|

시장보고서

상품코드

1910467

레이저 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Lasers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

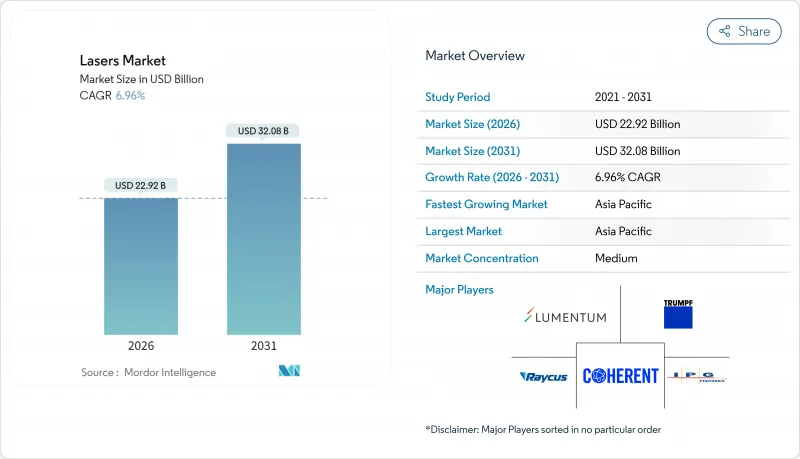

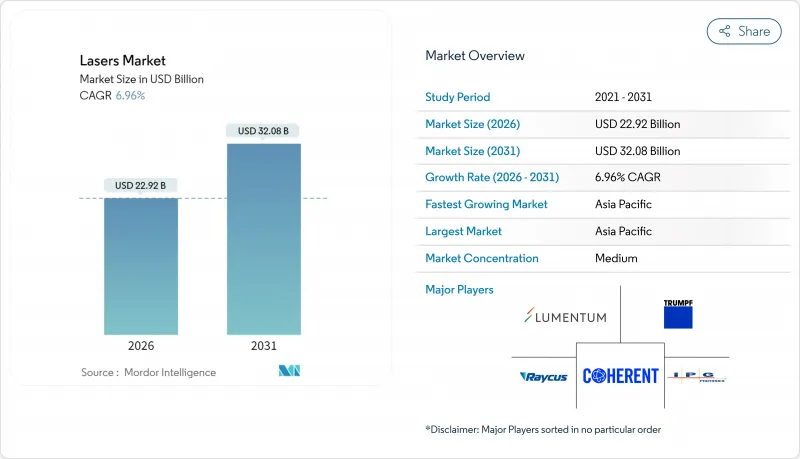

레이저 시장은 2025년 214억 3,000만 달러로 평가되었고, 2026년에는 229억 2,000만 달러, 2031년까지 320억 8,000만 달러에 이를 전망입니다. 2026년부터 2031년에 걸쳐 CAGR은 6.96%를 나타낼 전망입니다.

이 확대는 정밀 마이크로 가공, 적층 조형, 자율 이동체, 차세대 디스플레이 생산의 도입 증가를 반영합니다. 10nm 미만의 반도체 미세구조를 가공하는 초고속 펄스 광원과 두꺼운 금속판을 절단하는 kW급 파이버 시스템은 현재 대량 생산 공장에서 주류가 되고 있습니다. 정부 자금에 의한 포토닉스 클러스터가 아시아태평양에서 생태계 개발을 가속화하는 반면, 적층 성형 레이저는 항공우주 부품의 재료 폐기를 줄이고 생산 사이클을 단축합니다. 갈륨, 게르마늄 및 인화 인듐 기판을 둘러싼 공급망의 위험은 여전히 역풍이지만, 열 관리 및 빔 결합 아키텍처의 혁신으로 인해 달성 가능한 출력 상한은 계속 상승하고 있습니다.

