|

시장보고서

상품코드

1687343

송진화학 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Pine Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

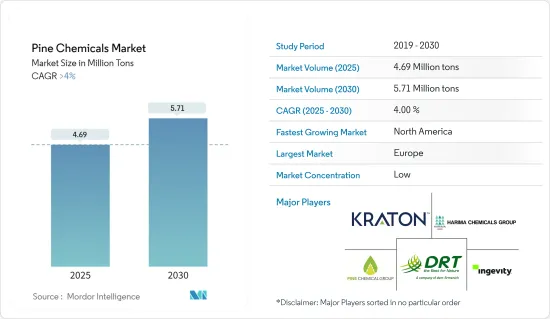

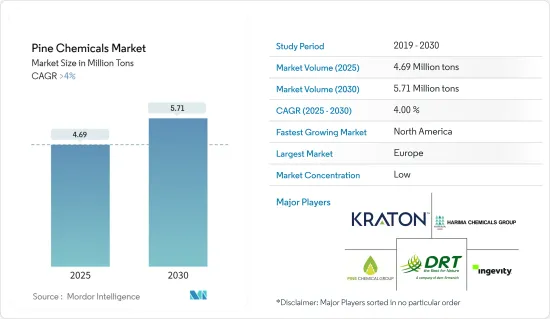

세계의 송진화학 시장 규모는 2025년에 469만 톤으로 예상되며 예측기간 중(2025-2030년) CAGR 4%를 넘어 2030년에는 571만 톤에 달할 것으로 예측됩니다.

COVID-19는 송진화학 시장에 다양한 영향을 미쳤습니다. 처음에는 공급망 혼란, 산업 활동 저하, 개인 소비 감소로 수요가 감소했습니다. 이 때문에 송진화학의 생산과 판매는 일시적으로 감속했습니다. 그러나 유행이 진행됨에 따라 특정 소나무 유래 제품, 특히 소독제, 살균제 및 의약품에 사용되는 제품에 대한 수요가 증가했습니다.

광업 부문과 향료 산업에서 송진화학에 대한 수요 증가는 송진화학 시장을 견인하는 주요 요인입니다.

그러나 저렴한 대체품 증가와 원료 가격의 변동은 송진화학 시장의 성장을 방해할 것으로 예상됩니다.

다양한 최종 사용자 산업에서 송진화학의 용도 확대는 송진화학 시장에 새로운 기회를 가져올 것으로 예상됩니다.

유럽은 독일과 이탈리아와 같은 국가에서 소비가 가장 크며 세계 송진화학 시장을 독점할 것으로 예상됩니다.

송진화학 시장 동향

접착제 및 실란트 부문이 시장을 독점할 전망

송진화학, 특히 송진과 그 유도체는 우수한 접착 특성을 나타내며 접착제와 밀봉제의 이상적인 원료가 되었습니다. 이 제품은 접착 강도와 응집력을 높여 성능과 내구성을 향상시킵니다.

소나무 유래 화학물질은 건축, 자동차, 포장, 목공, 전자기기 등의 산업에서 다양한 접착제나 밀봉제의 배합에 사용되고 있습니다. 감압 접착제, 핫멜트 접착제, 고무계 접착제 등의 제품에 이용되고 있습니다.

또한 건설 산업의 성장은 접착제와 밀봉제의 소비를 촉진하고 송진화학 시장 성장을 가속하고 있습니다. 중국은 세계 최대의 건설 시장 중 하나입니다. 국가통계국(NBS)에 따르면 중국 건설 업계의 사업활동지수는 2023년 11월 55.9에서 12월 기준 56.9로 상승했습니다.

송진화학은 건축에서 코킹, 눈 덮개 밀봉 및 내후성에 사용되는 실란트의 조합에서 주요 성분입니다. 톨유 기반의 실링재는 콘크리트, 석재, 유리, 금속 등 폭넓은 기재에 뛰어난 접착성을 발휘하기 때문에 건물의 외벽, 창문, 도어, 지붕의 틈, 균열, 눈길 등의 실링에 실용적입니다.

인도 건설 산업은 2025년까지 1조 4,000억 달러로 성장할 것으로 예측됩니다. 2030년까지는 6억명이 도시 중심부에 살게 되었고, 그 결과 중·초고급 주택이 2,500만호 추가될 필요가 있습니다. 국가투자계획(NIP) 하에 인도의 인프라 투자 예산은 1조 4,000억 달러로, 예산의 24%가 신재생에너지, 도로·고속도로, 도시 인프라, 12%가 철도에 적용되고 있습니다.

따라서 자동차 산업 및 건설 산업에서 접착제 및 밀봉제의 용도가 증가하는 것은 향후 수년간 시장 조사를 뒷받침할 것으로 예상됩니다.

시장을 독점하는 유럽

유럽에는 광범위한 소나무 숲이 있으며 특히 스웨덴, 핀란드, 러시아, 발트 삼국 등에 많습니다. 이 숲은 송지의 풍부한 공급원이며, 송지는 송지 화학제품의 원료입니다. 풍부하고 지속 가능한 소나무 자원을 활용할 수 있으므로 유럽 생산자는 세계 시장에서 경쟁 우위를 차지할 수 있습니다.

유럽 기업들은 접착제, 밀봉제, 페인트, 코팅제, 인쇄 잉크, 퍼스널케어 제품, 의약품 등 송진화학을 이용하는 광범위한 산업 및 용도에 대응하고 있습니다. 최종 이용 산업이 다양하기 때문에 이 지역의 송진화학 수요는 안정적입니다.

또한, 소나무 유래 수지는 건축용 접착제의 점착제로서 일반적으로 사용되고 있습니다. 이 접착제는 목재, 금속, 콘크리트, 플라스틱 등 다양한 건축자재의 접착에 사용됩니다. 이러한 접착제는 강력하고 내구성이 있기 때문에 건축의 구조 및 비구조 용도에 이상적입니다.

유로통계국이 발표한 최신 추계에 따르면 2023년 12월 건설업생산은 2022년 12월에 비해 유로권에서 1.9%, 유럽에서 2.4% 증가했습니다.

독일은 일반 고무 제품(GRG)과 타이어의 유럽 최대급 생산국입니다. Continental AG, Dunlop GmbH, Michelin Tire AG & Co.KGaA, Pirelli Deutschland GmbH 및 Freudenberg Group은 독일의 타이어 및 비 타이어 제품의 주요 제조업체 중 일부입니다.

독일 연방 통계국(Statistisches Bundesamt)이 2023년 6월에 발표한 추계에 따르면, 2022년 현재 독일 건설업의 매출은 토목 및 특정 건설업의 매출을 상회하고 있습니다. 토목 공사에서 가장 매출이 많은 것은 도로·철도 공사로 210억 유로(228억 3,000만 달러) 이상, 유틸리티은 120억 유로(130억 4,000만 달러)였습니다.

따라서 위의 요인은 주로 유럽의 송진화학 시장에 대한 수요를 촉진할 것으로 예상됩니다.

송진화학 산업 개요

송진화학 시장은 단편화되어 상위 5개 기업이 큰 시장 점유율을 차지하고 있습니다. 시장의 주요 기업(순부동)에는 KRATON CORPORATION, Ingevity Corporation, DRT, Harima Chemicals Group Inc., Pine Chemical Group 등이 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트·지원

목차

제1장 서론

- 조사의 전제

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 광업, 부유화학, 윤활유에서의 송진화학 수요 증가

- 향료 산업에서의 수요 증가

- 억제요인

- 정부의 장려책에 의한 CTO의 바이오연료 전용

- 보다 저렴한 대체품 증가

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화

- 제품 유형

- 톨유

- 미가공 톨유(CTO)

- 톨유 지방산(TOFA)

- 증류 톨유(DTO)

- 톨유 피치(TOP)

- 로진

- 톨유 로진

- 검 로진

- 우드 로진

- 타펜타인

- 검 우드 터펜타인

- 조제 황산 타펜타인

- 기타 타펜타인

- 용도

- 접착제 및 실란트

- 페인트

- 인쇄 잉크

- 윤활유 및 윤활 첨가제

- 바이오연료

- 종이 사이징

- 고무

- 비누 및 세제

- 기타 용도(유전용 화학제품, 화학 첨가물, 츄잉껌, 식품 첨가물)

- 톨유

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 시장 점유율 랭킹 분석

- 주요 기업의 전략

- 기업 프로파일(개요, 재무, 제품 및 서비스, 최근 동향)

- Arakawa Chemical Industries Ltd

- DRT(Derives Resiniques et Terpeniques)

- Forchem Oyj

- Harima Chemicals Group Inc.

- Ingevity Corporation

- Kraton Corporation

- Mercer International

- OOO Torgoviy Dom Lesokhimik

- Pine Chemical Group

- Respol Resinas SA

- Sunpine AB

- Synthomer Plc.

제7장 시장 기회와 앞으로의 동향

- 송진화학의 새로운 용도(DTO, TOFA, CTO, TOP, 우드로진)

- 접착제 및 실란트의 식품·포장 안전 규제

The Pine Chemicals Market size is estimated at 4.69 million tons in 2025, and is expected to reach 5.71 million tons by 2030, at a CAGR of greater than 4% during the forecast period (2025-2030).

COVID-19 has had mixed effects on the pine chemicals market. Initially, demand decreased due to disruptions in supply chains, reduced industrial activity, and lower consumer spending. This led to temporary slowdowns in the production and sales of pine chemicals. However, as the pandemic progressed, there was an increased demand for certain pine-derived products, particularly those used in disinfectants, sanitizers, and pharmaceuticals.

Increasing demand for pine chemicals from the mining sector and the flavors and fragrances industry are the major factors driving the pine chemicals market.

However, an increase in the availability of cheaper substitutes and fluctuations in the price of raw materials are expected to hamper the growth of the pine chemicals market.

The expanding applications of pine chemicals in various end-user industries are expected to unveil new opportunities for the pine chemicals market.

Europe is expected to dominate the pine chemicals market globally, with the most significant consumption coming from countries such as Germany and Italy.

Pine Chemicals Market Trends

The Adhesives and Sealants Segment is expected to Dominate the Market

Pine chemicals, particularly rosin and its derivatives, exhibit excellent tackifying properties, making them ideal ingredients for adhesives and sealants. They enhance the adhesion strength and cohesion of these products, improving their performance and durability.

Pine-derived chemicals are used in a diverse range of adhesives and sealant formulations across industries such as construction, automotive, packaging, woodworking, and electronics. They are utilized in products like pressure-sensitive adhesives, hot-melt adhesives, rubber-based adhesives, and more.

Furthermore, the growth in the construction industry has propelled the consumption of adhesives and sealants, thus propelling the growth of the pine chemicals market. China is one of the world's largest construction markets. According to the National Bureau of Statistics (NBS), the construction industry's business activity index in China rose to 56.9 as of December 2023 from 55.9 in November 2023.

Pine chemicals are the key ingredient in the formulation of sealants used for caulking, joint sealing, and weatherproofing in construction. Tall oil-based sealants offer excellent adhesion to a wide range of substrates such as concrete, masonry, glass, and metal, making them practical for sealing gaps, cracks, and joints in building envelopes, windows, doors, and roofing systems.

India's construction Industry is projected to grow to USD 1.4 trillion by 2025. By 2030, an estimated 600 million people will live in urban centers, resulting in a need for 25 million additional mid- and ultra-luxury units. Under the National Investment Plan (NIP), India has an infrastructure investment budget of USD 1.4 trillion, with 24% of the budget earmarked for renewable energy, roads & highways, urban infrastructure, and 12% for railways.

Thus, the rising application of adhesives and sealants in the automotive and construction industries is expected to boost the market studied in the coming years.

Europe Region to Dominate the Market

Europe has extensive pine forests, particularly in countries like Sweden, Finland, Russia, and the Baltic States. These forests provide a rich source of pine resin, which serves as the raw material for pine chemical production. The availability of abundant and sustainable pine resources gives European producers a competitive advantage in the global market.

European companies cater to a wide range of industries and applications that utilize pine chemicals, including adhesives, sealants, paints, coatings, printing inks, personal care products, pharmaceuticals, and more. The diversity of end-use industries ensures a stable demand for pine chemicals within the region.

Further, pine-derived resins are commonly used as tackifiers in construction adhesives. These adhesives are then used to bond various construction materials, including wood, metal, concrete, and plastics. They provide strong and durable bonds, making them ideal for structural and non-structural applications in construction.

According to the latest estimate published by Eurostat, in December 2023, compared with December 2022, production in construction increased by 1.9% in the euro area and by 2.4% in Europe.

Germany is one of Europe's largest producers of general rubber goods (GRG) and tires. Continental AG, Dunlop GmbH, Michelin Tire Werke AG & Co. KGaA, Pirelli Deutschland GmbH, and Freudenberg Group are some of the significant manufacturers of tire and non-tire products in the country.

According to the estimate released by the Statistisches Bundesamt in June 2023, as of 2022, the turnover of the construction industry in Germany was higher than that of any civil engineering or specific construction sector. The highest turnover in civil engineering activities was for road and railway construction, at more than EUR 21 billion (USD 22.83 billion), and utility projects, which amounted to EUR 12 billion (USD 13.04 billion).

Thus, the factors mentioned above are expected to drive the market demand for pine chemicals, mainly from the European region.

Pine Chemicals Industry Overview

The pine chemicals market is fragmented, with the top five players accounting for a significant market share. The major players in the market (not in any particular order include) KRATON CORPORATION, Ingevity Corporation, DRT, Harima Chemicals Group Inc., and Pine Chemical Group, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Report

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Pine Chemicals in Mining and Flotation Chemicals and Lubricants

- 4.1.2 Increasing Demand from the Flavors and Fragrances Industry

- 4.2 Restraints

- 4.2.1 Diversion of CTO to Biofuels due to Government Incentives

- 4.2.2 Increase in the Availability of Cheaper Substitutes

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Threat of New Entrants

- 4.4.3 Threat of Substitute Products and Services

- 4.4.4 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Product Type

- 5.1.1 Tall Oil

- 5.1.1.1 Crude Tall Oil (CTO)

- 5.1.1.2 Tall Oil Fatty Acid (TOFA)

- 5.1.1.3 Distilled Tall Oil (DTO)

- 5.1.1.4 Tall Oil Pitch (TOP)

- 5.1.2 Rosin

- 5.1.2.1 Tall Oil Rosin

- 5.1.2.2 Gum Rosin

- 5.1.2.3 Wood Rosin

- 5.1.3 Turpentine

- 5.1.3.1 Gum/Wood Turpentine

- 5.1.3.2 Crude Sulphate Turpentine

- 5.1.3.3 Other Turpentines

- 5.1.4 Application

- 5.1.4.1 Adhesives and Sealants

- 5.1.4.2 Coatings

- 5.1.4.3 Printing Inks

- 5.1.4.4 Lubricants and Lubricity Additives

- 5.1.4.5 Biofuels

- 5.1.4.6 Paper Sizing

- 5.1.4.7 Rubber

- 5.1.4.8 Soaps and Detergents

- 5.1.4.9 Other Applications (Oil Field Chemicals, Chemical additives, Chewing Gums, and Food Additives)

- 5.1.1 Tall Oil

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 ASEAN Countries

- 5.2.1.6 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles(Overview, Financials, Products and Services, and Recent Developments)

- 6.4.1 Arakawa Chemical Industries Ltd

- 6.4.2 DRT (Derives Resiniques et Terpeniques)

- 6.4.3 Forchem Oyj

- 6.4.4 Harima Chemicals Group Inc.

- 6.4.5 Ingevity Corporation

- 6.4.6 Kraton Corporation

- 6.4.7 Mercer International

- 6.4.8 OOO Torgoviy Dom Lesokhimik

- 6.4.9 Pine Chemical Group

- 6.4.10 Respol Resinas SA

- 6.4.11 Sunpine AB

- 6.4.12 Synthomer Plc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Applications of Pine Chemicals (DTO, TOFA, CTO, TOP, and Wood Rosin)

- 7.2 Food and Packaging Safety Regulations of Adhesives and Sealants