|

시장보고서

상품코드

1685956

중국의 풍력에너지 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)China Wind Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

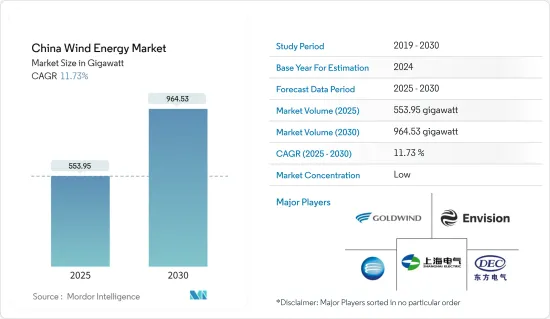

중국의 풍력에너지 시장 규모는 2025년 553.95기가와트로 추정되고, 2030년에는 964.53기가와트에 달할 것으로 예측되며, 예측기간 중(2025-2030년)의 CAGR은 11.73%를 나타낼 전망입니다.

주요 하이라이트

- 중기적으로는 정부 규제와 재생 에너지를 통해 생산되는 전력의 킬로와트당 비용 감소와 같은 요인이 시장을 주도할 것으로 예상됩니다. 국내 재생 에너지 프로젝트에 대한 수요 증가는 예측 기간 동안 풍력 에너지 시장의 성장을 촉진할 것으로 예상됩니다.

- 한편, 태양열, 수력 및 화석 연료와 같은 다른 에너지원과의 높은 경쟁은 시장의 성장을 제한 할 것으로 예상됩니다.

- 그럼에도 불구하고 건물 일체형 풍력 터빈(BIWT)의 개발은 향후 시장의 성장 기회를 창출할 것으로 예상됩니다.

중국의 풍력에너지 시장 동향

해상 부문은 상당한 성장을 보일 것으로 예상

- 해상 풍력 에너지 발전은 지난 5년 동안 낮은 풍속으로 더 많은 부지를 커버하기 위해 설치된 메가와트 용량당 생산되는 전기를 최대화하기 위해 발전해 왔습니다. 최근 몇 년 동안 풍력 터빈은 허브 높이가 높아지고, 직경이 넓어지고, 풍력 터빈 블레이드가 더 커지는 등 더욱 광범위해졌습니다.

- 약 18,000km의 해안선을 가진 중국은 허브 높이 90m에서 1,000GW 이상의 해상 풍력 발전의 기술적 가능성을 가지고 있습니다.

- 국제재생가능에너지기구(International Renewable Energy Agency)의 RE Capacity 2024에 따르면, 중국의 해상풍력발전설비는 2023년에 37,290메가와트에 달하고, 2022년의 30,460메가와트에서 증가했습니다.

- Global Wind Energy Council에 따르면 중국은 2023년에 6.8GW의 해상풍력발전을 개발했으며, 2024년에는 6년 연속 세계 1위를 차지했습니다.

- Global Wind Energy Council(GWEC)에 따르면, 중국은 2030년까지 세계의 해상 풍력 터빈의 5분의 1 이상, 즉 약 5200만 kW의 해상 풍력 터빈을 도입할 전망입니다 .

- 중국의 연안지방은 새로운 해상풍력발전의 개발에 힘을 쏟고 있습니다. 복건성, 절강성, 강소성은 각각 2025년까지 1,330만 kW, 600만 kW, 900만 kW의 해상 풍력 발전 프로젝트의 설치를 목표로 하고 있습니다.

- 2024년 2월, 중국 화넝 그룹(Huaneng Group Co. 는 친환경 및 저탄소 전환을 위한 노력의 일환으로 태양광 및 해상 풍력을 포함한 222개의 새로운 에너지 프로젝트에 대한 투자를 늘렸습니다(설치 용량 기준 세계 2위의 전력 회사).

- 이러한 개발 활동으로 인해 해상 부문은 향후 몇 년 동안 크게 성장할 것으로 예상됩니다.

재생 에너지에 대한 수요 증가가 시장을 견인할 것으로 예상

- 중국은 전 세계 최대 에너지 소비국이자 재생 에너지 시장으로, 국내 에너지 수요를 충족하기 위해 재생 에너지 용량을 빠르게 확대하고 있습니다.

- 제14차 5개년 계획(2021-2025년)의 일환으로서, 2025년까지, 국내의 전력 소비의 33%를 재생 가능 에너지로 충당하는 것을 목표로 하고 있습니다. 또한, 2030년까지 재생 가능 에너지 발전을 3,300TWh까지 증가시키는 것을 목표로 하고 있습니다.

- 최근 업데이트된 국가결정기여(NDC)에서 중국은 2030년까지 최대 배출량을 달성하고 파리 협정에 따른 약속의 일환으로 탄소 중립을 달성하기로 약속했습니다.

- 에너지 목표와 관련해서는 GDP 단위당 CO2 배출량을 2005년 수준에서 65% 이상 감축하고 풍력 및 태양광 총 설치 용량을 1,200GW로 늘리는 것을 목표로 하고 있습니다. CarbonBrief에 따르면, 중국의 재생에너지 산업이 빠르게 성장함에 따라 중국은 2030년 목표보다 훨씬 앞당겨 풍력+태양광 1,200GW 설치 목표를 달성할 것으로 예상됩니다.

- 중국의 각 성에서는 국가 목표의 일환으로 재생 에너지 프로젝트에 대한 개별 목표를 설정했습니다.

- 국제재생가능에너지기관의 RE Capacity 2024에 따르면 2023년 중국의 풍력발전설비 용량은 441.89기가와트에 달하고, 2022년 365.96기가와트에서 증가했습니다.

- Global Wind Energy Council의 Global Wind Report 2024에 따르면, 국가 수준에서 중국과 미국은 여전히 세계 최대 육상 풍력 추가 시장이며 브라질, 독일, 인도가 그 뒤를 잇고 있습니다.

- 2023년 11월에는 중국의 Longyuan Power Group과 Shanghai Electric Wind Power Group이 개발한 심해 부체식 풍력 발전과 양식을 조합한 1일 96,000kWh의 전력을 생산할 수 있는 세계 최초의 해상 재생 에너지 프로젝트가 완공되어 중국 풍력 에너지 부문이 크게 발전할 수 있는 계기가 마련되었습니다.

- 따라서 국유 기업의 투자 증가와 풍력 에너지 발전에 대한 정부의 우호적인 정책이 예측 기간 동안 중국 풍력 에너지 시장의 성장을 견인할 것으로 예상됩니다.

중국의 풍력에너지 산업 개요

중국의 풍력에너지 시장은 단편화되어 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 범위

- 조사의 전제조건과 시장 정의

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 소개

- 풍력에너지의 설치 용량 및 예측(-2029년)

- 최근 동향과 개발

- 정부의 규제와 정책

- 시장 역학

- 성장 촉진요인

- 재생 에너지에 대한 수요 증가

- 풍력 에너지원을 통해 생성되는 전기의 킬로와트 당 비용 감소

- 억제요인

- 태양 에너지와 같은 기타 재생 가능 에너지 원의 설치 증가

- 성장 촉진요인

- 공급망 분석

- PESTLE 분석

제5장 시장 세분화, 장소별

- 육상

- 해상

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 프로파일

- Nordex SE

- Xinjiang Goldwind Science & Technology Co. Ltd

- General Electric Company

- Siemens Gamesa Renewable Energy SA

- Vestas Wind Systems AS

- Envision Group

- Shanghai Electric Group Company Limited

- Dongfang Electric Corporation

- Ming Yang Smart Energy Group Limited

- 한화그룹

- 시장 랭킹 분석

제7장 시장 기회와 앞으로의 동향

- 건물 일체형 풍력 터빈(BIWT)의 개발

The China Wind Energy Market size is estimated at 553.95 gigawatt in 2025, and is expected to reach 964.53 gigawatt by 2030, at a CAGR of 11.73% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as government regulations and decreasing cost per kilowatt of electricity generated through renewables are expected to drive the market. Rising demands for renewable energy projects within the country are expected to propel the growth of the wind energy market during the forecast period.

- On the other hand, the high competition from other energy sources such as solar, hydro, and fossil fuels is expected to restrain the growth of the market.

- Nevertheless, the development of building-integrated wind turbines (BIWTs) is expected to create a growth opportunity for the market in the future.

China Wind Energy Market Trends

The Offshore Segment is Expected to Witness Significant Growth

- Offshore wind energy power generation has evolved over the last five years to maximize the electricity produced per megawatt capacity installed to cover more sites with lower wind speeds. In recent years, wind turbines have become more extensive, with taller hub heights, broader diameters, and larger wind turbine blades.

- With a coastline of approximately 18,000 km, China has more than 1,000 GW of technical potential for offshore wind at a hub height of 90 meters. China has no long-term national offshore wind target, but coastal provinces have set ambitious official targets.

- According to the International Renewable Energy Agency RE Capacity 2024, offshore installations in China reached 37,290 megawatts in 2023, an increase from 30,460 megawatts in 2022.

- According to the Global Wind Energy Council, China ranked first globally in terms of annual offshore wind development for the sixth year in a row in 2024, with 6.8 GW commissioned in 2023. These additions made up 58% of global additions and brought China's total offshore wind installations close to 38 GW, 4.9 GW higher than Europe combined.

- According to the Global Wind Energy Council (GWEC), China is expected to host more than a fifth of the world's offshore wind turbines, equating to approximately 52 GW of offshore wind by 2030.

- Coastal provinces in China have been focused on developing new offshore wind capacity. Guangdong aims to install 18 GW of offshore capacity by 2025, while Fujian, Zhejiang, and Jiangsu aim to install 13.3 GW, 6 GW, and 9 GW of offshore wind power projects by 2025, respectively.

- In February 2024, China Huaneng Group Co. Ltd, the second-largest power utility in the world by installed capacity, increased investments in 222 new energy projects, including solar and offshore wind power, as part of efforts toward green and low-carbon transformation.

- Owing to such development activities, the offshore segment is expected to grow significantly in the upcoming years.

The Rising Demand for Renewable Energy is Expected to Drive the Market

- China is the largest energy consumer and renewable energy market globally, and the country is rapidly expanding its renewable energy capacity to satiate its domestic energy demand. As the country has been suffering from air pollution caused primarily by fossil-fuel-fired power plant emissions, it is focused on expanding its renewable energy capacity to meet its growing energy demands while reducing overall emissions.

- As part of its 14th five-year plan (2021-2025), by 2025, the country aims to supply 33% of national power consumption from renewables, up from 29% in 2021. The country aims to increase renewable energy generation to 3,300 TWh by 2030.

- In its latest updated Nationally Determined Contributions (NDC), China committed to reaching peak emissions by 2030 and achieving carbon neutrality as part of its commitments under the Paris Agreement. In terms of energy targets, the country aims to cut CO2 emissions per unit of GDP by more than 65% from 2005 levels and increase the total installed wind plus solar capacity to 1,200 GW.

- According to CarbonBrief, based on the rapid growth of the renewable energy industry in the country, it is estimated that China will reach its target of 1,200 GW of wind+solar deployment significantly ahead of its 2030 deadline. Such rapid growth in the installed wind energy capacity is due to the rising demand created as a result of environmental commitments, and the rising domestic energy consumption is expected to drive the wind energy market during the forecast period.

- China's provinces have set up individual targets for renewable energy projects as a part of national targets. The largest targets have been set up by the northwestern provinces of Inner Mongolia and Gansu to leverage the presence of large tracts of uninhabited desert lands. These two provinces plan to add a cumulative 190 GW of wind and solar projects by 2025.

- According to the International Renewable Energy Agency RE Capacity 2024, wind installed capacity in China in 2023 reached 441.89 gigawatts, increasing from 365.96 gigawatts in 2022, clearly indicating the role of wind energy in increasing renewable energy capacity in China.

- According to the Global Wind Energy Council's Global Wind Report 2024, at the country level, China and the United States remained the world's two largest markets for onshore wind additions, followed by Brazil, Germany, and India.

- In November 2023, the world's first maritime renewable energy project with a capacity to generate 96,000 kWh of electricity daily, which combines deep-sea floating wind energy and aquaculture, developed by Longyuan Power Group and Shanghai Electric Wind Power Group in China, was completed, enabling a significant step forward for the Chinese wind energy sector.

- Thus, increasing investments from state-owned companies and favorable government policies in wind energy generation are expected to drive the growth of the Chinese wind energy market during the forecast period.

China Wind Energy Industry Overview

The Chinese wind energy market is fragmented. Some of the major players in the market include Xinjiang Goldwind Science & Technology Co. Ltd, ENVISION GROUP, Shanghai Electric, Dongfang Electric Corporation, and Mingyang Smart Energy Group Limited.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Study Assumptions And Market Definition

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Wind Energy Installed Capacity and Forecast in GW, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Rising Demand for Renewable Energy

- 4.5.1.2 Decreasing Cost per Kilowatt of Electricity Generated Through Wind Energy Sources

- 4.5.2 Restraints

- 4.5.2.1 Increasing Installation of Other Renewable Sources Such as Solar Energy

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

5 MARKET SEGMENTATION - BY LOCATION

- 5.1 Onshore

- 5.2 Offshore

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Nordex SE

- 6.3.2 Xinjiang Goldwind Science & Technology Co. Ltd

- 6.3.3 General Electric Company

- 6.3.4 Siemens Gamesa Renewable Energy SA

- 6.3.5 Vestas Wind Systems AS

- 6.3.6 Envision Group

- 6.3.7 Shanghai Electric Group Company Limited

- 6.3.8 Dongfang Electric Corporation

- 6.3.9 Ming Yang Smart Energy Group Limited

- 6.3.10 Hanwha Group

- 6.4 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Development of Building-integrated Wind Turbines (BIWTs)