|

시장보고서

상품코드

1685828

기업 애플리케이션 통합 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Enterprise Application Integration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

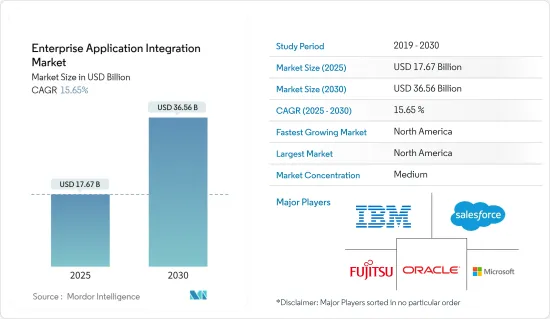

기업 애플리케이션 통합 시장 규모는 2025년에 176억 7,000만 달러에 달할 것으로 추정됩니다. 예측 기간 중(2025-2030년) CAGR은 15.65%를 나타낼 것으로 전망되고, 2030년에는 365억 6,000만 달러에 이를 것으로 예상됩니다.

디지털 변혁이 기업의 정세를 변화

디지털 전환은 모든 산업에 혁명을 가져옵니다. 비즈니스가 진화함에 따라 다양한 애플리케이션을 원활하게 통합할 필요성이 가장 중요해집니다. 기업 애플리케이션 통합(EAI) 솔루션은 이 혁신의 최전선에 있으며 조직이 비즈니스 애플리케이션과 관련된 데이터베이스 및 워크플로우를 통합할 수 있도록 합니다. EAI의 채택은 기업 소프트웨어의 생태계가 복잡해지고 있다는 배경입니다. Okta의 "Businesses at Work" 보고서에 따르면 대기업은 평균 187개의 애플리케이션을 도입했으며, 전 세계적으로 애플리케이션의 사용이 지속적으로 증가하고 있음을 보여줍니다. 이러한 추세는 강력한 기업 애플리케이션 통합 솔루션의 중요한 필요성을 강조합니다.

통합 과제 :

주요 하이라이트

- 다른 시스템 : 기업은 종종 호환되지 않는 프레임워크에서 운영되며 ERP, CRM 및 기타 중요한 시스템 간의 데이터 교환을 방해합니다.

- 자동화 장애물 : 통합되지 않으므로 단순 작업 자동화가 어려워 업무 효율성에 영향을 미칩니다.

- 재무 영향 : 클레오 보고서에 따르면 공급망 기업의 24%는 부적절한 소프트웨어 시스템 통합으로 연간 50만 달러 이상의 손실을 입고 있습니다.

EAI 솔루션

주요 하이라이트

- 미들웨어 인프라 : EAI는 이기종 애플리케이션과 레거시 디바이스 간의 개방형 데이터 공유를 위한 보안 플랫폼을 도입합니다.

- 통합된 접근법 : EAI 미들웨어 플랫폼은 애플리케이션 제약으로부터 데이터를 해제함으로써 데이터의 중앙 집중식 관리와 통합을 지원합니다.

- 운영 효율성 : 통합은 정보 공유를 간소화하여 클라우드 컴퓨팅, 빅 데이터 및 IoT 기술 간의 데이터 제어를 용이하게 합니다.

실시간 데이터 액세스 : 민첩한 기업의 핵심

기업이 민첩성과 업무 효율성을 추구함에 따라 실시간 데이터 액세스 및 관리에 대한 수요가 급증하고 있습니다. 실시간 통찰력은 정보 기반 의사 결정, 고객 경험 향상, 개인화 추진에 필수적입니다. 이러한 추세는 최신 데이터 저장소의 복잡성과 양을 수용할 수 있는 클라우드 기반 기업 통합 솔루션에 대한 투자를 촉진합니다.

시장 반응

주요 하이라이트

- 클라우드 연결 : Qlik은 Qlik-cloud 데이터 연결성을 발표했습니다. iPaaS(Integration Platform as a Service) 솔루션으로 기업의 모든 데이터 소스를 실시간으로 클라우드에 연결합니다.

