|

시장보고서

상품코드

1685941

스칸듐 : 시장 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)Scandium - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

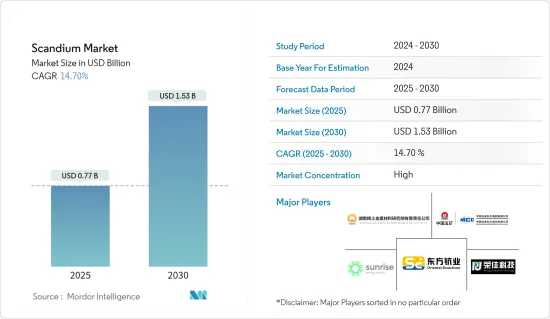

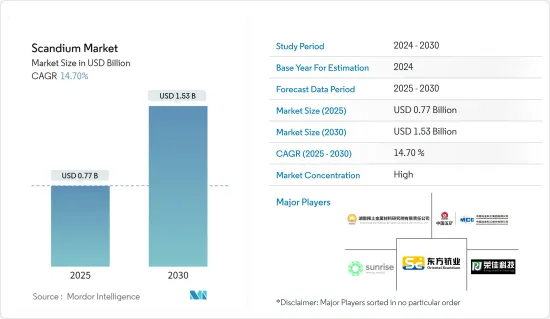

스칸듐 시장 규모는 2025년에 7억 7,000만 달러로 추계되고, 2030년에는 15억 3,000만 달러에 달할 것으로 예측되며, 예측 기간(2025-2030년)의 CAGR은 14.7%를 나타낼 전망입니다.

주요 하이라이트

- COVID-19 팬데믹은 스칸듐 시장에 부정적인 영향을 주었습니다.

- 단기적으로는 고체 산화물 연료전지(SOFCS)의 사용 증가와 항공 우주 및 방위 산업에서 알루미늄-스칸듐 합금에 대한 수요 증가가 연구 된 시장을 주도하는 요인입니다.

- 그러나 높은 스칸듐 가격은 2024년에서 2029년 사이에 연구 대상 시장의 성장을 저해할 수 있습니다.

- 자동차 산업에서의 잠재적 응용과 에너지 저장 기술의 성장은 향후 몇 년 동안 시장 기회를 제공 할 가능성이 높습니다.

- 중국이 시장을 독점하고 유럽연합이 2024년부터 2029년에 걸쳐 가장 높은 CAGR을 나타낼 것으로 예상됩니다.

스칸듐 시장 동향

고체 산화물 연료전지(SOFC) 부문이 시장을 지배할 전망

- SOFC는 전해질이라고 하는 고체 산화물 물질을 사용하여 음이온을 음극에서 양극으로 이동시키는 데 도움을 줍니다. 이 셀에서 양극과 음극은 전해질을 덮는 특수 잉크로 만들어집니다.

- 전해질 재료는 천연 가스를 에너지로 전환하는 촉매 역할을 하기 위해 고온에 노출됩니다.

- 고체 전해질에 스칸듐을 사용하면 기존 SOFC보다 훨씬 낮은 온도에서 시스템이 작동할 수 있습니다.

- 전기 가격이 상승함에 따라 사람들은 더 환경 친화적인 방법으로 전력을 생산해야 할 것이며, 이는 SOFC에 많은 시장 기회를 창출하고 스칸듐의 중요성을 더욱 중요하게 만들 것입니다.

- 석탄과 천연가스 같은 전통적인 에너지원에 대한 환경 우려가 커지면서 고체 산화물 연료전지는 앞으로 수요가 증가할 것으로 보입니다.

- 석탄, 천연가스 등 기존 에너지원에 대한 환경 우려로 청정에너지에 대한 수요가 증가하면서 향후 고체 산화물 연료전지에 대한 수요가 증가할 것으로 예상됩니다. 고체 산화물 연료전지는 높은 효율을 제공하며 환경적, 재정적 이점을 제공합니다. 고체 산화물 연료전지의 전기 효율은 최대 60%에 달합니다.

- 또한 에너지정보국에 따르면 2023년에는 약 2조 8,000억 달러가 에너지에 투자되었으며, 그 중 1조 7,000억 달러는 재생가능 에너지, 원자력, 송전망, 저장, 저배출 연료, 효율 개선, 최종 용도의 재생 가능 에너지와 전기를 포함한 청정 에너지에 사용되었습니다.

- 또한 미국 에너지부에 따르면 2030년 청정 에너지원의 전력 비중은 인플레이션 저감법 통과 전 예상치의 거의 두 배에 달하는 80%까지 증가할 수 있을 것으로 전망됩니다.

- 또한 SOFC 시장의 다양한 확장이 스칸듐 수요를 촉진하고 있습니다.

- HD현대는 2023년 10월 에스토니아의 고체 산화물 연료전지 회사 엘코젠에 4,500만 유로(4,760만 달러)를 투자할 것이라고 발표했습니다. 이 새로운 투자를 통해 양사는 Elcogen의 독점적 인 고체 산화물 연료전지(SOFC) 기반 해양 추진 시스템과 거치 발전 및 Elcogen의 고체 산화물 전해조 셀(SOEC) 기술을 기반으로 한 그린 수소 제조에 주력 할 예정입니다.

- 2023년 8월, 고체 산화물 연료전지 제조업체인 블룸 에너지(Bloom Energy)는 대만의 유명한 칩 기판 및 인쇄 회로 기판(PCB) 제조업체인 Unimicron Technologies와의 계약을 통해 획기적인 10메가와트(MW) 고체 산화물 연료전지의 초기 단계를 성공적으로 설치했습니다.

- 고체 산화물 연료전지 시장은 가까운 장래에 스칸듐 수요가 크게 증가할 것으로 보입니다.

중국이 시장을 독점할 전망

- 중국의 스칸듐은 티타늄, 철광석, 지르코늄과 같은 다른 재료의 부산물로 생산됩니다. 중국 내 상당량의 스칸듐은 중국 판즈화에 위치한 마그네토바나-일메나이트와 같은 티타늄 광석과 같은 안료 공장에서 이산화티타늄(TiO2) 침출수의 잔류물을 0.04% 농도로 활용하여 생산됩니다.

- 전 세계적으로 스칸듐의 주요 공급원은 니오븀-희토류 원소-철(Nb-REE-Fe)로, 세계 최대 REE 자원이자 스칸듐의 두 번째로 큰 자원입니다. 중국 내몽골에 위치하고 있으며 전 세계 스칸듐 생산량의 약 90%를 차지합니다.

- 중국은 정부가 저탄소 경제로의 전환을 위해 청정 에너지 기술 활용에 점점 더 집중하고 있기 때문에 연료전지 시장에서 큰 잠재력을 가지고 있습니다. 지난 2-3년 동안 중국 정부는 중국 내 연료전지 모빌리티의 보급에 중점을 두어 공공 지원의 초점을 BEV에서 FCEV로 약간 이동시켰습니다.

- 게다가 중국 정부는 2025년까지 약 5만대의 무공해 연료전지 차량을 지원할 계획을 발표하고,2030년까지 100만 대까지 빠르게 확대하여 SOFC와 중국 내 스칸듐 시장에 기회를 제공할 계획입니다.

- 중국은 최대 항공기 제조업체 중 하나이자 국내 항공 승객이 가장 많은 시장 중 하나입니다.

- 또한 중국의 항공기 부품 및 조립 제조 부문은 200개 이상의 소규모 항공기 부품 제조업체가 존재하며 빠르게 성장하고 있습니다. 또한 중국 정부는 국내 제조 역량을 강화하기 위해 막대한 투자를 하고 있습니다.

- 따라서 위에서 언급 한 요인은 연구 된 시장에 대한 수요에 영향을 미칠 것으로 예상됩니다.

스칸듐 산업 개요

스칸듐 시장은 통합된 성질을 가지고 있습니다. 시장의 주요 기업으로는 호남 희토류 금속 재료 연구소, MCC 그룹, Sunrise Energy Metals Limited, 호남 동방 스칸듐, Henan Rongjia Scandium Vanadium Technology 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 고체 산화물 연료전지(SOFCS)의 사용 증가

- 항공 우주 및 방위 산업에서 알루미늄-스칸듐 합금에 대한 수요 증가

- 억제요인

- 높은 스칸듐 비용

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

- 가격 분석

- 환경 영향 분석

제5장 시장 세분화

- 제품 유형

- 산화물

- 불화물

- 염화물

- 질산염

- 요오드화물

- 합금

- 탄산염 및 기타 제품 유형

- 최종 사용자 산업

- 항공 우주 및 방위

- 고체 산화물 연료전지

- 세라믹

- 조명

- 전자

- 3D 프린팅

- 스포츠 용품

- 기타 최종 사용자 산업

- 지역

- 생산 분석

- 중국

- 러시아

- 필리핀

- 세계 기타 지역

- 소비 분석

- 미국

- 중국

- 러시아

- 일본

- 브라질

- 유럽연합

- 세계 기타 지역

- 생산 분석

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 시장 점유율(%) 및 랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- Guangxi Maoxin Technology Co. Ltd

- Henan Rongjia Scandium Vanadium Technology Co. Ltd

- Huizhou Top Metal Materials Co. Ltd

- Hunan Rare Earth Metal Materials Research Institute Co. Ltd

- Hunan Oriental Scandium Co. Ltd

- JSC Dalur

- MCC Group

- NioCorp Development Ltd

- Rio Tinto

- Rusal

- Scandium International Mining Corporation

- Stanford Advanced Materials

- Sumitomo Metal Mining Co. Ltd(Taganito HPAL nickel Corp.)

