|

시장보고서

상품코드

1910672

종이컵 산업 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Paper Cups Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

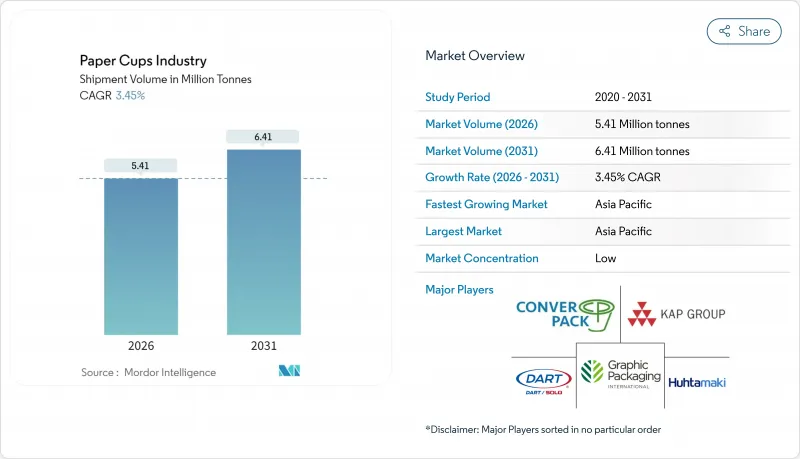

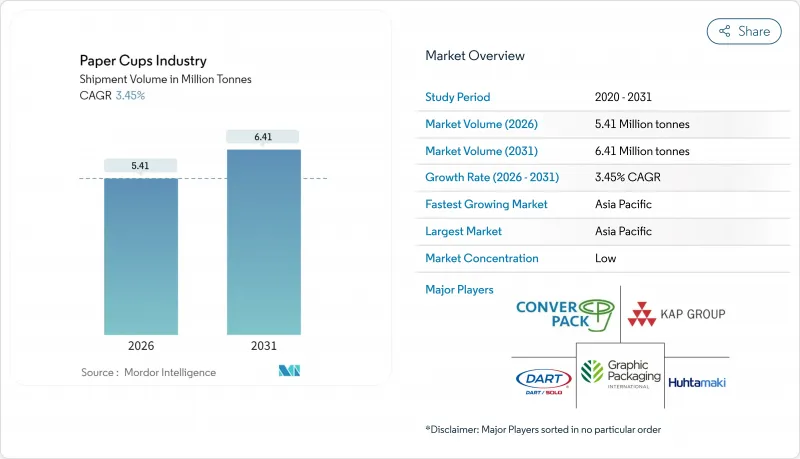

세계의 종이컵 산업 시장 규모는 2026년 541만 톤으로 추정되고 있으며, 2025년 523만 톤에서 계속 성장하고 있습니다. 2031년까지 641만톤에 달할 것으로 예측되고, 2026년부터 2031년까지 CAGR 3.45%로 확대가 전망되고 있습니다.

종이컵 시장 규모의 이러한 꾸준한 확대는 섬유 기반 포장에 대한 규제 추진, 수성 및 미네랄 기반 코팅 기술의 급속한 진화 및 푸드서비스 브랜드에서 쉽게 재활용 가능한 형태로의 선호 확대를 반영합니다. 소비자의 행동 변화에 따른 테이크아웃 음료 수요 증가, 새로운 QSR(퀵 서비스 레스토랑) 점포의 전개, 고속 성형 라인의 기술 진보가 수량 수요를 확대하고 있으며, 성숙 경제권에서의 프리미엄화가 단가 수익을 밀어 올리고 있습니다. 아시아태평양은 2024년 39.56%의 점유율로 세계 생산량을 선도했으며, 도시화 및 식품 배달 시장의 성장이 이를 이끌고 있습니다. 한편, 북미와 유럽에서는 보다 높은 이익률을 실현하는 저PFAS 함유 완전 재활용 핫컵 형식으로의 전환이 진행되고 있습니다. 경쟁의 치열성은 여전히 적당하며 기존 기업은 규모의 경제, 수직 통합 및 R&D 투자를 활용하여 틈새 지속가능성 요구를 목표로 하는 신흥 전문 컨버터 기업에 선행하고 있습니다.

