|

시장보고서

상품코드

1687134

태국의 비료 시장 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)Thailand Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

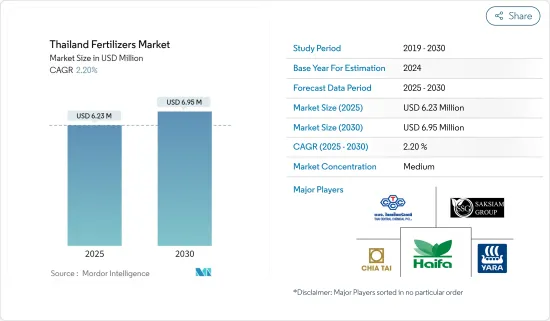

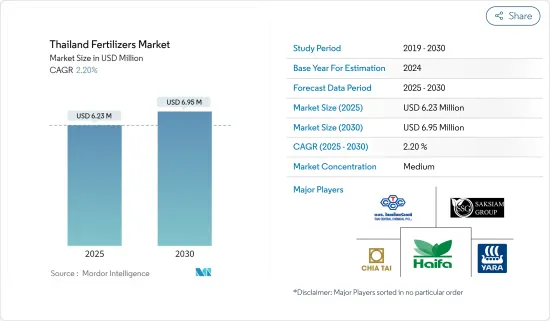

태국의 비료 시장 규모는 2025년에 623만 달러로 추정되고, 예측 기간인 2025-2030년 CAGR 2.2%로 성장할 전망이며, 2030년에는 695만 달러에 달할 것으로 예측되고 있습니다.

태국의 비료 시장은 증가하는 식량 수요를 충족시키기 위해 농업 생산성을 향상시킬 필요성이 증가하고 있기 때문에 확대되고 있습니다. 옥수수, 카사바, 사탕수수, 쌀 등의 주요 작물은 대량의 양분 투입을 필요로 하여 비료 수요를 견인하고 있습니다. 질소 비료가 태국 시장을 독점하고 있는데, 이는 주로 질소 결핍 토양 및 벼농사의 보급에 의한 것입니다. 요소가 가장 많이 사용되는 비료입니다. 유기농의 면적이 확대되고 있음에도 불구하고 농업 종사자들은 바이오 비료 및 유기 비료와 관련된 과제를 이유로 화학 합성비료 및 화학비료를 즐겨 사용하고 있습니다.

비료 보조금 및 소프트 론을 통한 정부 지원은 시장 역학에 큰 영향을 미쳤습니다. 2024년에는 기존의 농업 종사자 수당 제도 대신 새로운 비료 보조금 제도가 도입되어 1라이 당 29.7달러(20라이 또는 3.2 헥타르까지)의 현금 지원이 이루어졌습니다. 정부는 전년도에 이 프로그램에 17억 달러를 할당했습니다. 이러한 지원 확대로 향후 수년간 비료 소비가 촉진되고 농업 종사자의 생산성이 향상될 것으로 예상됩니다.

태국의 비료 시장 동향

농업 생산성 향상의 필요성

태국의 농업 생산성은 농지 면적이 안정되어 있음에도 불구하고 최근 낮아지고 있습니다. FAOSTAT의 데이터에 따르면 콩류의 수확량은 2021년 953.2kg/ha에서 2022년 952.4kg/ha로 감소했습니다. 이러한 농업 수확량의 감소는 비료를 포함한 다양한 농업 제품과 기술의 채택을 증가시킬 가능성이 높습니다.

태국의 동북지방은 농지 보유수가 가장 많은 지역입니다. 이 지역은 질이 나쁜 토양, 계절에 의한 강우량의 변동, 지표수의 부족 등, 몇개의 농업 과제에 직면하고 있습니다. 이러한 요인에 의해, 이 지역에서 보다 높은 생산성의 향상을 달성하기 위해서는, 비료의 시용이 불가결하게 되어 있습니다.

태국 정부는 국내 농업 생산을 촉진하기 위해 농업 투입물에 보조금을 지급하여 농업 종사자를 지원해 왔습니다. 예를 들어, 정부는 비료에 대한 보조금이라는 형태로 태국의 농업 종사자에 대한 새로운 자극책을 도입했습니다. 이 조치는 국가복지스마트카드를 통해 실시되었으며, 카드 소유자에게 직접 보조금이 지급되었습니다. 이러한 정부의 대처와 농업 생산 증가에 대한 대처가 맞물려 예측 기간 중 태국의 비료 수요를 견인할 것으로 예상됩니다.

질소 비료 수요 증가

경작지역의 감소 및 경제에서 농산물 수출의 중요성이 증가함에 따라 태국의 농업 부문에 비료를 사용하는 것이 필수적입니다.

태국의 토양은 대규모 벼농사가 주요 원인으로 질소가 부족합니다. 따라서 질소 비료, 특히 요소가 가장 많이 사용되고 있습니다. 황안(AS)은 태국에서 요소에 이어 두 번째로 널리 사용되는 질소 비료입니다. AS는 식물에 필수적인 질소(N)와 황(S)의 영양소를 공급해 다른 질소 비료에 비해 독성(NH3수용액)이 낮고 NH3의 휘발에 의한 질소 손실이 적은 등 농업적으로나 환경적으로 이점이 있습니다.

질소 비료는 옥수수, 카사바, 사탕수수 등 태국의 주요 작물에 널리 시용되고 있습니다. 요소는 널리 사용되고 있기 때문에 여전히 가장 많이 수입되는 비료입니다. 치아타이는 단비 요소 시장에서 강한 존재감을 보이고 있으며, 러시아로부터 고품질의 요소를 입수할 수 있는 혜택을 받고 있습니다. 국제비료협회(IFA)에 따르면 태국의 요소 소비량은 2022년 92만 6,000톤에 달했습니다. 이 나라의 질소 비료 수요는 더 빠른 성장과 높은 수확량을 촉진하는 비료에 대한 수요가 증가함에 따라 예측 기간 동안 증가할 것으로 예측되고 있습니다.

태국의 비료 산업 개요

태국의 비료 시장은 통합되어 있으며, 진출기업은 Yara(Thailand) Company Limited, Haifa, Chai Thai, Thai Central Chemical Public Company Limited, Saksiam Group입니다. 합병 및 인수, 제휴, 사업 확대, 신제품의 발매는, 이러한 적극적인 시장 참가 기업이 채용하는 가장 일반적인 사업 전략의 일부입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 정부의 대처 및 지원

- 농업 생산성 저하 및 지역 과제

- 식품 수요 증가

- 시장 성장 억제요인

- 기후 변화 및 자연 재해

- 유기농업으로의 이동

- Porter's Five Forces 분석

- 구매자의 협상력

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 제품별

- 질소 비료

- 요소

- 질산암모늄칼슘(CAN)

- 질산암모늄

- 황산암모늄

- 무수 암모니아

- 기타 질소 비료

- 인산 비료

- 인산1암모늄(MAP)

- 제2인산암모늄(DAP)

- 트리플과인산염(TSP)

- 기타 인산비료

- 칼리 비료

- 미량요소 비료

- 기타

- 질소 비료

- 용도별

- 곡물 및 곡류

- 콩류 및 지방종자

- 상업 작물

- 과일 및 야채

- 기타

제6장 경쟁 구도

- 가장 채용된 전략

- 시장 점유율 분석

- 기업 프로파일

- Yara International ASA

- NFC Public Company Limited

- Chai Thai Co. Ltd

- Thai Central Chemical Public Company Limited

- Haifa Group

- SAKSIAM GROUP

- ICL Group Ltd

- Rayong Fertilizer Trading Company Limited(UBE Group)

- Grupa Azoty SA(Compo Expert)

- ICP FERTILIZER COMPANY

제7장 시장 기회 및 향후 동향

AJY 25.05.02The Thailand Fertilizers Market size is estimated at USD 6.23 million in 2025, and is expected to reach USD 6.95 million by 2030, at a CAGR of 2.2% during the forecast period (2025-2030).

The Thailand fertilizer market is growing due to the growing need to improve agricultural productivity to meet the growing food demand. Major crops such as corn, maize, sugarcane, and rice require substantial nutrient inputs, driving fertilizer demand. Nitrogenous fertilizers dominate the Thai market, primarily due to nitrogen-deficient soils and widespread rice cultivation. Urea is the most commonly used fertilizer. Despite an expanding area under organic cultivation, farmers prefer synthetic or chemical fertilizers due to challenges associated with biofertilizers and organic alternatives.

Government support through fertilizer subsidies and soft loans has significantly influenced market dynamics. In 2024, a new fertilizer subsidy scheme replaced the previous farmers' allowance program, which provided cash support of USD 29.7 per rai (up to 20 rai or 3.2 hectares). The government allocated USD 1.7 billion to this program in the previous year. This increased support is expected to drive fertilizer consumption and enhance farm productivity in the coming years.

Thailand Fertilizers Market Trends

Need for Increasing Agricultural Productivity

Thailand's agricultural productivity has declined in recent years, despite stable agricultural land area. FAOSTAT data indicates a decrease in pulses yield from 953.2 kg/ha in 2021 to 952.4 kg/ha in 2022. This reduction in agricultural yield is likely to increase the adoption of various agricultural products and technologies, including fertilizers.

The Northeastern region of Thailand has the largest number of farm holdings. This area faces several agricultural challenges, including poor-quality soil, seasonal rainfall variability, and scarcity of surface water. These factors have made fertilizer application essential for achieving higher productivity gains in the region.

The Thai government has supported farmers by providing subsidies on farm inputs to boost agricultural production in the country. For example, the government introduced new stimulus measures for Thai farmers in the form of subsidized fertilizers. This measure was implemented through the state welfare smartcard, providing the subsidy directly to cardholders. These government initiatives, combined with efforts to increase agricultural production, are expected to drive the demand for fertilizers in Thailand during the forecast period.

Growing Demand for Nitrogenous Fertilizers

Fertilizer usage is essential for Thailand's agricultural sector, driven by decreasing arable land and the increasing significance of agricultural exports to the economy.

Thailand's soil is predominantly nitrogen-deficient, largely due to extensive rice cultivation. As a result, nitrogenous fertilizers, particularly urea, are the most commonly used. Ammonium sulfate (AS) ranks as the second most widely used nitrogenous fertilizer in Thailand after urea. AS provides essential nitrogen (N) and sulfur (S) nutrients for plants, offering agronomic and environmental advantages such as reduced toxicity (aqueous NH3) and decreased N loss through NH3 volatilization compared to other N fertilizers.

Nitrogen fertilizers are extensively applied to major crops in Thailand, including corn, cassava, and sugarcane. Urea remains the most imported fertilizer due to its widespread use. Chia Tai has a strong presence in the single-nutrient urea market, benefiting from access to high-quality urea from Russia. According to the International Fertilizer Association (IFA), urea consumption in Thailand reached 926 thousand metric tons in 2022. The demand for nitrogen fertilizers in the country is projected to increase during the forecast period due to increasing the need for fertilizers that promote faster growth and higher yields.

Thailand Fertilizers Industry Overview

Thailand Fertilizer market is consolidated, with players such as Yara (Thailand) Company Limited, Haifa, Chai Thai Co. Ltd, Thai Central Chemical Public Company Limited, and Saksiam Group. being some of the active players in the market. Mergers and acquisitions, partnerships, expansion, and product launches are some of the most adopted business strategies by these active players.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Initiatives and Support

- 4.2.2 Declining Agricultural Productivity and Regional Challenges

- 4.2.3 Rising Food Demand

- 4.3 Market Restraints

- 4.3.1 Climate Change and Natural Disasters

- 4.3.2 Shift Towards Organic Farming

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Product

- 5.1.1 Nitrogenous Fertilizers

- 5.1.1.1 Urea

- 5.1.1.2 Calcium Ammonium Nitrate (CAN)

- 5.1.1.3 Ammonium Nitrate

- 5.1.1.4 Ammonium Sulfate

- 5.1.1.5 Anhydrous Ammonia

- 5.1.1.6 Other Nitrogenous Fertilizers

- 5.1.2 Phosphatic Fertilizers

- 5.1.2.1 Mono-Ammonium Phosphate (MAP)

- 5.1.2.2 Di-Ammonium Phosphate (DAP)

- 5.1.2.3 Triple Superphosphate (TSP)

- 5.1.2.4 Other Phosphatic Fertilizers

- 5.1.3 Potash Fertilizers

- 5.1.4 Micronutrient Fertilizers

- 5.1.5 Other Products

- 5.1.1 Nitrogenous Fertilizers

- 5.2 Application

- 5.2.1 Grains and Cereals

- 5.2.2 Pulses and Oilseeds

- 5.2.3 Commerical Crops

- 5.2.4 Fruits and Vegetables

- 5.2.5 Other Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Yara International ASA

- 6.3.2 NFC Public Company Limited

- 6.3.3 Chai Thai Co. Ltd

- 6.3.4 Thai Central Chemical Public Company Limited

- 6.3.5 Haifa Group

- 6.3.6 SAKSIAM GROUP

- 6.3.7 ICL Group Ltd

- 6.3.8 Rayong Fertilizer Trading Company Limited (UBE Group)

- 6.3.9 Grupa Azoty S.A. (Compo Expert)

- 6.3.10 ICP FERTILIZER COMPANY