|

시장보고서

상품코드

1687127

건설용 복합재료 시장 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)Construction Composite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

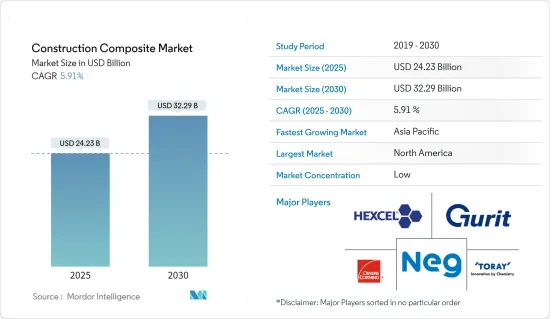

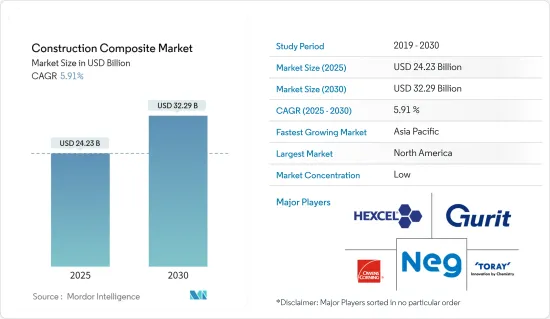

건설용 복합재료 시장 규모는 2025년에 242억 3,000만 달러로 추정되고, 예측 기간인 2025-2030년 CAGR 5.91%로 성장할 전망이며, 2030년에는 322억 9,000만 달러에 달할 것으로 예측되고 있습니다.

COVID-19는 팬데믹이 국제 무역에 심각한 영향을 미치고 제조, 건축 및 건설을 포함한 여러 산업에 지장을 주었기 때문에 2020년 시장에 부정적인 영향을 미쳤습니다. 그러나 2021년에는 이러한 부문으로부터 시장 수요가 크게 회복되었습니다.

주요 하이라이트

- 중기적으로는 건설용 복합재료의 사용 증가 및 노후화된 콘크리트 구조물의 수복이 시장 성장의 원동력이 되고 있습니다.

- 한편 복합재료의 초기 생산비용 및 시공비용이 높고, 숙련노동자의 부족도 함께 시장의 성장을 방해하고 있습니다.

- 건설용 복합재료의 대량 생산 능력 향상은 향후 몇 년 동안 시장에 기회를 가져올 가능성이 높습니다.

- 북미가 수익면에서 시장을 독점할 것으로 예상되는 반면, 아시아태평양은 예측 기간 동안 가장 높은 CAGR을 나타낼 것으로 예상됩니다.

건설용 복합재료 시장 동향

토목 건설 부문이 시장을 독점

- 토목 건설은 교량, 댐, 도로, 공항, 운하, 철도 인프라 및 관련 구조물의 건설로 구성됩니다.

- 2021년 말에는 중국의 일부 성이 대규모 인프라 프로젝트를 발표했습니다. 중국 남부의 광시 치완족 자치구는, 투자 총액 1,859억 위안(291억 5,000만 달러)의 대형 건설 프로젝트를 발표했습니다. 이러한 프로젝트는 교통, 신에너지, 물류, 기초 인프라 등 많은 부문을 커버하고 있습니다.

- 또한 중국은 도시화를 추진하고 지역경제를 활성화시키는 장기계획의 일환으로 세계 2위 규모를 자랑하는 철도망을 향후 15년간 3분의 1로 확대할 계획입니다. 국유기업인 중국국유철도집단이 발표한 계획에 따르면, 중국은 2035년 말까지 약 20만 km(124,274 마일)의 철도를 부설하는 것을 목표로 하고 있으며, 그 중에는 약 7만 km의 고속철도도 포함되어 있습니다.

- 독일에서는 교통 및 디지털 인프라부가 전기모빌리티, 전기자동차 충전 인프라의 자동화 및 네트워크화 운전 등의 미래 기술에 3억 4,872만 달러를 투자할 계획입니다. 또 슈발름슈타트와 헤센주 중부 옴타르 인터체인지를 연결하는 A49 고속도로 프로젝트에도 착수했습니다. 이로 인해 복합재료의 소비량이 증가할 것으로 예상됩니다.

- 슈발름슈타트-옴타르 프로젝트는 관민 파트너십 모델에 근거하고 있으며, 투자액은 8억 1,368만 달러입니다. 93km의 도로로 구성된 이 공사는 2024년 3분기에 완공될 예정입니다. 이러한 대규모 철도 및 도로 건설 프로젝트가 예측 기간 중 건설용 복합재료의 수요를 견인할 가능성이 있습니다.

- 미국 인구 조사국에 따르면, 미국에서 실시된 고속도로와 도로 건설의 연간 금액은 2020년의 1억 232만 달러에 대해, 2021년은 1억 68만 달러였습니다.

- 캐나다에서는 '캐나다에 대한 투자' 계획의 일환으로 정부는 2028년까지 국내 주요 인프라 개발에 약 1,400억 달러를 투자할 계획을 발표했습니다.

시장을 독점하는 북미

- 북미에서는 미국, 캐나다, 멕시코 등의 나라에서 건설 부문이 성장하고 있기 때문에 건설용 복합재료의 이용이 증가하고 있습니다.

- 북미는 건설용 복합재료의 최대 소비 시장 중 하나입니다. 미국은 세계 최대의 건설 산업 중 하나입니다. 2021년 연중 건설 지출은 1조 5,903억 7,000만 달러에 달했으며, 2020년의 1조 4,692억 달러를 8.2% 웃돌았습니다.

- 미국 인구조사국에 따르면 2022년 2월 이 나라 건설지출은 계절조정된 연율 1,704억 달러로 평가되었으며, 1월 수정치인 1조 6,955억 달러를 0.5% 웃돌았습니다. 2021년 2월의 추정치 1조 5,333억 달러를 11.2% 웃돌았습니다.

- 캐나다에서는 최근, 주택 및 상업 부문이 안정된 성장을 이루고 있습니다. 캐나다(보다 구체적으로는 토론토)에서는 최근, 초고층 빌딩의 건설 붐이 일어나고 있습니다. 2025년까지 30동 이상의 초고층 빌딩이 완성될 전망으로, 토론토에서는 또 50동의 초고층 빌딩이 제안 및 계획 단계에 있습니다.

- 또한 '캐나다에 대한 투자 계획'의 일환으로 정부는 2028년까지 국내 인프라 개발에 1,400억 달러 가까이 투자할 계획을 발표하고 있습니다.

건설용 복합재료 산업 개요

세계의 건설용 복합재료 시장은 세분화되어 있습니다. 이 시장의 주요 기업에는 Hexcel Corporation, Owens Corning, Nippon Electric Glass, Toray Industries Inc., Gurit 등이 있습니다.(순부동)

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 건설용 복합재료 사용 증가

- 노후 콘크리트 구조물의 수복

- 성장 억제요인

- 복합재료의 높은 초기 제조 비용 및 설치 비용

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화

- 수지 유형별

- 폴리에스테르 수지

- 비닐에스테르

- 폴리에틸렌

- 폴리프로필렌

- 에폭시 수지

- 기타

- 섬유 유형별

- 탄소 섬유

- 유리 섬유

- 천연 섬유

- 기타 섬유 유형

- 최종 용도 부문별

- 공업용

- 상업

- 주택용

- 민간

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 스페인

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴 및 협정

- 시장 점유율(%)** 및 랭킹 분석

- 주요 기업의 전략

- 기업 프로파일(개요, 재무, 제품 및 서비스, 최근 동향)

- Aegion Corporation

- Exel Composites

- Gurit

- Hexcel Corporation

- Kordsa Teknik Tekstil AS

- Toray Industries Inc.

- Mitsubishi Chemical Corporation

- Nippon Electric Glass Co. Ltd

- Owens Corning

- SGL Carbon

- Teijin Limited

제7장 시장 기회 및 향후 동향

- 건설용 복합재료의 대량 생산 능력 향상

The Construction Composite Market size is estimated at USD 24.23 billion in 2025, and is expected to reach USD 32.29 billion by 2030, at a CAGR of 5.91% during the forecast period (2025-2030).

COVID-19 negatively impacted the market in 2020 as the pandemic severely affected international trade and hampered several industries, including manufacturing, building, and construction. However, in 2021, the market demand from these sectors recovered significantly.

Key Highlights

- Over the medium term, the factors driving the growth of the market studied are the increasing usage of composites in construction applications and the rehabilitation of old concrete structures.

- On the other hand, the high initial production and installation costs of composites, coupled with the inadequacy of skilled labor, are hindering the market's growth.

- Increasing the ability to mass-produce composites in the construction sector will likely create opportunities for the market in the coming years.

- North America is expected to dominate the market in terms of revenue while the Asia-Pacific region is likely to witness the highest CAGR during the forecast period.

Construction Composites Market Trends

Civil Construction Sector to Dominate the Market

- Civil construction comprises the construction of bridges, dams, roads, airports, canals, railway infrastructure, and related structures.

- Toward the end of 2021, several Chinese provinces announced major infrastructure projects. South China's Guangxi Zhuang Autonomous Region unveiled a batch of major construction projects, with a total investment of CNY 185.9 billion (USD 29.15 billion). Those projects cover many sectors, including transportation, new energy, logistics, and basic infrastructure.

- Furthermore, China plans to expand its railway network, which is the second-largest in the world, by one-third in the next 15 years, as part of a long-term plan to propel urbanization and stimulate local economies. According to a plan issued by the state-owned China State Railway Group, China aims to have about 200,000 km (124,274 miles) of railway tracks by the end of 2035, including about 70,000 km of high-speed railways.

- In Germany, the Ministry of Transport and Digital Infrastructure plans to invest USD 348.72 million in future technologies, such as electric mobility or automated and networked driving for electric vehicle charging infrastructure. Also, the country has started working on the A49 highway project connecting Schwalmstadt and the Ohmtal interchange in Central Hesse. This, in turn, is expected to increase the consumption of composite materials.

- The Schwalmstadt-Ohmtal project is based on a public-private partnership model with an investment of USD 813.68 million. The construction, which comprises 93 km of road, is expected to be completed in the third quarter of 2024. These massive railway and road construction projects may drive the demand for construction composites during the forecast period.

- According to US Census Bureau, annual value of highway and street construction put in place of United states, in 2021 accounted for USD 100.68 million, compared to USD 102.32 million in 2020.

- In Canada, as part of the "Investing in Canada" plan, the government announced plans to invest nearly USD 140 billion in major infrastructure developments in the country by 2028.

North America Region to Dominate the Market

- In North America, the utilization of construction composites is increasing due to the growing construction sector in countries such as the United States, Canada, and Mexico.

- The North American region is one of the largest consumption markets for construction composites. The United States has one of the world's largest construction industries. In the full year 2021, construction spending amounted to USD 1,590.37 billion, 8.2% above USD 1,469.2 billion in 2020, thereby increasing the consumption of construction composites from various construction applications.

- According to the US Census Bureau, during February 2022, the construction spending in the country was estimated at a seasonally adjusted annual rate of USD 1704.4 billion, 0.5% more than the revised January estimate of USD 1,695.5 billion. Moreover, the February 2022 estimation is 11.2% more than the February 2021 estimate of USD 1,533.3 billion. During the first two months of 2022, construction spending amounted to USD 237.8 billion, 10.4% percent above USD 215.4 billion for the same period in 2021.

- In Canada, the residential and commercial sectors have been witnessing steady growth in the recent past. There has been a boom in the construction of skyscrapers in Canada (more specifically in Toronto) in recent times. Over 30 high-rise buildings are expected to be completed by 2025, and another 50 such buildings are in the proposal and planning phases in Toronto.

- Moreover, as part of the ''Investing in Canada Plan'', the government has announced plans to invest nearly USD 140 billion in infrastructure developments in the country by 2028.

Construction Composites Industry Overview

The global construction composite market is fragmented. Some major players in the market (in no particular order) include Hexcel Corporation, Owens Corning and Nippon Electric Glass Co. Ltd., Toray Industries Inc., and Gurit.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Use of Composites in Construction Applications

- 4.1.2 Rehabilitation of Old Concrete Structures

- 4.2 Restraints

- 4.2.1 High Initial Production and Installation Costs of Composites

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Revenue)

- 5.1 Resin Type

- 5.1.1 Polyester Resin

- 5.1.2 Vinyl Ester

- 5.1.3 Polyethylene

- 5.1.4 Polypropylene

- 5.1.5 Epoxy Resin

- 5.1.6 Other Resin Types

- 5.2 Fiber Type

- 5.2.1 Carbon Fibers

- 5.2.2 Glass Fibers

- 5.2.3 Natural Fibers

- 5.2.4 Other Fiber Types

- 5.3 End-use Sector

- 5.3.1 Industrial

- 5.3.2 Commercial

- 5.3.3 Housing

- 5.3.4 Civil

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) ** / Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles (Overview, Financials, Products and Services, and Recent Developments)

- 6.4.1 Aegion Corporation

- 6.4.2 Exel Composites

- 6.4.3 Gurit

- 6.4.4 Hexcel Corporation

- 6.4.5 Kordsa Teknik Tekstil AS

- 6.4.6 Toray Industries Inc.

- 6.4.7 Mitsubishi Chemical Corporation

- 6.4.8 Nippon Electric Glass Co. Ltd

- 6.4.9 Owens Corning

- 6.4.10 SGL Carbon

- 6.4.11 Teijin Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Ability to Mass Produce Composites in the Construction Sector