|

시장보고서

상품코드

1687387

시멘트 보드 시장 : 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)Cement Board - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

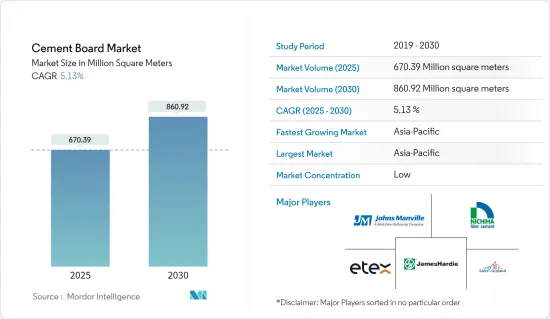

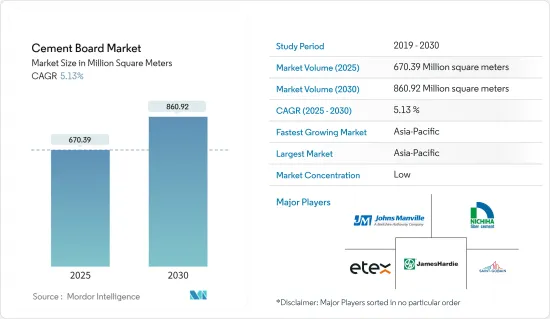

세계의 시멘트 보드 시장 규모는 2025년 6억 7,039만 평방미터로 추정되며, 예측 기간 중(2025-2030년) CAGR 5.13%로 확대되어, 2030년에는 8억 6,092만 평방미터에 이를 것으로 예측됩니다.

주요 하이라이트

- 주택 및 상업 건축에 있어서의 채용 증가와, 내충격성과 내구성이라고 하는 바람직한 특성이, 예측 기간중의 시멘트 보드 시장을 견인할 것으로 예상됩니다.

- 그러나, 기존에 비해 초기 코스트가 높은 것이 시장 성장의 방해가 될 것으로 예상됩니다.

- 그렇다고는 해도, 미관을 향상시키려는 동향의 고조는 시장에 새로운 기회를 낳을 것으로 예상됩니다.

- 아시아태평양이 시장을 독점할 것으로 예상되며, 수요의 대부분은 중국과 인도에 의한 것입니다.

시멘트 보드 시장 동향

주택 및 상업 건축에서 채용 증가

- 시멘트 보드은 내구성, 내화성, 내습성, 비용 효과 등의 독특한 조합을 제공하기 위해 주택 건설에 자주 사용됩니다.

- 상업 분야는 시멘트 보드 시장에 있어서 매우 중요한 분야로서 두드러지고 있어 오피스 부문이 그 선두를 달리고 있습니다. 세계의 상업 활동의 급증에 따라, 이 분야에서의 시멘트 보드 수요도 증가하고 있습니다.

- 오피스 공간의 거점으로 급성장하고 있는 아시아태평양은 상업 건축의 톱 시장에 랭크되고 있습니다.

- 인도에서는 신흥기업의 에코시스템이 급성장하고 있어 오피스 스페이스에 대한 의욕이 높아지고 있습니다.

- 미국도 건축 및 건설 업계에 있어서 거대한 시장입니다. 미국 인구 조사국의 데이터에 의하면, 2023년, 미국은 민간의 비주택 건축물의 신축에 7,061억 달러 이상을 지출해, 2022년의 5,965억 달러에서 대폭으로 증가했습니다.

- 2023년에는 추정 146만 9,800호의 주택건설이 허가되어 2022년의 166만 5,100호를 11.7% 밑돌았습니다.

- 2024년 7월의 건축 허가에 의한 민간 주택 착공 호수의 계절 조정이 끝난 연율은 1,396,000호였습니다.

- 독일의 견조한 경제는 상업 공간, 특히 고품질의 ESG를 준수하는 사무실 건물에 대한 수요를 촉진하고 있으며, 이는 프라임 임대료 상승으로도 분명합니다. 소매 스페이스 개발, 특히 쇼핑 센터도 2023년에 일관된 성장을 보였습니다.

- 브라질의 주택 섹터는 급속한 도시화에 힘입어 대폭적인 민간투자를 모으고 있습니다.

- 사우디아라비아에서는 제다 센트럴 거대 프로젝트로 대표되는 건설 붐이 일어나고 있습니다. 공공건설기금(PIF)의 자회사인 제다 중앙개발회사(JCDC)가 주도하는 이 야심적인 200억 달러의 프로젝트에는 박물관, 오페라 하우스, 스포츠 스타디움 등의 랜드마크 외에 17,000호의 주택과 3,000채 이상의 호텔이 포함되어 있습니다.

- 이러한 움직임은 주택과 상업 건축의 양쪽에 있어서의 시멘트 보드 수요가 세계적으로 왕성하다는 것을 뒷받침하고 있어 예측 기간중의 성장도 유망합니다.

아시아태평양이 시장을 독점할 전망

- 아시아태평양은 중국을 필두로 세계의 시멘트 보드 시장에서 지배적인 지위를 차지하고 있습니다.

- 중국은 적극적으로 도시화를 진행하고 있으며, 2030년까지 도시화율 70%를 목표로 하고 있습니다.

- 중국의 홍콩에서는 주택 당국이 합리적인 가격의 주택 건설을 시작하기 위해 여러 시책을 시작했습니다.

- 2025년까지 2억 5,000만 명의 농촌 주민을 새로운 거대도시로 이전할 계획도 있어 중국 정부의 야심적인 건설구상은 시멘트 보드 시장을 뒷받침하게 될 것 같습니다.

- 곤경에 처한 경제에 대한 대응으로 중국 지사는 주요 건축 프로젝트 예산을 20% 가까이 증액하고 있습니다. 중국의 3분의 2 이상의 지역이 교통 인프라와 산업 지대를 포함한 중요한 프로젝트를 진행하고 있으며, 2024년 총 예산은 12조 2,000억 위안(1조 8,000억 달러)을 넘어섰습니다.

- 중국의 가처분 소득 증가는 쇼핑몰과 호텔 등 고급 상업 공간 수요를 촉진하고 있습니다. 중국은 쇼핑센터 개발의 최전선에 서 있으며, 기존 센터는 4,000곳 가까이, 2025년까지는 추가로 7,000 곳이 될 것으로 추정되고 있습니다. 2021년 3분기에 착공했으며, 2025년 4분기에 완성될 예정인 무한 Fosun Bund Center T1과 같은 프로젝트는 시장을 더욱 강화하고 있습니다.

- 인도에서는 저렴한 주택이 70% 증가할 전망입니다. Invest India에 따르면 건설 부문은 2025년까지 1조 4,000억 달러의 평가 금액을 달성할 것으로 예상됩니다. 2030년에는 인구의 30% 이상이 도시 거주자가 된다는 예측도 있어, 2,500만호 이상의 중급 주택과 저렴한 주택이 급무가 되고 있습니다. 부동산법, GST(물품 및 서비스세), REIT(부동산투자신탁) 등의 최근 개혁은 인가를 가속화하고 건설 업계를 강화하는 것을 목표로 하고 있으며, 시장의 성장을 가속하고 있습니다.

- 한국은 대규모 산업건설사업에 종사하고 있습니다. 특필해야 할 예는 2026년 완성을 목표로 S-Oil Corp.가 울산에 건설중인 야심찬 Shaheen 정유소 통합 석유화학 플랜트입니다. 이 시설에는 세계 최대의 나프타 공급형 스팀 크래커가 설치되어 연산 180만 톤의 에틸렌을 생산할 수 있습니다.

- 이러한 움직임으로부터, 아시아태평양의 시멘트 보드 수요는 예측 기간 중에 크게 성장하는 것이라고 생각됩니다.

시멘트 플레이트 산업의 세분화

시멘트 보드 시장은 부분적으로 세분화되어 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트·지원

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 성장 촉진요인

- 주택 및 상업 건축에 있어서의 채용 증가

- 내충격성과 내구성이라는 바람직한 특성

- 기타 촉진요인

- 시장 성장 억제요인

- 기존 경쟁품에 비해 높은 초기 비용

- 기타 억제요인

- 업계 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화

- 제품 유형별

- 섬유 시멘트 보드(FCB)

- 우드 울 시멘트 보드(WWCB)

- 우드 스트랜드 시멘트 보드(WSCB)

- 시멘트 접착 파티클 보드(CBPB)

- 용도별

- 바닥재

- 외벽 및 칸막이벽

- 지붕재

- 기둥 및 빔

- 외관, 날씨 보드, 클래딩

- 차음 및 단열재

- 기타 용도(프리팹 주택, 상설 셔터, 내화 구조 등)

- 최종 사용자 산업별

- 주택용

- 상업

- 산업 및 시설

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 튀르키예

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 카타르

- 아랍에미리트(UAE)

- 나이지리아

- 이집트

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 시장 점유율(%)**/랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- Etex Group

- Elementia Materials

- Everest Industries Limited

- James Hardie Industries PLC

- Johns Manville

- Knauf Gips KG

- Saint-Gobain

- BetonWood SRL

- Cembrit Holding A/S

- HIL Limited

- GAF

- NICHIHA Co. Ltd

제7장 시장 기회와 앞으로의 동향

- 심미성 향상을 위한 동향의 고조

- 기타 기회

The Cement Board Market size is estimated at 670.39 million square meters in 2025, and is expected to reach 860.92 million square meters by 2030, at a CAGR of 5.13% during the forecast period (2025-2030).

Key Highlights

- The increasing adoption in residential and commercial construction and desirable properties of impact resistance and durability are expected to drive the cement board market during the forecast period.

- However, the high initial cost compared to its traditional counterparts is expected to hinder market growth.

- Nevertheless, the rising trends for aesthetic improvement are expected to create new opportunities for the market.

- Asia-Pacific is expected to dominate the market, with the majority of demand coming from China and India.

Cement Board Market Trends

Increasing Adoption in Residential and Commercial Construction

- Cement boards offer a unique combination of durability, fire resistance, moisture resistance, and cost-effectiveness, making them a popular choice for residential construction.

- The commercial segment stands out as a pivotal player in the cement board market, with the office sector leading the way. As global commercial activities surge, so does the demand for cement boards in this segment.

- Asia-Pacific, a burgeoning hub for office spaces, ranks among the top markets in commercial construction. Countries like India and China have seen a consistent uptick in demand for office spaces, driven by sectors such as technology, e-commerce, and banking, leading to a flurry of new office constructions.

- India's burgeoning startup ecosystem highlights an increasing appetite for office spaces. Bolstered by government initiatives, the Department for Promotion of Industry and Internal Trade (DPIIT) recognized a remarkable 1,17,254 startups by December 2023.

- The United States is also a huge market for the building and construction industry. As per the data from the US Census Bureau, in 2023, the United States spent over USD 706.1 billion on new private non-residential buildings, a significant increase from USD 596.5 billion in 2022. Moreover, the residential construction in 2023 was only USD 864.9 billion.

- In 2023, an estimated 1,469,800 housing units were authorized by building permits, 11.7% below the 2022 figure of 1,665,100. Moreover, an estimated 1,413,100 housing units were started in 2023, 9% (+-2.5%) below the 2022 figure of 1,552,600.

- In July 2024, the seasonally adjusted annual rate for privately-owned housing units authorized by building permits stood at 1,396,000. This figure represents a 4% decline from the revised June rate of 1,454,000 and a 7% drop compared to the July 2023 rate of 1,501,000.

- Germany's robust economy is fueling a demand for commercial spaces, especially high-quality, ESG-compliant office buildings, which is evident from rising prime rents. In Q3 2023, 246,000 square meters of office space were completed, with projections reaching 1.8 million sq. m by 2024. Retail space development, particularly in shopping centers, also saw consistent growth in 2023.

- Brazil's residential sector is drawing substantial private investments fueled by swift urbanization. In response to this burgeoning demand, the government reintroduced the "Minha Casa, Minha Vida" (My Home, My Life) program in February 2023, setting an ambitious goal of 2 million new projects by 2026.

- Saudi Arabia is witnessing a construction boom, highlighted by the Jeddah Central megaproject. Spearheaded by the Jeddah Central Development Company (JCDC), a subsidiary of the Public Investment Fund (PIF), this ambitious USD 20 billion project includes landmarks like a museum, opera house, and sports stadium, alongside 17,000 residential units and over 3,000 hotels. The first phase is set for completion in 2027, with further developments extending to 2030 and beyond.

