|

시장보고서

상품코드

1685930

집광형 태양열발전(CSP) - 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Concentrated Solar Power (CSP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

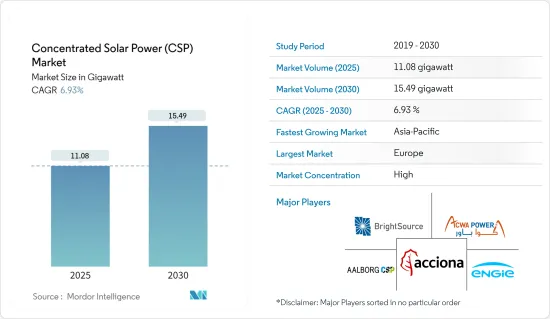

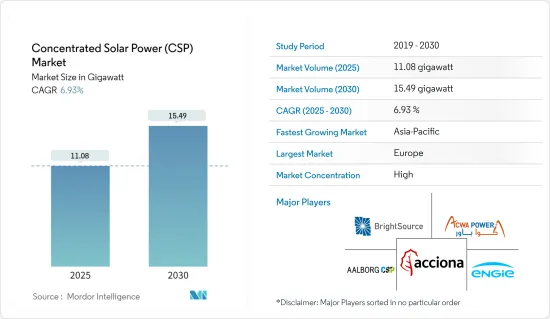

집광형 태양열발전(CSP) 시장 규모는 2025년 11.08기가와트, 2030년에는 15.49기가와트에 달할 것으로 예측됩니다. 예측기간(2025년-2030년) CAGR은 6.93%를 나타낼 전망입니다.

주요 하이라이트

- 장기적으로는 집광형 태양광 발전 기술의 비용 절감이 시장을 견인할 것으로 예상됩니다.

- 한편, 태양광 발전 및 기타 재생 가능 기술의 채용이 증가하고 있는 것이 예측 기간 동안 시장 성장을 방해할 것으로 예상됩니다.

- 그럼에도 불구하고 기술 개선과 하이브리드 발전소에 집광형 태양광 발전의 통합은 환경에 긍정적인 영향을 미칩니다. 이는 환경에 긍정적인 영향을 미치며 기후 변화는 미래에 집광형 태양광 시장에 몇 가지 기회를 만들 것으로 예상됩니다.

- 이 지역의 태양전지 섹터에서는 전력 수요가 증가함에 따라 신규 프로젝트가 일어나 오염 수준을 억제하기 위해 재생 가능 에너지원의 이용에 주력하고 있기 때문에 예측 기간 동안 CSP 수요가 증가하게 되어 유럽이 시장을 독점할 것으로 예상됩니다.

집광형 태양열발전(CSP) 시장 동향

파라볼릭 트로프형이 시장을 독점

- 파라볼릭 트로프형 집광장치(PTC)는 직선축 추적식의 긴 U자형 미러로 구성되어 있습니다. 거울은 초점선을 따라 직사광선을 반사하고 거기에 흡수관이 배치됩니다. 리시버, 업소버 튜브는 스틸제입니다. 태양 스펙트럼의 파장 영역에서는 높은 흡광도를 유지하고 적외선 스펙트럼의 파장 영역에서는 높은 반사율을 유지하는(즉 가능한 한 방출하지 않는다.) 선택 코팅이 실시되어 있습니다.

- 가장 일반적으로 사용되는 유체는 열 오일이지만 물, 증기 및 용융 염도이 구성에 사용됩니다. 이들은 CSP로 가장 널리 도입되는 구성입니다.

- 파라볼라 트로프형 집열기는 세계에서 가장 일반적으로 도입되고 있는 CSP의 하나이며, 가정용 난방, 해수 담수화, 냉동 시스템, 산업용 열, 발전소, 관개용수의 양수 등에 도입되고 있습니다. 미국 국립재생가능에너지연구소(NREL)에 따르면 2022년 6월 현재 파라볼릭 트로프는 세계 CSP 설비 용량의 63.5%를 차지하고 있습니다.

- 파라볼릭 트로프 컬렉터(PTC)의 운전 및 보수 부분은 동종의 것에 비해 약간 복잡합니다. 태양전지의 운영과 유지 보수에 관한 가장 빈번한 활동은 거울의 반사율을 정기적으로 측정하고 세척하는 것입니다. 거울의 반사율은 태양열 수집기가 공급하는 귀중한 열 에너지의 양에 직접 영향을 미칩니다. 또한 정기적인 청소 및 유지 보수를 위해서는 키가 큰 자동차와 크레인이 필요할 수 있습니다.

- 예를 들어 2020년 인도 공과대학 마드라스의 연구자들은 해수 담수화, 공간 난방, 공간 냉방 등 산업용 태양에너지를 집광하기 위한 저비용 태양광 파라볼라토르 트로프 컬렉터(PTC) 장치를 개발했습니다. 인도에서 개발된 이 시스템은 가볍고 다양한 기후와 부하 상황에서 높은 효율을 발휘합니다.

- 따라서 예측 기간 동안 파라볼라 트로프가 집광형 태양열 발전 시장을 독점할 것으로 예상됩니다.

시장을 독점하는 유럽

- 유럽에서는 전력부문이 온실가스 배출량의 75% 이상을 차지하고 있습니다.

- 솔라 부문은 전력 수요가 증가함에 따라 신규 프로젝트를 시작하여 지역 전체의 오염 수준을 억제하기 위해 재생 가능 에너지원의 이용에 주력하고 있습니다.

- 유럽에서는 MUSTEC(태양열 발전 시장 도입)과 같은 에너지 협력이 EU의 2030년 기후 에너지 틀을 근거로 하여 이 지역에서의 CSP 프로젝트의 공동 개척에 중점을 두고자 하고 있습니다.

- 마찬가지로 CSP 및 태양열 에너지를 위한 유럽 연구 기반인 EU Solaris ERIC은 CSP의 연구 관련 활동과 응용 개발을 목적으로 하고 있습니다.

- 게다가 2022년, 독일 정부는 산업용도의 그린 난방에의 클린 에너지 전환을 가속시키기 위해, CSP 설치에 55%의 보조금을 도입했습니다.또, CSP 기술의 투자 회수 기간을 3년 이하로 인하하는 것도 상정하고 있습니다.

- 마찬가지로 스페인은 2002년에 유럽에서 처음으로 CSP의 고정가격 임베디드제도를 도입하여 CSP의 도입 확대에 공헌했습니다.

- 게다가 2022년, 스페인의 에코로지 이행성은 동국에 있어서의 CSP 프로젝트의 개발에 연결되는 경매 메커니즘을 통해, CSP 설치 용량 220MW를 획득했습니다.

- 따라서 설치 용량이 증가함에 따라 예측 기간 동안 유럽이 CSP 시장을 독점할 것으로 예상됩니다.

집광형 태양열발전(CSP) 산업 개요

집광형 태양열발전(CSP) 시장은 적당히 통합되어 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 조사의 전제

제2장 조사 방법

제3장 주요 요약

제4장 시장 개요

- 소개

- 2028년까지 시장 규모와 수요 예측

- 2028년까지의 CSP 설치 용량과 예측

- 최근 동향과 개발

- 정부의 규제와 정책

- 시장 역학

- 성장 촉진요인

- 집광형 태양열 발전 기술의 비용 저하

- 억제요인

- 기타 신재생에너지원에 대한 정부의 지원정책

- 성장 촉진요인

- 공급망 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 세분화

- 기술분야

- 파라볼라 트로프

- 리니어 프레넬

- 파워 타워

- 접시, 스털링

- 열매체

- 용융염

- 수성

- 유성

- 기타 열매체

- 지역

- 북미

- 미국

- 멕시코

- 기타 북미

- 유럽

- 독일

- 이탈리아

- 프랑스

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 한국

- 기타 아시아태평양

- 남미

- 브라질

- 칠레

- 기타 남미

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 프로파일

- Nextera Energy Inc.

- Acciona SA

- ACWA Power

- Brightsource Energy Inc.

- Engie

- SR Energy

- Aalborg CSP

- Chiyoda Corporation

제7장 시장 기회와 앞으로의 동향

- 기술의 향상과 하이브리드 발전소에 있어서의 집광형 태양열발전(CSP)의 통합

The Concentrated Solar Power Market size is estimated at 11.08 gigawatt in 2025, and is expected to reach 15.49 gigawatt by 2030, at a CAGR of 6.93% during the forecast period (2025-2030).

Key Highlights

- Over the long term, the declining cost of concentrated solar power technologies is expected to drive the market.

- On the other hand, the increasing adoption of solar photovoltaics and other renewable technologies is expected to hinder the market growth during the forecast period.

- Nevertheless, technology improvements and integration of concentrated solar power in hybrid power plants. This will positively impact the environment, and climate change is expected to create several opportunities for Concentrating the solar power market in the future.

- Europe is expected to dominate the market as the solar sector in the region is witnessing new projects at the outset of growing electricity demand and focusing on using renewable energy sources to curb pollution levels, therefore resulting in increasing demand for CSP during the forecast period.

Concentrated Solar Power (CSP) Market Trends

Parabolic Trough Segment to Dominate the Market

- Parabolic-trough collectors (PTCs) consist of long U-shaped mirrors with a linear axis tracking system. The mirrors reflect direct solar radiation along their focal line, where an absorber tube is located. The receiver/absorber tube is made of steel. It has a selective coating that maintains high absorbance in the solar spectrum wavelength range but high reflectance in the infrared spectrum (i.e., it emits as little as possible).

- The most commonly used fluid is thermal oil, although water/steam or molten salt are also used for this configuration. These are some of the most widely deployed configurations for CSPs.

- Parabolic trough collectors are one of the most commonly deployed CSPs around the globe; they can be deployed in domestic heating, desalination, refrigeration systems, industrial heat, power plants, pumping irrigation water, etc. According to the National Renewable Energy Laboratory (NREL), as of June 2022, Parabolic trough accounts for a share of 63.5% of total global CSP installed capacity.

- The Parabolic Trough Collector (PTC) 's operations and maintenance part is slightly complicated compared to its counterparts. The most frequent activities related to solar field operations and maintenance are the periodic measurement of mirror reflectivity and washing. Mirror reflectivity directly affects the amount of valuable thermal energy solar collectors deliver. It may also require tall vehicles or cranes to perform routine cleaning and maintenance.

- For instance, in 2020, researchers from the Indian Institute of Technology Madras created a low-cost Solar Parabolic Trough Collector (PTC) device for concentrating solar energy for industrial uses such as desalination, space heating, and space cooling. This system, created and developed in India, is lightweight and highly efficient under various climate and load circumstances.

- Hence, the parabolic trough is expected to dominate the market for concentrated solar power during the forecast period.

Europe to Dominate the Market

- In Europe, the power sector accounts for more than 75% of greenhouse gas emissions in the region. Increasing the share of renewable energy has become a potential option for the region to tackle climate change.

- The solar sector is witnessing new projects at the outset of growing electricity demand and focusing on using renewable energy sources to curb pollution levels across the region. In 2022, Europe had about 2.3 GW of installed CSP capacity. As per IRENA, by 2030, Europe will likely install 4 GW of concentrated solar power (CSP)

- In Europe, Energy cooperation such as MUSTEC or Market Uptake of Solar Thermal Electricity intends to focus on the collaborative development of CSP projects in the region, given the EU 2030 climate and energy framework. MUSTEC aims to deploy CSP projects in Southern Europe to meet the electricity demand of Central and North European countries.

- Likewise, the EU Solaris ERIC, the European Research Infrastructure for CSP/Solar thermal energy, aims to develop CSP research-related activities and applications. The development of tools and techniques, new capacities, solutions, everyday standards, and protocols to ramp up CSP technology in the region.

- Further, in 2022, the German government introduced a 55% subsidy to install CSP to speed up the clean energy transition to green heating for industrial applications. It also envisages lowering payback time to below three years for CSP technology. This would significantly help CSP installations to increase in Germany.

- Similarly, Spain was the first European country to initiate feed-in-tariff mechanisms for CSP in 2002, which helped ramp up CSP deployment. Moreover, in 2007, Spain commissioned the PS10 solar power tower as the first commercial CSP plant to use tower technology worldwide.

- Further, in 2022, the Ministry of Ecological Transition, Spain, awarded 220 MW capacity for CSP installation through an auction mechanism that would give rise to the development of CSP projects in the country. Spain's government also announced to float tenders for 600 MW of CSP capacity by 2025.

- Hence, with the increasing installed capacities, Europe is expected to dominate the CSP market during the forecast period.

Concentrated Solar Power (CSP) Industry Overview

The concentrated solar power (CSP) market is moderately consolidated. Some of the key players in this market (in no particular order) include Aalborg CSP, Acciona SA, ACWA Power, Brightsource Energy Inc., and Engie SA., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2028

- 4.3 Installed CSP Capacity and Forecast in MW, till 2028

- 4.4 Recent Trends and Developments

- 4.5 Government Policies and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.1.1 Declining Cost of Concentrated Solar Power Technologies

- 4.6.2 Restraints

- 4.6.2.1 Supportive Government Policies for Other Renewable Energy Sources

- 4.6.1 Drivers

- 4.7 Supply Chain Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Parabolic Trough

- 5.1.2 Linear Fresnel

- 5.1.3 Power Tower

- 5.1.4 Dish/Stirling

- 5.2 Heat Transfer Fluid

- 5.2.1 Molten Salt

- 5.2.2 Water-based

- 5.2.3 Oil-based

- 5.2.4 Other Heat Transfer Fluids

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Mexico

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 Italy

- 5.3.2.3 France

- 5.3.2.4 Spain

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 South Korea

- 5.3.3.4 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Chile

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Nextera Energy Inc.

- 6.3.2 Acciona SA

- 6.3.3 ACWA Power

- 6.3.4 Brightsource Energy Inc.

- 6.3.5 Engie

- 6.3.6 SR Energy

- 6.3.7 Aalborg CSP

- 6.3.8 Chiyoda Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technology Improvements and Integration of Concentrated Solar Power in Hybrid Power Plants