|

시장보고서

상품코드

1687908

우주 추진 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Space Propulsion - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

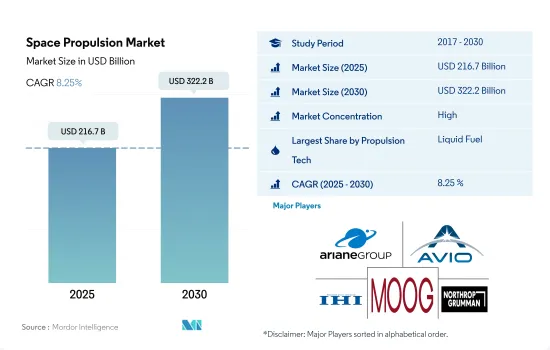

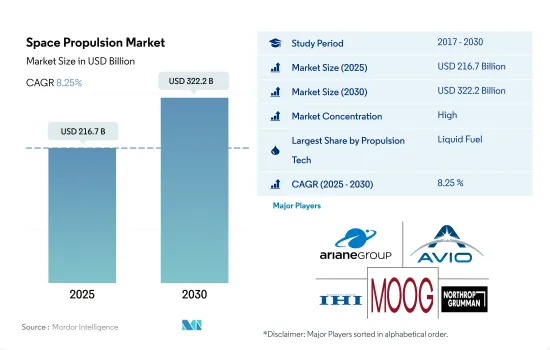

우주 추진 시장 규모는 2025년에 2,167억 달러, 2030년에는 3,222억 달러에 이를 것으로 예측되며, 예측 기간 중(2025-2030년) CAGR은 8.25%를 나타낼 전망입니다.

가스 기반 추진 드라이브의 일관된 채택은 부문을 선도

- 속도와 방향을 바꾸기 위해 위성 추진 시스템은 중요한 역할을합니다. 또한 궤도에서 우주선의 위치를 조정하는 데 사용됩니다. 궤도에 들어간 후, 우주선은 지구와 태양에 대해 올바르게 방향을 맞추기 위해 자세 제어가 필요합니다. 어떤 경우에는 한 궤도에서 위성을 이동시켜야 하며, 궤도를 조정할 수 있는 능력이 없으면 위성의 수명이 다할 것으로 예상됩니다. 따라서 추진 시스템의 중요성이 시장 성장의 원동력이 될 것으로 예상됩니다.

- 다양한 유형의 추진제가 목적에 따라 사용됩니다. 액체 추진제는 액체 연료를 사용하는 로켓 엔진을 사용합니다. 가스 추진제도 사용할 수 있지만 밀도가 낮고 기존의 펌프 방식을 적용하기가 어렵기 때문에 일반적이지 않습니다. 이동을 가능하게 한 화학 추진 시스템은 효율적이고 신뢰할 수 있음이 입증되었습니다. 여기에는 히드라진 시스템, 단일 또는 트윈 추진 시스템, 하이브리드 시스템, 콜드, 핫 에어 시스템, 고체 추진제가 포함됩니다. 이들은 강한 추력이나 신속한 조종이 필요한 경우에 사용됩니다. 따라서, 화학 추진 시스템은 총 임펄스 용량이 미션 요건을 충족시키기에 충분할 때 선택된 우주에서의 추진 기술입니다.

- 전기 추진은 상업 통신 위성의 스테이션을 유지하는 데 일반적으로 사용되며 비 추력이 높기 때문에 일부 우주 과학 미션의 주요 추진이되었습니다. 노스 롭 그라만, 무그, 시에라 네바다, 스페이스 X, 블루 오리진은 추진 시스템의 주요 공급업체입니다. 인공위성의 새로운 발사는 예측 기간 동안 시장 성장을 가속시킬 것으로 예상됩니다.

우주탐사에 대한 정부와 민간기업의 관심이 높아지면서 이 시장 확대에 박차를 가하고 있습니다.

- 위성 추진 시스템 세계 시장은 다양한 분야에서 위성 배치 수요 증가에 견인되어 최근 몇 년간 강력한 성장을 이루고 있습니다. 북미는 NASA 등의 확립된 우주 기관이나 SpaceX, Blue Origin, Boeing 등의 비공개 회사의 존재 등에 의해 세계의 우주에서의 추진 시장의 지배적인 기업로서 대두해 왔습니다. 이러한 기업들은 야심찬 우주 임무와 위성 배치를 위해 노력하고 있으며, 선진 추진 시스템 수요를 견인하고 있습니다. NASA도 태양전기 추진 프로젝트를 진행하고 있으며, 야심찬 발견과 과학 미션의 기간과 능력의 연장을 목표로 하고 있습니다.

- 아시아태평양은 최근 우주 능력의 급속한 확대를 목격하고 있습니다. 중국, 인도, 일본과 같은 국가들은 우주 기술과 위성 제조에서 큰 진보를 이루고 있으며 세계 시장에서 강력한 선수로서의 지위를 확립하고 있습니다. 2022년 5월 중국 위성전기 추진 회사인 콩티안 동리는 중국 위성 발사 계획이 급증하면서 수백만 위안의 엔젤 라운드 자금을 확보했습니다.

- 유럽에는 ESA와 같은 조직을 통한 우주 탐사에서 협력의 강한 전통이 있습니다. ESA와 여러 회원국 간의 파트너십은 우주 기술, 위성 제조 및 발사 능력에 큰 진보를 가져왔습니다. 2023년 2월 스페인에 기반을 둔 우주 이동성 제공업체인 IENAI SPACE는 ATHENA(NAnotechnology를 동력원으로 하는 일렉트로스프레이 기반 적응 가능한 THruster) 추진 시스템의 성숙과 추가 개발을 위해 일반 지원 기술 프로그램 내에서 2개의 ESA 계약을 획득했습니다.

세계 우주에서 추진 시장 동향

세계 우주에서 추진 시장에서 투자 기회 증가

- 연구와 투자를 위한 보조금은 북미 위성 발사 로켓 시장의 혁신과 성장의 주요 원동력이 되고 있습니다. 이는 위성 발사 비용을 크게 줄일 수 있는 재사용 로켓과 같은 신기술 개발에 자금을 제공하는 데 도움이 됩니다. 2023년, 2022년부터 2027년까지의 대통령 예산 요구 요약에 따르면 NASA는 태양전기 추진 개발에 9,800만 달러를 받을 전망입니다. 2021년 3월, NASA는 Maxar Technologies 및 Busek Co.와 함께 6킬로와트(kW)의 태양 전기 추진 서브시스템을 성공적으로 테스트했습니다.

- 또한 2022년 11월 ESA는 우주 프로젝트에서 유럽의 리드를 유지하기 위해 향후 3년간 우주 자금을 25% 증가할 것을 제안했다고 발표했습니다. ESA는 22개국에 2023년부터 2025년까지 185억 유로의 예산을 지지할 것을 요구하고 있습니다. 2023년 4월, 돈 에어로스페이스는 DLR(독일항공우주센터)과 공동으로 인공위성 및 심우주 미션을 위한 아산화질소 기반의 녹색추진제의 성능을 높이기 위한 실현가능성 조사를 실시하는 계약을 체결했습니다.

- 아시아태평양에서는 우주 계획이 증가함에 따라 우주에서 추진제에 대한 수요가 증가하고 있습니다. 2022년 5월 중국 위성전기 추진 회사인 콩티안 동리(Kongtian Dongli)는 중국의 별자리 계획이 급증하면서 수백만 위안의 엔젤 라운드 자금을 확보했다고 발표했습니다. 이 회사의 주요 제품은 홀 추진기와 마이크로파 전기 추진 시스템입니다. 마찬가지로 2023년 2월 인도 정부는 ISRO가 액체 추진 시스템 센터(LPSC)와 ISRO 추진 복합 시설의 개발을 포함한 다양한 우주 관련 활동을 위해 20억 달러를 받을 전망이라고 발표했습니다.

우주에서의 추진 산업 개요

우주에서의 추진시장은 상당히 통합되어 있으며 상위 5개사에서 68%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. Ariane Group, Avio, IHI Corporation, Moog Inc. and Northrop Grumman Corporation(sorted alphabetically).

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 우주 개발에의 지출

- 규제 프레임워크

- 세계

- 호주

- 브라질

- 캐나다

- 중국

- 프랑스

- 독일

- 인도

- 이란

- 일본

- 뉴질랜드

- 러시아

- 싱가포르

- 한국

- 아랍에미리트(UAE)

- 영국

- 미국

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 추진 기술

- 전기식

- 가스베이스

- 액체 연료

- 지역

- 아시아태평양

- 국가별

- 호주

- 중국

- 인도

- 일본

- 뉴질랜드

- 싱가포르

- 한국

- 유럽

- 국가별

- 프랑스

- 독일

- 러시아

- 영국

- 북미

- 국가별

- 캐나다

- 미국

- 세계 기타 지역

- 국가별

- 브라질

- 이란

- 사우디아라비아

- 아랍에미리트(UAE)

- 세계 기타 지역

- 아시아태평양

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일.

- Ariane Group

- Avio

- Blue Origin

- Honeywell International Inc.

- IHI Corporation

- Moog Inc.

- Northrop Grumman Corporation

- OHB SE

- Sierra Nevada Corporation

- Sitael SpA

- Space Exploration Technologies Corp.

- Thales

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Space Propulsion Market size is estimated at 216.7 billion USD in 2025, and is expected to reach 322.2 billion USD by 2030, growing at a CAGR of 8.25% during the forecast period (2025-2030).

Consistent adoption of gas-based propulsion drives to lead the segment

- To change the velocity and direction, the satellite's propulsion system plays an important role. It is also used to coordinate the position of the spacecraft in orbit. After entering into orbit, the spacecraft needs attitude control which helps to correctly align its direction with respect to the Earth and the Sun. In some cases, satellites need to be moved from one orbit, and without their ability to adjust to their orbit, the life of satellites is considered to be over. Therefore, the importance of propulsion systems is expected to drive the market growth.

- Various types of propellants are used for different purposes. Liquid propellants use rocket engines that use liquid fuel. Gas propellants can also be used but are not common due to their low density and difficulty in applying conventional pumping methods. The chemical propulsion systems that enabled movements proved to be efficient and reliable. These include hydrazine systems, single or twin propulsion systems, hybrid systems, cold/hot air systems, and solid propellants. They are used when strong thrust or rapid maneuvering is required. Therefore, chemical systems remain the space propulsion technology of choice when their total impulse capacity is sufficient to meet the mission requirements.

- Electric propulsion is commonly used to hold stations for commercial communication satellites, and it is the main propulsion of some space science missions due to their high specific impulses. Northrop Grumman Corporation, Moog Inc., Sierra Nevada Corporation, SpaceX, and Blue Origin are some of the major providers of propulsion systems. The new launch of satellites is expected to accelerate market growth during the forecast period.

The growing interest of governments and private players in space exploration have fueled the expansion of this market

- The global market for satellite propulsion systems witnessed robust growth in recent years, driven by the increasing demand for satellite deployments across various sectors. North America has emerged as a dominant player in the global space propulsion market, mainly due to the presence of established space agencies such as NASA and private companies like SpaceX, Blue Origin, and Boeing. These entities have undertaken ambitious space missions and satellite deployments, driving the demand for advanced propulsion systems. NASA is also working on the Solar Electric Propulsion project, which aims to extend the duration and capabilities of ambitious discoveries and science missions.

- Asia-Pacific has witnessed a rapid expansion of its space capabilities in recent years. Countries like China, India, and Japan have made significant strides in space technology and satellite manufacturing, positioning themselves as formidable players in the global market. In May 2022, Kongtian Dongli, a Chinese satellite electric propulsion company, secured multi-million yuan angel round financing amid a proliferation of Chinese constellation plans.

- Europe has a strong tradition of collaboration in space exploration through organizations like the ESA. ESA's partnerships with multiple member states have resulted in significant advancements in space technology, satellite manufacturing, and launch capabilities. In February 2023, IENAI SPACE, an in-space mobility provider based in Spain, received two ESA contracts within the General Support Technology Program to mature and further develop ATHENA (Adaptable THruster based on Electrospray powered by NAnotechnology) propulsion systems.

Global Space Propulsion Market Trends

Rising investment opportunities in the global space propulsion market

- The grant for research and investment has been a major driver of innovation and growth in the North American satellite launch vehicle market. It has helped to fund the development of new technologies, such as reusable launch vehicles, which have the potential to significantly reduce the cost of satellite launches. In FY2023, according to the President's budget request summary from FY2022 to FY2027, NASA is expected to receive USD 98 million for the development of Solar Electric Propulsion. In March 2021, NASA, along with Maxar Technologies and Busek Co., successfully completed a test of the 6-kilowatt (kW) solar electric propulsion subsystem.

- Additionally, in November 2022, ESA announced that it had proposed a 25% boost in space funding over the next three years to maintain Europe's lead in space projects. The ESA is asking its 22 nations to back a budget of EUR 18.5 billion for 2023-2025. In April 2023, Dawn Aerospace was awarded a contract to conduct a feasibility study with DLR (German Aerospace Center) to increase the performance of a nitrous-oxide-based green propellant for satellites and deep-space missions.

- In Asia-Pacific, the demand for space propulsion is driven by increasing space programs. In May 2022, Kongtian Dongli, a Chinese satellite electric propulsion company, announced that it had secured multi-million yuan angel round financing amid a proliferation of Chinese constellation plans. The company's main products are hall thrusters and microwave electric propulsion systems. Likewise, in February 2023, the Indian government announced that ISRO is expected to receive USD 2 billion for various space-related activities, including the development of the Liquid Propulsion Systems Centre (LPSC) and ISRO Propulsion Complex.

Space Propulsion Industry Overview

The Space Propulsion Market is fairly consolidated, with the top five companies occupying 68%. The major players in this market are Ariane Group, Avio, IHI Corporation, Moog Inc. and Northrop Grumman Corporation (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Spending On Space Programs

- 4.2 Regulatory Framework

- 4.2.1 Global

- 4.2.2 Australia

- 4.2.3 Brazil

- 4.2.4 Canada

- 4.2.5 China

- 4.2.6 France

- 4.2.7 Germany

- 4.2.8 India

- 4.2.9 Iran

- 4.2.10 Japan

- 4.2.11 New Zealand

- 4.2.12 Russia

- 4.2.13 Singapore

- 4.2.14 South Korea

- 4.2.15 United Arab Emirates

- 4.2.16 United Kingdom

- 4.2.17 United States

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Propulsion Tech

- 5.1.1 Electric

- 5.1.2 Gas based

- 5.1.3 Liquid Fuel

- 5.2 Region

- 5.2.1 Asia-Pacific

- 5.2.1.1 By Country

- 5.2.1.1.1 Australia

- 5.2.1.1.2 China

- 5.2.1.1.3 India

- 5.2.1.1.4 Japan

- 5.2.1.1.5 New Zealand

- 5.2.1.1.6 Singapore

- 5.2.1.1.7 South Korea

- 5.2.2 Europe

- 5.2.2.1 By Country

- 5.2.2.1.1 France

- 5.2.2.1.2 Germany

- 5.2.2.1.3 Russia

- 5.2.2.1.4 United Kingdom

- 5.2.3 North America

- 5.2.3.1 By Country

- 5.2.3.1.1 Canada

- 5.2.3.1.2 United States

- 5.2.4 Rest of World

- 5.2.4.1 By Country

- 5.2.4.1.1 Brazil

- 5.2.4.1.2 Iran

- 5.2.4.1.3 Saudi Arabia

- 5.2.4.1.4 United Arab Emirates

- 5.2.4.1.5 Rest of World

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Ariane Group

- 6.4.2 Avio

- 6.4.3 Blue Origin

- 6.4.4 Honeywell International Inc.

- 6.4.5 IHI Corporation

- 6.4.6 Moog Inc.

- 6.4.7 Northrop Grumman Corporation

- 6.4.8 OHB SE

- 6.4.9 Sierra Nevada Corporation

- 6.4.10 Sitael S.p.A.

- 6.4.11 Space Exploration Technologies Corp.

- 6.4.12 Thales

7 KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

샘플 요청 목록