|

시장보고서

상품코드

1851234

폴리우레탄 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Polyurethane - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

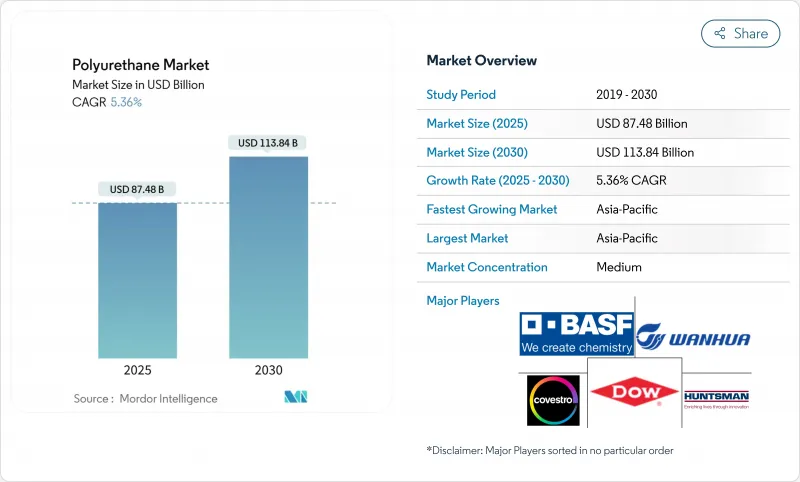

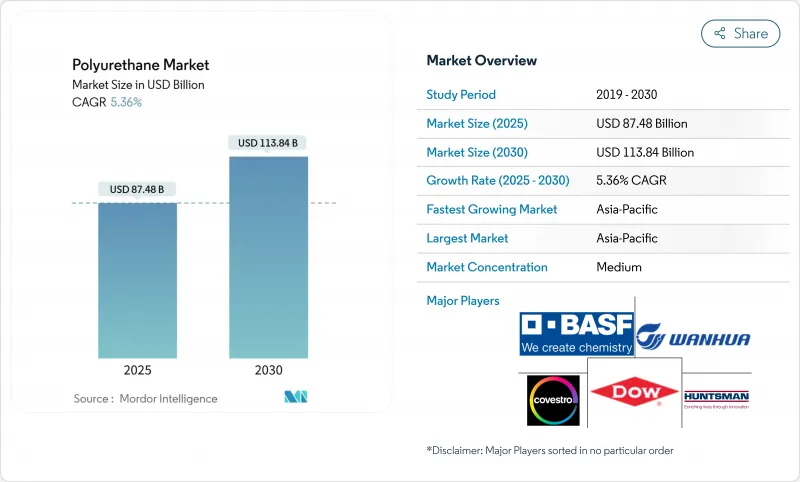

세계의 폴리우레탄 시장 규모는 2025년 874억 8,000만 달러로 추계되어 2030년까지 1,138억 4,000만 달러에 이르고, 2025-2030년 CAGR은 5.36%로 확대될 것으로 예측되고 있습니다.

이 견조한 성장은 폴리우레탄의 단열성, 경량화, 내구성 등의 장점을 평가하는 건설, 자동차, 가구, 전자기기 등 폭넓은 분야에서의 채용에 의한 것입니다. 아시아태평양은 중국의 대규모 생산 능력 증대와 인도의 견조한 석유화학 투자에 힘입어 46%의 매출을 이끌고 있으며, 세계 공급은 아시아태평양으로 계속 기울고 있습니다. 건축 부문은 에너지 기준의 엄격화를 통해 기준선 양을 유지하고, 자동차 제조 업체는 자동차 경량화 및 연비 향상을 위해 고급 폴리우레탄 복합재료에 대한 수요를 가속화하고 있습니다. 혁신의 기세는 바이오 폴리올, 폐쇄 루프 재활용 기술, 수명주기 배출량 및 규제 노출을 줄이는 저 VOC 페인트에 대한 투자로 강화됩니다. MDI/TDI 가격의 난고하나 향후의 무역조사에 있어서도 폴리우레탄 시장은 밸류체인 통합의 정착과 지속가능성을 중시한 용도의 확대라는 장점을 누리고 있습니다.

세계 폴리우레탄 시장 동향과 통찰

자동차용 경량 재료

자동차 제조업체는 차체 중량의 경량화, 연비 규제에 대응, 테일 파이프 CO2의 억제를 위해서 금속 부품을 섬유 강화 폴리우레탄으로 치환하고 있습니다. 다우의 성형 PU 시트는 편안함을 유지하면서 시트 당 풋프린트를 50% 줄이고 순환형 등급 폼이 대량 생산에 적합하다는 것을 증명합니다. Covestro의 음향적으로 최적화된 헤드 라이너와 인테리어 트림은 소음과 휘발성 유기 화합물(VOC)의 방출을 줄이고 최소한의 설계 변경으로 캐빈의 공기 품질을 향상시킵니다. 이러한 복합재료를 채택한 Tier-1 공급업체는 새로운 자본 지출 없이 조립 라인에 적합하다고 보고하여 2030년까지 채용 전망을 강화하고 있습니다.

건축 및 건설의 성장

세계의 에너지 기준은 현재 더 높은 R 값과 더 엄격한 기밀성을 규정하고 있으며, 강성 폴리우레탄의 열 및 증기 제어의 강점이 직접적으로 활용되고 있습니다. 아시아태평양의 건설 붐은 북미의 리노베이션 장려책과 함께 건축가를 얇지만 고성능의 분사 단열재와 보드 스톡 단열재에 의존하고 있습니다. 제조업체는 생산 능력을 확대하고 화석 폴리올의 20%를 대체하는 CO2 개질 경질 폼을 출시함으로써 가공 파라미터를 변경하지 않고 제품 탄생부터 출하까지의 배출량을 삭감함으로써 대응하고 있습니다. 정책 주도의 기운은 신축 및 개수 시장 전체의 꾸준한 수요 증가를 지원하고 있습니다.

MDI/TDI 원료 변동성

MDI의 원재료 점유율은 41.20%이며, 폴리우레탄 제조업체는 벤젠과 원유의 변동에 좌우됩니다. Wanhua의 닝보 폐쇄와 같은 예정된 턴어라운드와 2025년 미국에 들어가는 중국제 MDI에 대한 반덤핑 조치는 가격 상승과 배당 삭감을 일으킵니다. 가공업자는 계약기간의 연장으로 헤지하고 있지만, 마진의 압축은 계속되고 있으며, 공급이 안정될 때까지 강하의 확장 라인에 대한 투자는 연기됩니다.

부문 분석

2024년 폴리우레탄 시장 점유율에서는 연질 폼이 32%를 차지했으며 침구, 가구, 자동차 좌석의 쾌적성 주도의 우위성을 유지하고 있습니다. 연질 폼 폴리우레탄 시장 규모는 2030년까지 연평균 복합 성장률(CAGR) 6.07%를 보일 것으로 예측되며, 체중 분산을 개선하는 점탄성 업그레이드와 압축되고 신속하게 회복되는 폼에 의존하는 '베드 인 박스' 완성 모델이 이를 뒷받침합니다. 생산자는 탄력성과 통기성을 향상시켜 인체 공학적 프리미엄 기대에 부응하는 얇은 매트리스를 가능하게 합니다. 재활용업체는 폴리올의 흐름을 82%의 수율로 재생하는 산분해 공정을 개선하여 이 분야를 순환형 공급 루프에 가깝게 하고 있습니다.

경질 폼은 인치당 R값이 높고, 단일 패스로 기밀성을 확보할 수 있기 때문에 건축용 단열재로서 지지되어 제2위에 위치합니다. 벽의 공동으로 두께가 제한되는 리노베이션 프로젝트에서의 채용이 가속화되어 온대뿐만 아니라 극단적인 기후 시장에서도 지속적인 수량 수요가 강화됩니다. CASE 하위 부문(코팅, 접착제, 실란트, 엘라스토머)는 진동 감쇠, 산업용 바닥재, 내식성 라이닝에 폴리우레탄의 유용성을 확대합니다. 열가소성 폴리우레탄(TPU)은 제조 탄소를 최대 59% 절감하는 Lubrizol의 바이오물질 수지 ESTANE RNW 등급에 뛰어나게 되어, 신발과 일렉트로닉스 케이스로 점유율을 획득하고 있습니다.

