|

시장보고서

상품코드

1685730

안과용 의약품 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Ophthalmic Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

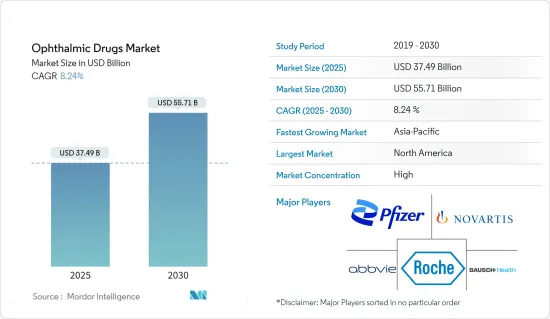

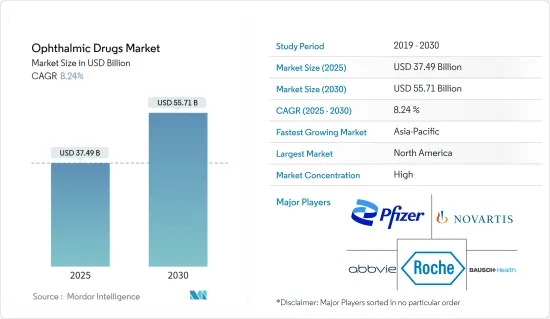

안과용 의약품 시장 규모는 2025년에 374억 9,000만 달러, 예측 기간(2025-2030년)의 CAGR은 8.24%를 나타낼 전망이며, 2030년에는 557억 1,000만 달러에 이를 것으로 예측됩니다.

업계의 혁신과 확대를 촉진하는 다양한 요인에 힘입어 현저한 성장을 이루고 있습니다. 주요 촉진요인으로는 눈과 관련된 질병의 유병률 증가와 시장 전망을 재구성하는 의약품 개발 기술의 발전 등이 있습니다.

업계를 형성하는 메가 동향 : 안질환의 세계 증가, 인구 고령화, 약물 제제 기술의 진보가 시장 성장의 견고한 기반이되고 있습니다. 이러한 요인은 특정 산업 촉진요인과 함께 안과용 의약품 업계를 새로운 높이로 끌어 올리고 있습니다.

눈과 관련된 장애 발생률 및 유병률 증가 : 시력 장애를 가진 사람 증가가 시장 성장을 가속하는 주요 요인입니다. National Eye Institute의 데이터에 따르면 2030년까지 연령 황반 변성이 미국에서 370만 명에 영향을 미칠 것으로 예상됩니다. 또한 같은 출처는 녹내장이 2030년까지 430만 명의 미국인에게 영향을 미칠 것으로 추정합니다. 이러한 안질환의 부담은 새롭고 효과적인 안과 치료에 대한 긴급한 필요성을 강조하고 시장을 전진시킵니다.

신약 개발과 관련된 연구개발 증가 : 안과용 의약품의 세계 시장 조사에 의하면 업계는 신규 치료 솔루션의 창출을 목적으로 하는 R&D 활동 증가로 혜택을 누리고 있습니다. 임상시험과 의약품 승인 증가는 이 동향을 부각하고 있습니다. 2023년, FDA는 안구 건조를 위한 새로운 항염증제 CyclASol의 신약 신청을 수락했습니다. 마찬가지로, Xbrane Biopharma AB와 STADA Arzneimittel AG에 의한 라니비주맙의 바이오시밀러의 유럽 출시는 비용 효과적인 치료 옵션의 급증을 보여줍니다. 이러한 혁신적인 의약품은 치료 영역을 확대하고 시장 성장률을 끌어 올리고 있습니다.

