|

시장보고서

상품코드

1852089

치과 임플란트 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Dental Implants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

티타늄의 기계적 신뢰성은 2024년에 85.1% 시장 점유율을 획득했지만, 지르코니아의 뛰어난 연조직 반응성이 2030년까지 연평균 복합 성장률(CAGR) 10.8%로 채택이 증가하고 있습니다.

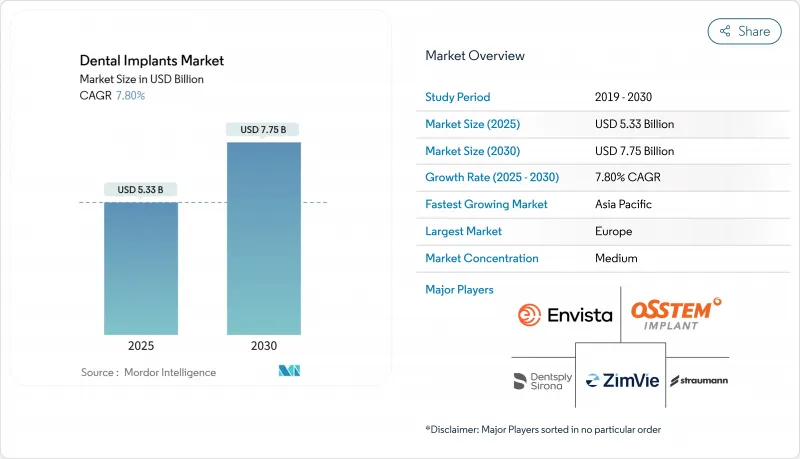

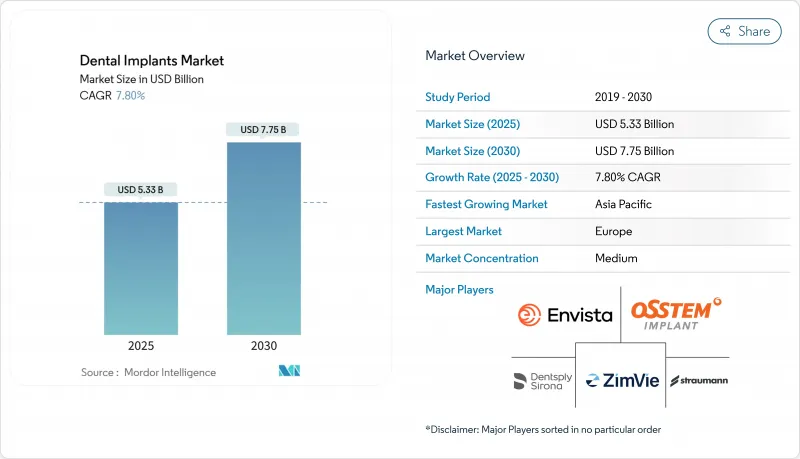

치과 임플란트 산업의 2024년 시장 규모는 53억 3,000만 달러에 달했고, 2030년에는 CAGR 7.8%로 성장하여 77억 5,000만 달러로 확대될 것으로 예측됩니다. 나노스케일의 표면공학에 의존하는 보다 치유의 빠른 즉각 부하 프로토콜을 중심으로 기세가 증가하고 있습니다. 이 전환은 치료 사이클을 단축하고 클리닉의 의자 용량을 확장하지 않고 더 많은 경우에 대응할 수 있습니다. 금속 과민증에 대한 우려와 환자의 미적 기대로부터, 티타늄에서 지르코니아로의 꾸준한 이행이 진행되어 세라믹 가공을 대규모로 실시할 수 있는 제조업체에 제품의 화이트 스페이스가 퍼지고 있습니다. 유럽에서 보험 상환을 확대하고 다른 지역에서의 적용 범위를 선택적으로 확대하는 것은 환자의 접근을 넓히고 있지만 가격만으로 경쟁하는 것이 아니라 픽스처에 디지털 계획 소프트웨어와 수술 후 케어 키트를 번들로 마진을 지키려는 공급업체도 뒷받침하고 있습니다. 구강내 스캐닝, CBCT, CAD/CAM 기술을 전면적으로 도입하고 있는 클리닉에서는 증례 수용율의 향상이 보고되고 있어 임플란트 제조업체는 스캐너와 치료 계획 플랫폼을 장기적인 하드웨어 판매에의 전략적 게이트웨이로 자리 매김하고 있습니다. 이와 병행하여 AI에 의한 진단과 로봇에 의한 임베디드수술에 대한 관심도 높아지고 있으며, 이러한 툴을 일관된 워크플로우에 통합할 수 있는 기업들은 경쟁 기준을 재설정하기 시작했습니다.

