|

시장보고서

상품코드

1851380

메탄올 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Methanol - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

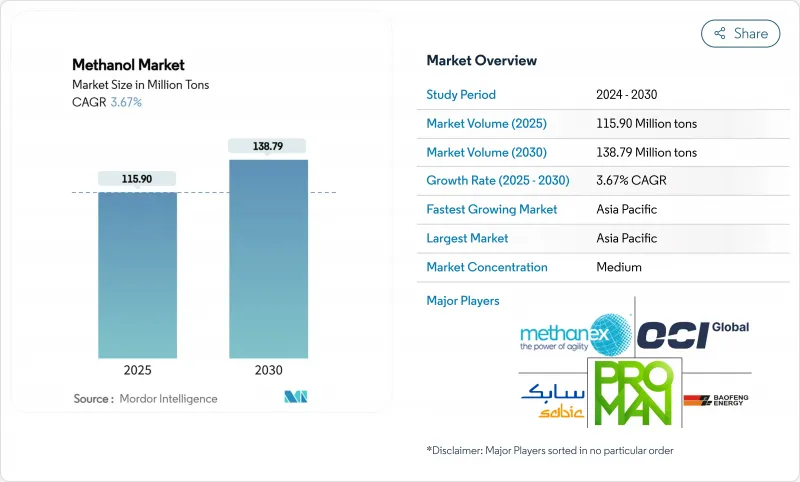

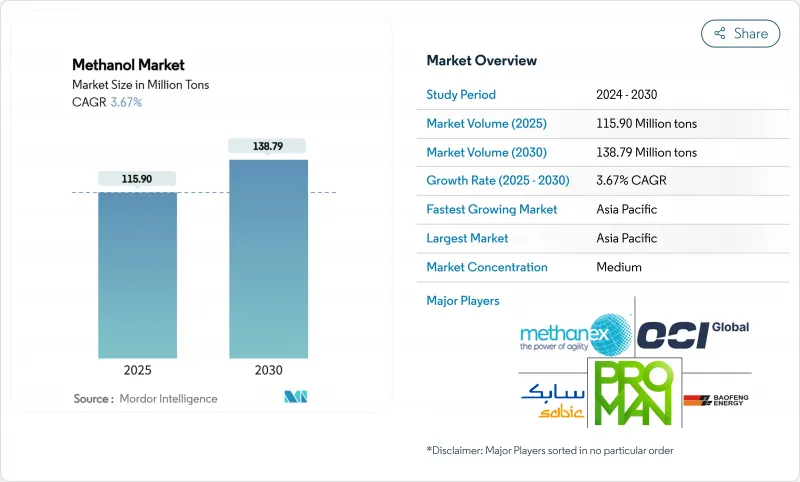

메탄올 시장 규모는 2025년에 1억 1,590만 톤으로 추정되고, 2030년에는 1억 3,879만 톤에 달할 것으로 예측되며, 예측 기간(2025-2030년) CAGR 3.67%로 성장할 전망입니다.

대략적인 숫자에는 지역 대비가 숨겨져 있습니다. 대서양 유역의 가격은 예기치 않은 정전을 거쳐 견조하게 추이했지만 아시아의 스팟 가격은 연화되어 상인의 재정 거래 창을 넓혔습니다. 중국 대 올레핀(MTO) 생산 능력 확대, 북미의 '메가 메가' 플랜트, 해양 연료 수요의 급증이 성장 시나리오의 축이 되고 있습니다. 재생 가능한 메탄올 프로젝트는 큰 업사이드를 가져오지만 인증 지연과 인프라 갭은 당분간 공급 구축을 제한합니다. 그러나 저탄소 생산 및 해운전환에 대한 지속적인 투자는 메탄올 시장의 중기 안정 궤도를 지원합니다.

세계의 메탄올 시장 동향 및 인사이트

중국, 미국, 신흥아시아에서 석유화학 생산 능력 확대

2024년 중국의 종합콤비나트에서 1,480만B/D라는 기록적인 원유처리 능력을 달성함으로써 정제업자가 화학 원료로 축발을 옮기고 있기 때문에 메탄올 수요가 높아지고 있습니다. 동시에 미국의 '메가 메가' 메탄올 플랜트는 중국의 MTO 유닛에 공급되도록 설계되었으며 기존의 무역 흐름을 변화시키는 태평양 횡단 밸류체인을 형성합니다. 아시아의 신흥 생산자는 이 모델을 모방하고 있으며, 석탄에서 메탄올에 대한 투자가 일부 건설 중입니다. 이러한 프로젝트는 총체적으로 지역의 자급률을 올리지만 동시에 수요 증가를 메탄올 시장의 펀더멘탈스에 확실히 연결해 둡니다. 이 역동적인 움직임은 2030년까지 약 800만 톤의 새로운 소비를 추가할 전망이며, 아시아태평양의 세계 수지의 중심성을 확고하게 할 것으로 예측됩니다.

해양 부문의 저탄소 연료로의 전환

2023년에는 메탄올 대응선 138척이 발주되어 LNG 대응선 130척을 웃돌았습니다. 2025년 초에 발주 척수는 추가로 23척 증가했으며, 마스크와 같은 주요 운송 회사는 2027년까지 25척의 듀얼 연료 컨테이너선 취항을 목표로 하며 매년 150만 톤의 CO2를 절감할 수 있습니다. 재생가능한 메탄올은 라이프사이클의 온실가스 배출량을 최대 95%까지 줄일 수 있으며, IMO의 2024년 라이프사이클 원단위 가이드라인에 적합합니다. 선박의 급속한 채용 페이스는 실현된 연료 공급을 상회하고 견조한 수요 기대를 뒷받침하고 메탄올 시장에 장기적인 견인력을 강화하고 있습니다.

원료 가격 변동

지정학적 긴장이 유럽과 아시아의 LNG 벤치마크에 영향을 미치고 수입에 의존하는 지역의 메탄올 생산 비용이 상승했기 때문에 천연 가스 가격은 2024년에 크게 변동했습니다. 특히 유럽에서는 가스 공급이 확보되지 않은 생산자는 북미나 중동의 플랜트에 비해 마진이 압축되는 사태에 직면했습니다. 메탄올 시장은 천연 가스가 여전히 원료의 65%를 차지하기 때문에 이러한 변화에 노출되어 있습니다. 변동성은 또한 새로운 장비의 투자 결정을 복잡하게 하고 다운스트림 구매자의 가격 투명성을 저해합니다. 위험 회피 전략과 통합 전략으로 인해 일부 위험이 상쇄되고 불안정한 상황이 지속되면 단기 성장 전망이 약해집니다.

부문 분석

2024년에는 천연가스가 전 원료의 65%를 차지했습니다. 헤인즈빌 지역과 퍼미안 지역에서의 견조한 셰일 생산은 비용 경쟁력 있는 생산을 지원하고 메탄올 시장 규모의 신뢰할 수 있는 공급을 보장합니다. 바이오메탄올과 e-메탄올을 결합한 재생가능한 경로는 2030년까지 3,570만 톤의 잠재 용량을 가진 210개의 프로젝트가 발표되었으며, 메탄올 산업에서 전환의 징후를 보여줍니다.

천연가스는 2030년까지 주요 공급원료로 지속될 것으로 예상되지만, 인증된 녹색 대체 원료가 해운과 화학 고객으로부터 프리미엄을 획득함에 따라 점유율이 점차 줄어들고 있습니다. 메탄올 시장은 이 두 가지 성장 궤도로부터 이익을 얻고 있습니다. 기존의 기업에서 원료의 우위성을 살려, 재생가능 기술을 재빨리 채용한 기업은 보다 높은 마진과 브랜드 차별화를 획득하고 있습니다.

MTO, 가솔린 혼합연료, 선박용 연료를 포함한 에너지 관련 용도는 2024년 소비량의 54%를 차지했으며, 메탄올 시장 역학에 대한 영향력을 두드러지게 하고 있습니다. 중국의 메탄올에서 올레핀으로의 붐만으로 2024년에는 400만 톤이 추가적으로 흡수되어 이 지역의 세계 무역에 대한 영향력이 강화되었습니다.

현재 톤수로는 겸손하지만 선박용 연료 수요는 큰 점유율을 차지하고 있습니다. 듀얼 연료의 주문 톤수는 2030년까지 연간 700만 톤의 벙커 수요가 추가됨을 시사하고 있으며, 해양 용도의 메탄올 시장 규모가 기존의 에너지 용도에 필적할 수 있음을 나타냅니다. 메탄올은 연료와 화학물질에 범용성이 있기 때문에 주기적인 변동을 원활하게 하고, 이 분야의 회복력을 높이고 있습니다.

지역 분석

아시아태평양은 2024년 메탄올 소비량의 78%(약 90,400킬로톤)를 차지했습니다. 중국의 석탄에서 올레핀으로의 전환, 인도네시아의 바이오디젤 B40의 전개, 동남아시아의 생산 능력 증강 계획에 의해 이 지역의 리더십은 확고해졌습니다. 아시아태평양의 메탄올 시장 규모는 해운과 재생가능 연료에 의한 새로운 수요 노드가 석유화학의 필요량을 증가시키기 때문에 2030년까지 연평균 복합 성장률(CAGR) 3.86%로 성장할 것으로 예측됩니다. 아시아태평양의 가격은 여전히 중국의 수입평가와 밀접하게 관련되어 있으며, 이 지역은 세계적인 감정의 지표가 되고 있습니다.

메탄올 시장에서 북미의 역할은 변화하고 있습니다. 풍부한 셰일 가스는 루이지애나 주에 있는 레이크 찰스 메탄올의 32억 달러의 복합 시설로 대표되는 수출 지향 프로젝트의 파도를 지원합니다. 한때 주로 국내 포름알데히드용이었던 미국의 생산량은 현재 아시아의 MTO 구매자를 향해 무역회랑이 재조합되어 재정거래의 옵션성이 제공되고 있습니다.

유럽과 중동에서는 전략이 다릅니다. 유럽은 'Fit for 55' 목표를 달성하기 위해 e-메탄올에 투자하고 Forestal del Atlantico의 스페인 공장과 같은 프로젝트는 선박용 벙커를 대상으로 합니다. 반대로 중동은 기존의 천연가스 기반 시설을 두배로 하고 아시아에 공급하기 위한 원료의 우위성을 활용하고 있습니다. 이러한 지역이 일체가 되어 저탄소화 프리미엄을 추구하는 측과 비용 리더십을 최대한 발휘하는 측이라는 점점 이분화된 메탄올 시장을 형성하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 중국, 미국, 신흥 아시아에서 확대하는 석유화학 생산 능력

- 해양 분야에서 저탄소 연료로의 이행-세계 선사에 의한 그린 메탄올 채용

- 메탄올 가솔린과 DME를 촉진하는 ASEAN과 LATAM의 혼합연료에 관한 정부의 의무화

- 올레핀 생산에 있어서의 메탄올의 이용 확대

- 프로파일렌 공급 부족이 중동의 메탄올 기반 수요 강화

- 시장 성장 억제요인

- 원료 가격의 변동

- 그린 메탄올의 인증 프레임워크 지연이 오프테이크 계약 제한

- 건강에 해로운 영향

- 밸류체인 분석

- 기술의 전망

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 정도

- 주요 원료별 생산 능력 분석

- 무역 흐름 분석

- 가격 동향 및 예측

제5장 시장 규모 및 성장 예측

- 원료별

- 천연가스

- 석탄

- 재생 가능 원료(바이오매스, 고형 폐기물)

- 기타(CO2, 그린 수소, 석유 잔류물, 나프타)

- 유도체별 및 용도별

- 전통 화학

- 포름알데히드

- 아세트산

- 용제

- 메틸아민

- 기타 전통 화학

- 에너지 관련

- 메탄올루올레핀(MTO)

- 메틸tert-부틸에테르(MTBE)

- 가솔린 혼합

- 디메틸에테르(DME)

- 바이오디젤

- 전통 화학

- 최종 이용 산업별

- 자동차 및 운수

- 화학제품

- 해상연료

- 기타(전자 및 가전, 발전)

- 등급별

- 화학 등급

- 연료 등급

- 기타(울트라 클린 및 배터리 등급, 재생 가능 연료(바이오 및 E 메탄올))

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 베트남

- 태국

- 인도네시아

- 말레이시아

- 호주

- 뉴질랜드

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 튀르키예

- 러시아

- 북유럽 국가

- 스페인

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 카타르

- 아랍에미리트(UAE)

- 이란

- 남아프리카

- 나이지리아

- 이집트

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Atlantic Methanol

- BASF SE

- Carbon Recycling International(CRI)

- Celanese Corporation

- China National Chemical Corporation(ChemChina)

- Coogee

- Enerkem

- Eni SpA

- Gujarat State Fertilizers & Chemicals Limited(GSFC)

- INEOS

- Kaveh Methanol Company

- Kingboard Holdings Limited

- LyondellBasell Industries Holdings BV

- Methanex Corporation

- MITSUBISHI GAS CHEMICAL COMPANY, INC

- Natgasoline

- Ningxia Baofeng Energy Group

- OCI

- Petroliam Nasional Berhad(PETRONAS)

- Proman

- SABIC

- Yankuang Energy

- ZPC Integrated Refining & Petrochemical(Zhejiang)

제7장 시장 기회 및 향후 전망

AJY 25.11.21The Methanol Market size is estimated at 115.90 Million tons in 2025, and is expected to reach 138.79 Million tons by 2030, at a CAGR of 3.67% during the forecast period (2025-2030).

The headline figures hide sharp regional contrasts: Atlantic basin prices firmed after unplanned outages, while Asian spot prices softened, widening arbitrage windows for traders. China's expanding methanol-to-olefins (MTO) capacity, North American "mega-mega" plants, and surging marine-fuel demand anchor the growth narrative. Renewable methanol projects offer sizeable upside, yet certification lags and infrastructure gaps restrict near-term supply build-out. Feedstock volatility and uneven policy support add complexity, but sustained investment in low-carbon production and shipping conversions underpin a steady medium-term trajectory for the methanol market.

Global Methanol Market Trends and Insights

Expanding Petrochemical Capacity in China, US and Emerging Asia

Record crude throughput of 14.8 million bpd at Chinese integrated complexes in 2024 has raised methanol demand as refiners pivot toward chemical feedstocks. Concurrently, purpose-built US "mega-mega" methanol plants are geared to serve Chinese MTO units, forging a trans-Pacific value chain that recasts traditional trade flows. Emerging Asian producers are replicating this model, with several coal-to-methanol investments under construction. These projects collectively lift regional self-sufficiency, yet they also keep incremental demand firmly tethered to methanol market fundamentals. The dynamic is expected to add around 8 million tons of new consumption by 2030, cementing Asia-Pacific's centrality to global balances.

Marine Sector Transition to Low-Carbon Fuels

Methanol displaced LNG as the leading alternative fuel for newbuilds in 2023, when 138 methanol-capable vessels were ordered versus 130 LNG-ready ships. In early 2025, the orderbook grew by a further 23 ships, and major carriers such as Maersk now target 25 dual-fuel containerships on the water by 2027, potentially abating 1.5 million tCO2 each year. Renewable methanol can cut lifecycle greenhouse-gas emissions by up to 95%, aligning with the IMO's 2024 life-cycle intensity guidelines. The rapid pace of vessel commitments has outstripped realized fuel supply, underpinning firm demand expectations and reinforcing the long-term pull on the methanol market.

Feedstock Price Volatility

Natural-gas prices swung sharply in 2024 as geopolitical tensions affected European and Asian LNG benchmarks, inflating methanol production costs in import-dependent regions. Producers without secure gas supply, notably in Europe, faced compressed margins relative to plants in North America and the Middle East. The methanol market remains exposed to these swings because natural gas still accounts for 65% of feedstock. Volatility also complicates investment decisions for new capacity and hampers price transparency for downstream buyers. While hedging and integration strategies partly offset the risk, persistent instability tempers near-term growth prospects.

Other drivers and restraints analyzed in the detailed report include:

- Government Mandates on Blended Fuels in ASEAN & LATAM

- Increasing Utilization of Methanol in the Production of Olefins

- Slow Certification Frameworks for Green Methanol

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Natural gas accounted for 65% of total feedstock in 2024. Robust shale production in the Haynesville and Permian regions underpins cost-competitive output, ensuring reliable supply for the methanol market size. Renewable pathways-biomethanol and e-methanol-together represent 210 announced projects with potential capacity of 35.7 million t by 2030, signalling an incipient shift in the methanol industry.

Natural gas is projected to remain the anchor feedstock through 2030, but its share gradually contracts as certified green alternatives secure premiums from shipping and chemical customers. The methanol market benefits from this dual-track growth: conventional players capitalize on feedstock advantage, while early adopters of renewable technologies command higher margins and brand differentiation.

Energy-related uses-including MTO, gasoline blending and marine fuel-captured 54% of consumption in 2024, underscoring their influence on methanol market dynamics. The methanol-to-olefins boom in China alone absorbed an incremental 4 million t in 2024, reinforcing the region's pull on global trade.

Although currently modest in tonnage, marine fuel demand holds a significant share. Dual-fuel tonnage on order implies an additional 7 million t of annual bunker demand by 2030, indicating that the methanol market size for marine applications could rival existing energy uses. The versatility of methanol across fuels and chemicals thus smooths cyclical swings, enhancing the sector's resilience.

The Methanol Market Report Segments the Industry by Feedstock (Natural Gas, Coal, and More), Derivative/Application (Traditional Chemical and Energy Related), End-Use Industry (Automotive and Transportation, Chemical, and More), Grade (Chemical Grade, Fuel Grade, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (tons).

Geography Analysis

Asia-Pacific held a commanding 78% of global methanol consumption in 2024, equal to almost 90,400 kilotons. China's coal-to-olefins build-out, Indonesia's biodiesel B40 rollout and Southeast Asia's planned capacity additions cement regional leadership. The methanol market size in Asia-Pacific is forecast to grow at 3.86% CAGR to 2030 as new demand nodes from shipping and renewable fuels augment petrochemical requirements. Regional pricing remains closely tied to Chinese import parity, making the area the bellwether for global sentiment.

North America's role in the methanol market is undergoing transformation. Abundant shale gas underwrites a wave of export-oriented projects, typified by Lake Charles Methanol's USD 3.2 billion complex in Louisiana. US output, once mainly for domestic formaldehyde, is now squarely aimed at Asian MTO buyers, realigning trade corridors and providing arbitrage optionality.

Europe and the Middle East illustrate divergent strategies. Europe channels investment into e-methanol to meet "Fit for 55" goals, with projects such as Forestal del Atlantico's Spanish plant targeting shipping bunkers. Conversely, the Middle East doubles down on conventional natural-gas-based facilities, leveraging feedstock advantage to supply Asia. Together, these regions shape an increasingly bifurcated methanol market: one side chasing low-carbon premiums, the other maximizing cost leadership.

- Atlantic Methanol

- BASF SE

- Carbon Recycling International (CRI)

- Celanese Corporation

- China National Chemical Corporation (ChemChina)

- Coogee

- Enerkem

- Eni S.p.A.

- Gujarat State Fertilizers & Chemicals Limited (GSFC)

- INEOS

- Kaveh Methanol Company

- Kingboard Holdings Limited

- LyondellBasell Industries Holdings B.V.

- Methanex Corporation

- MITSUBISHI GAS CHEMICAL COMPANY, INC

- Natgasoline

- Ningxia Baofeng Energy Group

- OCI

- Petroliam Nasional Berhad (PETRONAS)

- Proman

- SABIC

- Yankuang Energy

- ZPC Integrated Refining & Petrochemical (Zhejiang)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Petrochemical Capacity in China, US, and Emerging Asia

- 4.2.2 Marine Sector Transition to Low-Carbon Fuels - Adoption of Green Methanol by Global Carriers

- 4.2.3 Government Mandates on Blended Fuels in ASEAN and LATAM Promoting Methanol Gasoline and DME

- 4.2.4 Increasing Utilization of Methanol in the Production of Olefins

- 4.2.5 On-Purpose Propylene Deficit Strengthening Demand for Methanol-Based Routes in the Middle East

- 4.3 Market Restraints

- 4.3.1 Feedstock Price Volatility

- 4.3.2 Slow Certification Frameworks for Green Methanol Limiting Off-take Agreements

- 4.3.3 Hazardous Impacts on Health

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products and Services

- 4.6.5 Degree of Competition

- 4.7 Production Capacity Analysis by Key Feedstock

- 4.8 Trade Flow Analysis

- 4.9 Pricing Trends and Forecasts

5 Market Size and Growth Forecasts (Volume and Value)

- 5.1 By Feedstock

- 5.1.1 Natural Gas

- 5.1.2 Coal

- 5.1.3 Renewable Feedstock (Biomass, Municipal Solid Waste)

- 5.1.4 Others (CO2, Green Hydrogen, Petroleum Residues and Naphtha)

- 5.2 By Derivative/Application

- 5.2.1 Traditional Chemical

- 5.2.1.1 Formaldehyde

- 5.2.1.2 Acetic Acid

- 5.2.1.3 Solvent

- 5.2.1.4 Methylamine

- 5.2.1.5 Other Traditional Chemicals

- 5.2.2 Energy Related

- 5.2.2.1 Methanol-to-olefin (MTO)

- 5.2.2.2 Methyl Tert-butyl Ether (MTBE)

- 5.2.2.3 Gasoline Blending

- 5.2.2.4 Dimethyl Ether (DME)

- 5.2.2.5 Biodiesel

- 5.2.1 Traditional Chemical

- 5.3 By End-use Industry

- 5.3.1 Automotive and Transportation

- 5.3.2 Chemical

- 5.3.3 Marine Fuel

- 5.3.4 Others (Electronics and Appliances, power generation)

- 5.4 By Grade

- 5.4.1 Chemical Grade

- 5.4.2 Fuel Grade

- 5.4.3 Others (Ultra-Clean/Battery Grade and Renewable (Bio-/E-Methanol))

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Vietnam

- 5.5.1.6 Thailand

- 5.5.1.7 Indonesia

- 5.5.1.8 Malaysia

- 5.5.1.9 Australia

- 5.5.1.10 New Zealand

- 5.5.1.11 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 Italy

- 5.5.3.4 France

- 5.5.3.5 Turkey

- 5.5.3.6 Russia

- 5.5.3.7 Nordics

- 5.5.3.8 Spain

- 5.5.3.9 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 Qatar

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Iran

- 5.5.5.5 South Africa

- 5.5.5.6 Nigeria

- 5.5.5.7 Egypt

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Atlantic Methanol

- 6.4.2 BASF SE

- 6.4.3 Carbon Recycling International (CRI)

- 6.4.4 Celanese Corporation

- 6.4.5 China National Chemical Corporation (ChemChina)

- 6.4.6 Coogee

- 6.4.7 Enerkem

- 6.4.8 Eni S.p.A.

- 6.4.9 Gujarat State Fertilizers & Chemicals Limited (GSFC)

- 6.4.10 INEOS

- 6.4.11 Kaveh Methanol Company

- 6.4.12 Kingboard Holdings Limited

- 6.4.13 LyondellBasell Industries Holdings B.V.

- 6.4.14 Methanex Corporation

- 6.4.15 MITSUBISHI GAS CHEMICAL COMPANY, INC

- 6.4.16 Natgasoline

- 6.4.17 Ningxia Baofeng Energy Group

- 6.4.18 OCI

- 6.4.19 Petroliam Nasional Berhad (PETRONAS)

- 6.4.20 Proman

- 6.4.21 SABIC

- 6.4.22 Yankuang Energy

- 6.4.23 ZPC Integrated Refining & Petrochemical (Zhejiang)

7 Market Opportunities and Future Outlook

- 7.1 Growing Trends Toward Renewable Methanol

- 7.2 White-space and Unmet-Need Assessment