병용요법 개발에 대한 관심 증가 : 안과용 의약품 시장에서는 병용요법에 대한 주목이 높아지고 있습니다. 이러한 치료는 복잡한 안질환 관리에 탁월한 치료 효과를 제공합니다. 예를 들어, 2023년 7월, Tenpoint Therapeutics는 변성 안질환과 싸우는 것을 목표로 출시 선진을 자르기 위한 자금을 확보했습니다. 이 회사는 다양한 세포 기반 치료제를 결합하고 개별 사례에 맞는 치료를 수행하는 것을 전문으로 합니다. 이 회사의 접근법은 노화와 유전성 질환으로 인한 손상된 안구 세포를 회춘시키는 데 중점을 둡니다. 이러한 파트너십은 이 분야의 기술 혁신에 박차를 가하고 언메트 메디컬 요구에 대응함으로써 시장 확대를 가속화하고 있습니다.

세계의 산업은 이러한 시장 동향과 개발에 견인되어 꾸준한 성장 궤도를 타고 있습니다. 의약품 혁신, 개인화 치료, 안과 의료에 대한 접근성 향상의 향후 진보는 계속 업계를 형성해 나갈 것으로 보입니다. 눈 건강에 대한 사람들의 의식이 높아지고 조기 개입이 더욱 중요해짐에 따라 시장은 지속적인 성장을 이루고 있습니다.

안과용 의약품 시장 동향

처방약 : 안과 치료의 원동력

부문 개요 : 처방약은 안과 치료에서 매우 중요한 역할을 하며, 녹내장, 안구건조증, 망막 질환 등 광범위한 증상에 대응하고 있습니다. 이러한 의약품은 효능과 정확도가 높기 때문에 의학적 모니터링이 필요합니다. 처방전 안과 치료제는 시장 점유율의 약 65%를 차지하며 안과 치료 관리에서 지배적인 역할을 보여줍니다.

성장의 원동력 : 노화 황반 변성과 녹내장과 같은 만성 안질환의 유병률의 상승이 처방 안과 약 수요를 끌어 올리고 있습니다. 서방형 기술과 병용 요법의 진보로 환자의 컴플라이언스와 치료 성적이 더욱 향상되었습니다. 세계의 고령화 사회는 특히 이러한 질병에 걸리기 쉽고, 업계의 연구개발 노력 증가와 함께 이 분야의 성장을 뒷받침할 것으로 예상됩니다.

경쟁 구도 : 처방약 시장의 주요 기업은 경쟁력을 높이기 위해 기술 혁신에 주력하고 있습니다. 유리체 내 임플란트와 같은 고급 약물전달 시스템의 개발은 복잡한 안질환에 대한 새로운 솔루션을 제공합니다. 전략적 제휴와 인수는 제품 포트폴리오를 확대하고, 맞춤형 의료의 상승은 표적 치료의 개발을 촉진하고 있습니다. 그러나 유전자 치료와 재생 의학을 포함한 잠재적인 혼란이 시장을 재구성 할 수 있습니다.

북미 : 안과 의료 혁신의 견인역

지역 역학 : 북미는 계속해서 세계 안과용 의약품 시장 규모를 선도하고 있으며, 강력한 성장과 혁신을 보여주고 있습니다. 고도로 발달한 헬스케어 인프라와 강력한 시장 존재로 인해 북미는 2024년부터 2029년까지 연평균 복합 성장률(CAGR) 8% 이상으로 확대될 것으로 예상되고 있습니다. 이 성장의 원동력이 되는 것은 기술의 진보, 헬스케어 투자 증가, 눈의 건강에 대한 의식 증가입니다.

마켓 카탈리스트 : 북미가 안과용 의약품으로 우위를 차지하는 원동력이되는 몇 가지 요인이 있습니다. 이 지역은 고령화가 진행되고 있어 생활습관과 관련된 안질환이 만연하고 있기 때문에 환자수가 많습니다. 또한 호의적인 보험 상환 정책과 지원 규제 환경은 의약품 기술 혁신과 환자 치료에 대한 접근을 뒷받침하고 있습니다. 산업연구에 왕성한 자금공급과 정밀의료에 대한 주력으로 북미는 안과용 의약품 개발의 리더십을 유지할 것으로 예상됩니다.

전략적 과제 시장에서의 지위를 유지하기 위해 기업은 유전자 치료 및 재생 의료 등의 연구 분야에 투자하고 있습니다. 혁신을 가속화하기 위해서는 생명 공학 기업 및 학술 기관과의 협력이 필수적입니다. 또한 원격 의료 및 인공지능(AI)을 포함한 디지털 건강 솔루션이 안과 의료에 통합되고 있습니다. 기업은 또한 하이테크 기업의 진입과 가치 기반 케어 모델에 의한 경쟁 구도의 잠재적인 변화에도 대비해야 합니다.

안과용 의약품 업계 개요

시장 역학 : 세계 기업이 통합 상황을 지배

이 세계의 업계는 광범위한 제품 포트폴리오를 보유한 선도적 다국적 제약 회사에 의해 거의 지배되고 있습니다. 노바티스, 로슈, 리제네론 등 주요 기업들은 광범위한 연구개발 능력과 강력한 판매망으로 안과용 의약품 시장에서 큰 점유율을 차지하고 있습니다. 시장은 통합되어 있으며 소수 시장 리더와 주요 기업이 총 매출의 대부분을 차지합니다. 진입장벽이 높고 규제 프레임워크가 복잡하고 연구개발에 많은 투자가 필요하기 때문에 신규 진입 기업이 기존기업과 경쟁하기는 어렵습니다.

시장 리더 : 혁신과 파이프라인의 힘이 성공의 원동력

노바티스, 로슈, 리제네론 퍼머슈티컬즈와 같은 주요 기업들은 망막 질환 치료 및 기타 안과 영역에서 큰 진보를 이루고 있습니다. 노바티스의 망막치료에 있어서의 기술 혁신과 리제네론의 노화황반변성 치료에 있어서의 EYLEA의 성공이 그 예입니다. 또한 이 시장 리더는 향후 수년간 상시가 예정된 여러 후기 임상 후보 화합물을 보유한 강력한 제품 파이프라인에 의해 강화되고 있습니다. 광대한 세계 존재와 건강 관리 이해 관계자간의 깊은 관계가 경쟁 우위를 확고하게합니다.

미래 성공을 위한 전략 : 충족되지 않은 요구와 신기술에 주력

향후 시장 성장을 이루기 위해 기업은 안과 부위의 미충족 요구, 특히 안구건조증 및 당뇨병성 망막증과 같은 치료에 주력해야 합니다. 유전자 치료나 서방형 약물전달 시스템 등의 신기술을 활용하면 경쟁력을 높일 수 있다고 생각됩니다. 예를 들어, 녹내장을 위한 장기간 작용하는 안구 임플란트를 개발하는 기업은 전통적인 치료에서 큰 시장 점유율을 얻을 수 있습니다. 아시아태평양과 같은 고성장 지역으로의 진출은 혁신을 촉진하기 위해 생명 공학 기업 및 연구 기관과의 제휴와 함께 중요합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 눈과 관련된 질환의 발생률과 유병률 증가

- 신약 개발에 관련된 연구 개발의 활성화

- 병용 요법 개발에 주목의 고조

- 시장 성장 억제요인

- 대중약 특허 만료

- 신흥 국가의 의료 보험 부족

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자, 소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 약제 클래스별

- 항녹내장약

- 안구건조증 치료제

- 안과용 항알레르기, 항염증제

- 망막용 약

- 항감염증약

- 기타 의약품

- 제품 유형별

- 일반용 의약품

- 처방약

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 기업 프로파일

- Aerie Pharmaceuticals Inc.

- AbbVie(Allergan)

- Bausch Health Companies Inc.

- Bayer AG

- F. Hoffmann-La Roche Ltd

- Novartis AG

- Viatris Inc.

- Regeneron Pharmaceuticals Inc.

- Santen Pharmaceutical Co. Ltd

- Alcon

- Sun Pharmaceutical Industries Ltd.

- Teva Pharmaceutical Industries Ltd.

제7장 시장 기회와 앞으로의 동향

SHW 25.04.01The Ophthalmic Drugs Market size is estimated at USD 37.49 billion in 2025, and is expected to reach USD 55.71 billion by 2030, at a CAGR of 8.24% during the forecast period (2025-2030).

It is witnessing significant growth, underpinned by various factors driving both innovation and expansion in the industry. Key drivers include the increasing prevalence of eye-related disorders and advancements in drug development technologies, which are reshaping the market landscape.

Megatrends Shaping the Industry: The global rise in ocular conditions, an aging population, and advancements in drug formulation technologies are creating robust foundations for market growth. These factors, along with specific industry drivers, are pushing the ophthalmic drugs industry to new heights.

Increasing Incidence and Prevalence of Eye-related Disorders: The growing number of individuals with vision impairment is a major factor driving the market growth. Data from the National Eye Institute projects that by 2030, age-related macular degeneration will impact 3.7 million individuals in the United States. Additionally, the same source estimates that glaucoma will affect 4.3 million Americans by 2030. The high burden of these eye diseases underscores the urgent need for new and effective ophthalmic treatments, driving the market forward.

Rising Research and Development Pertaining to the Development of Novel Drugs: Global ophthalmic drugs market research says that the industry is benefiting from increased R&D activity aimed at creating novel therapeutic solutions. The rise in clinical trials and drug approvals highlights this trend. In 2023, the FDA accepted a New Drug Application for CyclASol, a novel anti-inflammatory product for dry eye disease. Similarly, the European launch of a ranibizumab biosimilar by Xbrane Biopharma AB and STADA Arzneimittel AG showcases the surge in cost-effective treatment options. These innovative drugs are expanding the therapeutic landscape and boosting the market at a decent growth rate.

Increasing Focus on Developing Combination Therapies: The emphasis on combination therapies within the ophthalmic drugs market is growing. These treatments offer superior therapeutic results for managing complex ocular diseases. For instance, in July 2023, Tenpoint Therapeutics secured funding to spearhead its launch aimed at combating degenerative eye diseases. The company specializes in combining various cell-based therapeutics and crafting treatments tailored to individual cases. Their approach centers on rejuvenating eye cells compromised by age-related or inherited ailments. Such partnerships are fueling innovation in the field, accelerating market expansion by addressing unmet medical needs.

Global industry is on a steady growth trajectory, driven by these market trends and developments. Future advancements in drug innovation, personalized treatments, and increased access to eye care will continue to shape the industry. As public awareness around eye health rises and early intervention becomes more critical, the market is poised for sustained growth.

Ophthalmic Drugs Market Trends

Prescription Drugs: Driving Force in Ophthalmic Treatments

Segment Overview: Prescription drugs play a pivotal role in ophthalmic treatments, addressing a wide range of conditions including glaucoma, dry eye, and retinal disorders. These drugs require medical oversight due to their potency and precision. Prescription ophthalmic medications account for approximately 65% of the market share, illustrating their dominant role in eye care management.

Growth Drivers: The rising prevalence of chronic eye disorders, such as age-related macular degeneration and glaucoma, is boosting demand for prescription ophthalmic drugs. Advances in sustained-release technologies and combination therapies are further enhancing patient compliance and treatment outcomes. The global aging population is particularly susceptible to these disorders, which, along with increasing industry research and development efforts, are expected to bolster the growth of this segment.

Competitive Landscape: Leading companies in the prescription drug market are focusing on innovation to gain a competitive edge. The development of advanced drug delivery systems, such as intravitreal implants, is providing new solutions for complex eye conditions. Strategic collaborations and acquisitions are expanding product portfolios, while the rise of personalized medicine is driving the development of targeted therapies. However, potential disruptions, including gene therapies and regenerative medicine, may reshape the market.

North America: Leading the Charge in Ophthalmic Innovation

Regional Dynamics: North America continues to lead the global ophthalmic drugs market size, exhibiting robust growth and innovation. With a highly developed healthcare infrastructure and strong market presence, North America is expected to expand at a compound annual growth rate (CAGR) of over 8% from 2024 to 2029. This growth is fueled by technological advancements, increasing healthcare investments, and rising awareness around eye health.

