|

시장보고서

상품코드

1685780

살충제 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Insecticide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

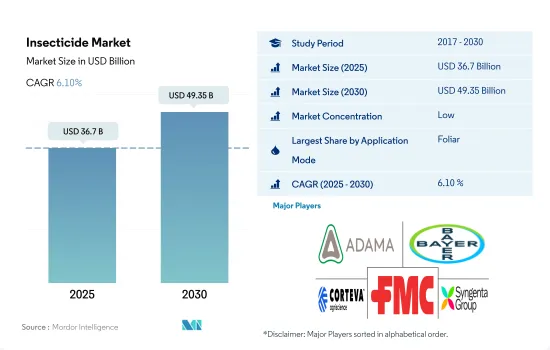

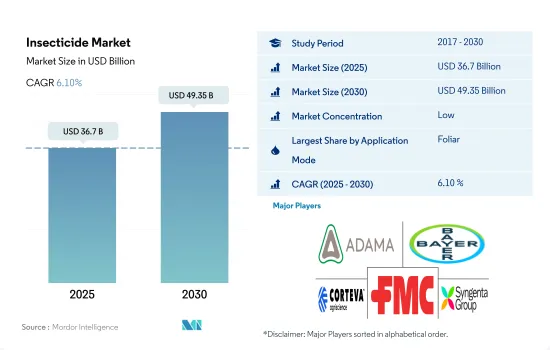

살충제 시장 규모는 2025년에 367억 달러로 추계되며, 2030년에는 493억 5,000만 달러에 달할 것으로 예측되며, 예측 기간(2025-2030년)의 CAGR은 6.10%로 성장합니다.

해충 압력 증가와 해충으로부터 작물을 보호해야 할 필요성이 살충제 수요를 주도

- 해충으로부터 작물을 보호하기 위해 다양한 살포 방법으로 살충제 사용이 증가하고 있으며, 2022년에는 엽면 살포 분야가 전체 살충제 시장의 56.9%를 차지하여 큰 비중을 차지하고 있습니다. 이는 해충 방제 압력 증가와 해충 방제 효과, 빠른 효과, 표적 방제 때문인 것으로 보입니다.

- 금액 기준으로 세계 살충제 시장에서 종자 처리 방법의 CAGR은 2023-2029년 4.5%를 나타낼 것으로 예상됩니다. 이 방법은 주로 진딧물, 엉겅퀴벌레, 꽃매미, 노린재, 총채벌레 등 종자나 묘목을 가해하는 많은 해충을 작물 생애주기 초기에 방제할 수 있으므로 주로 채택되고 있습니다.

- 살충제 시장의 토양 처리 시장은 2023-2029년 4.1%의 연평균 복합 성장률(CAGR)을 나타낼 것으로 예상됩니다. 밀, 콩, 유채, 코코아, 커피 등 경제적으로 중요한 작물의 뿌리 성장에 영향을 미치는 주요 해충은 슬러그, 와이어웜, 선충, 흰점박이꽃무지, 토양매미충 등입니다. 따라서 이러한 해충으로부터 작물을 보호하기 위해 토양처리 측면에서 살충제 수요가 증가할 것으로 예상됩니다.

- 농가 사이에서 화학 관개법에 대한 인식이 높아지고 있습니다. 살충제 살포와 관개를 결합하여 농가는 시간과 노동력을 절약할 수 있으며, 대규모 농업 경영을 관리하는 농가에 편리한 선택이 되고 있습니다. 이러한 요인으로 인해 이 적용 모드의 살충제 시장 가치는 예측 기간(2023-2029) 동안 3.7%의 연평균 복합 성장률(CAGR)로 성장할 것으로 예상됩니다.

- 이러한 적용 방법의 세계 살충제 시장은 2023-2029년 4.2%의 연평균 복합 성장률(CAGR)을 보이고, 큰 성장을 보일 것으로 예상됩니다.

기후 조건의 변화에 따른 재배 면적 확대가 시장 성장에 기여

- 세계 인구 증가와 식량 증산에 대한 수요로 인해 농업 생산이 확대되면서 해충으로부터 농작물을 보호하기 위한 살충제 수요가 증가하고 있습니다. 지난 기간(2017-2022년) 동안 살충제 시장은 84억 4,980만 달러 규모로 성장했습니다.

- 남미는 농업 생산의 주요 지역 중 하나이며, 2022년 시장 규모는 24.9%를 차지했습니다. 콩, 옥수수, 사탕수수 및 기타 작물의 막대한 생산량은 해충을 효과적으로 관리하기 위한 살충제에 대한 큰 수요를 창출하고 있습니다. 남방거세미나방(Spodoptera eridania)과 같은 곤충의 침입이 증가하면서 시장 성장을 가속하고 있습니다.

- 아시아태평양은 살충제 시장에서 가장 큰 시장 점유율을 차지하고 있으며, 예측 기간(2023-2029년) 동안 3.9%의 연평균 복합 성장률(CAGR)을 기록하여 가장 빠르게 성장할 것으로 예상됩니다. 기후 변화로 인해 농작물에 피해를 줄 수 있는 해충이 확산되고 있습니다. 따라서 살충제는 이러한 해충에 대처하고 작물의 생산성을 보장하는 효율적인 수단이기 때문에 수요가 증가할 것으로 예상됩니다.

- 북미는 예측 기간(2023-2029년) 동안 4.7%의 연평균 복합 성장률(CAGR)을 나타낼 것으로 예상됩니다. 농작물 보호의 필요성과 침입성 해충의 유입 또는 확산이 결합되어 이러한 새로운 위협을 관리하고 제거하기 위한 살충제에 대한 수요가 증가할 것으로 예상됩니다.

- 그러나 유럽과 아프리카는 농업 부문이 잘 발달되어 있으며, 세계 살충제 시장에서 중요한 역할을 하고 있습니다. 이들 지역의 CAGR은 해당 기간 중 각각 4.6%와 3.7%를 나타낼 것으로 예상됩니다.

- 세계 살충제 시장은 2023-2029년 동안 CAGR 4.2%를 나타낼 것으로 예상됩니다. 기후 변화에 따른 농업 부문의 급격한 확장이 시장 성장을 가속하고 있습니다.

세계 살충제 시장 동향

지구 온난화로 인한 해충 증가로 살충제 사용량 증가

- 전 세계 평균 화학 살충제 소비량은 농지 1헥타르당 918.7g입니다. 이는 농업의 집약화, 해충 증가, 세계 식량안보를 보장하기 위한 높은 수확량과 작물 생산성의 필요성 등의 요인으로 인해 해마다 증가하고 있습니다. 유엔식량농업기구의 데이터에 따르면 매년 전 세계 농작물 생산량의 40%가 해충에 의해 손실되고 있으며, 그 경제적 손실은 평균 약 700억 달러에 달할 전망입니다.

- 유럽은 세계 기타 지역에 비해 살충제 사용량이 많으며, 특히 독일은 헥타르당 3,028.0g으로 가장 많이 사용하고 있습니다. 이는 작물 수확량을 극대화하는 데 중점을 둔 매우 집약적인 농법을 사용하기 때문인 것으로 보입니다. 집약적 농업에서는 해충을 관리하고 최적의 작물 생산을 보장하기 위해 살충제를 포함한 높은 투입량을 사용하는 경우가 많습니다. 유럽에 이어 아시아태평양의 평균 살충제 살포량은 1헥타르당 975.1g입니다.

- 북미 국가 중 미국이 헥타르당 살충제 소비량이 가장 많으며, 2022년에는 791.7g을 기록했습니다. 이는 농작물 재배 면적이 넓고 끊임없이 변화하는 기후 조건으로 인해 해충의 침입에 노출될 가능성이 높기 때문입니다.

- 지구 온난화로 인한 기후 조건의 변화는 특정 해충에 유리한 조건을 만들어 심각한 대유행을 일으키고 있습니다. 예를 들어 2020년에 발생한 메뚜기 대발생으로 23개국, 즉 중동 9개국, 북중동 및 아프리카 11개국, 남아시아 3개국이 심각한 피해를 입어 85억 달러의 손실이 발생한 것으로 추산됩니다. 이러한 상황으로 인해 농가는 농업에서 살충제를 다량으로 사용해야만 했습니다.

이미다클로프리드는 가장 저렴한 가격의 살충제이며, 광범위한 활성 스펙트럼을 가지고 있습니다.

- 람다-시할로트린은 피레스로이드계 살충제에 속하며 국화꽃에 함유된 천연 피레트린을 모델로 한 합성 화학물질입니다. 람다-시할로트린은 면화, 옥수수, 콩, 채소, 과일 등의 작물에서 진딧물, 엉겅퀴, 노린재, 흰등멸구, 총채벌레, 각종 애벌레 등의 해충을 방제하는 데 사용됩니다. 이 활성 성분은 신경독으로 작용하여 곤충의 신경계를 표적으로 삼습니다. 신경세포의 정상적인 작용을 억제하고 마비를 일으켜 결국 해충을 죽게 하는 것. 2022년 가격은 1톤당 2만 2,700달러로 책정되었습니다.

- 시퍼메트린은 비합성 피레스로이드계로 벼룩, 딱정벌레, 흰개미, 바퀴벌레, 흰개미, 흰개미, 무당벌레, 전갈, 황색 재킷을 방제하는 데 사용되며, 2022년 가격은 2만 1,000달러였습니다. 브라질은 세계 3대 시퍼메트린 수입국 중 하나이며, EU-Mercosur 협정에 따라 유럽연합은 브라질의 주요 수출국이 되었습니다.

- 에마멕틴 벤조산염은 아벨멕틴이라는 화학적 분류에 속하는 살충제입니다. 신경계를 표적으로 삼아 해충을 죽입니다. 신경세포의 특정 수용체에 결합하여 해충을 마비시켜 결국 사망에 이르게 합니다. 에마멕틴 벤조산염은 유럽 국가에서 농업의 다양한 해충 방제에 사용되고 있습니다. 가격은 톤당 1만 7,300 달러입니다.

- 이미다클로프리드는 네오니코티노이드 계통의 살충제로 진딧물, 노린재, 흰등멸구, 꽃벵이, 엉겅퀴, 일부 딱정벌레 등 다양한 해충을 효과적으로 방제할 수 있습니다. 이 활성 성분의 2022년 가격은 톤당 1만 7,170달러였습니다. 말라티온은 살충제 중 가장 저렴한 화학물질로, 2022년 가격은 톤당 12,500달러였습니다.

살충제 업계의 개요

살충제 시장은 세분화되어 있으며, 상위 5사에서 33.15%를 차지하고 있습니다. 이 시장의 주요 기업은 다음과 같습니다. ADAMA Agricultural Solutions Ltd., Bayer AG, Corteva Agriscience, FMC Corporation and Syngenta Group(알파벳순).

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 개요와 주요 조사 결과

제2장 리포트 오퍼

제3장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 1헥타르당 농약 소비량

- 유효 성분의 가격 분석

- 규제 프레임워크

- 아르헨티나

- 호주

- 브라질

- 캐나다

- 칠레

- 중국

- 프랑스

- 독일

- 인도

- 인도네시아

- 이탈리아

- 일본

- 멕시코

- 미얀마

- 네덜란드

- 파키스탄

- 필리핀

- 러시아

- 남아프리카공화국

- 스페인

- 태국

- 우크라이나

- 영국

- 미국

- 베트남

- 밸류체인과 유통 채널 분석

제5장 시장 세분화

- 사용 방법

- 화학 관개

- 엽면살포

- 훈증

- 종자 처리

- 토양 처리

- 작물 유형

- 상업 작물

- 과일·채소

- 곡물

- 두류·지방 종자

- 잔디·관상용

- 지역

- 아프리카

- 국가별

- 남아프리카공화국

- 기타 아프리카

- 아시아태평양

- 국가별

- 호주

- 중국

- 인도

- 인도네시아

- 일본

- 미얀마

- 파키스탄

- 필리핀

- 태국

- 베트남

- 기타 아시아태평양

- 유럽

- 국가별

- 프랑스

- 독일

- 이탈리아

- 네덜란드

- 러시아

- 스페인

- 우크라이나

- 영국

- 기타 유럽

- 북미

- 국가별

- 캐나다

- 멕시코

- 미국

- 기타 북미 지역

- 남미

- 국가별

- 아르헨티나

- 브라질

- 칠레

- 기타 남미 국가

- 아프리카

제6장 경쟁 구도

- 주요 전략적 움직임

- 시장 점유율 분석

- 기업 상황

- 기업 개요

- ADAMA Agricultural Solutions Ltd.

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Jiangsu Yangnong Chemical Co. Ltd

- Nufarm Ltd

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Porter's Five Forces 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원과 참고 문헌

- 도표

- 주요 인사이트

- 데이터 팩

- 용어집

The Insecticide Market size is estimated at 36.7 billion USD in 2025, and is expected to reach 49.35 billion USD by 2030, growing at a CAGR of 6.10% during the forecast period (2025-2030).

The rising pest pressure and the need to protect crops from damaging insects are driving the demand for insecticides

- Insecticide use is increasing through different application modes to protect crops from insect pests. In 2022, the foliar segment held the major share, accounting for 56.9% of the overall insecticide market. This could be attributed to increasing pest pressure and its effectiveness in controlling insects, rapid action, and targeted control.

- In terms of value, the seed treatment method in the global insecticide market is expected to record a CAGR of 4.5% between 2023 and 2029. This method is being majorly adopted because it protects against many pests that attack seeds or seedlings, such as aphids, thrips, wireworms, and beetles, at the very beginning of a crop's life cycle.

- Soil treatment in the insecticide market is expected to record a 4.1% CAGR between 2023 and 2029. The main pests affecting the root growth of economically significant crops such as wheat, soybean, oil palm, cocoa, and coffee are slugs, wireworms, fungi gnats, and soil mealybugs. Therefore, to protect crops from these pests, the demand for insecticides in terms of soil treatment is expected to increase.

- Farmers are becoming more and more aware of the chemigation method. By combining insecticide application with irrigation, farmers can save time and labor, making it a convenient choice for farmers managing large-scale agricultural operations. Due to these factors, the insecticide market value in this application mode is projected to record a 3.7% CAGR during the forecast period (2023-2029).

- The global insecticide market in these application methods is expected to witness significant growth and is projected to record a 4.2% CAGR from 2023 to 2029.

The expansion of cropland areas with changes in climate conditions is contributing to the growth of the market

- The increase in global population and the need for higher food production have led to the expansion of agricultural production, which, in turn, boosted the demand for insecticides to protect the crops from damaging pests. During the historical period (2017-2022), the insecticide market grew by USD 8,449.8 million.3

- South America was one of the major regions in agriculture production, with a 24.9% market value in 2022. The vast production of soybeans, corn, sugarcane, and other crops creates a significant demand for insecticides to manage pests effectively. The rise of infestation of insects such as southern armyworm (Spodoptera eridania) has driven the growth of the market.

- Asia-Pacific holds the largest insecticide market value share, and the market is anticipated to grow fastest in the region, registering a CAGR of 3.9% during the forecast period (2023-2029). Insect pests that could damage crops are spreading due to the changing climate. Consequently, the demand for insecticides is expected to rise as they are efficient tools for addressing these pests and ensuring crop productivity.

- North America is projected to register a CAGR of 4.7% during the forecast period (2023-2029). The need to protect the crops, coupled with the introduction or spread of invasive pests, could lead to increased demand for insecticides to manage and control these new threats.

- However, Europe and Africa have a substantial agricultural sector and play a vital role in the global insecticide market. These regions are projected to register CAGRs of 4.6% and 3.7%, respectively, during the period.

- The global insecticide market is projected to register a CAGR of 4.2% during 2023-2029. The rapidly expanding agriculture sector with a changing climate is driving the growth of the market.

Global Insecticide Market Trends

Increased pest proliferation due to global warming is increasing the usage of insecticides

- The average global consumption of chemical insecticides is 918.7 g per hectare of agricultural land. It has been increasing over the years owing to factors like the intensification of agriculture, increasing pest populations, and the need for higher yield and crop productivity to ensure global food security. According to the data provided by the Food and Agriculture Organization, 40% of global crop production is lost to pests annually, resulting in an average economic loss of around USD 70.0 billion.

- Europe witnessed higher insecticide applications compared to other regions of the world, with Germany having a higher per-hectare consumption of 3,028.0 g, which may be attributed to its highly intensive agricultural practices, with a significant focus on maximizing crop yields. Intensive agriculture often involves the use of higher inputs, including insecticides, to manage pests and ensure optimal crop production. Europe is followed by Asia-Pacific, with an average insecticide application of 975.1 g per hectare.

- Among the North American countries, the United States witnessed the largest consumption of insecticides per hectare, with 791.7 g in 2022, attributed to the large area under the cultivation of crops and increased exposure to insect pest infestations due to constantly changing climatic conditions.

- Changing climatic conditions due to global warming have created favorable conditions for certain pests, resulting in severe outbreaks. For instance, a locust outbreak in 2020 severely affected 23 countries, i.e., nine in East Africa, 11 in North Africa and the Middle East, and three in South Asia, causing an estimated loss of USD 8.5 billion. These circumstances necessitate farmers to use higher amounts of insecticides in agriculture.

Imidacloprid is the most affordable insecticide with a broad spectrum of activity

- Lambda-cyhalothrin belongs to the class of pyrethroid insecticides, which are synthetic chemicals modeled after natural pyrethrins found in chrysanthemum flowers. Lambda-cyhalothrin is used to control pests such as aphids, thrips, leafhoppers, whiteflies, and various caterpillar species in crops like cotton, corn, soybean, vegetables, and fruits. This active ingredient acts as a neurotoxin, targeting the nervous system of insects. It disrupts the normal functioning of nerve cells, leading to paralysis and, ultimately, the death of the pests. In 2022, it was priced at USD 22.7 thousand per metric ton.

- Cypermethrin is a non-synthetic pyrethroid used to control flea beetles, boxelder bugs, cockroaches, termites, ladybugs, scorpions, and yellow jackets. It was priced at USD 21.0 thousand in 2022. Brazil ranks among the top three importers of cypermethrin globally, with the European Union being a major exporter to Brazil under the EU-Mercosur deal.

- Emamectin benzoate is an insecticide belonging to the chemical class of avermectins. It kills the pests by targeting the nervous system. It binds to specific receptors in nerve cells, leading to paralysis and the eventual death of the pests. Emamectin benzoate is majorly used in European countries to control various insect pests in agriculture. It was priced at USD 17.3 thousand per metric ton.

- Imidacloprid is a neonicotinoid insecticide used to effectively manage various pests, including aphids, leafhoppers, whiteflies, thrips, and certain beetle species. This active ingredient was priced at USD 17.17 thousand per metric ton in 2022. Malathion is the most affordable chemical among the insecticides. It was valued at USD 12.5 thousand per metric ton in 2022.

Insecticide Industry Overview

The Insecticide Market is fragmented, with the top five companies occupying 33.15%. The major players in this market are ADAMA Agricultural Solutions Ltd., Bayer AG, Corteva Agriscience, FMC Corporation and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Australia

- 4.3.3 Brazil

- 4.3.4 Canada

- 4.3.5 Chile

- 4.3.6 China

- 4.3.7 France

- 4.3.8 Germany

- 4.3.9 India

- 4.3.10 Indonesia

- 4.3.11 Italy

- 4.3.12 Japan

- 4.3.13 Mexico

- 4.3.14 Myanmar

- 4.3.15 Netherlands

- 4.3.16 Pakistan

- 4.3.17 Philippines

- 4.3.18 Russia

- 4.3.19 South Africa

- 4.3.20 Spain

- 4.3.21 Thailand

- 4.3.22 Ukraine

- 4.3.23 United Kingdom

- 4.3.24 United States

- 4.3.25 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 By Country

- 5.3.1.1.1 South Africa

- 5.3.1.1.2 Rest of Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 By Country

- 5.3.2.1.1 Australia

- 5.3.2.1.2 China

- 5.3.2.1.3 India

- 5.3.2.1.4 Indonesia

- 5.3.2.1.5 Japan

- 5.3.2.1.6 Myanmar

- 5.3.2.1.7 Pakistan

- 5.3.2.1.8 Philippines

- 5.3.2.1.9 Thailand

- 5.3.2.1.10 Vietnam

- 5.3.2.1.11 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 By Country

- 5.3.3.1.1 France

- 5.3.3.1.2 Germany

- 5.3.3.1.3 Italy

- 5.3.3.1.4 Netherlands

- 5.3.3.1.5 Russia

- 5.3.3.1.6 Spain

- 5.3.3.1.7 Ukraine

- 5.3.3.1.8 United Kingdom

- 5.3.3.1.9 Rest of Europe

- 5.3.4 North America

- 5.3.4.1 By Country

- 5.3.4.1.1 Canada

- 5.3.4.1.2 Mexico

- 5.3.4.1.3 United States

- 5.3.4.1.4 Rest of North America

- 5.3.5 South America

- 5.3.5.1 By Country

- 5.3.5.1.1 Argentina

- 5.3.5.1.2 Brazil

- 5.3.5.1.3 Chile

- 5.3.5.1.4 Rest of South America

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd.

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Jiangsu Yangnong Chemical Co. Ltd

- 6.4.7 Nufarm Ltd

- 6.4.8 Sumitomo Chemical Co. Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

샘플 요청 목록