세계 치과 임플란트 시장 동향과 통찰

새로운 표면 처리를 가능하게 하는 즉시 하중 임플란트 채택 확대

즉각 하중 프로토콜은 CAGR 11.7%로 진전되어 시장 전체를 크게 웃돌고 있습니다. 임상 수준에서 장기적인 뼈 리모델링을 손상시키지 않으면 서 피브린 부착을 촉진할 수있는 표면 화학이 성공의 열쇠를 잡고 있습니다. 최신 세대의 나노 텍스처 코팅은 이러한 이면성을 실현하여 기능적 치유 기간을 수개월에서 수주간 단축하여 클리닉이 당일 복구를 홍보할 수 있도록 하고 있습니다. 2차적인 의미는 환자 1인당 약속의 수가 줄어들어 진료 일정의 효율성을 향상시키고 의자의 잠재적인 용량을 확보하는 것입니다.

디지털 치과 워크플로우 통합으로 임플란트 사례 수 증가

구강 스캐너, CBCT 이미지, CAD/CAM 설계를 활용한 디지털 치료 계획은 표준 치료 진단을 구성하는 것을 재정의하고 있습니다. 완전히 디지털화된 워크플로우로 전환된 클리닉에서는 환자가 수술 전에 결과를 시각화할 수 있기 때문에 사례 수락이 2자리 증가한 것으로 보고되는 경우가 많습니다. 사실, 현재 일부 제조업체는 특정 골밀도에 해당하는 스레드 모양을 미세 조정하기 위해 익명화된 스캔 데이터를 수집하고 있으며 설치된 스캐너는 실시간 R&D 자산이 되고 있습니다.

2단계 도시에서 훈련된 임플란트 전문의 부족

인도와 중국에서는 대도시 지역 이외의 임플란트 전문공급 부족이 심각하고 치료 건수에 제약이 있습니다. 장비 공급업체는 가이드 수술 키트, 사전 구성된 드릴링 프로토콜, 원격 지도자 지원을 통합한 턴키 시스템으로 지원합니다. 이 모델은 예측 가능한 결과를 내는 데 필요한 능력의 임계값을 효과적으로 낮추고 지리적 보급을 가속화합니다. 투자자들은 지역 수요의 선행 지표로서 교육 프로그램의 수강자 수를 추적하고 있으며, 교육에 대한 조기 자본 투하가 이러한 지역이 중요한 도입 임계값을 초과할 때 선행자 이익을 초래할 수 있음을 시사합니다.

부문 분석

2024년 임플란트 수익의 76%는 픽스처가 차지하지만, 시장이 매스커스터마이제이션으로 축족을 옮기고 있기 때문에 어버트먼트는 CAGR9.2%로 진전하고 있습니다. 디지털 라이브러리를 통해 기술공사는 에머전스 프로파일과 잇몸 심미성을 최적화하는 환자별 어버트먼트를 설계할 수 있습니다. 현실적인 귀결로 여러 거점을 가진 클리닉의 조달 팀은 픽스처와 보철 구성요소의 개별 계약을 협상하는 것이 늘어나고 있으며, 지금까지 단일 벤더로 정리된 것이 분리되어 있습니다. 구성요소 간의 정확한 적합성을 입증할 수 없는 공급업체는 이러한 모듈 구매 프레임워크에서 제거될 위험이 있습니다.

일부 학술적 메타 분석은 표면 개질 지르코니아와 전통적인 티타늄 사이에 뼈와 임플란트의 접촉에 통계적으로 의미있는 차이가 없다는 것이 밝혀졌으며, 전체 세라믹 픽스처에 대한 마지막 큰 임상적 논거가 무너져 왔습니다. 현재 진행 중인 종단적 연구를 통해 임플란트 주위의 연조직의 안정성이 계속 확인되면 보험 회사는 결국 보험료의 차이를 조정하여 지르코니아의 성장 노선을 더욱 견고하게 만들 수 있습니다. 현재, 조기 진입 브랜드는 지르코니아를 엄격한 의학적 개선이 아닌 라이프 스타일 업그레이드로 자리매김함으로써 더 높은 마진을 획득하고 있습니다.