Market Catalysts: Several factors are driving North America's dominance in ophthalmic drugs. The region's aging population and the prevalence of lifestyle-related ocular disorders contribute to a significant patient base. Favorable reimbursement policies and a supportive regulatory environment also encourage drug innovation and patient access to treatments. With strong funding for industry research and a focus on precision medicine, North America is expected to maintain its leadership in ophthalmic drug development.

Strategic Imperatives: To maintain their market position, companies are investing in research areas like gene therapy and regenerative medicine. Collaborations with biotech firms and academic institutions are essential for accelerating innovation. Additionally, digital health solutions, including telemedicine and artific ial intelligence (AI), are increasingly integrated into eye care. Companies should also prepare for potential shifts in the competitive landscape, driven by tech entrants and value-based care models.

Ophthalmic Drugs Industry Overview

Market Dynamics: Global Players Dominate Consolidated Landscape

This global industry is largely controlled by major multinational pharmaceutical firms with broad product portfolios. Leading companies such as Novartis, Roche, and Regeneron hold substantial ophthalmic drugs market share due to their expansive R&D capabilities and strong distribution networks. The market is consolidated, with a few market leaders and key players dominating a large portion of the total revenue. High entry barriers, complex regulatory frameworks, and the need for significant investment in R&D make it challenging for new entrants to compete with established players.

Market Leaders: Innovation and Pipeline Strength Drive Success

Leading companies like Novartis, Roche, and Regeneron Pharmaceuticals Inc. have made significant strides in retinal disease treatments and other areas of ophthalmology. Novartis' innovations in retinal therapies and Regeneron's success with EYLEA in treating age-related macular degeneration exemplify this. These market leaders are also bolstered by their strong product pipelines, with several late-stage clinical candidates set to launch in the coming years. Their vast global presence and deep relationships with healthcare stakeholders solidify their competitive advantage.

Strategies for Future Success: Focus on Unmet Needs and Emerging Technologies

To capture future market growth, companies must focus on unmet needs in ophthalmology, particularly in treating conditions like dry eye disease and diabetic retinopathy. Leveraging emerging technologies such as gene therapies and sustained-release drug delivery systems could provide a competitive edge. Companies developing long-acting intraocular implants for glaucoma, for instance, could capture significant market share from traditional treatments. Expansion into high-growth regions such as the Asia-Pacific will be critical, alongside partnerships with biotechnology firms and research institutions to foster innovation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Incidence and Prevalence of Eye-related Disorders

- 4.2.2 Rising Research and Development Pertaining to the Development of Novel Drugs

- 4.2.3 Increasing Focus on Developing Combination Therapies

- 4.3 Market Restraints

- 4.3.1 Loss of Patent Protection for Popular Drugs

- 4.3.2 Lack of Health Insurance in the Developing Countries

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value- USD)

- 5.1 By Drug Class

- 5.1.1 Anti-glaucoma Drugs

- 5.1.2 Dry Eye Drugs

- 5.1.3 Ophthalmic Anti-allergy/Inflammatory

- 5.1.4 Retinal Drugs

- 5.1.5 Anti-infective Drugs

- 5.1.6 Other Drugs

- 5.2 By Product Type

- 5.2.1 OTC Drugs

- 5.2.2 Prescription Drugs

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Aerie Pharmaceuticals Inc.

- 6.1.2 AbbVie (Allergan)

- 6.1.3 Bausch Health Companies Inc.

- 6.1.4 Bayer AG

- 6.1.5 F. Hoffmann-La Roche Ltd

- 6.1.6 Novartis AG

- 6.1.7 Viatris Inc.

- 6.1.8 Regeneron Pharmaceuticals Inc.

- 6.1.9 Santen Pharmaceutical Co. Ltd

- 6.1.10 Alcon

- 6.1.11 Sun Pharmaceutical Industries Ltd.

- 6.1.12 Teva Pharmaceutical Industries Ltd.