세계 레이저 시장 동향과 인사이트

반도체 백엔드 패키징에서 고정밀 마이크로 가공 수요 급증

팬아웃 웨이퍼 레벨 패키징 및 스루글래스 비아 프로세스는 10 마이크로미터 미만의 미세 구조와 1% 미만의 펄스간 에너지 편차를 실현하는 펨토초 엑시머 광원을 지정하여 300mm 웨이퍼 전체에서 균일한 비아 형성을 보장합니다. 와이어 본딩을 레이저 형성 마이크로 범프로 대체하여 상호 연결 저항을 40% 줄이고 3차원 칩 적층으로 가는 길을 엽니다. 빔 성형 모듈과 인사이트 모니터링의 동기화는 대량 생산 팹의 수율 향상과 폐기율 감소를 실현합니다. 아시아태평양의 주조회사에서는 턴키형 레이저 스테이션의 조달이 계속되고 있어 초고속 광원 공급업체에 대한 수요를 대폭 견인하고 있습니다. 패키징 라인의 택트 타임이 단축되는 가운데, 더 높은 반복 주파수에 대한 수요가 높아져, 프리미엄 초고속층에 있어서의 평균 판매 가격의 상승이 전망됩니다.

항공우주용 초합금 부품에서 적층 성형 레이저 채택 확대

항공우주 주요 제조업체는 현재 티타늄 알루미나이드 및 니켈 초합금을 95% 이상의 재료 이용률로 가공하는 분말 바닥 용융 파이버 레이저의 인정을 추진하고 있어 절삭 가공을 크게 웃도는 성능을 발휘하고 있습니다. 동적 빔 쉐이핑 기술은 빌드 사이클을 40% 단축하고 에너지 소비를 60% 줄이면서 비행 장비에 필수적인 미세 구조의 무결성을 유지합니다. AS9100 표준 개정판에서는 레이저 성형 부품이 명시적으로 언급되어 인증 워크플로우가 간소화되었습니다. 미국 및 유럽의 엔진 프로그램에서는 경제적인 가공이 불가능한 "프린트 우선" 형상의 설계가 증가하고 있습니다. 이러한 전환으로 레이저 수요는 와이드 바디 기대 업데이트 및 2020년대 후반 취항을 예정하는 극초음속 추진 프로젝트와 연동하고 있습니다.

고품질 갈륨 비소/인듐 린 에피웨이퍼의 지속적인 부족

갈륨 및 게르마늄의 수출 규제 강화로 고출력 레이저 다이오드에 필수적인 화합물 반도체 기판의 부족이 심각화되고 있습니다. 로트 간의 열전도율 편차로 인해 레이저 제조업체는 재인증 사이클의 장기화를 강요하여 출하 지연과 재고 버퍼 증가를 초래하고 있습니다. 북미 및 유럽의 신흥기업은 새로운 결정성장 공장의 계획을 진행하고 있습니다만, 장치의 리드 타임과 프로세스 노하우의 습득에 의해 실질적인 양산 개시는 2027년 이후가 될 전망입니다. 고가의 기판 가격은 부품 원가를 두 자리로 끌어 올리고 있으며 특히 고온 접합 온도에서 작동하는 LiDAR 및 통신 레이저에서 두드러집니다. 제조업체는 기존 에피웨이퍼 공급을 보충하기 위해 실리콘 베이스의 중간 기판의 실험을 진행하고 있습니다만, 성능면에서의 페널티는 여전히 무시할 수 없는 수준입니다.

부문 분석

파이버 레이저는 2025년 세계 레이저 시장의 41.40%를 차지했으며, 우수한 빔 품질, 올 파이버 구조 및 최소의 유지보수성을 제공했습니다. 그러나 고체 레이저 플랫폼은 지향성 에너지 무기와 핵융합 실험이 수 메가와트급 광 체인을 필요로 하기 때문에 2031년까지 9.18%라는 가장 빠른 CAGR을 기록했습니다. 방위 자금의 흐름을 반영하여 고체 레이저 장치 세계 시장 규모는 2031년까지 56억 2,000만 달러 이상에 달할 것으로 예측됩니다. 슬래브 증폭 매체를 장갑 파이버 전송 라인에 연결하는 하이브리드 구성은 휘도를 유지하면서 단일 파이버의 출력 한계를 초과하는 데 도움이 됩니다. CO2 광원은 후판 절단 분야에서 존재감을 유지하는 한편, 다이오드 레이저는 펌프 어레이나 직접 라이팅 용도로 확대되고 있습니다. 엑시머 레이저와 UV 레이저는 100nm 미만의 반도체 리소그래피에 필수적이며, 주조 설비 투자가 주기적인 변동을 보이는 중에서도 안정적인 수요를 지지하고 있습니다.

분산 이득 아키텍처에 대한 지속적인 조사는 열 유도 모드 불안정성이 없는 출력 스케일링을 약속합니다. 자유 전자 레이저와 양자 캐스케이드 기술은 여전히 틈새 분광 영역을 차지하지만, 컴팩트 가속기 구조의 획기적인 것은 중적외 영역에 대한 액세스를 궁극적으로 보급 할 수 있습니다. IEC 60825-1에 따른 안전 기준은 인클로저 설계를 규정하며 고도 자동화 공장의 총 도입 비용에 영향을 미칩니다. 광섬유의 신뢰성과 고체 레이저의 우위성을 융합시킨 벤더는 응용 분야의 경계가 모호해지는 가운데 압도적인 점유율 획득의 입장을 확립하고 있습니다.

재료 가공 분야는 2025년 시점에서 세계 레이저 시장의 30.10%를 차지해 자동차 및 항공우주 및 일반산업에 있어서의 절단, 용접, 드릴링, 적층 조형 프로세스를 망라하고 있습니다. 그러나 특히 LiDAR과 분광 모듈 등의 센서 도입은 8.58%의 연평균 복합 성장률(CAGR)을 나타내고 있으며, 10년 이내에 이 차이를 줄일 전망입니다. 중공업용 오더는 여전히 경기 순환의 영향을 받지만 기존 플랜트의 리노베이션 프로그램은 기준 수요를 지원합니다. 병행하여 저침습성과 신속한 회복을 특징으로 하는 외래수술 증가에 따라 의료 및 미용용 레이저 시장은 점진적인 성장을 이루고 있습니다.

리소그래피 분야의 지출은 주요 주조 회사에서 첨단 노드의 양산에 의존하고 있으며 각 EUV 스캐너에는 여러 개의 고반복 엑시머 광원이 통합되어 있습니다. 차세대 디스플레이는 수율 유지를 위한 초고속 복구 기술에 의존하며, 이로 인해 패널의 이익률 향상이 예상됩니다. 대 UAS 임무용 고에너지 시스템의 군사 조달에 의해 수요에 편차가 생기는 한편, 공공 부문에 의한 기초 광학 조사에의 자금 투입도 증가하고 있습니다. 에지 및 클라우드 데이터센터가 급증함에 따라 광 인터커넥트 수요가 통신용 레이저 출하량을 늘리고 세계 레이저 시장에서의 응용 분야의 다양성을 강화하고 있습니다.

지역별 분석

아시아태평양은 2025년 세계 레이저 시장의 46.40%를 차지했고 2031년까지 연평균 복합 성장률(CAGR) 8.17%로 확대될 것으로 전망됩니다. 이것은 고밀도 반도체 팹, 급성장하는 디스플레이 생산 라인, 정부 지원 포토닉스 파크가 견인하고 있습니다. 중국은 선진 리소그래피 노드용 엑시머 레이저 및 초고속 레이저 조달을 주도하고 있으며, 일본은 우수한 빔 품질을 요구하는 정밀 가공 용도를 고도화하고 있습니다. 한국의 OLED 및 마이크로 LED 생산 라인은 높은 가동률을 유지하고 지속적인 레이저 보수 계약을 지원하고 있습니다. 인도의 생산 연동형 장려책은 공작기계 제조업체에 레이저 절단 및 용접 능력의 현지화를 촉진해 잠재 수요를 확대하고 있습니다. 대만과 싱가포르는 각각 화합물 반도체 클러스터와 정밀 공학 클러스터에서 틈새 수요에 기여합니다.