세계 종이컵 산업 동향과 통찰

이동 중 음료 섭취 수요 증가

모바일 라이프 스타일의 보급으로 평소 테이크아웃 음료 수요가 증가하고 종이컵은 이동에 적합한 음료의 표준 포장재로서 지위를 확립하고 있습니다. 도시의 통근자는 대중교통의 매너에 적합하는 흐르지 않는 형상을 요구하고, 유연한 근무 형태가 점심시간의 커피 구입을 촉진하고 있습니다. 미국의 식품 배달 시장은 2024년 1조 2,200억 달러 규모에 달할 것으로 전망됐고, 연간 8.29%의 성장률을 나타내고 있으며, 디지털 플랫폼이 앱 주문을 컵 수요 증가에 연결하고 있는 실태를 뒷받침하고 있습니다. 동남아시아와 중동에서 확대하는 전문 카페에서는 크레마를 손상시키지 않고 브랜드 로고를 선명하게 인쇄할 수 있는 고급 컵 사양을 도입하고 있습니다. 로열티 앱은 소액 구매를 촉진하고 신규 방문객을 늘리지 않으면서도 포장재 소비량을 증가시키고 있습니다. 이러한 움직임은 지역을 불문하고 종이컵 시장에 대해 일관된 고빈도 수요를 낳고 있으며, 소매업체가 목표로 하는 프릭션리스 서비스와의 시너지 효과를 가져오고 있습니다.

일회용 플라스틱에 대한 정부 규정

입법부는 일회용 플라스틱을 보다 고비용으로 제한된 선택으로 전환하여 섬유 소재로의 체계적인 이행을 촉진하고 있습니다. 2024년 3월 최종 결정된 EU 포장 및 포장 폐기물 규제는 완전한 재활용 가능성을 의무화하고 2030년까지 폐기물을 5% 삭감하는 목표를 설정했습니다. 남호주에서는 2024년 9월부터 플라스틱 음료 용기의 사용을 금지하고 수요를 즉시 섬유제 컵 대체품으로 유도했습니다. 스코틀랜드에서는 2025년 말까지 일회용 음료 컵 한잔에 대해 25펜스의 과징금을 도입하는 방침으로, 소매업체에게 재이용 순환을 촉구하는 동시에, 종이컵을 가장 저비용의 일회용 대체품으로 자리 매김하고 있습니다. 이러한 법적 조치는 예측 가능한 대체 사이클을 생성하여 컨버터 기업이 새로운 성형 라인에 대한 설비 투자를 간소화 할 수있게합니다.

폐기 및 재활용 인프라 문제

많은 지자체 시스템에서는 컵의 섬유와 코팅을 분리하는 설비가 여전히 부족하기 때문에 기술적으로 재활용 가능한 수집 컵도 매립 처리되는 경우가 적습니다. 개발도상국에서는 자원 회수 예산이 한정되어 있어 종이컵 선별 시스템의 도입이 저지되고 있습니다. EU의 순환 경제 규칙은 폐기물 처리 경로 모니터링을 강화하고 기업 구매자는 계약 체결 전에 지역의 종이컵 회수 실적 증명을 요구하게 되었습니다. 인프라가 따라잡을 때까지 종이컵 업계는 평판 위험에 직면하여 틈새 카페와 시설에서 재사용 가능한 파일럿 사업으로 수요가 이동할 수 있습니다.