지역 분석

2024년 세계 매출의 34%를 차지한 유럽의 성숙한 임플란트 섹터는 프리미엄 세라믹에 대한 높은 지불 의향과 지속 교육 기관의 치밀한 네트워크가 특징입니다. 시장 규모 전망은 양호하며, 업계 공개에 따르면 독일만으로도 2025년에는 10억 달러 이상에 달할 것으로 예상되고 있습니다. 보험 상환 제도에서는 임플란트 주위의 유지 보수 프로토콜의 증거가 점점 의무화되고 있기 때문에 공급업체는 현재 각 임플란트에 후속 키트를 번들하고 수술 후 관리를 임베디드 기능으로 재구성하고 있습니다. 이 번들은 임상의의 컴플라이언스에 대한 마찰을 줄이고 클리닉을 자체 소모품에 미묘하게 가두어 공급업체의 끈적 끈적성을 향상시킵니다.

아시아태평양의 치과 임플란트 시장 규모는 2025년부터 2030년에 걸쳐 CAGR 9.9%로 성장할 것으로 예측되며, 다른 모든 지역을 능가할 것으로 예측됩니다. 중국, 인도, 일본이 판매량을 견인하고 있지만 규제 경로가 다르기 때문에 미묘한 업스트림가 필요합니다. 특히 해외에서 수술을 받고 현지에서 소모품을 구입하는 것을 선호하는 의료 관광객에게 대응하기 위해 지역 유통업체가 국경을 넘은 전자상거래에 투자하고 있다는 것입니다. 이러한 이중 수요 패턴은 재고 과제를 야기하지만, 민첩한 제조업체는 분산형 3D 프린팅 허브를 통해 이를 극복하고 과잉 재고 없이 리드 타임을 단축할 수 있습니다.

북미의 인구동태의 고령화는 내구 소비재 수요를 지지하고 있습니다. 미국에서는 2030년까지 65세 이상의 노인이 18세 미만을 넘어 1억 5,000만명 이상의 미국인이 적어도 1개의 치아를 잃고 있습니다. 연간 약 100만개만 임플란트가 임베디드되어 있기 때문에 잠재적인 보급률은 여전히 큽니다. 예를 들어, AI 주도 진단 도구를 통합한 클리닉에서는 치료 계획 수락이 빨라졌다고 보고되었으며, 소프트웨어 채택이 치료 건수를 증가시키고 그것이 추가 소프트웨어 업그레이드의 재원이 되는 선순환이 강화되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 새로운 표면 처리가 가능하게 하는 즉시 하중 임플란트의 채택 확대

- 디지털 치과 워크플로우 통합으로 임플란트 케이스 수 증가

- 국내 임플란트 상환제도 확대

- 임플란트 주위염의 유행이 대체 임플란트의 매출을 견인

- 심미성을 중시하는 환자층에 있어서의 임플란트의 대두

- 치과 의료 서비스 기관의 통합에 의한 일괄 조달의 활성화

- 시장 성장 억제요인

- Tier 2 도시의 임플란트 전문의 부족

- 개발도상국에서의 인식 부족

- 티타늄 수요를 억제하는 금속과민증 소송

- 신제품 상시를 막는 규제 인증의 지연

- 공급망 분석

- 기술의 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 구성요소별

- 비품

- 골내 임플란트

- 골막하 임플란트

- 경골막 임플란트

- 점막내 임플란트

- 지대주

- 비품

- 소재별

- 티타늄 임플란트

- 지르코늄 임플란트

- 설계별

- 테이퍼 임플란트

- 평행 벽 임플란트

- 수술 유형별

- 즉각 하중 임플란트 수술

- 종래의 절차

- 최종 사용자별

- 치과 병원 & 클리닉

- 치과기공소

- 학술기관 및 연구기관

- 지리

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Institut Straumann AG

- Dentsply Sirona Inc.

- ZimVie Inc

- Osstem Implant Co., Ltd.

- Envista Holdings(Nobel Biocare Services AG)

- Dentium Co., Ltd.

- Thommen Medical AG

- Ivoclar Vivadent AG

- Solventum Corporation

- Ziacom Medical SL

- BioHorizons IPH Inc.

- Bicon LLC

- MegaGen Implant Co., Ltd.

- Kyocera Medical Corporation

- GC Corporation

- BEGO GmbH & Co. KG

- Blue Sky Bio LLC

- Cortex Dental Implants Industries Ltd.

- DIO Corporation

- AlphaBio Tec.

제7장 시장 기회와 장래의 전망

SHW 25.11.19Titanium's mechanical reliability remains unmatched having 85.1% market share in 2024, yet zirconia's superior soft-tissue response is driving adoption with 10.8 % CAGR by 2030.

The dental implants industry is valued at USD 5.33 billion in 2024 and is expected to advance to USD 7.75 billion by 2030, reflecting a compound annual growth rate (CAGR) of 7.8%. Momentum is building around faster-healing immediate-load protocols that rely on nanoscale surface engineering, a shift that shortens treatment cycles and allows clinics to accommodate more cases without expanding chair capacity. A steady move from titanium toward zirconia, driven by concerns about metal hypersensitivity and by patients' aesthetic expectations, has opened product white space for manufacturers that can master ceramic processing at scale. Broader reimbursement in Europe and selective coverage expansions elsewhere are widening patient access, but they are also pushing suppliers to defend margins by bundling fixtures with digital planning software and post-operative care kits rather than competing on price alone. Clinics that fully adopt intraoral scanning, CBCT, and CAD/CAM technology are reporting higher case-acceptance rates, prompting implant makers to position scanners and treatment-planning platforms as strategic gateways into long-term hardware sales. In parallel, interest in AI-assisted diagnostics and robotic placement systems is rising, and companies that can weave these tools into a cohesive workflow are beginning to reset the competitive baseline.

Global Dental Implants Market Trends and Insights

Growing Adoption of Immediate-Load Implants Enabled by Novel Surface Treatments

Immediate-load protocols are progressing at an 11.7% CAGR, materially faster than the overall market. At a clinical level, success hinges on surface chemistry that can accelerate fibrin attachment without compromising long-term bone remodeling. The latest generation of nano-textured coatings is delivering that duality, shortening functional healing windows from months to weeks and enabling practices to advertise same-month restorations. A second-order implication is that practice scheduling efficiency improves because fewer appointments are required per patient, which releases latent chair capacity; many multi-site dental service organizations are translating that capacity into incremental hygiene visits, effectively cross-subsidizing lower implant unit margins.

Integration of Digital Dentistry Workflows Boosting Implant Case Volumes

Digital treatment planning, powered by intraoral scanners, CBCT imaging and CAD/CAM design, is redefining what constitutes standard-of-care diagnostics. Practices that migrate to fully digital workflows often report double-digit increases in case acceptance because patients can visualize outcomes before surgery. A deeper implication is that data captured during these digital encounters creates a feedback loop for iterative product improvement; in fact, some manufacturers now collect anonymized scan data to fine-tune thread geometry for specific bone densities, turning the installed scanner base into a real-time R&D asset.

Shortage of Trained Implantologists in Tier-2 Cities

The supply deficit of implantologists outside major metropolitan areas is acute in India and China, constraining procedure volumes. Equipment vendors are responding with turnkey systems that integrate guided surgery kits, pre-set drilling protocols and remote mentor support. This model effectively lowers the competency threshold required to deliver predictable outcomes, which in turn accelerates geographical diffusion. Investors are tracking training program enrollments as a leading indicator for provincial demand, suggesting that early capital deployment in education may yield first-mover advantages when those regions cross critical adoption thresholds.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of National Implant Reimbursement Schemes

- Prevalence of Peri-implantitis Driving Replacement Implant Sales

- Lack of Awareness in Developing Countries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fixtures account for 76% of implant revenue in 2024, but abutments are advancing at a 9.2% CAGR as the market pivots toward mass-customization. Digital libraries now enable laboratories to design patient-specific abutments that optimize emergence profiles and gingival aesthetics. A practical consequence is that procurement teams at multi-site clinics increasingly negotiate separate contracts for fixtures and prosthetic components, decoupling what had been a single-vendor bundle. Suppliers that cannot prove cross-component precision fit risk being excluded from these modular purchasing frameworks.

Several academic meta-analyses have found no statistically meaningful difference in bone-to-implant contact between surface-modified zirconia and conventional titanium, eroding the last major clinical argument against full-ceramic fixtures. Should ongoing longitudinal studies continue to confirm peri-implant soft-tissue stability, insurers may eventually adjust premium differentials, further solidifying zirconia's growth path. For now, early mover brands capture higher margins by positioning zirconia as a lifestyle upgrade rather than a strictly medical improvement.

The Dental Implants Market Report is Segmented by Component (Fixture [Endosteal Implants, and More] and Abutment), Material (Titanium Implants and Zirconium Implants), Design (Tapered Implants and Parallel-Walled Implants), Procedure Type (Immediate-Load Implant and Conventional), End User (Dental Hospitals & Clinics, and More), Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

With 34% of global revenue in 2024, Europe's mature implant sector is characterized by high willingness to pay for premium ceramics and a dense network of continuing-education institutes. Market size visibility is strong; Germany alone is expected to remain above USD 1 billion in 2025 based on industry disclosures. Because reimbursement systems increasingly mandate evidence of peri-implant maintenance protocols, suppliers now bundle follow-up kits with each implant, re-framing post-operative care as a built-in feature. That bundling reduces compliance friction for clinicians and subtly locks practices into proprietary consumables, fortifying vendor stickiness.