- Sunrise Energy Metals Limited

- Treibacher Industrie AG

제7장 시장 기회와 앞으로의 동향

- 자동차 산업에서의 잠재적 용도

- 성장하는 에너지 저장 기술

The Scandium Market size is estimated at USD 0.77 billion in 2025, and is expected to reach USD 1.53 billion by 2030, at a CAGR of 14.7% during the forecast period (2025-2030).

Key Highlights

- The COVID-19 pandemic negatively impacted the scandium market. Due to the lockdown, major end-user segments such as aerospace and defense, ceramics, and electronics were suspended, reducing the usage of scandium. However, post-pandemic, the market expanded steadily because of the continued activities in major end-user segments.

- In the short term, increasing usage in solid oxide fuel cells (SOFCS) and increasing demand for aluminum-scandium alloys in the aerospace and defense industry are the factors driving the studied market.

- However, the high price of scandium may hinder the growth of the studied market between 2024 and 2029.

- Potential applications in the automotive industry and growing technology for storing energy are likely to give the market opportunities in the coming years.

- China is expected to dominate the market, and the European Union is expected to see the highest CAGR between 2024 and 2029.

Scandium Market Trends

The Solid Oxide Fuel Cells (SOFCs) Segment is Expected to Dominate the Market

- SOFCs use a solid oxide material called an electrolyte, which helps move negative oxygen ions from the cathode to the anode. In these cells, anodes and cathodes are made from special inks that cover the electrolyte. Therefore, SOFCs do not require any precious metal, corrosive acids, or molten material.

- Electrolyte materials are subjected to high temperatures to catalyze natural gas conversion to energy. However, the high temperature for the catalyzing conversion process can lead to the quick degradation of ceramic electrolytes, adding to the capital and maintenance costs.

- Using scandium in solid electrolytes helps the system work at much lower temperatures than traditional SOFCs. So, the use of scandium helped lower the cost of SOFCs, which made them easier to use for power generation in many places.

- As electricity prices go up, people will need to use more environmentally friendly ways to make power, which is likely to create many market opportunities for SOFCs and make scandium even more important.

- Due to growing environmental concerns regarding traditional energy sources like coal and natural gas, solid oxide fuel cells are likely to see increased demand in the future.

- The increasing demand for clean energy over environmental concerns of energy generation from conventional sources, such as coal and natural gas, is expected to drive the demand for solid oxide fuel cells in the future. Solid oxide fuel cells offer high efficiency and deliver environmental and financial benefits. The electrical efficiency of solid oxide fuel cells reaches up to 60%. This means 60% of the energy stored in the fuel is converted to useful electrical energy. This is much higher than the efficiency of coal power plants.

- Furthermore, according to the Energy Information Administration, around USD 2.8 trillion was invested in energy in 2023, out of which USD 1.7 trillion was used for clean energy, including renewable power, nuclear, grids, storage, low-emission fuels, efficiency improvements, and end-use renewables and electrification.

- In addition, according to the US Department of Energy, the share of electricity from clean sources in 2030 could grow to 80%, nearly twice the expected amount before the Inflation Reduction Act passed.

- Furthermore, various expansions in the SOFC market are fueling the demand for scandium. For instance:

- In October 2023, HD Hyundai announced an investment of EUR 45 million (USD 47.6 million) in Estonian solid oxide fuel cell firm Elcogen. With the new investment, the two companies intend to focus on marine propulsion systems and stationary power generation based on Elcogen's proprietary solid oxide fuel cell (SOFC) and green hydrogen production based around Elcogen's solid oxide electrolyzer cell (SOEC) technology.

- In August 2023, Bloom Energy, a manufacturer of solid oxide fuel cells, successfully installed the initial phase of a groundbreaking 10-megawatt (MW) solid oxide fuel cell contract with Unimicron Technology Corp., a prominent chip substrate and printed circuit board (PCB) manufacturer in Taiwan.

- The solid oxide fuel cell market is likely to witness a big increase in demand for scandium in the near future.

China is Expected to Dominate the Market

- Scandium in China is produced as a by-product of other materials such as titanium, iron ore, and zirconium. Nowadays, more than 60-70 % of the scandium production in China is as titanium by-products. The sizeable chuck of scandium in the country is also produced by exploiting the residue from titanium dioxide (TiO2) leach streams in pigment plants such as titanium ore like magnetovana-ilmenite located in Panzhihua, China, at a concentration as high as 0.04%.

- Globally, the principal source of scandium is niobium-rare earth element-iron (Nb-REE-Fe), the world's largest REE resource and second largest resource of scandium. It is located in Inner Mongolia, China, and accounts for approximately 90% of global scandium production. In Bayan Obo, scandium is regenerated as a by-product of the mining of the other REEs and iron.

- China has great potential in the fuel cell market as the government increasingly focuses on utilizing clean energy technology to switch to a low-carbon economy. For the past 2-3 years, the Chinese government put great emphasis on the roll-out of fuel cell mobility in the country, shifting the public support focus slightly away from BEV to FCEV. The national government offers CNY 500,000 (USD 73 thousand) as a subsidy for each vehicle.

- Furthermore, the Chinese government announced plans to support around 50,000 zero-emissions fuel cell vehicles by 2025, with plans to rapidly expand to 1 million FCEVs in service by 2030, providing opportunities to SOFCs and the scandium market in the country.

- China is one of the largest aircraft manufacturers and one of the largest markets for domestic air passengers. Moreover, the country's aircraft parts and assembly manufacturing sector has been growing rapidly, with the presence of over 200 small aircraft parts manufacturers. Also, the Chinese government is investing heavily in increasing its domestic manufacturing capacities.

- China is the largest base for electronics production in the world. China is actively engaged in manufacturing electronic products, such as smartphones, TVs, wires, cables, portable computing devices, gaming systems, and other personal electronic devices. Economic development in China and improving living standards among the population drive consumer electronics demand. Electronic products, such as smartphones, OLED TVs, and tablets, have the highest growth rates in the consumer electronics segment of the market in terms of demand. The revenue is expected to show an annual growth rate of 2.04% by 2025.

- Therefore, the above-mentioned factors are expected to impact the demand for the studied market.

Scandium Industry Overview

The scandium market is consolidated in nature. Some of the major players in the market are Hunan Institute of Rare Earth Metal Materials, MCC Group, Sunrise Energy Metals Limited, Hunan Oriental Scandium Co. Ltd, and Henan Rongjia Scandium Vanadium Technology Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Usage in Solid Oxide Fuel Cells (SOFCS)

- 4.1.2 Increasing Demand for Aluminum-Scandium Alloys in the Aerospace and Defense Industry

- 4.2 Restraints

- 4.2.1 High Cost of Scandium

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Price Analysis

- 4.6 Environmental Impact Analysis

5 MARKET SEGMENTATION

- 5.1 Product Type

- 5.1.1 Oxide

- 5.1.2 Fluoride

- 5.1.3 Chloride

- 5.1.4 Nitrate

- 5.1.5 Iodide

- 5.1.6 Alloy

- 5.1.7 Carbonate and Other Product Types

- 5.2 End-user Industry

- 5.2.1 Aerospace and Defense

- 5.2.2 Solid Oxide Fuel Cells

- 5.2.3 Ceramics

- 5.2.4 Lighting

- 5.2.5 Electronics

- 5.2.6 3D Printing

- 5.2.7 Sporting Goods

- 5.2.8 Other End-user Industries

- 5.3 Geography

- 5.3.1 Production Analysis

- 5.3.1.1 China

- 5.3.1.2 Russia

- 5.3.1.3 Philippines

- 5.3.1.4 Rest of the World

- 5.3.2 Consumption Analysis

- 5.3.2.1 United States

- 5.3.2.2 China

- 5.3.2.3 Russia

- 5.3.2.4 Japan

- 5.3.2.5 Brazil

- 5.3.2.6 European Union

- 5.3.2.7 Rest of the World

- 5.3.1 Production Analysis

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) **/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Guangxi Maoxin Technology Co. Ltd

- 6.4.2 Henan Rongjia Scandium Vanadium Technology Co. Ltd

- 6.4.3 Huizhou Top Metal Materials Co. Ltd

- 6.4.4 Hunan Rare Earth Metal Materials Research Institute Co. Ltd

- 6.4.5 Hunan Oriental Scandium Co. Ltd

- 6.4.6 JSC Dalur

- 6.4.7 MCC Group

- 6.4.8 NioCorp Development Ltd

- 6.4.9 Rio Tinto

- 6.4.10 Rusal

- 6.4.11 Scandium International Mining Corporation

- 6.4.12 Stanford Advanced Materials

- 6.4.13 Sumitomo Metal Mining Co. Ltd (Taganito HPAL nickel Corp.)

- 6.4.14 Sunrise Energy Metals Limited

- 6.4.15 Treibacher Industrie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Potential Applications in the Automotive industry

- 7.2 Growing Technology for Storing Energy

샘플 요청 목록