|

시장보고서

상품코드

1687438

소화관 치료제 - 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Gastrointestinal Therapeutics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

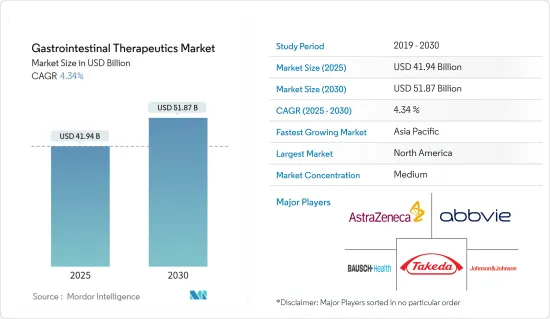

소화관 치료제 시장 규모는 2025년에 419억 4,000만 달러에 이를 것으로 추정됩니다. 예측 기간(2025-2030년)의 CAGR은 4.34%를 나타내 2030년에는 518억 7,000만 달러에 달할 것으로 예상됩니다.

소화기 질환의 신흥국 시장에 있어서의 유병률 증가, 제약 기업에 의한 연구개발 투자 증가 등의 요인이, 시장 개척을 뒷받침할 것으로 예상됩니다.

인구 사이에서 궤양성 대장염, 과민성 장 증후군, 크론병, 세리악병, 위장염 등 소화기 질환의 부담이 증가하고 있는 것이 시장 성장을 가속하는 주요 요인입니다. 예를 들어, 2023년 5월 국제 대장 질환 저널에 발표된 보고서에 따르면 일본에서는 궤양성 대장염(UC) 진단을 받은 환자가 여성에 비해 더 젊고 남성의 유병률이 높은 경향이 있는 반면, 미국에서는 그 반대의 경향이 관찰되었습니다.

게다가 2022년 7월에 NLM에 게재된 논문에 의하면, 가장 일반적인 위장질환인 GERD는 서양문화권에서는 20%의 사람이 앓았습니다. 같은 출처에 따르면 미국 내 GERD 유병률은 18.1%에서 27.8% 사이로 추정되며, 여성보다 남성의 유병률이 더 높습니다. 이와 같이, 암이나 GERD와 같은 소화관 질환의 부담이 큰 것으로부터, 효과적인 치료법에 대한 수요가 높아져 시장 성장이 촉진될 것으로 예상됩니다.

게다가 위장 관련 의약품의 연구개발에 대한 기업의 투자 증가나 시장에서의 의약품의 이용가능성을 높이는 의약품 출시 증가도 시장 성장을 뒷받침할 것으로 예상됩니다. 예를 들어, 2023년 9월 위장 건강 회사인 비반테 헬스는 새로운 투자자인 Mercato Partners가 주도한 시리즈 B 펀딩 라운드에서 3,100만 달러를 유치하여 총 4,700만 달러를 모금했습니다.

따라서 소화기 질환의 유병률 상승이나 소화기 질환 치료 개발을 위한 연구개발 활동의 활성화 등 위의 요인 덕분에 예측 기간에 걸쳐 소화관 치료제 시장의 성장을 뒷받침할 가능성이 높습니다.

소화관 치료제 시장 동향

크론병 부문은 예측 기간 동안 상당한 성장이 예상됩니다.

만성 면역 질환인 크론병은 그 특징적인 염증이 주로 소화관에 영향을 미치기 때문에 환자와 건강 관리 제공업체에게 여전히 큰 과제가되고 있습니다.의 내과적 치료는 관해의 도입과 유지를 위해 다양한 약제가 사용되고 있습니다.

세계적으로 크론병의 부담이 증가하고 있기 때문에 효과적인 치료에 대한 수요가 높아지고 이 분야의 성장을 뒷받침할 것으로 예상되고 있습니다. 예를 들어, 2023년 1월 MedLine.Gov에 게재된 기사에 따르면 크론병은 서유럽과 북미에서 가장 흔하며 인구 10만 명당 100-300명의 유병률을 보였습니다. 현재, 50만명 이상의 미국인이 이 질환에 걸려 크론병은 다른 민족의 사람들보다 북유럽의 조상을 가진 사람들과 동유럽 및 중앙유럽(아슈케나지)계 유태인들에게 더 많이 보입니다. 따라서 새로운 치료법의 대두는 유효하고 안전한 의약품이 시장에 나와 이 분야의 성장을 뒷받침할 것으로 기대됩니다.

게다가, 규제 당국에 의한 의약품 승인 증가는 크론병 환자의 치료에 사용되는 신규 치료제의 이용 가능성이 높아질 것으로 예상됩니다. 예를 들어, 2023년 10월, 일라이 릴리 앤 컴퍼니는 중등도에서 중증의 활성 크론병 성인 환자 치료를 위한 임상시험용 인터루킨-23p19 길항제인 밍키주맙을 평가하는 3상 임상시험에서 긍정적인 결과를 발표했습니다. VIVID-1로 알려진이 연구는 민키 주맙이 위약과 비교하여 주요 평가 항목 및 주요 부차 평가 항목을 달성했음을 보여 주며,이 환자 집단에 대한 유망 치료제로서의 가능성이 강조되었습니다. 크론병은 복통, 설사, 체중감소 등의 증상을 특징으로 하며 심각한 합병증을 일으킬 수 있으므로 밍키주맙과 같은 효과적인 치료제가 긴급하게 필요합니다.

따라서 크론병의 부담 증가나 제품 승인 등 위의 요인으로부터 조사 대상 부문은 예측 기간 동안 성장할 것으로 예상됩니다.

북미가 예측 기간 동안 큰 시장 점유율을 차지할 전망

북미는 소화기 질환 부담 증가, 제품 상시 증가, 기업 이니셔티브 증가 등의 요인으로 인해 예측 기간에 걸쳐 큰 시장 점유율을 차지할 것으로 예상됩니다.

인구 사이에서 궤양성 대장염과 같은 소화기 질환의 부담이 증가하고 있다는 것이 시장 성장을 가속하는 주요 요인입니다. 혹은 궤양성 대장염을 포함한 염증성 장 질환(IBD)을 앓고 있음을 강조하였습니다.

게다가 NBC 유니버설이 2023년 2월에 발표한 기사에서는 노로바이러스(노로바이러스 또는 위장 감기라고도 함)의 유행이 강조되었으며, 2023년 미국에서의 구토와 설사의 발생 건수는 1,900만-2,100만 건에 이르렀습니다. 그 결과, 465,000건의 긴급 입원과 109,000건의 입원이 발생했습니다.

게다가 소화기질환의 연구개발에 대한 정부자금 증가에 의해 신규 치료제의 개발에 주력하는 기업이 증가하여 시장개척의 추진력이 될 것으로 예상됩니다. 예를 들어, NIH가 발표한 데이터에 따르면 2022년 5월, 2022년 미국의 대장암 질환 연구 및 개발을 위해 정부가 지원한 금액은 3억 5,200만 달러로 2021년 3억 3,500만 달러에 비해 약 3.5배 증가했습니다. 또, 같은 정보원에 따르면, 크론병의 연구 개발에 대해서, 2021년의 8,800만 달러에 대해, 2022년에는 추정 9,200만 달러가 정부로부터 자금 제공되었습니다.

게다가 이 지역의 신약 상시 및 승인 증가, 제휴 및 파트너십 등 주요 전략 채용에 주력하는 기업 증가도 시장 성장에 기여하고 있습니다. 예를 들어, 2023년 10월 미국 식품의약국(FDA)은 궤양성 대장염(UC) 치료를 위해 새롭고 매우 효과적인 치료제인 미리키주맙을 승인하여 이 만성적이고 무력화되는 염증성 장 질환으로 고생하는 사람들에게 유망한 치료 방법을 제시했습니다. 또한, 2023년 8월에는 웨일 코넬 의과대학 및 뉴욕-프레즈비테리안과 공동으로 실시한 국제 3상 임상시험에서 새로 개발된 표적 치료제인 졸베툭시맙을 기존 화학요법과 함께 투여했을 때 진행성 위암 또는 위식도 접합부암 환자의 생존율이 연장되어 특정 바이오마커의 과발현을 억제한다는 사실이 밝혀졌습니다.

따라서, 소화관 치료제의 상시 증가, 소화관 질환의 높은 유병률, 자금 조달 증가, 주요 기업에 의한 기타 전략적 활동 등의 요인에 의해 조사 대상 부문은 예측 기간 중에 성장할 것으로 예상됩니다.

소화관 치료제 산업 개요

소화관 치료제 시장은 많은 시장 진출 기업이 존재하고 경쟁은 중간 정도입니다. 각 회사는 시장 포지션을 유지하기 위해 신제품 개발, 제휴, 파트너십 등의 주요 전략을 채용하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 소화기 질환의 유병률 증가

- 제약기업에 의한 R&D 투자 증가

- 시장 성장 억제요인

- 의약품 승인에 관한 엄격한 규제 기준

- 특허 만료 증가

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자/소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 약제 유형별

- 생물학적 제제/바이오시밀러

- 제산제

- 완하제

- 지사제

- 구토 방지제

- 항궤양제

- 기타 약제 유형

- 투여 형태별

- 경구용

- 비경구

- 기타 투여 형태

- 용도별

- 궤양성 대장염

- 과민성 대장 증후군

- 크론병

- 세리악병

- 위장염

- 기타 용도

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 기업 프로파일과 경쟁 구도

- 기업 프로파일

- Abbott

- Abbvie Inc.

- AstraZeneca

- Bayer AG

- GSK plc

- Johnson & Johnson(Janssen Global Services LLC)

- Pfizer Inc.

- Takeda Pharmaceutical Company Limited

- Bausch Health Companies Inc.(Salix Pharmaceuticals Inc.)

- Boehringer Ingelheim International GmbH

- Cipla Inc.

- Sebela Pharmaceuticals

제7장 시장 기회와 앞으로의 동향

KTH 25.05.07The Gastrointestinal Therapeutics Market size is estimated at USD 41.94 billion in 2025, and is expected to reach USD 51.87 billion by 2030, at a CAGR of 4.34% during the forecast period (2025-2030).

Factors such as the increasing prevalence of gastrointestinal diseases and the rising investments in research and development by pharmaceutical companies are expected to boost the market growth.

The increasing burden of gastrointestinal diseases such as ulcerative colitis, irritable bowel syndrome, Crohn's disease, celiac disease, gastroenteritis, and others among the population is the key factor driving the market growth. For instance, according to a report published by the International Journal of Colorectal Disease in May 2023, in Japan, patients diagnosed with ulcerative colitis (UC) tended to be younger and exhibited a higher prevalence among men compared to women, while the opposite trend was observed in the United States.

Additionally, as per an article published in NLM in July 2022, it was observed that GERD, the most prevalent gastrointestinal condition, affects 20% of individuals in Western culture. As per the same source, an estimated prevalence of GERD in the United States ranges between 18.1% and 27.8%, and the prevalence of GERD is higher among men than women. Thus, the high burden of GI tract diseases such as cancer and GERD is expected to increase demand for effective therapeutics approaches, thereby boosting the market growth.

Furthermore, the rising company's investment in research and development of gastro-related drugs and rising drug launches that increase the availability of the drugs in the market are also expected to fuel the market growth. For instance, in September 2023, gastrointestinal health company Vivante Health received USD 31 million in its Series B funding round led by new investor Mercato Partners, bringing its total raise to USD 47 million. Vivante provides personalized care plans to track their symptoms and connect patients with a coordinated care team, including dietitians, internists, and gastroenterologists. Similarly, in June 2023, the American Gastroenterological Association invested in Oshi Health. Oshi Health provides diagnosis and integrated care for digestive conditions.

Therefore, owing to the factors above, such as the rising prevalence of GI disorders and the increasing R&D activities for the development of gastrointestinal disease treatment, it is likely to boost the growth of the gastrointestinal therapeutics market over the forecast period. However, stringent regulatory norms regarding drug approvals and an increasing number of patent expiries are expected to impede the market growth over the forecast period.

Gastrointestinal Therapeutics Market Trends

Crohn's Disease Segment is Expected to Witness Significant Growth Over the Forecast Period

Crohn's disease, a chronic immune-mediated disorder, remains a significant challenge for both patients and healthcare providers, with its hallmark inflammation primarily affecting the digestive tract. In the medical management of Crohn's disease, various drugs are used to induce and maintain remission. For instance, infliximab and adalimumab are used to target proteins to decrease inflammation in the intestines.

The growing burden of Crohn's disease across the world is expected to create the demand for effective treatment, thereby boosting the segment growth. For instance, according to an article published in MedLine.Gov in January 2023, Crohn's disease is most common in Western Europe and North America, where it has a prevalence of 100 to 300 per 100,000 people. More than half a million Americans are currently affected by this disorder. Crohn's disease occurs more often in people of northern European ancestry and those of eastern and central European (Ashkenazi) Jewish descent than among people of other ethnic backgrounds. For reasons that are not clear, the prevalence of Crohn's disease has been increasing in the United States and some other parts of the world. Thus, the rising new and emerging treatments are expected to increase the availability of effective and safe drugs in the market, boosting segment growth.

Furthermore, the increasing drug approval by regulatory bodies is expected to increase the availability of novel therapeutics for treating Crohn's disease patients. It is anticipated to fuel the market growth over the forecast period. For instance, in October 2023, Eli Lilly and Company revealed positive results from its Phase 3 study evaluating minkizumab, an investigational interleukin-23p19 antagonist, for treating adults with moderately to severely active Crohn's disease. The study, known as VIVID-1, demonstrated that minkizumab met both co-primary and major secondary endpoints compared to placebo, underscoring its potential as a promising therapeutic agent for this patient population. Crohn's disease, characterized by symptoms such as abdominal pain, diarrhea, and weight loss, can lead to serious complications, highlighting the urgent need for effective treatments like minkizumab.

Therefore, owing to the factors above, such as the growing burden of Crohn's Disease and product approvals, the studied segment is expected to grow over the forecast period.

North America is Expected to Hold a Significant Market Share Over the Forecast Period

North America is expected to hold a significant market share over the forecast period owing to factors such as the increasing burden of gastrointestinal diseases, rising product launches, and growing company initiatives.

The increasing burden of gastrointestinal diseases such as ulcerative colitis and others among the population is the key factor driving the market growth. For instance, in December 2023, an article from US Pharm highlighted that approximately 1.6 million individuals in the United States are afflicted with inflammatory bowel disease (IBD), encompassing Crohn's disease and ulcerative colitis. These conditions are characterized by gastrointestinal tract inflammation and may manifest symptoms, including persistent diarrhea, abdominal discomfort, and hematochezia.

Additionally, an article released by NBC Universal in February 2023 underscored the prevalence of Norovirus, also known as Norovirus or stomach flu, which accounted for 19 to 21 million incidents of vomiting and diarrhea in the United States during the year 2023. This resulted in 465,000 emergency room admissions and 109,000 hospitalizations. Notably, during the winter season in 2023, there was a notable increase in cases and outbreaks, peaking in March 2023, with elevated norovirus activity persisting well into late spring.

Furthermore, the rising government funding for gastrointestinal diseases research and development is expected to increase the company's focus on developing novel treatment drugs, propelling market growth. For instance, according to the data published by NIH, in May 2022, the government-funded an estimated USD 352 million for the research and development of colorectal cancer disease in the United States in 2022, compared to USD 335 million in 2021. In addition, as per the same source, an estimated USD 92 million was funded by the government for research and development of Crohn's disease in 2022, compared to USD 88 million in 2021.

Moreover, the rising drug launches and approvals in the region and an increasing company focus on adopting key strategies such as collaboration, partnerships, and others are also contributing to the market growth. For instance, in October 2023, the US Food and Drug Administration (FDA) approved mirikizumab, a novel and highly efficacious therapy, for the treatment of ulcerative colitis (UC), presenting a promising therapeutic avenue for individuals grappling with this chronic and incapacitating inflammatory bowel ailment. Similarly, in August 2023, an international phase 3 clinical trial conducted in collaboration with Weill Cornell Medicine and NewYork-Presbyterian revealed that zolbetuximab, a newly developed targeted intervention, when administered alongside conventional chemotherapy, prolonged survival rates among patients afflicted with advanced gastric or gastroesophageal junction cancer, demonstrating overexpression of a specific biomarker.

Therefore, owing to factors such as an increase in GI drug launches, high prevalence of GI diseases, rise in funding, and other strategic activities by the key players, the studied segment is expected to grow over the forecast period.

Gastrointestinal Therapeutics Industry Overview

The gastrointestinal therapeutics market is moderately competitive, with the presence of many market players. The companies are adopting key strategies such as new product development, collaborations, partnerships, and others to retain their market position. Some market players include Abbvie Inc., AstraZeneca, Johnson & Johnson (Janssen Global Services LLC), Takeda Pharmaceutical Company Limited, and Bausch Health Companies Inc. (Salix Pharmaceuticals Inc.).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Gastrointestinal Diseases

- 4.2.2 Rising Investments in Research and Development by Pharmaceutical Companies

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Norms Regarding Drug Approvals

- 4.3.2 Increasing Number of Patent Expiries

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Drug Type

- 5.1.1 Biologics/ Biosimilars

- 5.1.2 Antacids

- 5.1.3 Laxatives

- 5.1.4 Antidiarrheal agents

- 5.1.5 Antiemetics

- 5.1.6 Antiulcer agents

- 5.1.7 Other Drug Types

- 5.2 By Dosage Form

- 5.2.1 Oral

- 5.2.2 Parenteral

- 5.2.3 Other Dosage Forms

- 5.3 By Application

- 5.3.1 Ulcerative Colitis

- 5.3.2 Irritable Bowel Syndrome

- 5.3.3 Crohn's Disease

- 5.3.4 Celiac Disease

- 5.3.5 Gastroenteritis

- 5.3.6 Other Applications

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPANY PROFILES AND COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abbott

- 6.1.2 Abbvie Inc.

- 6.1.3 AstraZeneca

- 6.1.4 Bayer AG

- 6.1.5 GSK plc

- 6.1.6 Johnson & Johnson(Janssen Global Services LLC)

- 6.1.7 Pfizer Inc.

- 6.1.8 Takeda Pharmaceutical Company Limited

- 6.1.9 Bausch Health Companies Inc. (Salix Pharmaceuticals Inc.)

- 6.1.10 Boehringer Ingelheim International GmbH

- 6.1.11 Cipla Inc.

- 6.1.12 Sebela Pharmaceuticals