|

시장보고서

상품코드

1685770

크로마토그래피 시약 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Chromatography Reagents - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

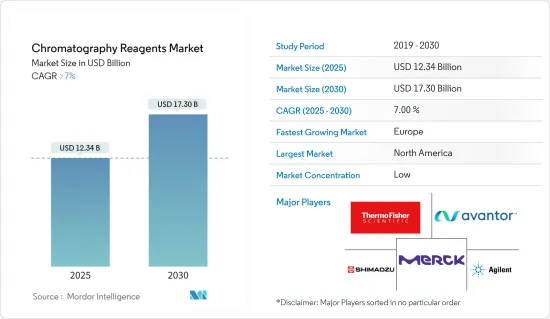

크로마토그래피 시약 시장 규모는 2025년에 123억 4,000만 달러에 달할 것으로 추정됩니다. 2030년에는 173억 달러에 이를 것으로 예상되며, 예측 기간 중(2025-2030년) CAGR은 7%를 나타낼 것으로 전망됩니다.

2021년에는 유행에 기인한 제약 산업의 다양한 의약품 수요가 증가함에 따라 시장은 수요의 급증을 보였습니다. 많은 국가들이 물과 환경 안전에 관한 다양한 규정을 부과하고 있습니다. 이로 인해 전 세계적으로 조사된 시장 수요가 증가하고 있습니다.

주요 하이라이트

- 제약 업계에서 크로마토그래피 시약 수요 증가가 시장 성장을 가속할 것으로 예상됩니다.

- 그러나 크로마토그래피 시약의 높은 비용이 시장 확대를 방해할 것으로 예상됩니다.

- 몇몇 최종 사용자 산업에서 크로마토그래피 기술의 채택이 진행되고 있기 때문에 시장 번영의 기회가 가져올 것으로 예상됩니다.

- 북미가 세계 시장을 석권하고 있어 미국이나 캐나다 등이 최대의 소비국이 되고 있습니다.

크로마토그래피 시약 시장 동향

제약 업계 수요 증가

- 제약 산업에서 크로마토그래피는 화학물질 및 미량 원소의 존재를 확인하기 위한 샘플의 동정 및 분석, 매우 순도가 높은 물질의 대량 제조, 키랄 화합물의 분리, 혼합물의 순도 및 미지 화합물의 검출, 의약품 개발 등 다양한 작업에 사용되고 있습니다.

- HPLC 크로마토그래피 기술은 의약품 식별 및 정량에 사용되는 제약 비즈니스에서 가장 중요한 분석 기술입니다.

- 의약품의 연구 개발 및 제조는 원료 약 또는 제형에 사용됩니다.

- 모든 의약품은 환자의 위험을 최소화하기 위해 최상의 품질이어야 합니다. 개발 과정에서 연구자, 생산자 및 개발자는 다양한 기술 장비 및 액체 크로마토그래피와 같은 분석 프로세스를 활용하여 의약품이 기준을 충족하는지 확인합니다.

- 의약품은 안전하고 효과적이어야 하기 때문에 제약 업계는 세계에서 가장 엄격하게 규제되는 업계 중 하나입니다.

- 세계 제약 산업은 규모가 크고 현재 기술 혁신과 세계 인구의 건강에 대한 긍정적인 영향으로 견인되고 있습니다. 이 업계는 지난 몇 년동안 괜찮은 성장을 이루었습니다. 아스트라제네카에 따르면 2022년 세계 의약품 매출은 1조 2,140억 달러로 전년 대비 8.4%의 성장을 보였습니다.

- 또한 독일은 유럽의 주요 의약품 시장으로 세계 4위 규모를 자랑하며 약 400개 바이오테크놀러지 기업이 존재합니다. 유엔의 COMTRADE에 따르면 2022년 독일 의약품 수출액은 1,260억 1,000만 달러였습니다.

- 그러므로 제약 산업의 성장과 함께 크로마토그래피 시약에 대한 수요는 향후 몇 년동안 증가할 가능성이 높습니다.

북미의 강력한 성장

- 북미는 세계 시장 점유율을 독점하고 있습니다. 주로 식품 및 제약 업계에서 크로마토그래피 기술의 채용이 증가하고 있는 것으로, 이 지역의 크로마토그래피 시약 수요를 견인하고 있습니다.

- 미국은 크로마토그래피 시약의 주요 시장으로, 유전체학 R&D 투자 증가와 정교한 기술 가용성 등의 요인이 향후 수년간 시장을 견인할 것으로 예상됩니다.

- 미국은 세계 최대의 제약 산업 중 하나입니다. 아스트라제네카에 따르면 2022년에는 미국이 세계 의약품 매출의 45% 이상, 세계 생산량의 22%를 차지하고 의약품 매출을 독점했습니다. 2024년 미국 의약품 매출액은 6,330억 달러에 달했습니다.

- 미국 농무부에 따르면 2022년에는 약 1조 5,000억 달러가 되었고, 식품 사업은 미국 경제의 상당 부분을 차지했습니다. GDP의 거의 4%를 차지하는 식음료 부문은 일본 경제에서 가장 큰 제조 부문 중 하나입니다. 슈퍼마켓과 기타 식품점으로 구성된 식품 소매 부문도 마찬가지로 연간 8,000억 달러를 초과하는 수익을 올리고 있으며 업계의 상당 부분을 차지하고 있습니다.

- 게다가 미국 농무부에 따르면 멕시코는 미국, 브라질에 이어 아메리카 3위의 식품 가공 산업입니다. 농업시장자문그룹(GCMA)의 데이터에 따르면 이 나라의 식품 생산량은 2022년 2억 8,700만 톤에서 2023년 2억 9,000만 톤에 이르렀습니다.

- 위와 같은 요인으로부터 북미는 가까운 미래에 조사 대상 시장에서 강한 수요가 예상됩니다.

크로마토그래피 시약 산업 개요

크로마토그래피 시약 시장은 세분화됩니다. 주요 기업(특별한 순서 없음)에는 Merck KGaA, Thermo Fisher Scientific Inc., Avantor, Inc., Agilent Technologies, Inc., 시마즈 제작소 등이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 제약 업계에서의 크로마토그래피 시약 수요 증가

- 생명공학 분야에서 R&D 투자 증가

- 기타 촉진요인

- 성장 억제요인

- 높은 크로마토그래피 시약 비용

- 기타 억제요인

- 업계 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 강도

제5장 시장 세분화

- 유형

- 버퍼

- 이온쌍 시약

- 용매

- 기타 유형(유도체화 시약 등)

- 이동상의 물리적 상태

- 기체 크로마토그래피 시약

- 액체 크로마토그래피 시약

- 초임계 유체 크로마토그래피(SFC) 시약

- 기술

- 이온 교환

- 친밀도 교환

- 크기 제외

- 소수성 상호작용

- 혼합 모드

- 기타 기술(흡착 크로마토그래피, 파티션 크로마토그래피 등)

- 용도

- 의약품

- 식음료

- 수질 및 환경 분석

- 기타 용도(법의학 분석, 화장품 응용 등)

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 시장 점유율(%)**/랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- Agilent Technologies, Inc.

- Avantor, Inc.

- ITW Reagents

- Merck KGaA

- Regis Technologies Inc.

- Santa Cruz Biotechnology, Inc.

- Shimadzu Corporation

- Thermo Fisher Scientific Inc.

- Tokyo Chemical Industry

- Tosoh India Pvt. Ltd.

- Waters Corporation

제7장 시장 기회와 앞으로의 동향

- 복수의 최종 사용자 산업에 있어서 크로마토그래피 기술의 채용 확대

- 기타 기회

The Chromatography Reagents Market size is estimated at USD 12.34 billion in 2025, and is expected to reach USD 17.30 billion by 2030, at a CAGR of greater than 7% during the forecast period (2025-2030).

The market saw a surge in demand in 2021 due to the increase in demand for various medicines in the pharmaceutical industry owing to the pandemic. Many countries have imposed various regulations with regard to water and the safety of the environment. This has led to increased demand in the market studied worldwide.

Key Highlights

- Increasing demand for chromatography reagents from the pharmaceutical sector is expected to fuel market growth.

- However, the high cost of chromatography reagents is anticipated to hamper market expansion.

- The growing adoption of chromatographic techniques in several end-user industries is expected to provide opportunities for the market to flourish.

- The North American region dominated the market around the world, with countries like the United States and Canada being the biggest consumers.

Chromatography Reagents Market Trends

Increasing Demand from Pharmaceutical Sector

- In the pharmaceutical industry, chromatography is used for a variety of tasks, including identifying and analyzing samples for the presence of chemicals or trace elements, preparing large quantities of extremely pure materials, separating chiral compounds, detecting mixture purity and unknown compounds, and drug development.

- The HPLC chromatography technique is the most important analytical technique used in the pharmaceutical business for identifying and quantifying pharmaceuticals.

- During the research, development, and production of medicine, this is used either in the active pharmaceutical ingredient or in the formulations.

- All pharmaceutical items must be of the greatest quality to ensure the least amount of danger to patients. During the development process, researchers, producers, and developers utilize a variety of technical equipment and analytical processes, like liquid chromatography, to guarantee that the items satisfy the criteria.

- Since drug products must be safe and effective, the pharmaceutical industry is one of the most heavily regulated industries in the world.

- The global pharmaceutical industry is larger and currently driven by innovations and positive implications for the global population's health. The industry has been witnessing decent growth over the past several years. According to AstraZeneca, the global pharmaceutical sales in 2022 were USD 1,214 billion, representing a growth of 8.4% compared to the previous year.

- Further, Germany constitutes the major European pharmaceutical market and the fourth-largest worldwide, with almost 400 biotech companies. According to the United Nations, COMTRADE, Germany's exports of pharmaceutical products were USD 126.01 billion in 2022.

- Therefore, with the growth of the pharmaceutical industry, the demand for chromatography reagents is likely to rise during the coming years.

Strong Growth in the North American Region

- The North American region dominated the global market share. The increased adoption of chromatography techniques, majorly in the food and beverage and pharmaceutical industries, drives the demand for chromatography reagents in the region.

- The United States is the leading market for chromatography reagents, with factors such as rising investments in genomics research and development and the availability of sophisticated technologies projected to drive the market in the coming years.

- The United States has one of the world's largest pharmaceutical industries. According to AstraZeneca, In 2022, the United States dominated pharmaceutical sales with a share of over 45% of global pharmaceutical sales and 22% of global production. The projected pharmaceutical sales for the United States in 2024 are expected to be USD 633 billion.

- According to the USDA, in 2022, about USD 1.5 trillion, the food business represents a sizeable portion of the United States economy. At almost 4% of the GDP, the food and beverage sector is one of the largest manufacturing sectors in the country's economy. With more than USD 800 billion in annual revenues, the food retail sector, which comprises supermarkets and other food stores, is likewise a sizable portion of the industry.

- Further, according to the USDA, Mexico is the third-largest food processing industry in the Americas, after the United States and Brazil. According to data from the Agricultural Markets Advisory Group (GCMA), the country's food production is anticipated to reach 290 million tons in 2023, growing from 287 million tons in 2022.

- Due to all the factors mentioned above, North America is expected to have a strong demand in the market studied in the near future.

Chromatography Reagents Industry Overview

The chromatography reagents market is fragmented in nature. The major players (not in any particular order) include Merck KGaA, Thermo Fisher Scientific Inc., Avantor, Inc., Agilent Technologies, Inc., and Shimadzu Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Chromatography Reagents from the Pharmaceutical Sector

- 4.1.2 Increasing R&D Investment in Biotechnology Sector

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Cost of Chromatography Reagents

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Buffers

- 5.1.2 Ion Pair Reagents

- 5.1.3 Solvents

- 5.1.4 Other Types (Derivatization Reagents, Etc.)

- 5.2 Physical State of Mobile Phase

- 5.2.1 Gas Chromatography Reagents

- 5.2.2 Liquid Chromatography Reagents

- 5.2.3 Super Critical Fluid Chromatography (SFC) Reagents

- 5.3 Technology

- 5.3.1 Ion Exchange

- 5.3.2 Affinity Exchange

- 5.3.3 Size Exclusion

- 5.3.4 Hydrophobic Interaction

- 5.3.5 Mixed Mode

- 5.3.6 Other Technologies (Adsorption Chromatography, Partition Chromatography, Etc.)

- 5.4 Application

- 5.4.1 Pharmaceutical

- 5.4.2 Food and Beverages

- 5.4.3 Water and Environmental Analysis

- 5.4.4 Other Applications (Forensic Analysis, Cosmeceutical Application, Etc.)

- 5.5 Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 Italy

- 5.5.3.4 France

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Agilent Technologies, Inc.

- 6.4.2 Avantor, Inc.

- 6.4.3 ITW Reagents

- 6.4.4 Merck KGaA

- 6.4.5 Regis Technologies Inc.

- 6.4.6 Santa Cruz Biotechnology, Inc.

- 6.4.7 Shimadzu Corporation

- 6.4.8 Thermo Fisher Scientific Inc.

- 6.4.9 Tokyo Chemical Industry

- 6.4.10 Tosoh India Pvt. Ltd.

- 6.4.11 Waters Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Adoption for Chromatographic Techniques in Several End-user Industries

- 7.2 Other Opportunities