지역 분석

아시아태평양은 2024년 폴리우레탄 시장 매출의 46%를 차지했으며 중국이 생산의 중심인 동시에 소비대국이기도 합니다. Wanhua와 같은 지역 리더는 MDI와 폴리올의 생산 능력을 적극적으로 확장하고 인도의 870억 달러의 석유화학 파이프라인은 지역 원료 확보와 파생 제품 성장을 가속합니다. 공공 및 민간 건설 붐이 급속한 동력화와 함께 이 지역이 2030년까지 CAGR 6.01%를 유지할 수 있도록 합니다.

북미는 성숙하면서도 혁신적인 시장으로 이어집니다. 미국은 주택 리모델링을 위한 높은 R값 단열재에 주목하고 기업 환경 목표를 달성하기 위해 서큘러 등급 자동차 시트 폼을 추구하고 있습니다. 중국제 MDI에 대한 2025년 안티덤핑 조사와 같은 정책적 움직임은 조달 전략을 재구성하고 국내 생산 능력에 대한 투자를 촉진합니다. 캐나다의 넷 제로 빌딩 계획은 이 지역의 견조한 수요를 더욱 지원합니다.

유럽의 폴리우레탄 시장은 엄격한 화학물질 규정에 의해 형성됩니다. 다가오는 PFAS 규제는 광범위한 배합의 재검토를 촉구하고 첨단 첨가물의 연구 개발과 신속한 규제 준수 프로세스를 가진 공급업체에게 유리합니다. 동시에, 그린 공공 조달 기준은 저 VOC 및 저탄소 제품에 보답하는 것으로, 제조업체를 바이오 물질 수지나 CO2 개량 그레이드로 유도하고 있습니다.

남미, 중동, 아프리카는 폴리우레탄 시장에서 차지하는 비율은 작지만 인프라, 가구, 포장 수요로 성장하고 있습니다. 브라질은 수입 의존도를 낮추기 위해 국내 석유화학제품의 확대를 추진하고 있으며, 사우디아라비아는 폴리우레탄 수출을 모색하기 위해 원료의 우위를 활용하고 있습니다. 큰 시장의 기술과 모범 사례의 보급은 신흥 지역이 국제 지속가능성 벤치마크를 신속하게 준수할 수 있도록 도와줍니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 자동차 산업에서 경량 및 고성능 복합재료 수요 증가

- 건축 및 건설 업계에서 수요 증가

- 침구, 카펫, 쿠션 산업에서 수요 증가

- 에너지 효율이 높은 소재에 대한 수요 증가

- 저 VOC(휘발성 유기 화합물)와 수성 폴리 우레탄으로의 이동

- 시장 성장 억제요인

- 메타크실렌과 원유 가격의 변동에 연동하는 MDI/TDI 원료의 변동성

- PFAS계 PU 첨가제에 관한 EU의 REACH 규제와 중국의 RoHS 규제

- 환경 문제

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 유형별

- 경질 폼

- 연질 폼

- CASE(코팅제, 접착제, 밀봉제, 엘라스토머)

- 열가소성 수지 폴리우레탄(TPU)

- 기타 유형

- 원재료별

- 메틸렌디페닐디이소시아네이트(MDI)

- 톨루엔디이소시아네이트(TDI)

- 폴리에테르 폴리올

- 폴리에스테르 폴리올

- 기타(바이오 베이스 폴리올)

- 최종 사용자 업계별

- 가구

- 건축 및 건설

- 일렉트로닉스 및 기기

- 자동차

- 신발

- 패키지

- 기타 최종 사용자 산업

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 나이지리아

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- BASF SE

- Carpenter Co.

- Covestro AG

- DIC Corporation

- Dow

- Huntsman International LLC

- INOAC Corporation

- LANXESS

- Mitsui Chemicals Inc.

- Momentive

- PPG Industries, Inc.

- Rogers Corporation

- Saint-Gobain

- Sekisui Chemical Co., Ltd.

- Sheela Foam Ltd.

- The Lubrizol Corporation

- Tosoh Corporation

- Wanhua

제7장 시장 기회와 장래의 전망

JHS 25.11.21The polyurethane market size is estimated at USD 87.48 billion in 2025 and is projected to reach USD 113.84 billion by 2030, expanding at a 5.36% CAGR during 2025-2030.

This solid growth is anchored in the material's broad adoption across construction, automotive, furniture, and electronics, each valuing polyurethane's insulation, lightweighting, and durability advantages. Asia-Pacific's 46% revenue lead-supported by large-scale capacity additions in China and robust petrochemical investments in India-continues to tilt global supply toward the region. The building sector sustains baseline volume through stricter energy codes, while automotive producers accelerate demand for advanced polyurethane composites to lower vehicle weight and boost fuel efficiency. Innovation momentum is reinforced by investments in bio-based polyols, closed-loop recycling technologies, and low-VOC coatings that reduce lifecycle emissions and regulatory exposure. Even amid MDI/TDI price swings and upcoming trade investigations, the polyurethane market benefits from entrenched value-chain integration and a growing roster of sustainability-driven applications.

Global Polyurethane Market Trends and Insights

Lightweight Materials in Automotive

Automakers are swapping metal components for fiber-reinforced polyurethane to trim curb weight, meet fuel-economy mandates, and curb tailpipe CO2. Dow's molded PU seats slash the embodied footprint by 50% per seat while preserving comfort, proving the readiness of circular-grade foams for mass production. Acoustically optimized headliners and interior trim from Covestro cut noise and volatile organic compound (VOC) release, raising cabin-air quality with minimal redesign effort. Tier-1 suppliers integrating these composites report assembly-line compatibility without new capital outlays, reinforcing adoption prospects through 2030.

Building & Construction Growth

Global energy codes now specify higher R-values and tighter air-sealing, which play directly to rigid polyurethane's thermal and vapor control strengths. Asia-Pacific's construction boom, coupled with North American retrofit incentives, keeps architects reliant on thin-but-high-performing spray and boardstock insulation. Manufacturers respond by widening capacity and launching CO2-modified rigid foams that substitute 20% of fossil polyol, lowering cradle-to-gate emissions without shifting processing parameters. The policy-led momentum supports steady demand expansion across new-build and retrofit markets.

MDI/TDI Feedstock Volatility

MDI's 41.20% raw-material share ties polyurethane producers to benzene and crude-oil swings. Scheduled turnarounds, such as Wanhua's Ningbo outage, and antidumping actions on Chinese MDI entering the United States in 2025 inject price spikes and allocation cuts. Processors hedge with longer contracts, yet margin compression persists, delaying downstream investment in expansion lines until supply stabilizes.

Other drivers and restraints analyzed in the detailed report include:

- Bedding & Furniture Demand

- Energy-Efficiency Requirements

- Regulatory Restrictions on Additives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flexible foam captured 32% of polyurethane market share in 2024, maintaining a comfort-driven edge across bedding, furniture, and automotive seating. The polyurethane market size for flexible foam is projected to rise at 6.07% CAGR through 2030, aided by viscoelastic upgrades that improve pressure redistribution and by "bed-in-a-box" fulfillment models that hinge on compressed, quick-recovery foams. Producers enhance resilience and airflow, enabling thinner mattress builds that match premium ergonomic expectations. Recyclers refine acidolysis processes that reclaim polyol streams at 82% yield, moving the segment closer to circular supply loops.

Rigid foam takes second position, favored in construction insulation for its high R-value per inch and ability to deliver air-sealing in a single pass. Adoption accelerates in retrofit projects where wall cavities constrain thickness, reinforcing sustained volume demand in temperate as well as extreme-climate markets. CASE sub-segments (coatings, adhesives, sealants, elastomers) extend polyurethane's utility to vibration damping, industrial flooring, and corrosion-resistant linings. Thermoplastic polyurethane (TPU) wins share in footwear and electronics enclosures, buoyed by Lubrizol's biomass-balanced ESTANE RNW grade that cuts manufacturing carbon by up to 59%.

The Polyurethane Market Report Segments the Industry by Type (Rigid Foam, Flexible Foam, and More), Raw Material (Methylene Diphenyl Di-Isocyanate (MDI), Toluene Di-Isocyanate (TDI), Polyether Polyols, and More), End-User Industry (Furniture, Building and Construction, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa).