부문 분석

2025년 보온 컵은 시장에서 44.92%를 차지하며 2031년까지 연평균 복합 성장률(CAGR) 5.24%로 확대될 것으로 전망됩니다. 종이컵 산업은 높은 보온성과 생생한 컵 그래픽으로 브랜드 스토리 전개를 필요로 하는 스페셜티 커피 매장 증가의 혜택을 누리고 있습니다. 고급 배리어 코팅과 이중 구조가 양립해, 체인점이 고가격 설정을 정당화할 수 있는 요인이 되고 있습니다. 콜드 컵은 아이스 티, 소다, 스무디 시장에서 점유율을 유지하고 있지만, 온난한 지역에서는 경량 PET 컵과의 경쟁이 계속되고 있으며, 성장은 둔화되고 있습니다. 콘형과 특수 디자인은 대량 판매가 아닌 차별화가 중시되는 이벤트 케이터링의 틈새 시장을 차지하고 있습니다. Starbucks의 미네랄 코팅 전환은 핫컵이 R&D 투자와 이익률 확보의 기반임을 보여줍니다. 콜드컵의 혁신은 빨대가 없는 뚜껑이나 섬유계 잉크에 초점을 맞추고 있지만 단열 필요성이 낮기 때문에 단가는 여전히 낮은 수준에 머물고 있습니다.

핫 컵의 이점은 지역 기후 특성과 음료 습관에도 반영됩니다. 북유럽과 북미에서는 시원한 계절이 오랫동안 지속되어 일상적인 따뜻한 음료 수요가 지속됩니다. 아시아태평양의 메가 시티에서는 아이스 음료 수요 증가를 볼 수 있지만, 따뜻한 차 전통은 기준선 소비량을 충분히 높여 균형 잡힌 제품 포트폴리오를 지원합니다. 종이컵 업계는 핫, 콜드를 전환할 수 있는 모듈식 라미네이트 라인을 제공함으로써 적응하여 연간 설비 가동률을 확보하고 있습니다. 전문 로스팅 업체는 빈번한 설계 변경에 대응하기 위해 최소 주문 수량의 인하를 공급자에게 요구하지만, 이 서비스 레벨은 첨단 컨버터만 대응 가능합니다. 이 고객 동향은 디자인, 성형 및 물류를 통합하는 규모가 큰 기업을 우대함으로써 시장의 세분화를 억제하고 있습니다.

이중벽 컵은 2025년 47.10%의 점유율을 차지했으며 뛰어난 감촉과 단열성으로 선호되고 있습니다. 체인 카페에서는 고급감의 촉각적 신호로서도 기능합니다. 그러나 단일벽 설계는 2031년까지 연평균 복합 성장률(CAGR) 5.78%에서 가장 빠르게 성장할 것으로 예측됩니다. 이 가속은 가격에 민감한 시장에서 비용 절감 목표와 성능을 저하시키지 않고 얇게 하는 것을 가능하게 하는 코팅 기술에 기인합니다. 미세한 공기층을 갖춘 수성 라이너로 단층 컵은 충분한 내열성을 확보합니다. 이를 통해 QSR 사업자는 벽 수를 줄여도 고객의 기대에 부응할 수 있습니다. 삼중벽 컵은 여전히 틈새 시장용이며, 끓는 수프가 일반적인 산업용 식당 등에서 사용되고 있습니다.

화물 배출 감축을 위해 경량화를 중시한 전자상거래의 포장방침의 변화도 단층 구조를 뒷받침하고 있습니다. 박스형 음료 키트를 배송하는 D2C 커피 로스팅 업체는 엄격한 탄소 계산에 적합한 슬림 컵을 선호합니다. 제조 현장에서는 컨버터 기업이 성형 사이클을 단층 구조로 최적화하여 라인 속도를 향상시키고 있습니다. 그러나 이중벽 컵은 고수익 시장에서의 지위를 유지하고 있습니다. 강력한 브랜드 가치를 가진 체인점에서는 두께가 있는 질감을 감각적 체험의 일부로 자리 매김하고 있습니다. 이에 따라 종이컵 시장은 양극화된 제품 구성을 나타내고 있으며, 광범위한 저렴한 가격대에는 단층 벽, 수익성이 높은 주력 상품에는 이중벽이 채용되고 있습니다.