북미는 항공우주산업의 생산 페이스와 메가와트급 지향성 에너지 시스템용 방위계약에 힘입어 제2위의 지위를 유지하고 있습니다. 미국에서는 Manufacturing USA 산하의 포토닉스 거점이 통합 포토닉스 및 양자 캐스케이드 설계 분야에서 스타트업 기업의 육성을 촉진하고 있습니다. 캐나다의 재료과학연구소는 현지 기계가공공장과 연계하여 레이저클래딩 및 경화처리의 실증시험을 실시합니다. 멕시코의 전기자동차 회랑에서는 배터리 트레이용 파이버 레이저 용접의 양산화가 진행됩니다. USMCA 조화로 인한 국경 간 공급 체인의 편의성 향상이 예상되는 반면, 수출 관리는 특정 지역으로의 고출력 장비의 수출을 제한합니다. 환경 감시 규제도 중적외 가스 검지 모듈의 국내 수요를 환기하고 있습니다.

유럽에서는 고에너지 연구용 레이저를 추진하는 독일의 기계 대기업과 프랑스의 방위 통합 기업이 현저한 점유율을 차지하고 있습니다. 영국은 박리 결함을 최소화하기 위해 레이저 어블레이션을 이용한 항공우주 복합재 가공을 추구하고, 이탈리아의 슈퍼카 제조업체는 알루미늄 섀시의 효율적인 용접에 수 kW급 디스크 레이저를 채택하고 있습니다. 기계 지침 및 IEC 60825-1 준수를 포함한 EU 전역의 규제가 수출용 시스템에 통합되는 안전 기능을 형성하고 있습니다. DioHELIOS와 같은 공동 프로그램은 다이오드 레이저 전문 지식을 모으고 비용 효율적인 규모 확장을 추진하는 컨소시엄을 통해 유럽이 융합 에너지 실현 기술에 주력하고 있음을 보여줍니다. 그린 수소 이니셔티브의 확대에 따라 지역 전체에서 레이저를 이용한 판재 절단이나 파이프 용접에 대한 관심이 높아지고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 반도체 백엔드 패키징에 있어서의 고정밀 마이크로 가공 수요 급증

- 항공우주용 초합금 부품용 적층 조형 레이저 채택 확대

- 자율 주행 시스템에서 LiDAR 레이저의 탑재 증가

- 차세대 OLED 및 마이크로 LED 디스플레이 수리에 있어서의 초고속 레이저의 응용 확대

- 정부 자금에 의한 포토닉스 클러스터가 지역의 제조 에코시스템을 견인

- 판금 절단용 kW급 파이버 레이저의 가격 성능비의 급속한 향상

- 시장 성장 억제요인

- 고급 갈륨 아세나이드(GaAs)/인듐 포스파이드(InP) 에피웨이퍼 지속적 부족

- 특정 국가 대상 고출력 레이저 수출 제한 규제

- 30kW이상 열 관리(Thermal Management) 문제로 절단 두께 확장 제한

- 안전기준의 단편화에 의해 OEM 인증 비용 증가

- 밸류체인 분석

- 기술의 전망

- 규제 상황

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 레이저 유형별

- 광섬유 레이저

- 다이오드 레이저

- CO2 레이저

- 고체 레이저

- 엑시머 레이저 및 자외선 레이저

- 기타 유형(양자 캐스케이드, 자유전자)

- 용도별

- 재료 가공(절단, 용접, 드릴링)

- 통신 및 광 인터커넥트

- 의료 및 미용 분야

- 리소그래피 및 반도체 계측 기술

- 군 및 방위

- 디스플레이(OLED, 마이크로 LED, 프로젝션)

- 센서(LiDAR, 분광법)

- 인쇄 및 마킹

- 출력별

- 저출력(1kW 미만)

- 중출력(1-3kW)

- 고출력(3kW 이상)

- 운용 모드별

- 연속파(CW)

- 펄스(ns, ps, fs)

- 최종 사용자 업계별

- 전자기기 및 반도체

- 자동차

- 산업기계

- 헬스케어

- 항공우주 및 방위

- 연구기관 및 학술기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 기타 아시아태평양

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Coherent Corp.

- IPG Photonics Corporation

- TRUMPF SE Co. KG

- nLIGHT, Inc.

- Lumentum Holdings Inc.

- Jenoptik AG

- Novanta, Inc.

- Lumibird SA

- Wuhan Raycus Fiber Laser Technologies Co. Ltd

- Hans Laser Technology Industry Group Co., Ltd.