Geography Analysis

Asia-Pacific generated 46% of polyurethane market revenue in 2024, with China acting as both production nucleus and consumption powerhouse. Local leaders such as Wanhua aggressively scale MDI and polyol capacity, while India's USD 87 billion petrochemical pipeline amplifies regional feedstock security and derivative growth. Public and private construction booms, paired with rapid motorization, ensure the region retains the highest 6.01% CAGR through 2030.

North America follows with a mature yet innovative market. The United States leans on high R-value insulation for residential retrofits and pursues circular-grade automotive seating foams to meet corporate environmental targets. Policy moves-such as the 2025 antidumping investigation on Chinese MDI-reshape sourcing strategies and encourage domestic capacity investments. Canada's net-zero building agenda further anchors steady regional demand.

Europe's polyurethane market is shaped by stringent chemical regulations. The looming PFAS restriction compels wide-ranging formulation revisions, favoring suppliers with advanced additive R&D and rapid regulatory compliance processes. At the same time, green public-procurement criteria reward low-VOC and low-carbon products, nudging manufacturers toward biomass-balanced and CO2-modified grades.

South America, the Middle East, and Africa represent smaller slices of the polyurethane market yet grow from infrastructure, furniture, and packaging demand. Brazil promotes domestic petrochemicals expansion to reduce import dependence, while Saudi Arabia leverages feedstock advantage to explore polyurethane exports. Technology and best-practice diffusion from larger markets help emerging regions fast-track compliance with international sustainability benchmarks.

- BASF SE

- Carpenter Co.

- Covestro AG

- DIC Corporation

- Dow

- Huntsman International LLC

- INOAC Corporation

- LANXESS

- Mitsui Chemicals Inc.

- Momentive

- PPG Industries, Inc.

- Rogers Corporation

- Saint-Gobain

- Sekisui Chemical Co., Ltd.

- Sheela Foam Ltd.

- The Lubrizol Corporation

- Tosoh Corporation

- Wanhua

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Lightweight and High-performance Composites from the Automotive Industry

- 4.2.2 Increasing Demand from the Building and Construction Industry

- 4.2.3 Increasing Demand from the Bedding, Carpet, and Cushioning Industries

- 4.2.4 Growing Demand for Energy-Efficient Materials

- 4.2.5 Shift Towards Low-VOC (Volatile Organic Compounds) and Waterborne Polyurethanes

- 4.3 Market Restraints

- 4.3.1 Volatility in MDI/TDI Feedstock Linked to Meta-Xylene and Crude Oil Price Swings

- 4.3.2 EU REACH and China RoHS Limits on PFAS-Based PU Additives

- 4.3.3 Environmental Concerns

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Type

- 5.1.1 Rigid Foam

- 5.1.2 Flexible Foam

- 5.1.3 CASE (Coatings, Adhesives, Sealants and Elastomers)

- 5.1.4 Thermoplastic Polyurethane (TPU)

- 5.1.5 Other Types

- 5.2 By Raw Material

- 5.2.1 Methylene Diphenyl Di-isocyanate (MDI)

- 5.2.2 Toluene Di-isocyanate (TDI)

- 5.2.3 Polyether Polyols

- 5.2.4 Polyester Polyols

- 5.2.5 Others (Bio-based Polyols)

- 5.3 By End-user Industry

- 5.3.1 Furniture

- 5.3.2 Building and Construction

- 5.3.3 Electronics and Appliances

- 5.3.4 Automotive

- 5.3.5 Footwear

- 5.3.6 Packaging

- 5.3.7 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Nordics

- 5.4.3.7 Russia

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/ Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Carpenter Co.

- 6.4.3 Covestro AG

- 6.4.4 DIC Corporation

- 6.4.5 Dow

- 6.4.6 Huntsman International LLC

- 6.4.7 INOAC Corporation

- 6.4.8 LANXESS

- 6.4.9 Mitsui Chemicals Inc.

- 6.4.10 Momentive

- 6.4.11 PPG Industries, Inc.

- 6.4.12 Rogers Corporation

- 6.4.13 Saint-Gobain

- 6.4.14 Sekisui Chemical Co., Ltd.

- 6.4.15 Sheela Foam Ltd.

- 6.4.16 The Lubrizol Corporation

- 6.4.17 Tosoh Corporation

- 6.4.18 Wanhua

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Increasing Demand for Bio-based Polyurethane