- These dynamics underscore a robust demand for cement boards in both residential and commercial construction globally, with promising growth during the forecast period.

Asia-Pacific Expected to Dominate the Market

- Asia-Pacific holds a dominant position in the global cement board market, led by China. Cement boards find extensive applications in China's diverse construction activities, spanning both residential and commercial sectors.

- China is actively pursuing urbanization, aiming for a 70% urban rate by 2030. This urbanization drives a demand for more living spaces and reflects the middle class's aspirations for better living conditions. Such dynamics are set to boost the housing market and residential construction, positively influencing the cement board market.

- In Hong Kong, China, housing authorities have initiated multiple measures to kickstart the construction of affordable housing. Officials have set a target to deliver 301,000 public housing units by 2030.

- With plans to relocate 250 million rural residents to new megacities by 2025, the Chinese government's ambitious construction initiatives are set to boost the cement board market.

- In response to a struggling economy, Chinese governors are ramping up budgets for major building projects by nearly 20%. Over two-thirds of China's regions have committed to significant projects, including transportation infrastructure and industrial zones, with a combined budget exceeding CNY 12.2 trillion (USD 1.8 trillion) for 2024.

- Rising disposable incomes in China are fueling the demand for upscale commercial spaces, including malls and hotels. China stands at the forefront of shopping center development, boasting nearly 4,000 existing centers and an estimated 7,000 more by 2025. Projects like the Wuhan Fosun Bund Center T1, with construction starting in Q3 2021 and completion slated for Q4 2025, further bolster the market.

- India is set to witness a 70% surge in the availability of affordable housing. According to Invest India, the construction sector is projected to attain a valuation of USD 1.4 trillion by 2025. With forecasts suggesting that over 30% of the population will be urban dwellers by 2030, there is a pressing need for 25 million more mid-end and affordable housing units. Recent reforms, such as the Real Estate Act, GST (goods and services tax), and REITs (real estate investment trusts), aim to expedite approvals and strengthen the construction industry, driving market growth.

- South Korea is undertaking significant industrial construction ventures. A notable example is S-Oil Corp.'s ambitious Shaheen refinery-integrated petrochemical plant in Ulsan, set to finish by 2026. This facility will house the world's largest naphtha-fed steam cracker, capable of producing 1.8 million mt/year of ethylene, underscoring the project's potential to elevate industrial demand and support market growth.

- Given these dynamics, the demand for cement boards in Asia-Pacific is poised for significant growth during the forecast period.

Cement Board Industry Segmentation

The cement board market is partially fragmented in nature. The major players (not in any particular order) include James Hardie Industries PLC, Etex Group, Saint-Gobain, Johns Manville, and NICHIHA Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Increasing Adoption in Residential and Commercial Construction

- 4.1.2 Desirable Properties of Impact Resistance and Durability

- 4.1.3 Other Drivers

- 4.2 Market Restraints

- 4.2.1 High Initial Cost in Comparison to Traditional Counterparts

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 By Product Type

- 5.1.1 Fiber Cement Board (FCB)

- 5.1.2 Wood Wool Cement Board (WWCB)

- 5.1.3 Wood Strand Cement Board (WSCB)

- 5.1.4 Cement Bonded Particle Board (CBPB)

- 5.2 By Application

- 5.2.1 Flooring

- 5.2.2 Exterior and Partition Walls

- 5.2.3 Roofing

- 5.2.4 Columns and Beams

- 5.2.5 Facades, Weatherboard, and Cladding

- 5.2.6 Acoustic and Thermal Insulation

- 5.2.7 Other Applications (Prefabricated Houses, Permanent Shuttering, Fire-resistant Construction, etc.)

- 5.3 By End-user Industry

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial and Institutional

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Qatar

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Etex Group

- 6.4.2 Elementia Materials

- 6.4.3 Everest Industries Limited

- 6.4.4 James Hardie Industries PLC

- 6.4.5 Johns Manville

- 6.4.6 Knauf Gips KG

- 6.4.7 Saint-Gobain

- 6.4.8 BetonWood SRL

- 6.4.9 Cembrit Holding A/S

- 6.4.10 HIL Limited

- 6.4.11 GAF

- 6.4.12 NICHIHA Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Trends for Aesthetic Improvement

- 7.2 Other Opportunities

샘플 요청 목록