- Maxphotonics Co., Ltd.

- Keyence Corporation

- EKSPLA UAB

- MKS Instruments, Inc.(Spectra-Physics)

- Panasonic Corporation

- EdgeWave GmbH

- Civan Lasers Ltd.

- Synrad Laser Division

- Amonics Ltd.

- TOPTICA Photonics AG

제7장 시장 기회와 장래의 전망

SHW 26.01.26The lasers market is expected to grow from USD 21.43 billion in 2025 to USD 22.92 billion in 2026 and is forecast to reach USD 32.08 billion by 2031 at 6.96% CAGR over 2026-2031.

This expansion reflects rising deployment across precision micromachining, additive manufacturing, autonomous mobility, and next-generation display production. Ultrafast pulse sources that machine sub-10 nm semiconductor features and kW-class fiber systems that cut thicker metal sheets are now mainstream in high-volume factories. Government-funded photonics clusters accelerate ecosystem development in Asia-Pacific, while additive manufacturing lasers lower material waste in aerospace components and shorten production cycles. Supply chain risks around gallium, germanium, and indium phosphide substrates remain a headwind, yet innovations in thermal management and beam-combining architectures continue to raise attainable power ceilings.

Global Lasers Market Trends and Insights

Surging Demand for High-Precision Micromachining in Semiconductor Back-End Packaging

Fan-Out Wafer Level Packaging and Through-Glass Via processes specify femtosecond and excimer sources that deliver sub-10 µm features with under-1% pulse-to-pulse energy deviation, ensuring uniform via formation across full 300 mm wafers. Replacing wire bonding with laser-formed micro-bumps reduces interconnect resistance by 40% and opens the path to three-dimensional chip stacks. Beam-shaping modules synchronized with in-situ monitoring raise yield and lower scrap rates in high-volume fabs. Asia-Pacific foundries continue to procure turnkey laser stations, creating a substantial pull on ultrafast source suppliers. As packaging line takt times tighten, demand for even higher repetition rates is expected to lift average selling prices in the premium ultrafast tier.

Growing Adoption of Additive Manufacturing Lasers for Aerospace Super-Alloy Parts

Aerospace primes now qualify powder-bed-fusion fiber lasers that process titanium aluminide and nickel super-alloys at material utilization rates above 95%, sharply outperforming subtractive machining. Dynamic beam shaping shortens build cycles by 40% and lowers energy consumption by 60%, while maintaining microstructure integrity critical for flight hardware. AS9100 revisions explicitly reference laser-printed parts, simplifying certification workflows. U.S. and European engine programs increasingly design for "print-first" geometries that cannot be machined economically. The shift ties laser demand to wide-body fleet renewal and hypersonic propulsion projects scheduled for late-decade entry into service.

Persistent Shortages of High-Grade Gallium Arsenide/Indium Phosphide Epi-Wafers

Export curbs on gallium and germanium intensify the scarcity of compound semiconductor substrates vital for high-power laser diodes. Variability in thermal conductivity across lots forces laser makers into lengthy re-qualification cycles, delaying shipments and elevating inventory buffers. Start-ups in North America and Europe plan new crystal-growth fabs, but tooling lead times and process know-how push meaningful volumes past 2027. Premium substrate pricing inflates the bill of materials by double digits, particularly for LiDAR and telecom lasers operating at elevated junction temperatures. Manufacturers are experimenting with silicon-based interposers to stretch the existing epi-wafer supply, yet performance penalties remain non-trivial.

Other drivers and restraints analyzed in the detailed report include:

- Rising Installation of LiDAR Lasers in Autonomous Mobility Stacks

- Expanding Use of Ultrafast Lasers for Next-Gen OLED and Micro-LED Display Repair

- Export-Control Regimes Limiting High-Power Laser Shipments to Certain Countries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fiber lasers held 41.40% of the global lasers market in 2025 thanks to robust beam quality, all-fiber architectures, and minimal service needs. Solid-state platforms, however, register the swiftest 9.18% CAGR to 2031 as directed-energy weapons and fusion experiments demand multi-megawatt optical chains. The global lasers market size for solid-state devices is projected to cross USD 5.62 billion by 2031, reflecting defense funding pipelines. Hybrid configurations that splice slab gain media into armored fiber delivery lines help transcend single-fiber power ceilings while preserving brightness. CO2 sources persist in thick-section cutting, whereas diode lasers expand in pump arrays and direct-write applications. Excimer and UV variants remain indispensable in sub-100 nm semiconductor lithography, anchoring steady demand despite cyclical foundry capex.

Ongoing research into distributed-gain architectures promises power scaling without thermally induced mode instabilities. Free-electron and quantum cascade technologies still occupy niche spectroscopy realms, but breakthroughs in compact accelerator structures could eventually democratize mid-infrared access. Safety compliance under IEC 60825-1 shapes enclosure designs, influencing total landed cost in high-automation factories. Vendors that fuse fiber reliability with solid-state punch position themselves to capture outsized share as application boundaries blur.

Materials processing retained a 30.10% share of the global lasers market in 2025, spanning cutting, welding, drilling, and additive build processes across automotive, aerospace, and general industry. Yet sensor deployments, notably LiDAR and spectroscopy modules, post an 8.58% CAGR, poised to narrow the gap by decade-end. Heavy-industry orders remain cyclical, but retrofit programs in brownfield plants sustain baseline volume. In parallel, medical and aesthetic lasers harvest incremental growth from outpatient procedures that favor low invasiveness and quick recovery.

Lithography expenditures hinge on advanced-node ramps at the top foundries, with each EUV scanner embedding multiple high-repetition excimer sources. Next-generation displays rely on ultrafast repair to maintain yield, unlocking higher panel profit margins. Military procurement of high-energy systems for counter-UAS duties injects lumpiness but also elevates public-sector funding for fundamental optics research. As edge and cloud data centers mushroom, optical interconnect demand boosts telecom laser volumes, reinforcing the application mix diversity within the global lasers market.

The Lasers Market Report is Segmented by Laser Type (Fiber Lasers, Diode Lasers, and More), Application (Materials Processing, and More), Power Output (Low-Power, Medium-Power, High-Power), Mode of Operation (Continuous-Wave, Pulsed), End-User Industry (Electronics and Semiconductor, and More), and Geography (North America, South America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific controlled 46.40% of the global lasers market in 2025 and is projected to compound at 8.17% CAGR to 2031, propelled by dense semiconductor fabs, burgeoning display lines, and state-backed photonics parks. China leads excimer and ultrafast procurement for advanced lithography nodes, while Japan refines precision machining applications that demand superior beam quality. South Korea's OLED and micro-LED lines maintain high utilization, feeding sustained laser service contracts. India's Production-Linked Incentive schemes entice machine-tool makers to localize laser cutting and welding capacities, widening addressable demand. Taiwan and Singapore contribute niche volumes from compound semiconductor and precision engineering clusters, respectively.

North America ranks second, buoyed by aerospace build rates and defense contracts for megawatt-class directed-energy systems. U.S. photonics hubs under the Manufacturing USA umbrella foster start-up formation in integrated photonics and quantum cascade designs. Canada's materials-science institutes partner with local machine shops to trial laser cladding and hardening, while Mexico's electric-vehicle corridor scales fiber-laser welding for battery trays. Cross-border supply chains benefit from USMCA harmonization, though export controls constrain outbound shipments of high-power units to certain destinations. Environmental-monitoring mandates also spur domestic demand for mid-infrared gas-sensing modules.

Europe holds notable share through Germany's machinery giants and France's defense integrators that champion high-energy research lasers. The United Kingdom pursues aerospace composites processing with laser ablation to minimize delamination defects, and Italy's super-car makers adopt multi-kW disk lasers to weld aluminum chassis efficiently. EU-wide regulations, including the Machinery Directive and IEC 60825-1 alignment, shape safety features embedded in export-grade systems. Collaborative programs like DioHELIOS illustrate Europe's focus on fusion-energy enablers, with consortiums pooling diode-laser expertise to drive cost-effective scaling. Growing green-hydrogen initiatives further elevate interest in laser-based plate cutting and pipe welding across the region.

- Coherent Corp.

- IPG Photonics Corporation

- TRUMPF SE + Co. KG

- nLIGHT, Inc.

- Lumentum Holdings Inc.

- Jenoptik AG

- Novanta, Inc.

- Lumibird SA

- Wuhan Raycus Fiber Laser Technologies Co. Ltd

- Hans Laser Technology Industry Group Co., Ltd.

- Maxphotonics Co., Ltd.

- Keyence Corporation

- EKSPLA UAB

- MKS Instruments, Inc. (Spectra-Physics)

- Panasonic Corporation

- EdgeWave GmbH

- Civan Lasers Ltd.

- Synrad Laser Division

- Amonics Ltd.

- TOPTICA Photonics AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for high-precision micromachining in semiconductor back-end packaging

- 4.2.2 Growing adoption of additive manufacturing lasers for aerospace super-alloy parts

- 4.2.3 Rising installation of LiDAR lasers in autonomous mobility stacks

- 4.2.4 Expanding use of ultrafast lasers for next-gen OLED and micro-LED display repair

- 4.2.5 Government-funded photonics clusters driving regional manufacturing ecosystems

- 4.2.6 Rapid price/performance improvements in kW-class fiber lasers for sheet-metal cutting

- 4.3 Market Restraints

- 4.3.1 Persistent shortages of high-grade gallium arsenide/indium phosphide epi-wafers

- 4.3.2 Export-control regimes limiting high-power laser shipments to certain countries

- 4.3.3 Thermal-management challenges above 30 kW limiting cutting-thickness roadmap

- 4.3.4 Fragmented safety standards increasing certification costs for OEMs

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Laser Type

- 5.1.1 Fiber Lasers

- 5.1.2 Diode Lasers

- 5.1.3 CO2 Lasers

- 5.1.4 Solid-State Lasers

- 5.1.5 Excimer and Ultraviolet Lasers

- 5.1.6 Other Types (Quantum Cascade, Free-Electron)

- 5.2 By Application

- 5.2.1 Materials Processing (Cutting, Welding, Drilling)

- 5.2.2 Communications and Optical Interconnects

- 5.2.3 Medical and Aesthetic

- 5.2.4 Lithography and Semiconductor Metrology

- 5.2.5 Military and Defense

- 5.2.6 Displays (OLED, Micro-LED, Projection)

- 5.2.7 Sensors (LiDAR, Spectroscopy)

- 5.2.8 Printing and Marking

- 5.3 By Power Output

- 5.3.1 Low-Power (Less than 1 kW)

- 5.3.2 Medium-Power (1-3 kW)

- 5.3.3 High-Power (More than 3 kW)

- 5.4 By Mode of Operation

- 5.4.1 Continuous-Wave (CW)

- 5.4.2 Pulsed (ns, ps, fs)

- 5.5 By End-User Industry

- 5.5.1 Electronics and Semiconductor

- 5.5.2 Automotive

- 5.5.3 Industrial Machinery

- 5.5.4 Healthcare

- 5.5.5 Aerospace and Defense

- 5.5.6 Research and Academia

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Coherent Corp.

- 6.4.2 IPG Photonics Corporation

- 6.4.3 TRUMPF SE + Co. KG

- 6.4.4 nLIGHT, Inc.

- 6.4.5 Lumentum Holdings Inc.

- 6.4.6 Jenoptik AG

- 6.4.7 Novanta, Inc.

- 6.4.8 Lumibird SA

- 6.4.9 Wuhan Raycus Fiber Laser Technologies Co. Ltd

- 6.4.10 Hans Laser Technology Industry Group Co., Ltd.

- 6.4.11 Maxphotonics Co., Ltd.

- 6.4.12 Keyence Corporation

- 6.4.13 EKSPLA UAB

- 6.4.14 MKS Instruments, Inc. (Spectra-Physics)

- 6.4.15 Panasonic Corporation

- 6.4.16 EdgeWave GmbH

- 6.4.17 Civan Lasers Ltd.

- 6.4.18 Synrad Laser Division

- 6.4.19 Amonics Ltd.

- 6.4.20 TOPTICA Photonics AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment