|

시장보고서

상품코드

1910530

염산 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Hydrochloric Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

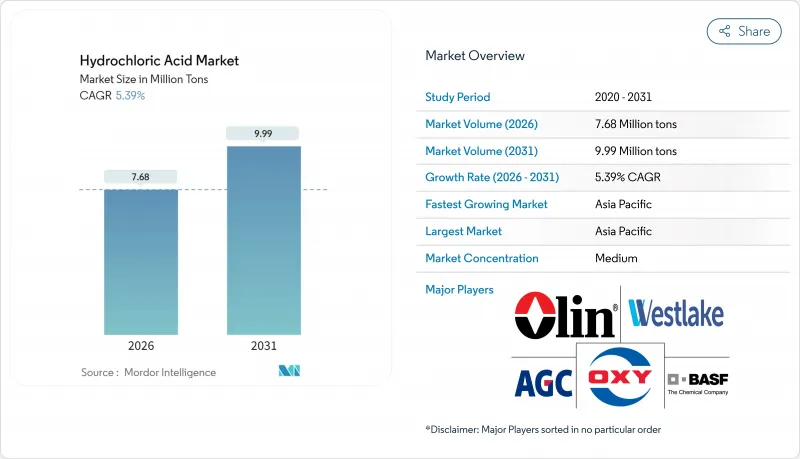

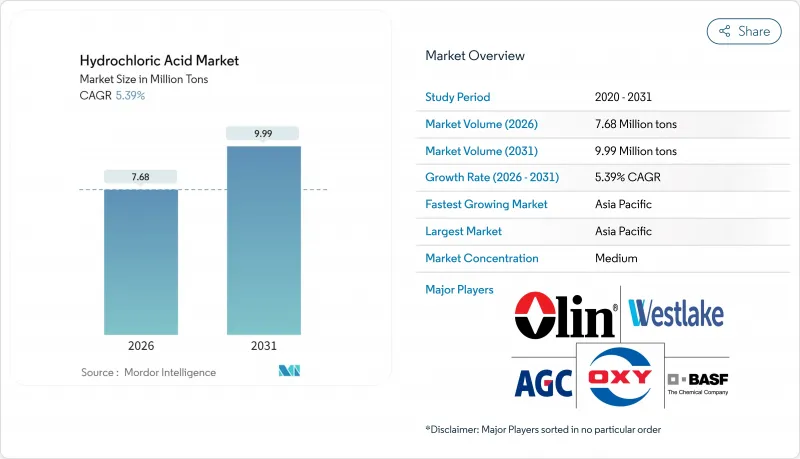

염산 시장 규모는 2026년 768만 톤으로 추정되며, 2025년 729만 톤에서 성장한 수치입니다. 2031년 999만톤으로 성장할 전망이며, 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 5.39%를 나타낼 전망입니다.

석유 및 가스정의 자극처리, 반도체 제조, 수처리, 무수한 중간체 합성에 있어서 본 화합물의 유용성은 세계 수요에 견고한 지지를 받고 있습니다. 공급의 회복력은 염산이 담당하는 이중 역할에서 유래합니다. 즉, 전용 플랜트에 있어서의 주요 제품인 동시에, 염소 알칼리 전해 장치의 제품별이기도 하기 때문에 생산자는 가성소다와 염소의 사이클 변동에 유연하게 대응할 수 있는 것입니다. 멕시코 걸프 지역의 조업 정지나 아시아 반도체 확장에 의해 스팟 수요가 흡수될 때 단기적인 박박이 발생하지만 통합 생산자는 규모의 경제성, 원료의 안정 공급, 분산형 물류 네트워크를 배경으로 장기 계약 시장에서의 우위성을 유지하고 있습니다.

세계 염산 시장 동향과 전망

석유 및 가스이 자극 수요의 급증

비 재래식 석유 및 가스 저류층의 개발로 염산 시장은 분획 및 매트릭스 산 처리 프로그램에 확고한 기반을 구축하고 있습니다. 오퍼레이터는 탄산염의 용해, 폐색된 천공공의 재개방, 갱정 수명의 연장을 목적으로 15-28%의 산농도를 사용하고 있습니다. 퍼미언 분지 및 오만에서의 현장 시험은 미처리 오프셋 갱정에 비해 18% 높은 유량을 확인했습니다. 유화산 및 지연산의 화학기술에 의해 고온·심부 지층에서의 작업이 가능하게 되어, 종래는 과제로 여겨지고 있던 저류층에 대한 수요가 확대하고 있습니다. 통합 서비스 기업은 현재 부식 방지제, 철분 제어제 및 계면활성제를 포장하고 있으며, 이들은 우물 비용 항목을 증가시키지만, 매트릭스 침투 효율을 향상시키고 간접적으로 우물당 염산 소비량을 밀어 올립니다. 셰일 생산자가 자연감쇠곡선을 상쇄하기 위한 증산기술을 도입하는 가운데 신규 완성 우물수는 감소하고 있음에도 불구하고 기준선 구매량은 증가하고 있으며, 적어도 2029년까지 수량 성장이 지속될 것으로 전망됩니다.

수처리 및 식품 가공의 위생 요구

지방 자치 단체와 식품 가공업자는 pH 조정과 이산화 염소 생성을 위해 염산의 채택을 계속하고 있습니다. 이는 정상 투여량에서 염산이 염소산염 또는 브롬산염의 부산물을 남기지 않기 때문입니다. 호주 식수 가이드라인은 응집·연화 처리에 대한 염산 사용이 규정되어 있으며, 세계의 규제상의 수용을 반영하고 있습니다. 식육가공 및 유제품 라인에서는 전해수 시스템이 소금과 묽은 염산을 조합하여 현장에서 차아염소산을 생성합니다. 이것은 60초 미만에서 5 로그의 박테리아 감소를 실현하고 잔류 염화물 농도를 1ppm 미만으로 억제하므로 클린 라벨의 요구를 충족시킵니다. 소규모 가공업자는 스키드 마운트형 전해 장치를 채택하여 필요에 따라 10-15%의 염산을 생성함으로써 포장산의 수송 비용(최대 150달러/톤)을 삭감하고 있습니다.

근로자의 안전과 환경 독성에 관한 규제

미국 노동안전보건국(OSHA)이 15분간 허용폭로 한계를 2ppm으로 엄격화함으로써 제철소와 식품공장에서는 국소배기환기설비와 내산성 바닥재의 갱신이 요구되어 1거점당 20만-50만 달러의 컴플라이언스 관련 설비 투자가 증가하고 있습니다. 유럽화학물질청 후보 리스트 선정 프로세스에 의해 염화물 함유량이 많은 폐기물류가 정사의 대상이 되고, 생산자는 제조 공정에 걸친 책임 있는 관리를 실증하거나 인가 취득의 장벽에 직면하게 됩니다. 독일과 이탈리아의 소규모 아연 도금업체는 노후화된 자사 탱크를 개조하는 대신 산세 공정을 제3자의 위탁업체에 외주하게 되어 직접적인 산 구입량을 삭감하고 있습니다.

부문 분석

산업용 등급 제품은 강재 산세, 알루미나 분해, 벌크 유기 합성에서 주력 시약으로 2025년 출하량의 52.90%를 차지했습니다. 이 부문은 고순도 하류 제품의 경기 순환 연화로부터 염산 시장을 보호했습니다. 2024년의 반도체 조정기에서도 건설용 강재의 수주가 공업용 그레이드의 출하량을 플러스로 유지한 것입니다. 33-35% 농도의 등급은 특히 내륙 유전에서 산성도 단위당 수송 비용이 조달처를 결정하는 틈새 시장에서 수요를 유지하고 있습니다. 초고순도품은 공급량의 불과 4.14%이면서, 상품그레이드의 12배를 넘는 프리미엄 가격에 의해 총가치의 18%를 차지하고 있습니다. 아시아의 팹 확장을 기반으로 초고순도 염산 시장 규모는 CAGR5.71%로 성장을 지속하여 2031년에는 389천톤에 이를 전망입니다.

앞면의 숫자 뒤에서 학년의 계층 구조는 유동적입니다. 유럽 3 거점에 있어서 에너지 절약형 막식 셀로의 개수에 의해 변동비를 28% 삭감해, 신규 설비 투자 없이 공업용 그레이드로부터 전자 그레이드에의 전략적 병목 해소를 실현했습니다. 데노라의 바이폴라 플레이트 전극은 35% 염산 1톤당 비 소비 전력을 2,000kWh로 감소시켜 잉여 산업용 스트림의 등급업 여지를 개척했습니다. 통합 정유소에서는 진공 증류 정제탑도 도입되어, 종래는 중화 폐기산으로서 취급되고 있던 것으로부터 가치를 회수하고 있습니다.

염산 시장 보고서는 등급별(공업용, 농축, 초고순도), 최종 사용자 산업별(화학, 석유 및 가스, 철강 및 금속, 식품 및 음료, 섬유 및 피혁, 기타 최종 사용자 산업), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)으로 분류되어 있습니다. 시장 예측은 수량(톤) 단위로 제공됩니다.

지역별 분석

아시아태평양의 주도적 지위는 장강 델타와 주강 델타로 퍼지는 통합 염소 알칼리망으로 인한 것입니다. 이 지역에서는 자사 소비용 염산이 염화비닐, 폴리카보네이트, 에피클로로히드린의 제조 라인에 공급되고 있습니다. 중국의 이중 치환 프로그램에 의해 수은 전해조는 폐지되었지만, 동시에 연간 300만 톤 이상의 염산 제품별을 낳는 막 분리 프로젝트가 승인되어 지역의 자급 체제가 확립되었습니다. 인도의 Atur사에 의한 투자로 100톤/일의 시판 염산이 추가되어 서인도 지역의 고운임인 걸프 수입에 대한 의존도가 저하되었습니다. 한국과 대만에서는 반도체 생산지수에 연동한 장기계약에 의해 고순도 염산을 조달하고 있으며, 벌크화학제품에서는 드문 헤지 구조가 되고 있습니다.

북미에서는 증산 기술에 의한 석유 회수 캠페인이 안정된 프랙처링산 수요를 낳고 꾸준한 성장을 계속하고 있습니다. 허리케인 아이다는 취약성을 드러냈습니다. 3도에 걸친 상륙으로 미국 걸프 지역의 염소 알칼리 명목 생산 능력의 80% 이상이 정지했고, 스팟 가격 지수는 2주간 부족해 40% 급등했습니다. 대응책으로서 지역 분산이 진행되고 있습니다. Chloram Solutions는 애리조나 주 카사 그란데에 7,000만 달러의 막 공장을 건설하여 서부 석유 화학 및 광업 클러스터에 공급하기 시작했습니다. 에너지 비용에 제약을 받는 유럽에서는 PFAS 수지 재생이나 의약품 중간체 등 고부가가치 용도로의 전환이 진행되고 있습니다. 앤트워프 로테르담을 통한 수입량은 2025년 12% 증가했으며 독일 전해장치가 가동을 억제한 시기에는 캐나다산이 계절적인 공급 부족을 보충했습니다. 동유럽의 강재 아연 도금업체는 여전히 범용품 등급을 조달하고 있지만, 염화물 배출 규제의 강화에 대응하기 위해 제로 배수식 산세 설비에 대한 투자를 진행하고 있습니다. 남미 및 중동 및 아프리카은 광업, 오일 샌드, 해수 담수화 프로젝트가 증가함에 따라 생산량이 작지만 성장하는 경향이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 석유 및 가스 유정 자극(Well-Stimulation) 수요 급증

- 수처리 및 식품 가공에 있어서의 위생 요구

- 첨단 공정 반도체 노드 식각용 반도체 등급(HCL) 수요

- PFAS 제거 수지 재생 요건

- 리튬 이온 배터리 재활용 침출 화학

- 시장 성장 억제요인

- 근로자의 안전 및 환경독성에 관한 규제

- 염소-알칼리(Chlor-Alkali) 부산물 가격 변동성

- 산세(Pickling) 공정 내 유기산으로의 대체 현상

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 등급별

- 산업용

- 농축용

- 초고순도

- 최종 사용자 업계별

- 화학

- 석유 및 가스

- 철강 및 금속

- 식음료

- 섬유 및 피혁

- 기타 최종 사용자 산업

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/순위 분석

- 기업 프로파일

- AGC Inc.

- BASF SE

- Coogee

- Covestro AG

- Detrex Corporation

- DONGYUE GROUP

- ERCO Worldwide

- Ercros SA

- INEOS Group

- Jones-Hamilton Co.

- Merck KGaA

- Occidental Petroleum Corporation(OxyChem)

- Olin Corporation

- TOAGOSEI CO.,LTD.

- Vynova Group

- Westlake Corporation

제7장 시장 기회와 장래의 전망

SHW 26.01.26Hydrochloric Acid Market size in 2026 is estimated at 7.68 Million tons, growing from 2025 value of 7.29 Million tons with 2031 projections showing 9.99 Million tons, growing at 5.39% CAGR over 2026-2031.

The compound's utility in oil-and-gas well stimulation, semiconductor fabrication, water treatment, and countless intermediate syntheses places a durable floor under global demand. Supply resilience derives from the dual role hydrochloric acid plays: it is both a primary product in dedicated units and a co-product of chlor-alkali electrolyzers, giving producers flexibility to respond to shifts in caustic-soda and chlorine cycles. Short-term tightness appears whenever Gulf-Coast outages or Asian semiconductor expansions absorb spot volumes, yet integrated producers continue to dominate long-term contracts thanks to scale economics, secure feedstock access, and distributed logistics networks.

Global Hydrochloric Acid Market Trends and Insights

Oil and Gas Well-Stimulation Demand Surge

Unconventional oil and gas reservoir development keeps the hydrochloric acid market firmly anchored to fracturing and matrix-acidizing programs. Operators employ 15%-28% acid concentrations to dissolve carbonates, reopen plugged perforations, and extend well life; field trials in the Permian and in Oman show 18% higher flow rates versus untreated offsets. Emulsified-acid and retarded-acid chemistries allow work in high-temperature, deep formations, pushing demand into reservoirs once considered too challenging. Integrated service companies now bundle corrosion inhibitors, iron controllers, and surfactants that raise well-cost line items but improve matrix penetration efficiency, indirectly lifting per-well HCl consumption. As shale producers pursue enhanced oil recovery to offset natural decline curves, baseline purchasing volumes rise despite fewer new completions, sustaining volume growth through at least 2029.

Water-Treatment and Food-Processing Hygiene Needs

Municipal utilities and food processors continue adopting HCl for pH adjustment and chlorine-dioxide generation because the acid leaves no chlorate or bromate by-products at typical dosing rates. Australia's drinking-water guidelines codify its use for coagulation and softening, reflecting worldwide regulatory acceptance. In meat-packing and dairy lines, electrolyzed-water systems combine salt and dilute HCl to form on-site hypochlorous acid that delivers five-log bacterial reductions in under 60 seconds while leaving sub-1 ppm residual chloride, satisfying clean-label expectations. Smaller processors embrace skid-mounted electrolyzers that generate 10-15% HCl on demand, cutting transport-cost premiums of up to USD 150 per ton for packaged acid.

Worker-Safety and Environmental-Toxicity Regulations

OSHA's tightened permissible-exposure limit of 2 ppm over 15 minutes compels steel mills and food plants to upgrade local exhaust ventilation and acid-proof flooring, raising compliance capex by USD 200,000-USD 500,000 per site. The European Chemical Agency's candidate-list process channels scrutiny toward chloride-rich waste streams, obliging producers to demonstrate cradle-to-gate stewardship or face authorization hurdles. Smaller galvanizers in Germany and Italy now outsource pickling to third-party tollers rather than retrofit aging on-site tanks, trimming direct acid purchases.

Other drivers and restraints analyzed in the detailed report include:

- Semiconductor-Grade HCl for Advanced Node Etching

- PFAS-Removal Resin Regeneration Requirements

- Chlor-Alkali Co-Product Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Industrial-grade product anchored 52.90% of 2025 shipments as the workhorse reagent for steel pickling, alumina digestion, and bulk organic synthesis. The segment cushioned the hydrochloric acid market against cyclical softness in high-purity downstreams: even during 2024's semiconductor correction, construction steel orders kept industrial-grade volumes positive. Concentrated 33%-35% grades retain niche appeal where freight cost per unit of acidity dictates sourcing, especially in inland oilfields. Ultra-high-purity supply, although just 4.14% of tonnage, now captures 18 % of total value thanks to premium pricing that exceeds commodity grades by 12-fold. The hydrochloric acid market size for ultra-high-purity is projected to reach 389 kt in 2031 on a 5.71% CAGR anchored in Asia's fab expansions.

Behind headline numbers, the grade hierarchy is fluid. Energy-efficient membrane-cell retrofits at three European sites shaved variable cost by 28%, enabling strategic debottlenecking from industrial to electronic quality without new greenfield units. De Nora's bipolar-plate electrodes reduced specific power consumption to 2 000 kWh per ton of 35% HCl, opening space to upgrade surplus industrial streams. Integrated refineries also deploy vacuum-distillation polishing columns, capturing value from what was formerly neutralized waste acid.

The Hydrochloric Acid Market Report is Segmented by Grade (Industrial, Concentrated, and Ultra-High Purity), End-User Industry (Chemical, Oil and Gas, Steel and Metallurgy, Food and Beverage, Textiles and Leather, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific's leadership stems from the integrated chlor-alkali grids along the Yangtze and Pearl River Deltas, where captive hydrochloric acid volumes feed vinyl chloride, polycarbonate, and epichlorohydrin lines. China's dual-replacement program has shut mercury-cell units yet simultaneously green-lighted membrane projects topping 3 million tpa HCl co-product, locking in regional self-reliance. India's Atul Ltd. investment added 100 TPD of merchant acid, cutting western-India's dependence on high-freight Gulf imports. Korea and Taiwan draw in high-purity barrels via term contracts that link to semiconductor output indexes, a hedging structure seldom seen in bulk chemicals.

North America posts steady growth where enhanced-oil-recovery campaigns require stable fracturing acid volumes. Hurricane Ida spotlighted vulnerability: three successive landfalls shuttered more than 80% of U.S. Gulf Coast chlor-alkali nameplate capacity, jolting spot price indices by 40% in under two weeks. Response strategies now include regional diversification: Chlorum Solutions chose Casa Grande, Arizona, for a USD 70 million membrane plant serving western petrochem and mining clusters. Europe, constrained by energy costs, pivots toward secondary uses that command premium pricing, such as PFAS-resin regeneration and pharmaceutical intermediates. Import flows through Antwerp and Rotterdam rose 12% in 2025, with Canadian cargoes filling seasonal gaps when German electrolyzers throttled down. Eastern-European steel galvanizers still lift commodity grades but invest in zero-liquid-discharge pickling to navigate tightening chloride-emission limits. South America and Middle-East-and-Africa remain volume-small but trend-positive as mining, oil-sands, and desalination projects proliferate.

- AGC Inc.

- BASF SE

- Coogee

- Covestro AG

- Detrex Corporation

- DONGYUE GROUP

- ERCO Worldwide

- Ercros S.A

- INEOS Group

- Jones-Hamilton Co.

- Merck KGaA

- Occidental Petroleum Corporation (OxyChem)

- Olin Corporation

- TOAGOSEI CO.,LTD.

- Vynova Group

- Westlake Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Oil and Gas Well-Stimulation Demand Surge

- 4.2.2 Water-Treatment and Food-Processing Hygiene Needs

- 4.2.3 Semiconductor-Grade HCL for Advanced Node Etching

- 4.2.4 PFAS-Removal Resin Regeneration Requirements

- 4.2.5 Lithium-Ion Battery Recycling Leaching Chemistry

- 4.3 Market Restraints

- 4.3.1 Worker-Safety and Environmental-Toxicity Regulations

- 4.3.2 Chlor-Alkali Co-Product Price Volatility

- 4.3.3 Organic-Acid Substitution in Pickling Baths

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Grade

- 5.1.1 Industrial

- 5.1.2 Concentrated

- 5.1.3 Ultra-high Purity

- 5.2 By End-user Industry

- 5.2.1 Chemical

- 5.2.2 Oil and Gas

- 5.2.3 Steel and Metallurgy

- 5.2.4 Food and Beverage

- 5.2.5 Textiles and Leather

- 5.2.6 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global overview, Market level overview, Core segments, Financials, Strategic information, Market rank/share, Products and services, Recent developments)

- 6.4.1 AGC Inc.

- 6.4.2 BASF SE

- 6.4.3 Coogee

- 6.4.4 Covestro AG

- 6.4.5 Detrex Corporation

- 6.4.6 DONGYUE GROUP

- 6.4.7 ERCO Worldwide

- 6.4.8 Ercros S.A

- 6.4.9 INEOS Group

- 6.4.10 Jones-Hamilton Co.

- 6.4.11 Merck KGaA

- 6.4.12 Occidental Petroleum Corporation (OxyChem)

- 6.4.13 Olin Corporation

- 6.4.14 TOAGOSEI CO.,LTD.

- 6.4.15 Vynova Group

- 6.4.16 Westlake Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment