|

시장보고서

상품코드

1686658

수력 발전 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Hydropower - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

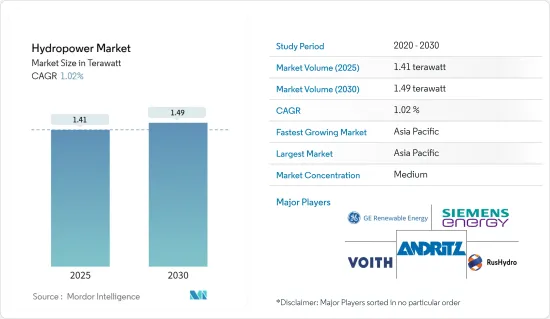

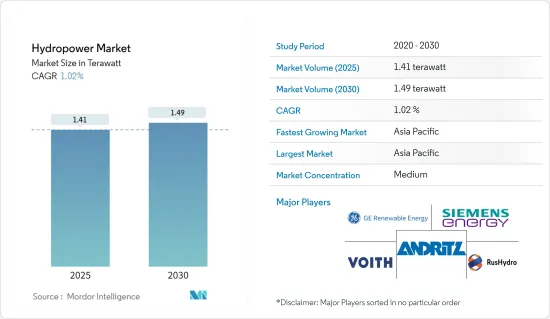

수력 발전 시장 규모는 2025년에 1.41테라와트로 추정되고, 2030년에는 1.49테라와트에 달할 것으로 예측되며, 예측기간 중(2025-2030년)의 CAGR은 1.02%를 나타낼 전망입니다.

주요 하이라이트

- 중기적으로는 정부 지원으로 뒷받침되는 새로운 수력 발전 프로젝트의 증가와 안정적인 전력 수요 증가와 같은 요인이 예측 기간 동안 시장을 주도 할 것으로 예상됩니다.

- 한편, 수력 발전 프로젝트의 부정적인 환경 영향은 예측 기간 동안 시장 성장을 저해 할 가능성이 높습니다.

- 그럼에도 불구하고 수력 발전을 늘리기위한 새로운 기술 트렌드는 향후 수력 발전 시장에 상당한 기회를 제공 할 것으로 예상됩니다.

- 아시아태평양은 이 지역의 여러 국가에서 수력 발전 프로젝트에 대한 투자가 증가함에 따라 시장을 지배할 것으로 예상됩니다.

수력 발전 시장 동향

시장을 지배할 대규모 수력 발전(100MW 이상) 부문

- 대규모 수력 발전은 대형 수력 터빈을 구동하는 데 사용되는 흐르는 물에서 파생되는 재생 에너지 발전의 한 형태입니다. 도시를 위한 대량의 수력 발전을 위해서는 발전, 관개, 가정 또는 산업용으로 나중에 방출할 물을 저장하고 조절하기 위해 호수, 저수지, 댐이 필요합니다. 대규모 수력 발전 시설은 쉽게 켜고 끌 수 있기 때문에 수력 발전은 하루 종일 피크 전력 수요를 충족하는 데 다른 에너지원보다 더 신뢰할 수 있게 되었습니다. 기존의 수력 발전 댐, 양수 발전, 유수 발전은 전 세계적으로 다양한 유형의 대규모 수력 발전소입니다

- 국제재생가능에너지기구에 따르면 2022년에는 세계에서 약 75억 5,000만 달러가 수력발전에 투자되었지만, 2021년에는 약 78억 3,000만 달러가 투자 새로운 수력 발전 용량에 대한 끊임없는 투자는 세계적으로 대규모 수력 발전 부문의 성장을 견인하고 있습니다.

- 중국, 브라질, 미국, 캐나다, 인도, 일본이 전 세계에서 대규모 수력 발전 프로젝트를 진행하는 주요 국가입니다.

- 주요 수력 발전 국가 외에도 동남아시아 지역의 소규모 국가들도 대규모 수력 발전 분야에서 빠르게 발전하고 있습니다.

- 예를 들어 라오스 정부는 총 용량 195만kW의 12개 수력발전 댐 프로젝트를 완성할 계획을 발표했습니다.

- 2022년 5월, 드랙스 그룹 PLC는 클루아찬 발전소에 6억 1,600만 달러를 투자했습니다.의 용량을 두배로 늘릴 계획으로, 2024년에 현지에서의 작업을 개시합니다.

- 따라서 위에서 언급 한 요인에 따라 대규모 수력(100MW 이상) 부문은 예측 기간 동안 세계의 수력 발전 시장을 지배 할 것으로 예상됩니다.

아시아태평양이 시장을 독점

- 아시아태평양 지역은 최근 수년간 수력 발전 시장을 지배해 왔으며, 예측 기간 동안에도 그 우위를 유지할 것으로 보입니다.

- 중국은 2060년까지 탄소 중립을 달성하고 2025년까지 석탄 소비를 최대화하겠다는 계획을 발표했습니다.

- 2023년 5월, 중국의 국가개발개혁위원회(NDRC)는 서유럽자치구에 약 84억 3,000만 달러의 자본지원을 받는 새로운 수력발전소의 건설을 승인한다고 발표했습니다.

- 게다가 2023년 2월에는 인도가 아르나찰 프라데시주의 국가수력발전공사(NHPC)의 디반수력발전 프로젝트(2,880메가와트(MW))에 39억 달러를 투자하는 것을 승인하고 있으며, 이 프로젝트의 건설에는 9년이 걸릴 것으로 추정되고 있습니다.

- 따라서 위에서 언급 한 요인에 따라 아시아태평양 지역은 예측 기간 동안 세계의 수력 발전 시장을 지배 할 것으로 예상됩니다.

수력 발전 산업 개요

수력 발전 시장은 반통합 시장입니다. 주요 기업으로는 GE Renewable Energy, Siemens Energy AG, Andritz AG, Voith GmbH & Co.KGaA, PJSC RusHydro 등이 있습니다.

2022년 3월, 안드리츠와 태국 전력청(EGAT)은 태국 및 주변 동남아시아 국가에서 수력 발전 프로젝트의 사업 기회를 공동으로 모색하고 확대하기 위한 양해각서(MoU)를 체결했습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 소개

- 설치 용량(GW) 및 예측(-2029년)

- 최근 동향과 개발

- 정부의 규제와 정책

- 시장 역학

- 성장 촉진요인

- 안정적인 전기에 대한 수요 증가

- 수력 발전에 대한 정부 지원 증가

- 억제요인

- 수력 발전 프로젝트의 부정적인 환경적 결과

- 성장 촉진요인

- 공급망 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 세분화

- 규모

- 대규모 수력 발전(100MW 이상)

- 소규모 수력 발전(10MW 미만)

- 기타 규모(10-100MW)

- 지역

- 북미

- 미국

- 캐나다

- 기타 북미

- 유럽

- 독일

- 프랑스

- 영국

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 프로파일

- GE Renewable Energy

- Siemens Energy AG

- Andritz AG

- Voith GmbH & Co. KGaA

- China Yangtze Power Co. Ltd

- PJSC RusHydro

- Electricite de France SA(EDF)

- Iberdrola SA

- 시장 랭킹 및 점유율 분석

제7장 시장 기회와 앞으로의 동향

- 수력 발전 증가를 목표로 하는 새로운 기술 동향

The Hydropower Market size is estimated at 1.41 terawatt in 2025, and is expected to reach 1.49 terawatt by 2030, at a CAGR of 1.02% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, gactors such as the increasing number of new hydropower projects backed by government support and the rising demand for reliable electricity are expected to drive the market during the forecast period.

- On the other hand, negative environmental consequences of hydropower projects are likely to hinder the market growth during the forecast period.

- Nevertheless, emerging technological trends aimed at increasing hydropower generation are expected to provide significant opportunities for the hydropower market in the coming years.

- Asia-Pacifc is estimated to dominate the market due to increasing investment in hydropower projects across the various countries in the region.

Hydropower Market Trends

The Large Hydropower (Greater Than 100 MW) Segment to Dominate the Market

- Large-scale hydropower is a form of renewable energy generation derived from flowing water, which is used to drive large water turbines. In order to generate large amounts of hydroelectricity for cities, lakes, reservoirs, and dams are needed to store and regulate water for later release for power generation, irrigation, and domestic or industrial use. Since large-scale hydropower facilities can easily be turned on and off, hydropower has become more reliable than most other energy sources for meeting peak electricity demands throughout the day.

- Conventional hydroelectric dams, pumped storage, and run-of-the-river are the different types of large-scale hydropower plants worldwide.

- As per International Renewable Energy Agency, around USD 7.55 billion was invested in hydropower globally in 2022, whereas around USD 7.83 billion was invested in 2021. The constant investment in new hydropower capacity globally drives growth in large hydropower segments. Also, the average cost of large hydropower installation is comparatively low.

- China, Brazil, the United States, Canada, India, and Japan are the major countries in the deployment of large-scale hydropower projects across the world. Factors such as a shift towards cleaner energy sources and plans to increase the share of renewable energy in the total power generation mix across all the major developed and emerging economies across the world are expected to drive the large hydropower segment during the forecast period.

- In addition to the major hydropower countries, smaller countries from the Southeast Asia region are also moving forward rapidly in the large hydropower development. Increasing demand for energy to boost the Mekong economy has attracted riparian countries' keen interest in hydropower development. Over the last few decades, this has been evidenced by extensive investment in hydropower projects across the region.

- For instance, the Lao government announced that it plans to complete 12 hydropower dam projects with a total capacity of 1,950 MW. Hydropower development is a central priority of the Lao government's plan to export around 20,000 MW of electricity to its neighboring countries by 2030.

- In May 2022, Drax Group PLC invested USD 616 million in the Cruachan power station. The company planned to add 600 MW of underground pumped storage hydropower capacity to the Cruachan power station. The company plans to double the Cruachan facility's capacity by 2030, and work on-site begins in 2024. The company plans to hollow out a cavern in Ben Cruachan and excavate around two million tons of rock to house the power station and related infrastructure.

- Therefore, based on the factors mentioned above, the large hydropower (greater than 100 MW) segment is expected to dominate the global hydropower market during the forecast period.

Asia-Pacific to Dominate the Market

- The Asian-Pacific region has dominated the hydropower market in recent years, and it is likely to maintain its dominance during the forecast period. According to International Renewable Energy Agency, as of 2022, China is the global leader in the hydropower market, with an installed capacity of 413.5 GW.

- China announced its plan to become carbon neutral by 2060 and peak coal consumption by 2025. This led to increased investment in the renewable sector, and in 2022, around 22.5 GW of new hydropower was installed.

- In May 2023, the National Development and Reform Commission (NDRC) of China announced to approval construction of a new hydropower plant in the Xizang Autonomous region which will have capital backing of around USD 8.43 billion. The annual average electricity volume produced by the plant will surpass 11.28 billion kilowatt-hours.

- Further, in February 2023, India approved a USD 3.9 billion investment for the 2,880 megawatts (MW) Dibang hydropower project in Arunachal Pradesh, National Hydroelectric Power Corporation (NHPC), and it is estimated that this project will take nine years to build.

- Therefore, based on the factors mentioned above, Asia-Pacific is expected to dominate the global hydropower market during the forecast period.

Hydropower Industry Overview

The hydropower market is semi-consolidated. Some of the major players include (not in particular order) GE Renewable Energy, Siemens Energy AG, Andritz AG, Voith GmbH & Co. KGaA, and PJSC RusHydro, among others.

In March 2022, ANDRITZ and the Electricity Generating Authority of Thailand (EGAT) signed a Memorandum of Understanding (MoU) to jointly explore and expand business opportunities for hydropower projects in Thailand and surrounding Southeast Asian countries.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Installed Capacity and Forecast in GW, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Rising Demand for Reliable Electricity

- 4.5.1.2 Increasing Government Support for Hydropower Gneeration

- 4.5.2 Restraints

- 4.5.2.1 Negative Environmental Consequences of Hydropower Projects

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Size

- 5.1.1 Large Hydropower (Greater Than 100 MW)

- 5.1.2 Small Hydropower (Smaller Than 10 MW)

- 5.1.3 Other Sizes (10-100 MW)

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 France

- 5.2.2.3 United Kingdom

- 5.2.2.4 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 South Africa

- 5.2.5.4 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 GE Renewable Energy

- 6.3.2 Siemens Energy AG

- 6.3.3 Andritz AG

- 6.3.4 Voith GmbH & Co. KGaA

- 6.3.5 China Yangtze Power Co. Ltd

- 6.3.6 PJSC RusHydro

- 6.3.7 Electricite de France SA (EDF)

- 6.3.8 Iberdrola SA

- 6.4 Market Ranking/Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Technological Trends Aimed at Increasing Hydropower Generation