Asia-Pacific's dental implants market size is projected to post a 9.9 % CAGR from 2025 to 2030, outpacing all other regions. China, India and Japan drive volume, yet divergent regulatory pathways require nuanced commercial playbooks. Notably, regional distributors are investing in cross-border e-commerce to serve medical tourists who prefer scheduling surgeries abroad but purchasing consumables locally. This dual-track demand pattern creates inventory challenges that agile manufacturers can exploit through decentralized 3D printing hubs, reducing lead times without over-stocking.

North America's aging demographic underpins durable demand. By 2030, individuals aged 65 plus will exceed those under 18 in the United States, and more than 150 million Americans are missing at least one tooth. With only about one million implants placed annually, latent penetration remains vast. Technology adoption accelerates market capture; for instance, practices that integrate AI-driven diagnostic tools report faster treatment plan acceptance, reinforcing a virtuous cycle where software adoption boosts procedure volumes, which then finances further software upgrades.

- Straumann Group

- Dentsply Sirona

- ZimVie

- Osstem Implant Co., Ltd.

- Envista

- Dentium Co., Ltd.

- Thommen Medical

- Ivoclar Vivadent

- Solventum Corporation

- Ziacom Medical SL

- BioHorizons IPH Inc.

- Bicon

- MegaGen Implant Co., Ltd.

- Kyocera Medical Corporation

- GC Corporation

- BEGO GmbH & Co. KG

- Blue Sky Bio LLC

- Cortex Dental Implants Industries Ltd.

- DIO

- AlphaBio Tec.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of Immediate-Load Implants Enabled by Novel Surface Treatments

- 4.2.2 Integration of Digital Dentistry Workflows Boosting Implant Case Volumes

- 4.2.3 Expansion of National Implant Reimbursement Schemes

- 4.2.4 Prevalence of Peri-implantitis Driving Replacement Implant Sales

- 4.2.5 Rise of Implants Among Aesthetics-Driven Patient Segments

- 4.2.6 Consolidation of Dental Service Organizations Elevating Bulk Procurement

- 4.3 Market Restraints

- 4.3.1 Shortage of Trained Implantologists in Tier-2 Cities

- 4.3.2 Lack of Awareness in Developing Countries

- 4.3.3 Metal Hypersensitivity Litigations Curtailing Titanium Demand

- 4.3.4 Regulatory Certification Delays Hindering New Product Launches

- 4.4 Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Fixture

- 5.1.1.1 Endosteal Implants

- 5.1.1.2 Subperiosteal Implants

- 5.1.1.3 Transosteal Implants

- 5.1.1.4 Intramucosal Implants

- 5.1.2 Abutment

- 5.1.1 Fixture

- 5.2 By Material

- 5.2.1 Titanium Implants

- 5.2.2 Zirconium Implants

- 5.3 By Design

- 5.3.1 Tapered Implants

- 5.3.2 Parallel-Walled Implants

- 5.4 By Procedure Type

- 5.4.1 Immediate-Load Implant Procedure

- 5.4.2 Conventional Procedure

- 5.5 By End User

- 5.5.1 Dental Hospitals & Clinics

- 5.5.2 Dental Laboratories

- 5.5.3 Academic & Research Institutes

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Institut Straumann AG

- 6.3.2 Dentsply Sirona Inc.

- 6.3.3 ZimVie Inc

- 6.3.4 Osstem Implant Co., Ltd.

- 6.3.5 Envista Holdings (Nobel Biocare Services AG)

- 6.3.6 Dentium Co., Ltd.

- 6.3.7 Thommen Medical AG

- 6.3.8 Ivoclar Vivadent AG

- 6.3.9 Solventum Corporation

- 6.3.10 Ziacom Medical SL

- 6.3.11 BioHorizons IPH Inc.

- 6.3.12 Bicon LLC

- 6.3.13 MegaGen Implant Co., Ltd.

- 6.3.14 Kyocera Medical Corporation

- 6.3.15 GC Corporation

- 6.3.16 BEGO GmbH & Co. KG

- 6.3.17 Blue Sky Bio LLC

- 6.3.18 Cortex Dental Implants Industries Ltd.

- 6.3.19 DIO Corporation

- 6.3.20 AlphaBio Tec.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment