|

시장보고서

상품코드

1687925

산업용 컴퓨터 X선 촬영 장치 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Industrial Computed Radiography - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

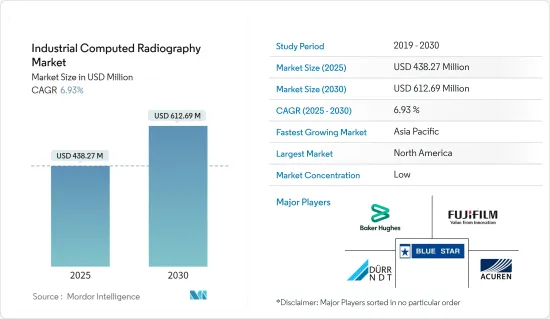

산업용 컴퓨터 X선 촬영 장치 시장 규모는 2025년에 4억 3,827만 달러로 추정되고, 예측 기간 2025년부터 2030년까지 CAGR 6.93%로 성장할 전망이며, 2030년에는 6억 1,269만 달러에 이를 것으로 예측됩니다.

컴퓨터 X선 촬영 장치 기술은 검사 작업에 엄청난 이점을 제공하고 소모품을 거의 사용하지 않기 때문에 이미지 생성에 소요되는 시간이 더욱 단축됩니다. 이러한 요인은 시장 도입 증가를 기대합니다.

주요 하이라이트

- 종래의 X선 촬영 장치의 필름보다 다이나믹 레인지가 높기 때문에 미세한 디테일이 가시화되어 분석이 가능합니다. 또한 워크플로우의 간소화, 운영자의 안전한 작업 환경, 환경 친화적인 무약 공정을 제공합니다.

- 다양한 벤더들이 디지털 엑스레이 스캐너, 인광체 이미징 플레이트, 소프트웨어 프로그램을 개선해 왔습니다. 그 결과 항공우주 및 방위, 석유 및 가스 등 업계의 요구에 직접 대응하는 신제품이 등장하고 있습니다.

- 시중에서 판매되는 다양한 제품은 실린더 스캐너와 평면 패널 스캐너를 사용하며, 소프트웨어는 14비트 로그에서 16비트 선형까지 광범위합니다. 최소 픽셀 크기는 12.5-25, 25-35, 35-70, 70-100 픽셀의 범위이며, 그 결과 많은 현행 규격을 충족하기 위해 본질적인 공간 분해능, S/N 비치, 그레이 값이 대폭 향상되고 있습니다. 이들은 재료의 결함을 검출할 가능성에 큰 영향을 미칩니다.

- 현재 CR 스캐너와 형광체 이미징 플레이트는 12.5-25(X선 촬영 필름의 D4/IX50과 동일) 해상도로 스캔할 수 있습니다. 이들은 X선 사진 감도 2% 이상과 같은 사양상의 감도 기준을 충족하고, 결함 검출의 가능성은 현저하게 높아지고 있습니다.

- 그러나 높은 설치 비용과 추가 기술 개선은 시장을 혼란시킬 수 있습니다.

- 인도국가통계국 및 통계계획부(MOSPI)가 발표한 2020-2021년 1분기 국내총생산(GDP)에 따르면 COVID-19가 건설업, 제조업, 광업부문의 조부가가치에 미치는 영향은 -12.6%, -9.4%, -12.4%였습니다. 이 때문에 이러한 산업의 성장 둔화는 시장 성장을 단기간 정체시켜 시장 성장에 영향을 미칠 것으로 예상됩니다.

산업용 컴퓨터 X선 촬영 장치 시장 동향

비파괴 검사가 시장 성장을 견인할 전망

- 컴퓨터 X선 촬영 장치는 비파괴 검사(NDT)의 일종으로, 제조된 부품 및 어셈블리의 안전성과 무결성을 확인하기 위해 산업 현장에서 사용됩니다. 예를 들어, 석유 및 가스 사업의 경우 NTT는 가동중인 모든 중요한 부품이 목적에 맞는지 확인해야 합니다. 석유 및 가스 이송에 사용되는 파이프는 충분한 유지 보수 및 검사가 필요한 필수 부품입니다. 따라서 산업계에서 비파괴 검사에 대한 수요가 증가함에 따라 산업 용도에서도 컴퓨터 X선 촬영 장치 기술의 채택이 증가하고 있습니다.

- 또한 산업 제조 및 인프라 부문에서 자동화가 증가함에 따라 균열, 기공, 제조 장애 등과 관련된 결함 검출에 대한 수요가 크게 증가하고 있습니다.

- 또한 미국 기계 학회(ASME) 및 국제 표준화 기구(ISO)와 같은 일부 정부 기관 및 지역 기관은 장비의 안전을 보장하고 엔지니어링 서비스 시험을 감독하기 위해 엄격한 조치를 취하도록 제정하고 있습니다. 따라서 비파괴 검사에 대한 수요는 산업 전반에 걸쳐 증가하고 있습니다.

- 또한 항공우주 분야에서의 컴퓨터 X선 촬영 장치의 적용에는 두께가 복잡한 형상, 금속 및 비금속 형상의 내부 결함 검출, 중요한 항공우주 부품, 구조물 및 조립품의 품질 검출이 포함됩니다. 게다가 안전기준 중시 증가, 서비스 간격의 단축, 저배출 목표, 신소재 및 신공정이 항공우주 분야의 컴퓨터 X선 검사 시장을 견인하는 주요 요인입니다.

북미가 시장을 독점할 전망

- 북미는 컴퓨터 X선 촬영 장치의 채용이 증가하고 기술적 진보도 진행되고 있기 때문에 세계의 컴퓨터 X선 촬영 장치 시장을 독점할 것으로 예측되고 있습니다. 후지필름과 지멘스 헬스케어 등 주요 기업도 강한 존재감을 보이고 있습니다.

- 2021년 9월-포드와 SK이노베이션은 미국에 114억 달러를 투자하였고 약 11,000명의 신규 고용을 창출할 계획을 발표했습니다. 켄터키 주에는 2곳, 테네시 주에는 1곳, 총 3곳의 BlueOval SK 배터리 공장이 신설되어 포드 미국에서 연간 129기가와트의 생산 능력이 가능합니다.

- 2021년 2월-조 바이든 대통령은 국내 반도체 제조가 일본 정부의 우선 과제라고 말했습니다. 신정권은 심각화하는 칩 부족을 해결하고 칩 제조 아웃소싱으로 미국이 공급망의 중단에 더욱 취약해졌다는 의원들의 우려에 대처할 자세입니다. 바이든은 정부의 추가 지원과 새로운 정책을 통해 미국 칩 기업을 뒷받침하는 100일간의 검토를 시작했습니다.

- 게다가 북미에서의 헬스케어 확대와 헬스케어 사업에 대한 적용은 이 지역 시장 성장을 뒷받침하고 있습니다.

산업용 컴퓨터 X선 촬영 장치 산업 개요

예측 기간 동안 시장 조사에서 경쟁 기업간 경쟁 관계는 치열합니다. X선 촬영 시장의 기술 개척에 따라 벤더와 최종 사용자는 신기술로 이동할 것으로 예상됩니다. 따라서 기존 기업은 시장 점유율을 유지하기 위해 제품 기술 혁신을 실시했습니다. 또한 많은 기업들이 지리적 확대를 시장 견인력을 얻는 길로 간주합니다.

- 2022년 2월-캐나다 정부는 캐나다 반도체 및 포토닉스 산업에 많은 투자를 발표했습니다. 2억 4,000만 캐나다 달러 투자는 포토닉스의 세계 리더로서 캐나다의 역할을 확고히 하고 반도체의 개발과 제조를 강화할 것으로 기대되고 있습니다. 캐나다에서는 국내외 반도체 기업 100개 이상이 마이크로칩 연구개발에 종사하고 있습니다. 화합물 반도체, 마이크로전기기계 시스템(MEMS), 고급 패키징 등의 분야에는 30개 이상의 용도 연구소와 5개의 상업시설이 있습니다.

- 2021년 3월-인텔은 애리조나 주에 추가로 두 개의 제조 공장(팹)을 신설합니다. 이 뉴스는 세계 칩 부족이 자동차에서 전자기기까지 업계를 괴롭히고 미국이 반도체 제조에 뒤처지고 있다고 우려되는 가운데 발표되었습니다. 파운드리은 모바일 기기에 사용되는 ARM 기술을 기반으로 다양한 칩을 제조하는 태세를 갖추고 있으며, 역사적으로 인텔이 지지하는 x86 기술과 경쟁해 왔습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 상정 및 시장 정의

- 조사 범위

제2장 조사 방법

- 조사 프레임워크

- 2차 조사

- 1차 조사

- 데이터의 삼각측량 및 인사이트 생성

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 업계의 매력도-Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

- 업계 밸류체인 분석

- 시장에 대한 COVID-19의 영향 평가

제5장 시장 역학

- 시장 성장 촉진요인

- 방사선 피폭 저감에 대한 수요 증가

- 비파괴 검사의 필요성 증가

- 시장 성장 억제요인

- 높은 설치 비용

제6장 시장 세분화

- 용도별

- 석유 및 가스

- 석유화학 및 화학

- 주조

- 항공우주 및 방위

- 기타 용도

- 지역별

- 북미

- 유럽

- 아시아태평양

- 세계 기타 지역

제7장 경쟁 구도

- 기업 프로파일

- Durr Ndt Gmbh & Co. Kg

- Baker Hughes

- Fujifilm Corporation

- Applus Services Sa

- Rigaku Corporation

- Shawcor Ltd

- Bluestar Limited

- Virtual Media Integration

- Acuren

제8장 시장 투자

제9장 시장 기회 및 향후 동향

AJY 25.04.04The Industrial Computed Radiography Market size is estimated at USD 438.27 million in 2025, and is expected to reach USD 612.69 million by 2030, at a CAGR of 6.93% during the forecast period (2025-2030).

Computed radiography technology offers enormous advantages for inspection tasks, and the use of consumables is virtually eliminated, further reducing the time to produce an image. These factors are expected to increase market adoption.

Key Highlights

- Minute details are visible and analyzable due to a higher dynamic range than a film in traditional x-ray machines. Further, it provides a simplified workflow, a safer working environment for operators, and a more environmentally-friendly chemical-free process.

- Various computed radiography vendors have improved digital radiography scanners, phosphor imaging plates, and software programs. As a result, new products have been introduced that directly meet the needs of industries such as aerospace and defense, oil and gas, etc.

- Various products on the market use cylinder or flat panel scanners with software ranging from 14-bit logarithmic to 16-bit linear. Minimum pixel sizes range from 12.5-25, 25-35, 35-70, and 70-100 pixels, resulting in significantly increased essential spatial resolution, signal-to-noise ratio values, and grey values to fulfill many of the current standards. These have a substantial impact on the likelihood of detecting faults in materials.

- Current CR scanners and phosphor imaging plates can scan resolutions of 12.5 - 25 (equal to D4/IX50 in radiography film). These fulfill the sensitivity criteria in specifications, such as 2% radiographic sensitivity or greater, and the likelihood of fault identification has increased significantly.

- However, high installation costs and further technological improvements may disrupt the market.

- As per the Gross Domestic Product (GDP) for the Q1 of 2020-21 released by the National Statistical Office and Ministry of Statistic and Program Institute (MOSPI) India, the impact of COVID-19 on the gross value-added of construction, manufacturing, and mining sector accounted for -12.6%, -9.4%, and -12.4%. Thus, the decline in the growth of these industries is expected to stall the market growth for a short period, impacting the market growth.

Industrial Computed Radiography Market Trends

Nondestructive Testing Expected to Drive the Market Growth

- Computed radiography is a sort of non-destructive testing (NDT) used in industrial settings to check the safety and integrity of manufactured components and assemblies. For example, NDT must ensure that all in-service and crucial parts are fit-for-purpose in the oil and gas business. Pipes used to transfer oil or gas are essential components to be well maintained and inspected. Hence, due to the growing demand for NDT in industries, the adoption of computed radiography techniques is also increasing in industrial applications.

- Also, with the increase in automation in the industrial manufacturing and infrastructure sectors, there has been a substantial hike in demand for flaw detection related to cracks, porosity, manufacturing disorders, and so on.

- Moreover, several governmental agencies and regional bodies, like the American Society of Mechanical Engineers (ASME) and the International Organization for Standardization (ISO), have instituted to take stringent measures to ensure the safety of instruments and oversee engineering services testing. Hence, the demand for non-destructive testing is increasing across industries.

- Also, computed radiography applications in aerospace include detecting internal defects in thick and complex shapes, metallic and non-metallic forms, and the quality of critical aerospace components, structures, and assemblies. Further, increasing emphasis on safety standards, decreasing service intervals, low emission targets, and new materials and processes are the major factors driving the computed radiography market in the aerospace segment.

North America Expected to Dominate the Market

- North America is expected to dominate the global computed radiography market due to the increasing adoption of added radiography equipment coupled with technological advancements in the region. Key players like Fujifilm Corporation and Siemens Healthcare also have a strong presence.

- In September 2021, Ford and SK Innovation announced a plan to invest USD11.4 billion and create nearly 11,000 new jobs in the United States. Three new BlueOval SK battery plants, two in Kentucky and one in Tennessee enable 129-gigawatt hours a year of US production capacity for Ford.

- In February 2021, President Joe Biden stated that domestic semiconductor manufacturing is a priority for the country's administration. The new administration is poised to fix growing chip shortages and address lawmakers' concerns that outsourcing chipmaking had made the United States more vulnerable to supply chain disruptions. In an executive action, Biden started began a 100-day review that could boost American chip companies with additional government support and new policies.

- Furthermore, the expansion of healthcare in the North American region and its application in the healthcare business boost the area's market growth.

Industrial Computed Radiography Industry Overview

The intensity of competitive rivalry in the market studied is high during the forecast period. With the technological developments in the radiography market, the vendors and end-users are expected to shift towards the new technology. Hence, the existing players are innovating their products to maintain their market share. Also, many companies view geographical expansion as a path to gaining market traction.

- February 2022 - The Government of Canada announced a significant investment in the Canadian semiconductor and photonics industries. The investment of CAD 240 million is expected to help solidify Canada's role as a global leader in photonics and may bolster the development and manufacturing of semiconductors. Over 100 domestic and international semiconductor companies are working on microchip research and development in Canada. In areas including compound semiconductors, microelectromechanical systems (MEMS), and advanced packaging, it has over 30 applied research laboratories and five commercial facilities.

- March 2021 - Intel committed to two more new fabrication plants, or fabs, in Arizona. The news comes during a global chip shortage that is snarling industries from automobiles to electronics and worries the United States is falling behind in semiconductor manufacturing. The foundry is poised to manufacture a range of chips based on ARM technology used in mobile devices and has historically competed with Intel's favored x86 technology.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of The Study

2 RESEARCH METHODOLOGY

- 2.1 Research Framework

- 2.2 Secondary Research

- 2.3 Primary Research

- 2.4 Data Triangulation and Insight Generation

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 The Increasing Demand for Decreasing the Exposure to Radiation

- 5.1.2 Growing Need for Nondestructive Testing

- 5.2 Market Restraints

- 5.2.1 High Installation Costs

6 MARKET SEGMENTATION

- 6.1 By Applications

- 6.1.1 Oil and Gas

- 6.1.2 Petrochemical and Chemical

- 6.1.3 Foundries

- 6.1.4 Aerospace and Defense

- 6.1.5 Other Applications

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia Pacific

- 6.2.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Durr Ndt Gmbh & Co. Kg

- 7.1.2 Baker Hughes

- 7.1.3 Fujifilm Corporation

- 7.1.4 Applus Services Sa

- 7.1.5 Rigaku Corporation

- 7.1.6 Shawcor Ltd

- 7.1.7 Bluestar Limited

- 7.1.8 Virtual Media Integration

- 7.1.9 Acuren