- 온프레미스의 장점 : 온프레미스를 사용하면 데이터의 기밀성을 높이면서 실시간으로 비즈니스를 모니터링할 수 있습니다.

- 종합적인 솔루션 Persistent의 기업 통합 서비스는 소프트웨어 애플리케이션의 원활한 연동을 가능하게 하며 여러 채널에 걸쳐 데이터의 일관된 실시간 뷰를 제공합니다.

업계에 미치는 영향

주요 하이라이트

- 성능 최적화 : 실시간 데이터 통합을 통해 소프트웨어 정의 기업 전체의 비즈니스 성능을 즉시 파악할 수 있습니다.

- 협업 효율성 : EAI 도구와 기술은 실시간 통찰력을 제공하고 여러 애플리케이션 간의 협력과 정보 교환을 촉진하기 위해 진화하고 있습니다.

- 복잡성 관리 : 다양한 인프라 및 애플리케이션 문제를 보다 효율적으로 처리하는 단일 서비스가 등장합니다.

API 주도 통합 : 커넥티드 기업 추진

모바일 애플리케이션, IoT 디바이스, 웨어러블의 보급으로 API를 중심으로 한 통합의 필요성이 높아지고 있습니다. 실시간 API 기반 통합은 이동 중에 다양한 매개변수를 모니터링할 수 있는 애플리케이션을 생성할 수 있어 여러 플랫폼 간의 원활한 데이터 흐름과 동기화를 촉진합니다.

연결성 규모:

주요 하이라이트

- 장치 급증 : 시스코는 2030년까지 5,000억 대의 장치가 인터넷에 연결될 것으로 예상하고 있으며, 이 엄청난 생태계를 관리하는 데 EAI가 중요한 역할을 한다고 강조합니다.

- 데이터 동기화 : 실시간 애플리케이션 통합은 PC, 노트북, 핸드헬드 장치 간의 데이터 일관성을 보장합니다.

기업에 미치는 영향 :

주요 하이라이트

- 생태계 결합 : 디지털 변환이 진행됨에 따라 기업 소프트웨어 통합은 백엔드에서 생태계 전체를 묶는 중요한 역할로 전환하고 있습니다.

- 아키텍처 유연성 : EAI 솔루션은 클라우드 및 온프레미스 환경, 민첩한 전달 및 플러그 앤 플레이 아키텍처를 지원하도록 진화하고 있습니다.

업계 특유의 채용 경향 EAI 솔루션의 채용은 업계에 따라 다르며 IT 및 통신, 은행/금융서비스/보험(BFSI), 제조업이 선도하고 있습니다. 각 부문은 자신의 과제를 해결하고 새로운 기회를 활용하기 위해 EAI를 활용합니다.

IT 및 통신

주요 하이라이트

- 시장 리더십 : IT 및 통신 분야는 2027년까지 72억 8,000만 달러에 이를 것으로 추정되고, CAGR 17.64%로 성장할 것으로 예측됩니다.

- 텔레콤 통합 : 기업 소프트웨어 통합 프로젝트는 커뮤니케이션 비즈니스에서 커스텀 및 시장 애플리케이션 시스템을 통합하는 데 필수적이며 기술과 비즈니스 요구의 균형을 이룹니다.

BFSI 분야 :

주요 하이라이트

- 디지털 결제 : 디지털 결제의 상승으로 견고한 데이터 관리 시스템의 요구가 증가하고 EAI 시장 성장에 박차를 가하고 있습니다.

- 혁신적인 플랫폼 : BlocPal International Inc.의 독자적인 물리적, 가상 금융 서비스 플랫폼 개발은 이 분야의 통합 디지털 솔루션에 대한 노력의 예입니다.

제조업

지식 엔지니어링 : EAI는 분산된 자율 제조 시스템을 통합하고 가상 기업 및 대중화와 같은 패러다임을 지원하는 데 중요합니다.

주요 하이라이트

- 경쟁 : EAI를 통한 IT 및 지식 기반 엔지니어링의 효율적인 활용은 기업 시장 개척에 신속한 대응 능력을 향상시킵니다.

- 미래 전망 : 진화하는 통합 전망 : 기업 애플리케이션 통합의 미래는 복잡성이 증가하고 보다 정교하고 민첩한 솔루션이 필요함을 특징으로 합니다. 조직이 기술에 크게 의존하는 동안 다양한 애플리케이션을 통합하는 수요는 점점 더 강해질 것으로 보입니다.

새로운 동향 :

주요 하이라이트

- 통합 범위 확대 : 미래의 EAI 솔루션은 조직 내외의 엄청난 수의 엔드포인트를 고려해야 합니다.

- 급속한 혁신 : 통합 요건의 변경 빈도가 가속화되고 보다 유연하고 응답성이 높은 EAI 플랫폼이 필요합니다.

- 모바일 통합 : 통합 지출의 20%는 모바일 장치의 데이터 통합을 목표로 하고 있으며 간헐적인 연결 및 처리량 변화와 같은 문제를 해결해야 합니다.

전략적 과제

주요 하이라이트

- 안정성과 혁신성의 균형 : IT 리더는 중요한 시스템의 제어를 유지하는 한편, 이러한 시스템에 액세스하는 애플리케이션의 신속한 반복을 촉진해야 합니다.

- 프리페치 및 캐싱 : 모바일 애플리케이션은 연결성 문제를 보완하기 위해 고급 데이터 프리페치 및 캐싱 전략을 채택하는 경우가 늘고 있습니다.

- 지속적인 적응 : EAI 솔루션은 디지털 변환 이니셔티브의 특징인 신속한 혁신 속도를 지원하기 위해 진화해야 합니다.

기업 애플리케이션 통합 시장 동향

IT 및 통신 부문 : 최대 최종 사용자 부문

IT 및 통신 부문은 기업 애플리케이션 통합(EAI) 시장의 지배적인 세력으로 부상하고 있으며, CAGR 17.64%로 성장을 지속하여 2027년까지 72억 8,000만 달러에 달할 것으로 예측됩니다. 이러한 대폭적인 성장은 특히 클라우드 컴퓨팅 및 디지털 변환 분야에서 IT 및 통신 업계의 복잡한 통합 요구를 충족시키는 기업 소프트웨어 통합 솔루션의 중요한 역할을 뒷받침합니다.

클라우드 마이그레이션이 통합 수요 견인

- 데이터 및 인프라 마이그레이션 : 은행 및 통신 사업자의 데이터, 프로세스 및 인프라 클라우드로의 전환이 진행되고 있는 것이 EAI 도입의 중요한 추진력이 되고 있습니다.

- 원활한 운영 : 이 시프트는 다양한 시스템과 애플리케이션의 원활한 운영을 보장하기 위해 견고한 통합 기능을 필요로 합니다.

- 클라우드 기반의 중요성 : 기업은 운영의 확장성을 높이기 위해 기존 서비스로서의 통합 플랫폼(iPaaS) 모델보다 서비스로서의 데이터 플랫폼(dPaaS)을 선호하는 경향이 커지고 있습니다.

통신 사업자의 핵심 프로세스 통합

- 통합의 복잡성 : 통신 사업자는 핵심 프로세스를 지원하기 위해 대규모 EAI 프로젝트를 수행하고 있으며 사용자 정의 시스템과 시장 애플리케이션 시스템을 통합하기 위한 미들웨어 인프라를 구축하고 있습니다.

- 국가를 넘어서는 통합 : 통신 사업자는 국제적인 자회사 간에 기술적인 해결책을 일치시키는 독특한 문제에 직면하고 종합적인 통합 플랫폼의 중요성을 강조합니다.

실시간 통합과 IoT의 융합 :

- API 중심 솔루션 : 모바일 애플리케이션, IoT, 웨어러블 융합으로 실시간으로 API 중심의 통합 솔루션에 대한 수요가 증가하고 있습니다.

- 디바이스 급증 : 2030년까지 5,000억 대의 디바이스가 연결될 것으로 예상되며, 이러한 생태계 전체의 데이터 흐름을 관리하는 견고한 통합 솔루션의 필요성이 강조되고 있습니다.

협업 소프트웨어 솔루션이 통합 요구를 촉진

- 가상 협업 급증 : Microsoft Teams 및 Zoom과 같은 가상 회의 및 협업 도구의 등장으로 통합 기업 솔루션 수요를 간접적으로 밀어 올리고 있습니다.

- 시스템 상호 운용성 : 기업은 협업 소프트웨어를 기존 시스템과 통합하는 솔루션을 찾고 있으며 EAI의 요구를 더욱 강화하고 있습니다.

북미 : 급성장하는 지역 부문

북미는 기업 애플리케이션 통합(EAI) 시장에서 가장 급성장하고 있는 지역 부문으로 눈에 띄고 있으며, 2027년까지 142억 6,000만 달러에 달할 것으로 추정되고, CAGR 16.41%를 나타낼 것으로 예측되고 있습니다. 이 지역은 디지털 전환의 리더십과 클라우드 기반 기업 통합 솔루션의 광범위한 채택으로 급성장 궤도를 돋보이게 합니다.

애플리케이션 통합의 보급 :

- 높은 도입률 : 미국 기업의 93% 이상이 비즈니스 애플리케이션을 사용하고 있으며 기업용 소프트웨어 통합 제공업체에게 있어 좋은 곳입니다.

- 비즈니스 효율성 : 기업이 더 많은 애플리케이션을 도입함에 따라 비즈니스 효율성을 높이는 원활한 통합 솔루션에 대한 수요가 계속 증가하고 있습니다.

전략적 제휴와 혁신적인 솔루션 :

- 혁신을 추진하는 파트너십 : HiQ의 European Cloud City Network와의 파트너십과 Frends iPaaS 플랫폼과 같은 전략적 제휴는 하이브리드 클라우드 통합 전략의 혁신을 추진하고 있습니다.

- 규정 준수 : 이러한 파트너십은 공공 부문 및 상업 부문의 비즈니스에 중요한 데이터 법률 및 규정에 대한 완전한 규정 준수를 보장하는 솔루션을 제공하는 데 중점을 둡니다.

클라우드 통합 및 디지털 변환

- 기술적 파괴 : IoT, 클라우드 컴퓨팅, 디지털 전환 이니셔티브의 채택이 증가하고 있으며, 북미의 다양한 업계에서 EAI 솔루션에 대한 수요가 증가하고 있습니다.

- 벤더 포커스 : IBM과 후지쯔 등 이 지역의 주요 기업은 SaaS 기반 보안 솔루션과 같은 혁신으로 시장을 선도하고 있으며 시장 성장을 이끌고 있습니다.

- 통합 시장 : 북미의 EAI 시장은 적당히 통합되어 있으며, 세계 기업은 경쟁력을 유지하기 위해 최첨단 기술에 주력하고 있습니다.

- 제로 트러스트 아키텍처 : 보안을 위한 제로 트러스트 아키텍처 구축과 같은 혁신은 기업 환경에서 EAI 솔루션을 배포하는 데 중요해지고 있습니다.

기업 애플리케이션 통합 업계 개요

세계 기업이 반통합 시장을 독점

기업 애플리케이션 통합(EAI) 시장은 IBM Corporation, 후지쯔 주식회사, 마이크로소프트 등 세계 기업들이 큰 시장 점유율을 차지하는 반연결 구조를 특징으로 합니다. 이러한 기술 융합은 광범위한 자원, 세계적인 존재, 기술적 전문 지식을 활용하여 시장을 독점하는 반면, 소규모의 혁신적인 기업은 전문적인 솔루션에서 틈새 역할을 개척하고 있습니다.

종합적인 서비스

엔드 투 엔드 솔루션 : 세계 리더는 업계에 관계없이 다양한 조직의 요구를 충족시키는 종합적인 기업 애플리케이션 통합 솔루션을 제공합니다.

파트너십 생태계 : IBM 및 Microsoft와 같은 기업은 파트너와의 광범위한 생태계를 구축하여 광범위한 비즈니스 애플리케이션 및 데이터 소스에 대한 통합을 제공할 수 있습니다.

R&D 포커스 :

신흥기술 : 주요 기업은 연구개발에 많은 투자를 하고, 인공지능(AI), 머신러닝, 클라우드 컴퓨팅의 혁신에 주력하고 EAI 플랫폼을 진화시키고 있습니다.

하이브리드 환경 지원 : 통합 솔루션은 하이브리드 클라우드 통합 전략을 지원하도록 설계되었으며 온프레미스와 클라우드 기반 인프라 간의 원활한 마이그레이션을 보장합니다.

혁신과 적응성 :

클라우드 네이티브 아키텍처 : 확장 가능하고 유연한 솔루션에 대한 수요가 증가함에 따라 클라우드 네이티브 아키텍처로의 전환이 진행되고 있습니다.

로우코드/노코드 툴 : 로우코드/노코드 툴의 도입으로 통합 기능의 범위가 확대되어 기술자가 아닌 사용자도 데이터 통합 서비스에 공헌할 수 있게 되었습니다.

보안 및 규정 준수 :

데이터 프라이버시에 대한 우려 : 기업이 데이터 프라이버시에 대한 우려를 높이고 있는 동안 EAI 공급업체와 공급업체는 경쟁력을 높이기 위해 솔루션의 보안, 컴플라이언스 및 거버넌스 기능을 강조합니다.

API 관리 : EAI를 위한 견고한 API 관리는 기업이 엄청난 수의 애플리케이션과 엔드포인트를 안전하게 통합할 수 있게 하여 중요한 차별화 요인이 되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업 밸류체인 분석

- 업계의 매력도 - Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 강도

- 기술 스냅샷

제5장 시장 역학

- 시장 성장 촉진요인

- 기업 정세를 바꾸는 디지털 전환

- 실시간 데이터 액세스 및 관리에 대한 수요 증가

- 커넥티드 기업를 지원하는 API 주도의 통합

- 시장의 과제

- 오픈소스 소프트웨어의 가용성

- 통합 부족으로 단순 작업 자동화가 어려워지고 비즈니스 효율성 지장

- COVID-19가 업계에 미치는 영향 평가

제6장 시장 세분화

- 배포 유형

- 온프레미스

- 클라우드

- 하이브리드

- 조직 규모

- 대기업

- 중소기업

- 최종 사용자 업계

- BFSI

- IT 및 통신

- 헬스케어

- 소매

- 정부기관

- 제조업

- 기타 최종 사용자 산업

- 지역

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

제7장 경쟁 구도

- 기업 프로파일

- IBM Corporation

- Fujitsu Limited

- Microsoft Corporation

- MuleSoft LLC(Salesforce Inc.)

- Oracle Corporation

- SAP SE

- Software AG

- Tibco Software Inc.

- iTransition Group

제8장 투자 분석

제9장 시장의 미래

KTH 25.04.02The Enterprise Application Integration Market size is estimated at USD 17.67 billion in 2025, and is expected to reach USD 36.56 billion by 2030, at a CAGR of 15.65% during the forecast period (2025-2030).

Digital Transformation Reshaping Enterprise Landscapes

Digital transformation is revolutionizing industries across the board. As businesses evolve, the need for seamless integration of diverse applications becomes paramount. Enterprise Application Integration (EAI) solutions are at the forefront of this transformation, enabling organizations to unify databases and workflows associated with business applications. The adoption of EAI is driven by the increasing complexity of enterprise software ecosystems. According to Okta's "Businesses at Work" report, large organizations deploy an average of 187 applications, showcasing a consistent rise in application utilization globally. This trend underscores the critical need for robust enterprise application integration solutions.

Integration Challenges:

Key Highlights

- Disparate Systems: Businesses often operate with incompatible frameworks, hindering data exchange between ERP, CRM, and other critical systems.

- Automation Hurdles: The lack of integration makes automating simple tasks challenging, impacting operational efficiency.

- Financial Impact: Cleo's report reveals that 24% of supply chain companies lose over USD 500,000 annually due to inadequate software system integrations.

EAI Solutions:

Key Highlights

- Middleware Infrastructure: EAI introduces a secure platform for open data sharing between heterogeneous applications and legacy devices.

- Unified Approach: By removing data from application restrictions, EAI middleware platforms aid in centralized data management and integration.

- Operational Efficiency: Integration streamlines information sharing and provides ease in controlling data across cloud computing, Big Data, and IoT technologies.

Real-time Data Access: The Cornerstone of Agile Enterprises

The demand for real-time data access and management is surging as businesses strive for agility and operational efficiency. Real-time insights are crucial for making informed decisions, improving customer experiences, and driving personalization efforts. This trend is propelling investments in cloud-based enterprise integration solutions that can handle the complexity and volume of modern data repositories.

Market Response:

Key Highlights

- Cloud Connectivity: Qlik introduced Qlik-cloud data connectivity, an Integration Platform as a Service (iPaaS) solution, linking all enterprise data sources to the cloud in real-time.

- On-premise Advantages: On-premise implementations offer real-time monitoring of business operations with enhanced data confidentiality.

- Comprehensive Solutions: Persistent's Enterprise Integration Services enable seamless interfacing of software applications, providing a consistent, real-time view of data across multiple channels.

Industry Impact:

Key Highlights

- Performance Optimization: Real-time data integration allows for immediate insights into total business performance across software-defined enterprises.

- Collaborative Efficiency: EAI tools and technologies are evolving to deliver real-time insights, fostering successful cooperation and information exchange across multiple applications.

- Managed Complexity: Single services are emerging to handle issues across a diverse range of infrastructure and applications more effectively.

API-Driven Integration: Powering the Connected Enterprise

The proliferation of mobile applications, IoT devices, and wearables is driving the need for API-centric integration. Real-time, API-driven integration enables the creation of applications that can monitor various parameters on the go, facilitating seamless data flow and synchronization across multiple platforms.

Connectivity Scale:

Key Highlights

- Device Proliferation: Cisco projects that 500 billion devices will be connected to the Internet by 2030, emphasizing the critical role of EAI in managing this vast ecosystem.

- Data Synchronization: Real-time application integration ensures data consistency across PCs, laptops, and handheld devices

Enterprise Impact:

Key Highlights

- Ecosystem Binding: As digital transformation advances, enterprise software integration is shifting from back-end to a critical role in binding the entire ecosystem.

- Architectural Flexibility: EAI solutions are evolving to support cloud and on-premise environments, agile delivery, and plug-and-play architectures.

Industry-Specific Adoption TrendsThe adoption of EAI solutions varies across industries, with IT and telecom, BFSI, and manufacturing sectors leading the charge. Each sector leverages EAI to address unique challenges and capitalize on emerging opportunities.

IT and Telecom:

Key Highlights

- Market Leadership: The IT and telecom segment is projected to reach USD 7.28 billion by 2027, growing at a CAGR of 17.64%.

- Telecom Integration: Enterprise software integration projects are crucial for integrating custom and market application systems in telecom operations, balancing technology with business imperatives.

BFSI Sector:

Key Highlights

- Digital Payments: The rise of digital payment methods is driving the need for robust data management systems, fueling EAI market growth.

- Innovative Platforms: BlocPal International Inc.'s development of a unique physical and virtual financial services platform exemplifies the sector's push towards integrated digital solutions.

Manufacturing:

Knowledge Engineering: EAI is critical in integrating dispersed and autonomous manufacturing systems, supporting paradigms like virtual enterprise and mass customization.

Key Highlights

- Competitiveness: Efficient application of IT and knowledge-based engineering through EAI enhances firms' ability to respond swiftly to market developments.

- Future Outlook: Evolving Integration Landscape : The future of Enterprise Application Integration is characterized by increasing complexity and the need for more sophisticated, agile solutions. As organizations continue to rely heavily on technology, the demand for integrating diverse applications will only intensify

Emerging Trends:

Key Highlights

- Expanded Integration Scope: Future EAI solutions will need to consider a vastly larger collection of endpoints both inside and outside the organization.

- Rapid Innovation: The frequency of changes in integration requirements is accelerating, necessitating more flexible and responsive EAI platforms.

- Mobile Integration: It's projected that 20% of integration spending will be directed towards integrating data on mobile devices, addressing challenges like intermittent connectivity and variable throughput

Strategic Imperatives:

Key Highlights

- Balancing Stability and Innovation: IT leaders must maintain control over critical systems while fostering rapid iteration of applications accessing those systems.

- Prefetching and Caching: Mobile apps are increasingly employing sophisticated data prefetching and caching strategies to compensate for connectivity issues.

- Continuous Adaptation: EAI solutions must evolve to support the rapid pace of innovation that distinguishes digital transformation initiatives.

Enterprise Application Integration Market Trends

IT and Telecom Segment: Largest End-User Segment

The IT and Telecom segment emerges as the dominant force in the Enterprise Application Integration (EAI) market, projected to reach USD 7.28 billion by 2027 with a CAGR of 17.64%. The substantial growth underscores the critical role of enterprise software integration solutions in addressing the complex integration needs of the IT and Telecom industries, particularly in the realm of cloud computing and digital transformation.

Cloud Migration Drives Integration Demand:

- Data and Infrastructure Migration: The increasing migration of data, processes, and infrastructure to the cloud by banks and telecom operators is a significant driver for EAI adoption.

- Operational Seamlessness: This shift necessitates robust integration capabilities to ensure seamless operation across diverse systems and applications.

- Cloud-based Focus: Businesses are increasingly prioritizing data platform as a service (dPaaS) over traditional integration platform as a service (iPaaS) models to enhance operational scalability.

Telecom Operators' Core Process Integration:

- Complexity of Integration: Telecom operators are undertaking extensive EAI projects to support core processes, creating middleware infrastructures to integrate custom and market application systems.

- Cross-National Integration: Telecom companies face unique challenges in aligning technical solutions across international subsidiaries, emphasizing the importance of comprehensive integration platforms.

Real-Time Integration and IoT Convergence:

- API-Centric Solutions: The convergence of mobile applications, IoT, and wearables is driving the demand for real-time, API-driven integration solutions.

- Proliferation of Devices: By 2030, projections of 500 billion connected devices emphasize the need for robust integration solutions to manage the data flow across these ecosystems.

Collaborative Software Solutions Drive Integration Needs:

- Virtual Collaboration Surge: The rise of virtual meeting and collaboration tools, such as Microsoft Teams and Zoom, has indirectly boosted demand for integrated enterprise solutions.

- System Interoperability: Businesses are seeking solutions that integrate collaborative software with existing systems, further driving the need for EAI.

North America: Fastest-Growing Regional Segment

North America stands out as the fastest-growing regional segment in the Enterprise Application Integration (EAI) market, projected to reach USD 14.26 billion by 2027, registering a CAGR of 16.41%. The region's leadership in digital transformation and the widespread adoption of cloud-based enterprise integration solutions highlight its rapid growth trajectory.

Widespread Application Integration:

- High Adoption Rate: Over 93% of U.S. businesses utilize business applications, creating fertile ground for enterprise software integration providers.

- Operational Efficiency: As companies adopt more applications, the demand for seamless integration solutions that enhance operational efficiency continues to grow.

Strategic Alliances and Innovative Solutions:

- Partnerships Driving Innovation: Strategic collaborations, such as HiQ's alliance with the European Cloud City Network and the Frends iPaaS platform, are driving innovation in hybrid cloud integration strategies.

- Regulatory Compliance: These partnerships focus on offering solutions that ensure full compliance with data laws and regulations, critical for public and commercial sector businesses.

Cloud Integration and Digital Transformation:

- Technological Disruptions: The increasing adoption of IoT, cloud computing, and digital transformation initiatives is propelling the demand for EAI solutions across various industries in North America.

- Vendor Focus: Key players in the region, such as IBM and Fujitsu, are leading with innovations like SaaS-based security solutions, driving market growth.

- Consolidated Market: The North American EAI market is moderately consolidated, with global players focusing on cutting-edge technologies to maintain their competitive edge.

- Zero-Trust Architecture: Innovations such as the introduction of zero-trust architecture for security are becoming critical in the deployment of EAI solutions in enterprise environments.

Enterprise Application Integration Industry Overview

Global Players Dominate Semi Consolidated Market

The Enterprise Application Integration (EAI) market is characterized by a semi consolidated structure, with global players such as IBM Corporation, Fujitsu Ltd, and Microsoft holding significant market share. These technology conglomerates leverage their extensive resources, global presence, and technological expertise to dominate the market while smaller, innovative companies carve out niche roles with specialized solutions.

Comprehensive Offerings:

End-to-End Solutions: Global leaders offer comprehensive enterprise application integration solutions that cater to the diverse needs of organizations across industries.

Partnership Ecosystems: Companies like IBM and Microsoft have built extensive ecosystems of partners, enabling them to provide integration across a wide range of business applications and data sources.

Research and Development Focus:

Emerging Technologies: Key players invest heavily in R&D, focusing on innovations in artificial intelligence (AI), machine learning, and cloud computing to advance their EAI platforms.

Support for Hybrid Environments: Their integration solutions are designed to support hybrid cloud integration strategies, ensuring smooth transitions between on-premise and cloud-based infrastructures.

Innovation and Adaptability:

Cloud-Native Architectures: Market players are increasingly shifting towards cloud-native architectures to meet the growing demand for scalable, flexible solutions.

Low-Code/No-Code Tools: The introduction of low-code/no-code tools is expanding the reach of integration capabilities, allowing non-technical users to contribute to data integration services.

Security and Compliance:

Data Privacy Concerns: As enterprises grapple with growing data privacy concerns, EAI vendors and providers are emphasizing security, compliance, and governance features in their solutions to gain a competitive edge.

API Management: Robust API management for EAI is becoming a critical differentiator, allowing organizations to securely integrate a vast number of applications and endpoints.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitutes

- 4.3.5 Degree of Competition

- 4.4 Technology Snapshot

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Digital Transformation Reshaping Enterprise Landscapes

- 5.1.2 Increasing Demand for Real-time Data Access and Management

- 5.1.3 API-Driven Integration Powering the Connected Enterprise

- 5.2 Market Challenges

- 5.2.1 Availability of Open Source Software

- 5.2.2 The lack of integration makes automating simple tasks challenging, impacting operational efficiency.

- 5.3 Assessment of Impact of COVID-19 on the Industry

6 MARKET SEGMENTATION

- 6.1 Deployment Type

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.1.3 Hybrid

- 6.2 Organisation Size

- 6.2.1 Large Enterprises

- 6.2.2 Small and Medium-sized Enterprises

- 6.3 End-user Industry

- 6.3.1 BFSI

- 6.3.2 IT and Telecom

- 6.3.3 Healthcare

- 6.3.4 Retail

- 6.3.5 Government

- 6.3.6 Manufacturing

- 6.3.7 Other End-user Industries

- 6.4 Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Fujitsu Limited

- 7.1.3 Microsoft Corporation

- 7.1.4 MuleSoft LLC (Salesforce Inc.)

- 7.1.5 Oracle Corporation

- 7.1.6 SAP SE

- 7.1.7 Software AG

- 7.1.8 Tibco Software Inc.

- 7.1.9 iTransition Group