|

시장보고서

상품코드

1686578

금속규소 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Silicon Metal - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

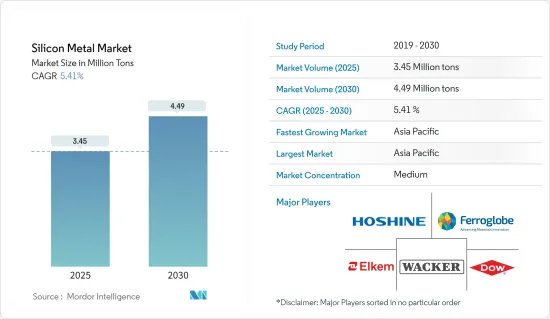

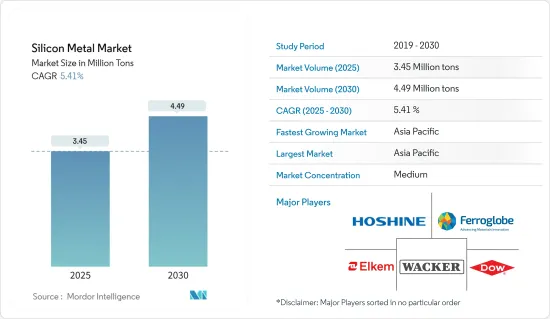

금속규소 시장 규모는 2025년에 345만 톤으로 추정되고, 예측 기간인 2025-2030년 CAGR 5.41%로 성장할 전망이며, 2030년에는 449만톤에 달할 것으로 예측되고 있습니다.

COVID-19는 금속규소 시장에 방해가 되었습니다. 자동차, 건설, 일렉트로닉스 등, 금속규소을 이용하는 많은 산업은 팬데믹 기간 중, 경기 후퇴, 개인 소비 감소, 생산 및 공급망의 혼란에 의해 수요가 감소했습니다. 그러나 운영 중단 및 규제가 완화됨에 따라 금속규소를 이용하는 산업은 회복되어 인프라 프로젝트, 자동차 생산, 반도체 제조, 신재생 에너지 설비에서의 수요가 증가하여 금속규소 수요를 밀어 올렸습니다.

주요 하이라이트

- 자동차 산업에서의 수요의 급증, 태양전지 산업에서의 사용 증가, 기타 여러가지 최종 사용자에서의 수요 증가가 세계의 금속규소 시장 확대로 이어질 것으로 예상됩니다.

- 그러나, 에너지 비용의 변동이 금속규소 시장의 성장을 방해하고 있습니다.

- 현재의 기술을 개선하는 것으로 생산 비용을 삭감하는 몇개의 방책 및 신재생 에너지 부문에서의 수요 증가가 향후 일정 기간, 시장 관계자에게 성장 기회를 가져올 것으로 예상됩니다.

- 아시아태평양은 가장 높은 시장 점유율을 유지하고 있으며 예측 기간 동안 금속규소 시장을 독점할 가능성이 높습니다.

금속규소 시장 동향

시장을 독점하는 태양 전지판 부문

- 현재 판매되고 있는 모듈의 약 95%를 차지하는 실리콘은 태양광 발전에서 가장 널리 사용되고 있는 반도체 재료입니다. 야금용 실리콘은 정제 과정에서 반도체나 태양 전지의 재료가 되는 고순도 실리콘으로 변환할 수 있습니다. 따라서 태양 전지 제조에 적합합니다.

- 태양 에너지는 세계 최대이며 급성장하고 있는 분야 중 하나입니다. 국제에너지기구(IEA)에 따르면, 이 분야는 세계 순 에너지 용량의 3분의 2 가까이를 차지하고 있습니다.

- 국제에너지기구(IEA)가 발표한 데이터에 따르면 2022년 태양광 발전의 생산량은 사상 최고인 270TWh 증가하여 26% 증가한 약 1300TWh에 이르렀습니다. 태양광 발전은 2022년에 모든 신재생 기술 중 가장 큰 폭의 절대적 발전량 성장을 보이며 사상 처음으로 풍력을 앞질렀습니다.

- 미국은 2022년에 도입된 인플레이션 삭감법(IRA)에 태양광 발전에 대한 후한 새로운 자금을 포함시켰습니다. 투자세액공제 및 생산세액공제는 태양광 발전의 설비 용량 및 공급망 성장을 크게 뒷받침할 것으로 보입니다.

- 국제에너지기구(IEA)가 발표한 데이터에 따르면 2022년 브라질은 약 11기가와트의 태양전지 용량을 추가해 2021년 성장률을 두배로 늘렸습니다. 산업계나 전력 소매업자로부터의 신재생 에너지에 대한 지속적인 수요를 고려하여 도입량은 중기적으로 이 수준을 유지할 것으로 예측되고 있습니다.

- 신재생 가능 에너지성(MNRE)이 발표한 데이터에 의하면, 2022년 말 시점에서 인도는 태양광 발전의 도입량에 있어서 세계 제4위의 지위를 차지했습니다. 태양광 발전의 누적 설비 용량은, 2022년 11월 시점에서 약 720만 kW에 이르렀습니다. 현재 인도의 태양광 발전 요금은 매우 경쟁력이 있고 그리드 패리티도 달성되고 있습니다.

- 상기의 개발에 의해 예측 기간을 통해 태양광 산업에 있어서 금속규소 시장이 견인될 것으로 예상되고 있습니다.

아시아태평양이 시장을 독점

- 아시아태평양, 특히 중국은 세계에서 가장 큰 금속규소 생산국입니다. 이 지역은 석영 및 석탄과 같은 원자재의 풍부한 매장량과 저비용 노동력에 대한 접근의 혜택을 받아 대규모 금속규소 생산 시설의 설립을 뒷받침하고 있습니다.

- 금속규소의 가장 중요한 용도는 실리콘 접착제, 밀봉제, 윤활제, 화학물질, 기타 물질, 알루미늄 합금입니다. 자동차, 건축 및 건설, 공업, 기타 최종 사용자 부문이, 이러한 제품의 주된 용도입니다.

- 중국에서는 신에너지차의 생산과 판매가 대폭 증가해, 판매 대수는 2022년까지 722만 대에 달했으며, 세계의 EV 판매 대수의 64%를 차지했습니다.

- 예측 기간 중 정부에 의한 EV, 하이브리드차, 연료전지차의 보급 촉진이 시장을 견인할 것으로 예측됩니다. 이 나라에서의 전기차 수요의 고조는 반도체, 알루미늄 합금, 실리콘 접착제의 필요성을 높이고 있습니다.

- 중국 기차공업협회(CAAM)가 발표한 보고서에 따르면 2022년 중국은 승용차 253만 대, 상용차 58만 대를 포함한 311만 대를 수출했으며, 2021년 대비 54.4% 증가했습니다.

- JinkoSolar, Trina Solar, JA Solar 등 세계의 태양광 발전 제조의 톱 기업은 중국에 본사를 두고 있습니다. 중국에서의 태양 전지 제조는 과거 2년간 대폭 증가하고 있습니다. 국제에너지기구(IEA)가 발표한 데이터에 따르면 2022년 추가되는 솔라 발전 용량은 100GW로 2021년 대비 60% 가까이 증가했으며, 중국은 태양광 발전 용량 추가라는 점에서 계속 앞서고 있습니다.

- 휴대폰, 노트북 및 기타 전자 제품 제조에 대한 투자는 중국에서 중요한 투자 분야입니다. 향후 수요 증가에 대응하기 위해 세계 주요 업체들이 중국 시장에 많은 자본을 투자하고 있습니다.

- 이러한 요인으로 인해 아시아태평양의 중국이 금속규소 시장을 독점할 것으로 예상됩니다.

금속규소 산업 개요

금속규소 시장은 부분적으로 통합되어 있습니다. 주요 기업는 Hoshine Silicon Industry, Ferroglobe, Elkem ASA, Dow, Wacker Chemie AG 등이 있습니다.(순부동)

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 자동차 산업에서 수요 급증

- 태양전지 산업에서 사용 증가

- 다양한 최종 사용자로부터의 실리콘 수요 증가

- 성장 억제요인

- 에너지 비용 변동

- 기타 억제요인

- 업계 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화

- 제품 유형별

- 야금 등급

- 화학 등급

- 용도별

- 알루미늄 합금

- 반도체

- 태양전지판

- 실리콘 유도체

- 기타 용도(건설 및 인프라)

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 인도네시아

- 태국

- 베트남

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 스페인

- 프랑스

- 튀르키예

- 러시아

- 노르딕

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 나이지리아

- 카타르

- 이집트

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴 및 협정

- 시장 점유율(%)** 및 랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- Anyang Huatuo Metallurgy Co., Ltd.

- Dow

- Elkem ASA

- Ferroglobe

- Hoshine Silicon Industry Co., Ltd.

- Liasa

- Minasligas

- Mississipi Silicon

- PCC SE

- RIMA INDUSTRIAL

- RusAL

- Shin-Etsu Chemical Co., Ltd.

- Wacker Chemie AG

- Zhejiang kaihua yuantong silicon industry co. LTD.

제7장 시장 기회 및 향후 동향

- 기존 기술의 혁신을 통한 생산 비용 절감 노력

- 신재생 에너지 분야 수요 증가

The Silicon Metal Market size is estimated at 3.45 million tons in 2025, and is expected to reach 4.49 million tons by 2030, at a CAGR of 5.41% during the forecast period (2025-2030).

The COVID-19 hampered the silicone metal market. Many industries that utilize silicone metal, such as automotive, construction, and electronics, experienced decreased demand during the pandemic due to economic downturns, reduced consumer spending, and disruptions in production and supply chains. However, as lockdowns and restrictions eased, industries that utilize silicone metal recovered, and there was increased demand for silicone from infrastructure projects, automotive production, semiconductor manufacturing, and renewable energy installations, which boosted the demand for silicone metals.

Key Highlights

- Surging demand for silicone from the automotive industry, increasing use in the solar industry, and increasing demand for silicones from various other end users are expected to increase the market for silicone metal globally.

- However, volatility in energy costs is hindering the growth of the silicon metal market.

- Several measures to reduce production costs by improving current technologies and increasing demand from the renewable energy sector are expected to create growth opportunities for the market players in the upcoming period.

- The Asia-Pacific holds the highest market share and is likely to dominate the silicon metal market during the forecast period.

Silicon Metal Market Trends

Solar Panels Segment to Dominate the Market

- Silicon, which accounts for about 95% of the modules sold today, is the most extensively used semiconductor material in photovoltaics. In the process of purification, metallurgical silicon can be transformed into high-purity silicon that is used to make semiconductors and solar cells. Therefore, it is suitable for the manufacture of photovoltaic cells.

- Solar energy is one of the largest and fastest-growing sectors worldwide. The sector is responsible for nearly two-thirds of global net energy capacity, according to the International Energy Agency.

- According to the data published by the International Energy Agency (IEA), in 2022, solar PV production increased by a record 270 TWh, which increased by 26%, reaching almost 1300 TWh. It demonstrated the most considerable absolute generation growth of all renewable technologies in 2022, surpassing wind for the first time in history.

- The United States included generous new funding for solar PV in the Inflation Reduction Act (IRA) introduced in 2022. Investment and production tax credits will likely significantly boost the growth of PV capacity and supply chains.

- According to the data published by the International Energy Agency (IEA), in 2022, Brazil added almost 11 gigawatts of solar PV capacity, doubling its growth rate for 2021. In view of the continued demand for renewable energy from industry and power retailers, deployment is projected to be maintained at this level over the medium term.

- According to the data published by the Ministry of New and Renewable Energy (MNRE), India held the fourth position in solar PV deployment worldwide as of the end of 2022. The Cumulative installed capacity of solar power reached around 7.2 GW as of November 2022. Today, India's solar tariffs are very competitive, and grid parity has been achieved.

- The developments mentioned above are expected to drive the market for silicone metal in the solar industry through the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific, particularly China, is the largest producer of silicone metal globally. The region benefits from abundant reserves of raw materials like quartz and coal, as well as access to low-cost labor, which supports the establishment of large-scale silicon metal production facilities.

- The most critical applications of silicon metal are silicone adhesives, sealants, lubricants, chemicals, and other substances, as well as aluminum alloys. The automotive, building and construction, industrial, and other end-user sectors are the primary uses of these products.

- The production and sales of new energy vehicles increased significantly in China, with the number of units sold reaching 7.22 million by 2022, representing 64 % of all EV sales worldwide.

- The market is projected to be driven by the government's promotion of EVs, hybrids, and fuel-cell vehicles in the forecast period. The rising demand for electric vehicles in this country increases the need for semiconductors, aluminum alloys, and silicon adhesives.

- According to the report released by the China Association of Automobile Manufacturers (CAAM), in 2022, China exported 3.11 million vehicles, including 2.53 million passenger cars and 580,000 commercial vehicles, an increase of 54.4 % compared to 2021.

- The top global solar PV manufacturing companies, such as JinkoSolar, Trina Solar, and JA Solar, are headquartered in China. Solar cell manufacturing in China has been increasing significantly in the past two years. According to the data published by the International Energy Agency (IEA), with 100 GW capacity of solar PV added in 2022, almost 60% more than in 2021, China continues to lead in terms of solar PV capacity additions.

- Investment in the manufacture of mobile phones, laptops, and other electrical appliances is a significant area for investment in China. In order to meet the upcoming increase in demand, large manufacturers from around the world have invested substantial capital into China's market.

- Due to these factors, Asia-Pacific region China is expected to dominate the silicon metal market.

Silicon Metal Industry Overview

The silicon metal market is partially consolidated. The major players (not in any particular order) include Hoshine Silicon Industry Co., Ltd, Ferroglobe, Elkem ASA, Dow, and Wacker Chemie AG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Surging Demand from the Automotive Industry

- 4.1.2 Increasing Use in the Solar Industry

- 4.1.3 Increasing Demand for Silicones from Different End Users

- 4.2 Restraints

- 4.2.1 Volatility in Energy Costs

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Product Type

- 5.1.1 Metallurgy Grade

- 5.1.2 Chemical Grade

- 5.2 Application

- 5.2.1 Aluminum Alloys

- 5.2.2 Semiconductors

- 5.2.3 Solar Panels

- 5.2.4 Silicone Derivatives

- 5.2.5 Other Applications (Construction and Infrastructure)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Indonesia

- 5.3.1.7 Thailand

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 Spain

- 5.3.3.5 France

- 5.3.3.6 Turkey

- 5.3.3.7 Russia

- 5.3.3.8 NORDIC

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Qatar

- 5.3.5.5 Egypt

- 5.3.5.6 UAE

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Anyang Huatuo Metallurgy Co., Ltd.

- 6.4.2 Dow

- 6.4.3 Elkem ASA

- 6.4.4 Ferroglobe

- 6.4.5 Hoshine Silicon Industry Co., Ltd.

- 6.4.6 Liasa

- 6.4.7 Minasligas

- 6.4.8 Mississipi Silicon

- 6.4.9 PCC SE

- 6.4.10 RIMA INDUSTRIAL

- 6.4.11 RusAL

- 6.4.12 Shin-Etsu Chemical Co., Ltd.

- 6.4.13 Wacker Chemie AG

- 6.4.14 Zhejiang kaihua yuantong silicon industry co. LTD.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Efforts to Reduce the Cost of Production by Innovating the Existing Technology

- 7.2 Increasing Demand from Renewable Energy Sector