

1906867

폴리아미드 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Polyamides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

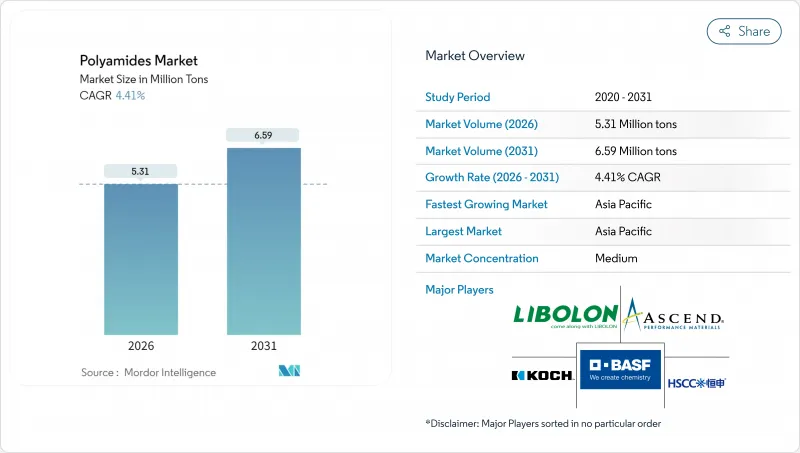

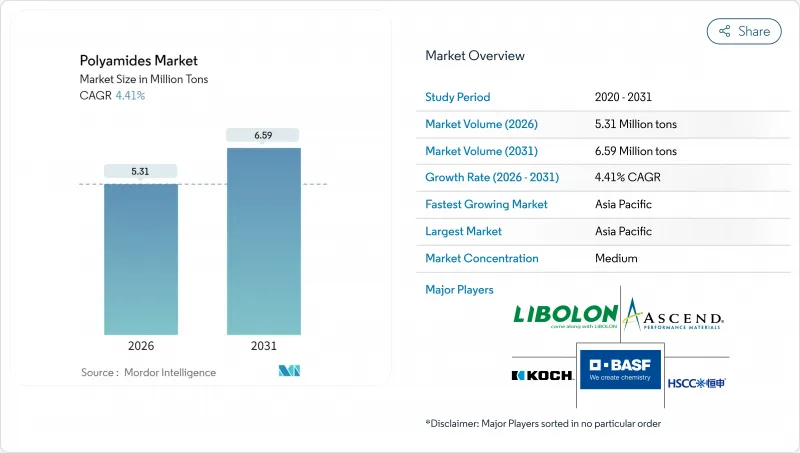

폴리아미드 시장은 2025년에 509만 톤으로 평가되었고, 2026년 531만 톤에서 2031년까지 659만 톤에 이를 것으로 예측되고 있습니다. 예측기간(2026-2031년)의 CAGR은 4.41%를 나타낼 전망입니다.

이러한 성장 추세는 자동차 경량화 의무화, 전기차(EV) 생산의 급속한 확대, 5G 전자제품에서 고온 폴리머의 가속화된 채택에 의해 뒷받침됩니다. 폴리아미드 등급, 특히 PA 6 및 PA 66은 180°C에 가까운 지속적인 온도를 견디면서도 무게를 절감할 수 있기 때문에 엔진룸 부품, 와이어 하네스, 배터리 구성 요소에서 금속을 계속 대체하고 있습니다. 식품 보존용 차단 필름 수요 증가로 포장 분야도 성장세를 보이고 있으며, 바이오 기반 폴리아미드는 브랜드 소유주의 지속가능성 목표 달성에 기여하고 있습니다. 공급 안정성은 여전히 전략적 우선순위입니다 : 2024년 원료 가격 변동으로 마진이 압박받았고, 아디포니트릴 공급 병목 현상으로 PA 66 생산량이 제한되면서 통합 생산 라인을 보유한 업체들이 시장 점유율을 확보했습니다.

세계의 폴리아미드 시장 동향 및 인사이트

경량화 자동차 용도의 견조한 수요

자동차 제조사들은 엄격한 연비 및 배출 규제를 준수하기 위해 PA 6 및 PA 66을 점점 더 많이 선택하고 있습니다. 전기화는 이 추세를 가속화하는데, 이는 제거된 질량 1kg당 실내 공간을 희생하지 않고도 주행 거리를 연장하기 때문입니다. 유럽 OEM들은 금속에서 유리섬유 강화 폴리아미드로 전환한 후 파워트레인 부품의 무게를 15-20% 절감했다고 보고합니다. 엔진룸 부품은 180°C까지의 폴리아미드 안정성으로 인해 기존 폴리프로필렌이 달성할 수 없는 성능 여유를 확보합니다. 세계의 승용차 생산량이 회복되고 전기차 보급률이 가속화됨에 따라 OEM 조달 전략은 장기 수지 물량을 확보하여 폴리아미드 시장의 가장 영향력 있는 성장 동력을 공고히 하고 있습니다.

전기 모빌리티용 와이어 하네스 및 열 관리 수요 급증

전기차 아키텍처는 고전압 및 열 유량을 견딜 수 있는 소형 배선 하네스와 견고한 배터리 하우징을 요구합니다. PA 12와 열안정화 PA 66은 우수한 전해질 저항성과 저온 유연성을 보여 얇은 벽 두께와 더 작은 굽힘 반경을 가능하게 합니다. 테슬라는 모델 Y 배선 네트워크에 특수 폴리아미드를 도입해 절연 특성을 유지하면서 하네스 질량을 줄였습니다. 전기차의 급속한 확산으로 이 수요 요인은 즉각적이며, 아시아, 유럽, 북미 지역에서 신규 배터리 및 하네스 공장이 가동되면서 프로젝트 초기부터 고성능 폴리아미드 등급을 지정하고 있습니다.

카프로락탐 및 아디프산 원료 가격의 변동성

원유 연계 카프로락탐 가격은 2024년 급등하여 헤지 공급망이 없는 폴리머 공장의 전환 마진을 잠식했습니다. 아시아 수입에 의존하는 유럽 및 북미 생산자들은 착륙 비용 스프레드 확대에 직면하여 BASF 폴리아미드 사업부의 수익성이 압박받았습니다. 아디픽산 규제로 인한 아산화질소 배출 제한은 공급을 더욱 압박하여 비용 변동성을 증폭시키고, 특히 중소 가공업체들의 장기 계약 체결을 저해했습니다.

부문 분석

PA 6은 균형 잡힌 특성 세트와 넓은 가공 범위로 대량 생산되는 자동차 부품 및 산업용 기어에 유리하여 2025년 폴리아미드 시장 규모의 58.12%를 차지했습니다. 지역 컴파운더들은 유리섬유 및 난연제와의 호환성을 높이 평가하여 기존 공급망을 유지하고 있습니다. 그러나 성숙한 응용 분야의 포화로 성장세는 완화되고 있습니다. PA 66은 열변형온도가 200°C를 초과하는 엔진룸 부품, 배터리 냉각판, 5G 커넥터 수요에 힘입어 2031년까지 4.74%의 최고 연평균 성장률(CAGR)을 기록할 전망입니다. 아디포니트릴 공급 병목 현상에도 불구하고 OEM 설계 잠금이 수요를 보호하며 가격 프리미엄은 유지 가능합니다.

특수 클러스터인 아라미드 섬유와 PPA(폴리페닐렌프로파일렌)는 틈새이면서 수익성이 높은 수요에 대응합니다. 항공우주용 허니컴, 방탄 보호재, 고장력 코드에 사용되는 아라미드 섬유는 높은 마진을 창출하지만 생산량은 여전히 적습니다. PPA 등급은 터보차저 에어쿨러 엔드 탱크와 전기 파워트레인 모듈에 적용되며 두 자릿수 가격 프리미엄을 형성합니다. BASF와 같은 기존 PA 6 공급사들은 특수 소재의 시장 진입에 대응하기 위해 유리전환온도와 내화학성을 향상시킨 울트라미드 어드밴스드 라인을 출시했습니다. 이는 카테고리 경계를 모호하게 하여 구매자들이 일반 수지 계열이 아닌 응용 분야별 성능을 평가하도록 유도합니다. 폴리아미드 시장 점유율 확대는 비용, 가용성, 기술적 여유 공간의 균형에 달려 있습니다. OEM 소재 선정 위원회는 점점 더 총소유비용 시나리오를 실행하며, 경량화나 소형화의 이점과 원료 가격 변동성을 비교 평가하고 있습니다. 이에 따라 PA 6은 비용이 중요한 부품에서 주도권을 유지하는 반면, PA 66과 PPA는 작동 온도나 화학 물질 노출이 증가하는 첨단 응용 분야를 선점하고 있습니다.

본 폴리아미드 시장 보고서는 수지 하위 유형별(PA 6, PA 66, 아라미드, PPA), 최종 사용자 산업별(자동차, 전기 및 전자, 항공우주, 산업 및 기계, 건축 및 건설, 포장, 기타 최종 사용자 산업), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 세분화되어 있습니다. 시장 예측은 수량(톤) 및 금액(달러)으로 제공됩니다.

지역별 분석

아시아태평양 지역은 2025년 폴리아미드 시장의 50.88% 점유율을 기록했으며, 2031년까지 연평균 4.89% 성장할 것으로 전망됩니다. 중국의 전기차 생산 증가로 와이어 하네스 수지 수요가 확대될 것이며, 인도의 전자산업 확대는 고온 등급 제품의 수요 증가로 이어질 것으로 예상됩니다. 일본은 하이브리드 파워트레인용 정밀 컴파운딩 및 방향족 폴리아미드를 공급하고, 한국은 세계의적으로 판매되는 5G 모듈에 PPA를 적용하고 있습니다. 원료 자급률은 개선되고 있지만, 카프로락탐 공급의 집중화로 인해 해당 지역은 원유 가격 변동에 취약합니다. 말레이시아와 태국 같은 국가들은 생산 기반 다각화를 위해 다운스트림 투자 인센티브를 목표로 삼아, 중국 플러스 원 전략을 추구하는 2차 가공업체들을 유치하고 있습니다.

미국의 자동차 제조사들은 경량화 폴리머를 적극적으로 도입하고 있으며, 항공우주 주요 업체들은 객실 및 엔진룸 부품용 3D 프린팅 파우더를 지정하고 있습니다. Ascend의 수직 통합형 PA 66 체인은 국내 구매자들을 일부 아디포니트릴 부족으로부터 보호하지만, 전문 등급 전반에 걸쳐 여전히 생산 능력 제약이 파급되고 있습니다. 멕시코의 차량 조립 증가세는 지역 컴파운더의 비용 효율적인 PA 6를 활용하는 반면, 캐나다 항공우주 공급망은 고성능 아라미드 실험을 진행 중입니다. 유럽은 순환경제를 강조합니다. 독일의 프리미엄 OEM들은 비용 증가에도 불구하고 바이오 함량 또는 재생 폴리아미드를 확보하며, 이를 통해 공급업체 평가 기준에 지속가능성을 반영하고 있습니다. 프랑스 항공 부문은 적층 제조 등급의 인증을 주도하고, 이탈리아 기계 클러스터는 엔지니어링 마모 부품에 대한 안정적 수요를 유지합니다. 유럽화학물질청(ECHA)은 REACH 규정에 따른 첨가제 심사를 확대하며, 견고한 규제 서류로 대응하는 생산자에게 혜택을 부여합니다. 브렉시트 시대 영국 제조업은 물량 유출을 상쇄하기 위해 고마진 특수 컴파운드를 목표로 합니다. 남미, 중동, 아프리카는 종합 점유율은 낮으나 자동차 현지화와 인프라 확장을 통해 성장 잠재력을 제공합니다. 브라질의 유연 포장 변환업체들은 수출 지향적 농식품 운송을 위한 폴리아미드 다층 구조를 탐구하고 있는 반면, 걸프협력회의(GCC) 국가들은 저비용 원료를 활용해 수지 투자를 유치하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 경량화 자동차 용도의 견조한 수요

- 전기 모빌리티용 와이어 하네스 및 열 관리 수요 급증

- 고온 폴리머를 필요로 하는 5G 전자기기의 성장

- 소비자 브랜드의 바이오 기반 폴리아미드 전환

- 항공우주용 적층 제조 등급 신흥 시장

- 시장 성장 억제요인

- 카프로락탐 및 아디프산 원료 가격의 변동성

- PA 66 기반 폴리머의 지속적인 수급 불균형

- 연포장의 PET 및 PP의 대체품 증가 경향

- 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 신규 참가업체의 위협

- 규제 상황

- 수출입 분석

- 가격 동향

- 재활용 개요

- 최종 용도 섹터 동향

- 항공우주(항공우주 부품 생산 수익)

- 자동차(자동차 생산 대수)

- 건축 및 건설(신축 바닥 면적)

- 전기 및 전자 기기(전기 및 전자 기기 생산 수익)

- 포장(플라스틱 포장량)

제5장 시장 규모와 성장 예측(금액 기준 및 수량 기준)

- 수지 서브 유형별

- 폴리아미드(PA 6)

- 폴리아미드(PA 66)

- 아라미드

- 폴리프탈아미드(PPA)

- 최종 사용자 업계별

- 자동차

- 전기 및 전자 기기

- 항공우주

- 산업 및 기계

- 건축 및 건설

- 포장

- 기타 최종 사용자 산업

- 지역별

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 말레이시아

- 기타 아시아태평양

- 북미

- 캐나다

- 멕시코

- 미국

- 유럽

- 독일

- 프랑스

- 이탈리아

- 영국

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 나이지리아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/순위 분석

- 기업 프로파일

- AdvanSix

- Arclin

- Arkema SA

- Ascend Performance Materials

- BASF SE

- Celanese Corporation

- Domo Chemicals

- Envalior

- Evonik Industries

- Hangzhou Juheshun New Materials Co., Ltd.

- Highsun Holding Group

- Invista

- Koch Industries, Inc.

- Kuraray Co., Ltd.

- LIBOLON

- Solvay SA

- Ube Corporation

제7장 시장 기회와 장래의 전망

제8장 CEO를 위한 주요 전략적 과제

HBR 26.01.26The Polyamides Market was valued at 5.09 million tons in 2025 and estimated to grow from 5.31 million tons in 2026 to reach 6.59 million tons by 2031, at a CAGR of 4.41% during the forecast period (2026-2031).

This growth trajectory is underpinned by automotive lightweighting mandates, the rapid scaling of electric vehicle (EV) production, and the accelerating adoption of high-temperature polymers in 5G electronics. Polyamide grades, notably PA 6 and PA 66, continue to displace metals in under-hood parts, wire harnesses, and battery components because they provide weight savings while withstanding sustained temperatures near 180 °C. Packaging applications are also gaining momentum as barrier-film requirements rise in food preservation, while bio-based polyamides answer brand-owner sustainability targets. Supply security remains a strategic priority: feedstock price swings in 2024 squeezed margins, and adiponitrile bottlenecks constrained PA 66 output, prompting producers with integrated chains to capture share.

Global Polyamides Market Trends and Insights

Robust Demand from Lightweight Automotive Applications

Automakers are increasingly selecting PA 6 and PA 66 to comply with stringent fuel-efficiency and emission regulations. Electrification intensifies this trend because every kilogram of mass eliminated extends driving range without sacrificing cabin space. European OEMs report 15-20% weight cuts in powertrain parts after shifting from metals to glass-fiber-reinforced polyamides. Under-hood components benefit from polyamides' stability up to 180 °C, providing performance margins that conventional polypropylene cannot achieve. As global passenger-vehicle output rebounds and EV penetration accelerates, OEM sourcing strategies lock in long-term resin volumes, anchoring the most influential growth pillar for the polyamides market.

Surge in E-Mobility Wire Harness and Thermal Management Needs

EV architecture demands compact wiring looms and robust battery housings that can handle higher voltages and heat flux. PA 12 and heat-stabilized PA 66 exhibit superior electrolyte resistance and low-temperature flexibility, enabling slim wall thickness and tighter bend radii. Tesla introduced specialized polyamides into the Model Y wiring networks, reducing harness mass while maintaining dielectric properties. Rapid EV scaling makes this driver immediate, with Asia, Europe, and North America commissioning greenfield battery and harness plants that specify high-performance polyamide grades from project inception.

Volatility in Caprolactam and Adipic Acid Feedstock Prices

Crude-linked caprolactam quotations spiked in 2024, eroding conversion margins at polymer plants that lack hedged sourcing. European and North American producers, who are dependent on Asian imports, faced wider landed-cost spreads, compressing profitability at BASF's polyamides division. Adipic-acid regulations restricting nitrous oxide emissions further squeezed the supply, amplifying cost volatility and deterring long-term contracts, especially for smaller processors.

Other drivers and restraints analyzed in the detailed report include:

- Growth in 5G Electronics Requiring High-Temperature Polymers

- Shift Toward Bio-Based Polyamides in Consumer Brands

- Persistent Supply-Demand Imbalance in PA 66 Base Polymer

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PA 6 accounted for 58.12% of the polyamides market size in 2025, as its balanced property set and wide processing window favor large-volume automotive components and industrial gears. Regional compounders appreciate its compatibility with glass fibers and flame retardants, sustaining entrenched supply chains. Yet growth moderates as mature applications saturate. PA 66 recorded the leading 4.74% CAGR through 2031, propelled by under-hood parts, battery cooling plates, and 5G connectors where heat deflection temperatures exceed 200 °C. Despite adiponitrile bottlenecks, OEM design lock-in protects demand, and price premiums remain defensible.

The specialty cluster-aramids and PPA-addresses niche but lucrative needs. Aramid fiber usage in aerospace honeycomb, ballistic protection, and high-tension cords yields strong margins; however, volumes remain modest. PPA grades penetrate turbocharger air-cooler end tanks and electric powertrain modules, commanding double-digit price premiums. Traditional PA 6 suppliers, such as BASF, introduced Ultramid Advanced lines that elevate glass-transition temperatures and chemical resistance to counter specialty incursions. This blurs category boundaries, nudging buyers to evaluate performance on an application-specific basis rather than generic resin families. Polyamides market share gains hinge on balancing cost, availability, and technical headroom. OEM material-selection committees are increasingly running total-cost-of-ownership scenarios, weighing feedstock volatility against the advantages of lightweighting or miniaturization. As such, PA 6 retains leadership in cost-critical parts, whereas PA 66 and PPA capture frontier applications where operating temperatures or chemical exposure escalate.

The Polyamides Market Report is Segmented by Sub-Resin Type (PA 6, PA 66, Aramid, and PPA), End-User Industry (Automotive, Electrical and Electronics, Aerospace, Industrial and Machinery, Building and Construction, Packaging, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). Market Forecasts are Provided in Terms of Volume (Tons) and Value (USD)

Geography Analysis

The Asia-Pacific region held a 50.88% share of the polyamides market in 2025 and is projected to grow at a 4.89% CAGR through 2031. China's growing EV output will magnify demand for wire harness resins, while India's electronics push is expected to add volumes in high-temperature grades. Japan supplies precision compounding and aromatic polyamides for hybrid powertrains, and South Korea deploys PPA in 5G modules sold worldwide. Although feedstock self-sufficiency is improving, the caprolactam supply concentration makes the region vulnerable to crude oil price fluctuations. Nations such as Malaysia and Thailand target downstream investment incentives to diversify production footprints, attracting second-wave processors seeking China-plus-one strategies.

United States automakers incorporate lightweighting polymers aggressively, and aerospace primes specify 3D-printing powders for cabin and engine-bay parts. Ascend's vertically integrated PA 66 chain shields domestic buyers from some adiponitrile shortages, but capacity constraints still ripple across specialist grades. Mexico's vehicle assembly uptrend taps cost-efficient PA 6 from regional compounders, while Canada's aerospace supply base experiments with high-performance aramids. Europe underscores circularity. Germany's premium OEMs are locking in bio-content or recycled polyamides despite higher costs, thereby embedding sustainability into their supplier scorecards. France's aviation segment drives certification of additive-manufacturing grades, and Italy's machinery cluster maintains reliable demand for engineered wear parts. The European Chemicals Agency continues to expand scrutiny of additives under REACH, rewarding producers with robust regulatory dossiers. Brexit-era U.K. manufacturing targets high-margin specialty compounds to offset volume leakage. South America, the Middle East, and Africa collectively account for smaller shares, yet deliver upside through automotive localization and infrastructure expansion. Brazil's flexible-packaging converters are exploring polyamide multilayers for export-oriented agrifood shipments, whereas Gulf Cooperation Council countries are leveraging low-cost feedstock to attract resin investments.

- AdvanSix

- Arclin

- Arkema S.A.

- Ascend Performance Materials

- BASF SE

- Celanese Corporation

- Domo Chemicals

- Envalior

- Evonik Industries

- Hangzhou Juheshun New Materials Co., Ltd.

- Highsun Holding Group

- Invista

- Koch Industries, Inc.

- Kuraray Co., Ltd.

- LIBOLON

- Solvay S.A.

- Ube Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Robust Demand from Lightweight Automotive Applications

- 4.2.2 Surge in E-Mobility Wire Harness and Thermal Management Needs

- 4.2.3 Growth in 5G Electronics Requiring High-Temperature Polymers

- 4.2.4 Shift Toward Bio-Based Polyamides in Consumer Brands

- 4.2.5 Emerging Aerospace Additive-Manufacturing Grades

- 4.3 Market Restraints

- 4.3.1 Volatility in Caprolactam and Adipic Acid Feedstock Prices

- 4.3.2 Persistent Supply-Demand Imbalance in PA 66 Base Polymer

- 4.3.3 Rising PET And PP Substitution in Flexible Packaging

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of Substitutes

- 4.5.4 Competitive Rivalry

- 4.5.5 Threat of New Entrants

- 4.6 Regulatory Landscape

- 4.7 Import and Export Analysis

- 4.8 Price Trends

- 4.9 Recycling Overview

- 4.10 End-use Sector Trends

- 4.10.1 Aerospace (Aerospace Component Production Revenue)

- 4.10.2 Automotive (Automobile Production)

- 4.10.3 Building and Construction (New Construction Floor Area)

- 4.10.4 Electrical and Electronics (Electrical and Electronics Production Revenue)

- 4.10.5 Packaging (Plastic Packaging Volume)

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Sub-Resin Type

- 5.1.1 Polyamide (PA) 6

- 5.1.2 Polyamide (PA) 66

- 5.1.3 Aramid

- 5.1.4 Polyphthalamide (PPA)

- 5.2 By End-User Industry

- 5.2.1 Automotive

- 5.2.2 Electrical and Electronics

- 5.2.3 Aerospace

- 5.2.4 Industrial and Machinery

- 5.2.5 Building and Construction

- 5.2.6 Packaging

- 5.2.7 Other End-User Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 Australia

- 5.3.1.6 Malaysia

- 5.3.1.7 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 Canada

- 5.3.2.2 Mexico

- 5.3.2.3 United States

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 Italy

- 5.3.3.4 United Kingdom

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Nigeria

- 5.3.5.4 South Africa

- 5.3.5.5 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AdvanSix

- 6.4.2 Arclin

- 6.4.3 Arkema S.A.

- 6.4.4 Ascend Performance Materials

- 6.4.5 BASF SE

- 6.4.6 Celanese Corporation

- 6.4.7 Domo Chemicals

- 6.4.8 Envalior

- 6.4.9 Evonik Industries

- 6.4.10 Hangzhou Juheshun New Materials Co., Ltd.

- 6.4.11 Highsun Holding Group

- 6.4.12 Invista

- 6.4.13 Koch Industries, Inc.

- 6.4.14 Kuraray Co., Ltd.

- 6.4.15 LIBOLON

- 6.4.16 Solvay S.A.

- 6.4.17 Ube Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment