|

시장보고서

상품코드

1687130

미국의 화물 및 물류 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)United States Freight and Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

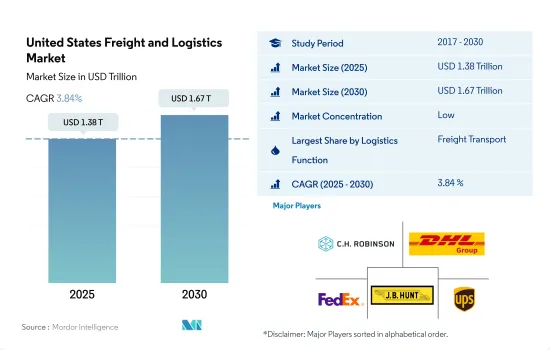

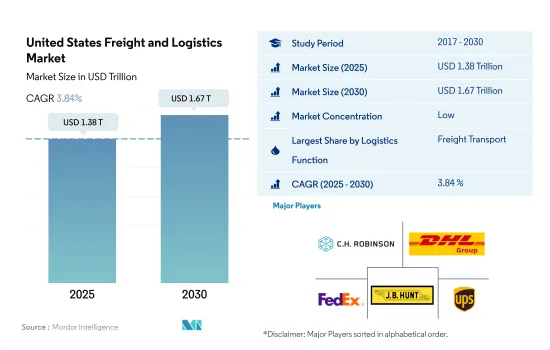

미국의 화물 및 물류 시장 규모는 2025년 1조 3,800억 달러로 예상되며, 2030년에는 1조 6,700억 달러에 이를 것으로 예측되며, 예측 기간 중(2025-2030년) CAGR 3.84%로 성장할 전망입니다.

미국은 혁신과 전략적 파트너십으로 번영

- 2024년 4월, UPS는 USPS와의 대규모 항공화물 계약을 발표하고 현재 진행 중인 파트너십을 심화시켰습니다. 단기간의 전환기간을 거쳐 UPS는 USPS의 주요 항공화물 제공업체가 되어 USPS의 전국 항공화물의 대부분을 감독하게 됩니다. 게다가 2023년 11월 UPS는 미국 지상 소포와 SurePost 납품의 연료 충전을 50 베이시스 포인트 인상하여 15.25%로 늘렸습니다. 동시에 OnTrac은 2024년 6.2%의 운임 가격 인상을 실시했으며, 운송 거리가 짧을수록 운임이 저렴해지는 단계제를 채택했습니다.

- 인프라 개발을 강화하기 위해 정부는 초당파 인프라법(BIL)하에 고속도로 구상에 3,500억 달러를 할당하고 프로젝트는 2026년 9월 30일까지 연장되었습니다. 2022년부터 2026년까지 BIL은 도로, 교량, 대량 수송 기관, 수도 시스템, 회복력 강화 방안, 광대역 서비스 등 다양한 인프라 부문에 대한 연방 투자를 위해 5,500억 달러를 배정합니다. 2024년 11월까지 동 정부는 BIL 하에 5,680억 달러 이상을 지출하고 66,000건 이상의 프로젝트에 자금을 제공했습니다.

미국 화물 및 물류 시장 동향

미국은 인프라와 공급망 투자가 견인해, 지역 GDP의 86%로 시장을 이끕니다.

- 2024년 9월 미국 운수부 산하 FAA는 519개 프로젝트에 19억 달러의 보조금을 할당했습니다. 이 프로젝트는 48 주, 괌, 푸에르토리코 및 기타 영토에 걸쳐 있으며, 모두 공항 개선 프로그램(AIP)의 일부입니다. 또한 2023년 추가 재량 보조금으로 2억 6,900만 달러가 미국 내 56개 공항에서 62개 프로젝트를 지원합니다. 이 경쟁 이니셔티브는 미국의 공항 시스템을 강화하기 위해 공항 소유자와 운영자를 지원합니다. 최대 규모가 되는 이 제5회 AIP 보조금 사이클은 공항의 안전성과 지속가능성 향상부터 소음 경감에 이르기까지 다양한 프로젝트에 자금이 제공됩니다. 보조금은 규모에 관계없이 미국 전역의 공항을 대상으로 합니다.

- 인프라 개발과 전자상거래 붐으로 인해 운수 및 창고 부문은 고용 급증이 예상되고 있습니다. 노동통계국(BLS)은 2022년부터 2032년까지 연간 성장률을 0.8%로 예측하고 있으며, 이는 약 57만 명의 신규 고용에 해당합니다. 주목할 점은 창고 및 보관업과 함께 택배 및 배달업이 고용 증가의 약 80%를 견인할 것으로 예상되고 있다는 점입니다.

2022년 미국은 80개국에서 628만 B/D의 원유를 수입했으며 계속해서 원유 순수입국이었습니다.

- 대통령 선거를 앞둔 2024년 10월까지 미국 가솔린 가격은 3년 내에 갤런당 3달러 미만으로 떨어질 것으로 예상됐습니다. 수요감퇴와 원유가격 하락을 주인으로 하는 이 예상되는 연료가격 하락은 인플레이션 압력에 시달리는 소비자들에게 휴식을 제공합니다. 2024년 9월 현재 정규 가솔린의 평균 가격은 1갤런 3.25달러로 전월 대비 19센트, 작년 동시기 대비 58센트 하락했습니다.

- 미국 에너지 정보국(EIA)의 발표에 따르면 2024년 원유 가격은 2023년 수준을 반영하여 안정적으로 추이했으나 2025년 하락할 것으로 예상됩니다. 미국은 2023년에 가동 가능한 정화 능력을 강화했으며, 그 후 2년 동안 석유 제품의 가격 압력이 완화될 것으로 예상됩니다. 한편, 쿠웨이트 및 중동의 다른 지역에서는 국제 정화 능력을 강화하고 있으며, 가솔린과 디젤 세계의 가격 압력을 더욱 완화하고 있습니다. 게다가 2024년 크랙 스프레드 축소는 2024년과 2025년 평균 소매 연료 가격 인하로 이어질 수 있으며, 2024년에는 1갤런당 USD 3.36, 2025년에는 갤런당 USD 3.24가 될 것으로 예상됩니다.

미국 화물 및 물류 산업 개요

미국의 화물 및 물류 시장은 단편화되고 있으며, 이 시장의 주요 기업은 CH Robinson, DHL Group, FedEx, JB Hunt Transport, Inc. and United Parcel Service of America, Inc.(UPS)의 5개 기업입니다(알파벳순).

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트·지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 인구동태

- 경제 활동별 GDP 분포

- 경제 활동별 GDP 성장률

- 인플레이션율

- 경제성과 및 프로파일

- 전자상거래 산업의 동향

- 제조업의 동향

- 운수·창고업의 GDP

- 수출 동향

- 수입 동향

- 연료 가격

- 트럭 운송 비용

- 유형별 트럭 보유 대수

- 물류 실적

- 주요 트럭 공급업체

- 모달 점유율

- 해상화물 능력

- 정기선의 접속성

- 기항지와 퍼포먼스

- 운임 동향

- 화물 톤수의 동향

- 인프라

- 규제 프레임워크(도로 및 철도)

- 미국

- 규제 프레임워크(해상 및 항공)

- 미국

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 최종 사용자 산업

- 농업, 어업, 임업

- 건설업

- 제조업

- 석유 및 가스, 광업, 채석업

- 도매·소매업

- 기타

- 물류 기능

- 쿠리어, 익스프레스, 파셀(CEP)

- 목적지별

- 국내

- 국제

- 화물

- 수송 모드별

- 항공

- 해상 및 내륙 수로

- 기타

- 화물

- 수송수단별

- 항공

- 파이프라인

- 철도

- 도로

- 해상 및 내륙 수로

- 창고 보관

- 온도 관리별

- 온도 관리 없음

- 온도 관리

- 기타 서비스

- 쿠리어, 익스프레스, 파셀(CEP)

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- CH Robinson

- Deutsche Bahn AG(including DB Schenker)

- DHL Group

- DSV A/S(De Sammensluttede Vognmaend af Air and Sea)

- Expeditors International of Washington, Inc.

- FedEx

- GXO Logistics

- JB Hunt Transport, Inc.

- Kuehne Nagel

- NFI Industries

- Penske Corporation(including Penske Logistics)

- United Parcel Service of America, Inc.(UPS)

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Porter's Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(시장 성장 촉진요인, 억제요인, 기회)

- 기술의 진보

- 정보원과 참고문헌

- 도표 목록

- 주요 인사이트

- 데이터 팩

- 용어집

- 환율

The United States Freight and Logistics Market size is estimated at 1.38 trillion USD in 2025, and is expected to reach 1.67 trillion USD by 2030, growing at a CAGR of 3.84% during the forecast period (2025-2030).

United States thrives with tech innovations and strategic partnerships

- In April 2024, UPS announced a major air cargo contract with USPS, deepening their ongoing partnership. After a brief transition, UPS will become the primary air cargo provider for USPS, overseeing most of its air shipments nationwide. Additionally, in November 2023, UPS raised its fuel surcharge for US ground parcel and SurePost deliveries by 50 basis points, bringing it to 15.25%. At the same time, OnTrac implemented a 6.2% tariff rate increase for 2024, adopting a tiered system where shorter hauls are charged less than longer ones.

- To bolster infrastructure development, the government allocated USD 350 billion for highway initiatives under the Bipartisan Infrastructure Law (BIL), with projects extending until September 30, 2026. Spanning from 2022 to 2026, BIL earmarked a substantial USD 550 billion for federal investments in diverse infrastructure sectors, including roads, bridges, mass transit, water systems, resilience efforts, and broadband services. By November 2024, the administration had disbursed over USD 568 billion under the BIL, funding more than 66,000 projects and awards.

United States Freight and Logistics Market Trends

United States leads regional GDP with 86% contribution, driven by infrastructure and supply chain investments

- In September 2024, the FAA, under the US Department of Transportation, allocated USD 1.9 billion in grants for 519 projects. These projects span 48 states, Guam, Puerto Rico, and other territories, all part of the Airport Improvement Program (AIP). Additionally, USD 269 million in Supplemental Discretionary Grants for 2023 will back 62 projects at 56 U.S. airports. This competitive initiative aids airport owners and operators in enhancing the U.S. airport system. Marking its largest round yet, this fifth AIP grant cycle funds diverse projects, from airport safety and sustainability upgrades to noise reduction. The grants cater to airports nationwide, regardless of size.

- With infrastructure development and the e-commerce boom, the transportation and storage sector is set for a job surge. The Bureau of Labor Statistics (BLS) projects a 0.8% annual growth rate from 2022 to 2032, translating to nearly 570,000 new jobs. Notably, the couriers and messengers industry, alongside warehousing and storage, is expected to drive about 80% of this job growth.

In 2022, the U.S. imported 6.28 million bpd of crude oil from 80 countries, continuing its streak as a net crude oil importer

- By October 2024, just ahead of the presidential election, U.S. gasoline prices were poised to dip below USD 3 a gallon for the first time in over three years. This anticipated drop in fuel prices, primarily driven by waning demand and declining oil prices, offers a much-needed respite to consumers grappling with inflationary pressures. As of September 2024, regular gas averaged USD 3.25 a gallon, marking a 19-cent decrease from the previous month and a 58-cent drop from the same time last year.

- Crude oil prices, as per the U.S. Energy Information Administration (EIA), remained stable in 2024, mirroring 2023 levels, before expected downturn in 2025. The U.S. bolstered its operable refining capacity in 2023, a move expected to ease price pressures on oil products in the subsequent two years. Meanwhile, Kuwait and other parts of the Middle East are ramping up international refining capacities, further alleviating global price pressures on gasoline and diesel. Additionally, narrowing crack spreads in 2024 could translate to reduced average retail fuel prices in both 2024 and 2025, with projections of USD 3.36/gal in 2024 and USD 3.24/gal in 2025.

United States Freight and Logistics Industry Overview

The United States Freight and Logistics Market is fragmented, with the major five players in this market being C.H. Robinson, DHL Group, FedEx, J.B. Hunt Transport, Inc. and United Parcel Service of America, Inc. (UPS) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Demographics

- 4.2 GDP Distribution By Economic Activity

- 4.3 GDP Growth By Economic Activity

- 4.4 Inflation

- 4.5 Economic Performance And Profile

- 4.5.1 Trends in E-Commerce Industry

- 4.5.2 Trends in Manufacturing Industry

- 4.6 Transport And Storage Sector GDP

- 4.7 Export Trends

- 4.8 Import Trends

- 4.9 Fuel Price

- 4.10 Trucking Operational Costs

- 4.11 Trucking Fleet Size By Type

- 4.12 Logistics Performance

- 4.13 Major Truck Suppliers

- 4.14 Modal Share

- 4.15 Maritime Fleet Load Carrying Capacity

- 4.16 Liner Shipping Connectivity

- 4.17 Port Calls And Performance

- 4.18 Freight Pricing Trends

- 4.19 Freight Tonnage Trends

- 4.20 Infrastructure

- 4.21 Regulatory Framework (Road and Rail)

- 4.21.1 United States

- 4.22 Regulatory Framework (Sea and Air)

- 4.22.1 United States

- 4.23 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes 1. Market value in USD for all segments 2. Market volume for select segments viz. freight transport, CEP (courier, express, and parcel) and warehousing & storage 3. Forecasts up to 2030 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Logistics Function

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.2.1.1 By Destination Type

- 5.2.1.1.1 Domestic

- 5.2.1.1.2 International

- 5.2.2 Freight Forwarding

- 5.2.2.1 By Mode Of Transport

- 5.2.2.1.1 Air

- 5.2.2.1.2 Sea and Inland Waterways

- 5.2.2.1.3 Others

- 5.2.3 Freight Transport

- 5.2.3.1 By Mode Of Transport

- 5.2.3.1.1 Air

- 5.2.3.1.2 Pipelines

- 5.2.3.1.3 Rail

- 5.2.3.1.4 Road

- 5.2.3.1.5 Sea and Inland Waterways

- 5.2.4 Warehousing and Storage

- 5.2.4.1 By Temperature Control

- 5.2.4.1.1 Non-Temperature Controlled

- 5.2.4.1.2 Temperature Controlled

- 5.2.5 Other Services

- 5.2.1 Courier, Express, and Parcel (CEP)

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 C.H. Robinson

- 6.4.2 Deutsche Bahn AG (including DB Schenker)

- 6.4.3 DHL Group

- 6.4.4 DSV A/S (De Sammensluttede Vognmaend af Air and Sea)

- 6.4.5 Expeditors International of Washington, Inc.

- 6.4.6 FedEx

- 6.4.7 GXO Logistics

- 6.4.8 J.B. Hunt Transport, Inc.

- 6.4.9 Kuehne+Nagel

- 6.4.10 NFI Industries

- 6.4.11 Penske Corporation (including Penske Logistics)

- 6.4.12 United Parcel Service of America, Inc. (UPS)

7 KEY STRATEGIC QUESTIONS FOR FREIGHT AND LOGISTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (Market Drivers, Restraints & Opportunities)

- 8.1.5 Technological Advancements

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 8.7 Currency Exchange Rate

샘플 요청 목록