종이컵 시장 보고서는 컵유형(핫 페이퍼 컵, 콜드 페이퍼 컵 등), 벽구조(단일층, 이중층, 삼중층), 용량(4-8온스, 9-12온스 등), 최종 사용자별(퀵서비스 레스토랑, 커피체인 및 자동판매기 사업자 등), 유통채널별(직접 B2B계약 등), 지역별로 분석했습니다. 시장 예측은 수량(백만 톤) 단위로 제시됩니다.

지역별 분석

아시아태평양은 2025년에 세계 총 생산량의 39.10%를 차지했고, 2031년까지 연평균 복합 성장률(CAGR) 6.55%로 성장하여 전 지역 중 가장 높은 성장률이 전망되고 있습니다. 중국 제지업계는 2024년 국내 생산능력을 10% 확대해 2025년 컵 가공용 기재의 안정공급을 확보하였습니다. 인도의 포장 시장은 2025년까지 2,048억 1,000만 달러 규모에 이르렀으며, 26.7%의 연평균 복합 성장률(CAGR)로 확대될 것으로 예측되고 있으며, 이 규모의 확대가 식품 배달용 컵의 최종 시장 수요를 더욱 깊게 하고 있습니다. 베트남의 포장 시장은 연률 9.73%로 성장하고 있으며, 제조 경쟁력을 나타내면서 ASEAN 전역에 컵 수출도 지지하고 있습니다. 가처분 소득 증가와 브랜드 카페 문화로의 전환은 지역 수요를 뒷받침하며, 아시아태평양은 종이컵 산업의 성장에 중점을 둡니다.

북미는 성숙 시장이면서 기술적으로 진보를 계속하고 있습니다. 미국 식품의약국(FDA)이 2025년 2월에 결정한 PFAS(과불화화합물)의 단계적 폐지는 수성 및 미네랄계 배리어 코팅의 채용을 촉진하고 있습니다. Georgia-Pacific은 2024년 생산 유연성 유지와 지속가능성 목표 달성을 위해 미국 내 7개 시설에 20억 달러를 투자했습니다. 현대적인 재활용 시스템과 기업의 ESG 보고서는 프리미엄 제품의 제공을 촉진하고 있으며, 컨버터는 순수한 가격 경쟁이 아닌 제품 수명이 끝나면 인증을 받았습니다. 수량 기준의 성장은 완만하지만, 섬유 뚜껑 등의 부가가치 사양에 의해 이익률은 향상하고 있습니다.

유럽은 규제 우선 궤도를 따르고 있습니다. 2030년까지 재활용 의무화로 플라스틱 포장에서 종이 컵으로의 꾸준한 대안이 진행되고 있습니다. Huhtamaki는 2024년 10월, 북아일랜드에서 섬유제 뚜껑의 생산 능력을 확대하여 플라스틱 프리 부품의 지역 수요에 대응했습니다. 이 지역에서는 소비자에게 재사용 가능한 제품으로의 전환을 촉구하기 위해 컵당 과금과 세제 우대 조치가 채용되고 있지만, 여전히 섬유 컵이 규제에 따른 일회용 옵션으로 자리매김하고 있습니다. 동유럽에서는 QSR(퀵서비스 레스토랑)의 보급률 상승에 견인되어 성장이 예상되는 지역이 존재하고 서유럽의 성숙한 시장 규모를 상쇄하는 역할을 하고 있습니다.

중동, 아프리카 및 남미는 신흥 기회 지역입니다. 인프라 부족과 경제 변동으로 인한 규모 확대는 억제되지만, 식품 배달 앱과 국제 커피 체인이 조기 기반을 구축하고 있습니다. 컨버터는 현지 제지공장과 합작회사를 설립하여 공급 현지화를 추진하고 외환 위험과 수입 관세를 경감하고 있습니다. 종이컵 시장 규모에 대한 공헌도는 여전히 작지만 장기적인 인구 동향으로 인해 생산량이 점차 증가할 것으로 예측됩니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 외출 시 음료 수요 증가

- 일회용 플라스틱 제품에 대한 정부의 금지 조치

- 퀵 서비스 레스토랑(QSR) 및 식품 배달 생태계 확대

- 수성 코팅을 실시한 완전 리사이클 가능한 핫 컵 발매

- 제로 웨이스트 스타디움 및 이벤트 조달 의무화

- AI 기반 고속 성형 라인에 의한 비용 절감

- 시장 성장 억제요인

- 폐기물 처리 및 재활용 인프라의 부족

- 펄프 가격 변동이 이익률을 압박

- 커피 체인에서 재사용 컵 순환 시스템의 시험 도입

- PFAS의 단계적 폐지에 따른 재설계와 인증 지연

- 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 컵 유형별

- 핫 페이퍼 컵

- 콜드 페이퍼 컵

- 콘 및 스페셜티 컵

- 벽 유형별

- 단일 벽

- 이중 벽

- 삼중 벽

- 용량별(온스)

- 4-8

- 9-12

- 13-20

- >20

- 최종 사용자별

- 퀵 서비스 레스토랑(QSR)

- 커피 체인점 및 자동판매기 사업자

- 법인용 케이터링

- 항공사 및 철도회사

- 기타

- 유통 채널별

- 직접 (B2B 계약)

- 리셀러 및 도매업체

- 온라인 B2B 마켓플레이스

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 중동

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Huhtamaki Oyj

- Dart Container Corp.

- Graphic Packaging International

- Georgia-Pacific LLC

- Seda International Packaging

- Kap Cones Pvt Ltd

- ConverPack Inc.

- Go-Pak UK Ltd(SCGP)

- Benders Paper Cups

- Hotpack Global

- Tekni-Plex Inc.

- CEE Schisler Packaging

- International Paper Foodservice

- Stora Enso Food-Service Boards

- Lollicup USA(Karat)

- Detmold Group

- F-Bender & Co.

- Nissin Paper Products

- Reynolds Consumer Products

- Pactiv Evergreen

제7장 시장 기회와 미래 전망

SHW 26.01.26Paper Cups Industry market size in 2026 is estimated at 5.41 Million tonnes, growing from 2025 value of 5.23 Million tonnes with 2031 projections showing 6.41 Million tonnes, growing at 3.45% CAGR over 2026-2031.

This steady rise in the paper cups market size reflects a regulatory push toward fiber-based packaging, rapid upgrades in aqueous and mineral coatings, and the widening preference of food-service brands for easily recyclable formats. Shifts in consumer behavior toward take-away beverages, the roll-out of new QSR outlets, and technological advances in high-speed forming lines are widening volume demand, while premiumization in mature economies is lifting unit revenues. Asia-Pacific leads global tonnage with 39.56% share in 2024, propelled by urbanization and food-delivery growth, whereas North America and Europe are pivoting toward low-PFAS, fully recyclable hot-cup formats that command higher margins. Competitive intensity remains moderate; incumbents leverage scale, vertical integration, and R&D investment to stay ahead of emerging specialty converters that target niche sustainability needs.

Global Paper Cups Industry Trends and Insights

Rising Demand for On-the-Go Beverages

Mobile lifestyles are lifting daily takeaway beverage volumes, positioning paper cups as the default pack for transit-friendly drinks. Urban commuters seek spill-proof formats that fit public-transport etiquette, and flexible work patterns elevate mid-day coffee runs. The U.S. food-delivery market is on track to generate USD 1.22 trillion in 2024, growing at 8.29% annually, underscoring how digital platforms translate app orders into incremental cup lifts. Specialty cafes expanding in Southeast Asia and the Middle East are introducing premium cup specifications that keep crema intact and print branding crisp. Loyalty apps encourage micro-purchases, which compound packaging volumes without requiring new footfall. Across regions, the result is a consistent, high-frequency pull on the paper cups market that aligns with retailer ambitions for frictionless service.

Government Bans on Single-Use Plastics

Legislators are turning single-use plastics into a costlier, restricted option, forcing a systemic shift toward fiber formats. The EU Packaging and Packaging Waste Regulation finalized in March 2024 mandates full recyclability and sets a 5% waste-cut target by 2030. South Australia banned plastic beverage containers from September 2024, instantly channeling demand to fiber cup alternatives. Scotland intends to levy a 25-pence surcharge on each single-use beverage cup by end-2025, nudging retailers toward reusable loops while positioning paper cups as the least-cost single-use substitute. These legal levers create predictable replacement cycles that let converters rationalize capex in new forming lines.

Disposal and Recycling Infrastructure Gaps

Many municipal systems still lack the equipment to delaminate cup fiber from coatings, so collected cups often end in landfill despite technical recyclability. Developing economies face limited material-recovery budgets, hindering paper cup sorting adoption. EU circular-economy rules tighten scrutiny on end-of-life pathways, and corporate buyers now demand evidence of regional cup recovery before awarding contracts. Until infrastructure catches up, the paper cups industry contends with reputational questions that can shift volumes to reusable pilots in niche cafes and venues.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of QSR and Food-Delivery Ecosystems

- Aqueous-Coated Fully-Recyclable Hot-Cup Launches

- Pulp-Price Volatility Squeezing Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hot cups represented 44.92% of 2025 volume, and the segment is projected to expand at a 5.24% CAGR through 2031. The paper cups industry benefits from a global surge in specialty coffee houses that require high heat retention and vivid on-cup graphics for brand storytelling. Premium barrier coatings and double-wall builds deliver both, letting chains justify higher ticket prices. Cold cups protect share in iced tea, soda, and smoothie channels, yet growth lags because competition from lightweight PET cups persists in warm climates. Cone and specialty designs occupy event catering niches where differentiation, not mass volume, rules. Starbucks' switch to mineral coatings underscores how hot cups anchor R&D investment and margin capture. Cold-cup innovation focuses on strawless lids and fiber inks, but without the thermal barrier imperative, unit values stay lower.

Hot-cup leadership also reflects regional weather patterns and beverage rituals. Northern Europe and North America experience extended cool seasons that sustain daily hot-drink demand. In APAC mega-cities, iced beverage upticks occur, but hot tea traditions keep baseline consumption high enough to support a balanced portfolio. The paper cups industry adapts by offering modular lamination lines that toggle between hot and cold specs, ensuring asset utilization year-round. Specialty roasters ask suppliers for smaller minimum order quantities with frequent artwork changeovers, a service level only advanced converters can accommodate. This client dynamic moderates fragmentation by favoring scale players that bundle design, forming, and logistics.

Double-wall cups held 47.10% share in 2025, preferred for superior hand comfort and heat insulation. They also serve as a tactile signal of premium positioning in chain cafes. Yet single-wall designs are forecast to grow fastest at 5.78% CAGR through 2031. This acceleration stems from cost-saving goals in price-sensitive markets and from coating technologies that allow thin walls without hurting performance. Aqueous liners with micro-air pockets give single-wall cups sufficient heat resistance, enabling QSR operators to downgrade wall count while meeting customer expectations. Triple-wall cups remain niche, used in industrial canteens where boiling-hot broths are common.

Shifts in e-commerce packaging policies-favoring lower-weight parcels to cut freight emissions-also help single-wall formats. Direct-to-consumer coffee roasters that ship boxed drink kits favor slim cups to fit tight carbon calculators. On factory floors, converters re-engineer forming cycles to align with single-wall geometry, increasing line speed. Still, double-wall cups keep a foothold in high-margin markets. Chains with strong brand equity treat the thicker feel as part of the sensory experience. The paper cups market thus offers a bifurcated product mix: single-wall for broad affordability and double-wall for revenue-rich flagships.

The Paper Cups Market Report is Segmented by Cup Type (Hot Paper Cups, Cold Paper Cups, and More), Wall Type (Single Wall, Double Wall, Triple Wall), Capacity (4-8 Oz, 9-12 Oz, and More), End User (Quick-Service Restaurants, Coffee Chains and Vending Operators, and More), Distribution Channel (Direct B2B Contracts, and More), and Geography. The Market Forecasts are Provided in Terms of Volume (Million Tonnes).

Geography Analysis

Asia-Pacific accounted for 39.10% of global tonnage in 2025 and is projected to grow at 6.55% CAGR to 2031, the highest among all regions. China's paper sector added 10% domestic capacity in 2024, ensuring ample substrate for cup converting in 2025. India's packaging market is expected to reach USD 204.81 billion by 2025, expanding at 26.7% CAGR, a scale that deepens end-market pull for cups in food delivery. Vietnam's packaging growth of 9.73% annually demonstrates manufacturing competitiveness that also feeds cup exports across ASEAN. Rising disposable incomes and a shift toward branded cafe culture underpin regional volume, making APAC the growth anchor of the paper cups industry.

North America remains a mature yet technologically progressive market. The PFAS phase-out finalized by the U.S. FDA in February 2025 is propelling adoption of aqueous and mineral barrier coatings. Georgia-Pacific invested USD 2 billion in seven U.S. facilities in 2024 to sustain production agility and comply with sustainability targets. Modern recycling systems and corporate ESG reporting encourage premium offerings, with converters competing on end-of-life certification rather than pure price. Unit growth is slower, but margins are stronger through value-added specs such as fiber lids.

Europe follows a regulation-first trajectory. Mandatory recyclability by 2030 ensures steady substitution away from plastic packaging to paper-based cups. Huhtamaki expanded fiber-lid capacity in Northern Ireland in October 2024 to meet regional demand for plastic-free components. The region adopts pay-per-cup or tax incentives to nudge consumers toward reusables but still positions fiber cups as the compliant single-use option. Eastern European growth pockets, driven by rising QSR penetration, help offset Western Europe's mature volumes.

The Middle East and Africa and South America constitute emerging opportunity zones. Infrastructure gaps and economic swings temper immediate scale, yet food-delivery apps and international coffee chains are planting early seeds. Converters form joint ventures with local paper mills to localize supply, mitigating currency risk and import tariffs. While their contribution to the paper cups market size is still modest, longer-term demographic trends suggest incremental tonnage upside.

- Huhtamaki Oyj

- Dart Container Corp.

- Graphic Packaging International

- Georgia-Pacific LLC

- Seda International Packaging

- Kap Cones Pvt Ltd

- ConverPack Inc.

- Go-Pak UK Ltd (SCGP)

- Benders Paper Cups

- Hotpack Global

- Tekni-Plex Inc.

- CEE Schisler Packaging

- International Paper Foodservice

- Stora Enso Food-Service Boards

- Lollicup USA (Karat)

- Detmold Group

- F-Bender & Co.

- Nissin Paper Products

- Reynolds Consumer Products

- Pactiv Evergreen

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for on-the-go beverages

- 4.2.2 Government bans on single-use plastics

- 4.2.3 Expansion of QSR and food-delivery ecosystems

- 4.2.4 Aqueous-coated fully-recyclable hot-cup launches

- 4.2.5 Zero-waste stadium and event procurement mandates

- 4.2.6 AI-driven high-speed forming lines lowering cost

- 4.3 Market Restraints

- 4.3.1 Disposal and recycling infrastructure gaps

- 4.3.2 Pulp-price volatility squeezing margins

- 4.3.3 Reusable cup loop pilots in coffee chains

- 4.3.4 PFAS-phase-out redesign and certification delays

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Cup Type

- 5.1.1 Hot Paper Cups

- 5.1.2 Cold Paper Cups

- 5.1.3 Cone and Specialty Cups

- 5.2 By Wall Type

- 5.2.1 Single Wall

- 5.2.2 Double Wall

- 5.2.3 Triple Wall

- 5.3 By Capacity (oz)

- 5.3.1 4-8

- 5.3.2 9-12

- 5.3.3 13-20

- 5.3.4 >20

- 5.4 By End User

- 5.4.1 Quick-Service Restaurants (QSR)

- 5.4.2 Coffee Chains and Vending Operators

- 5.4.3 Institutional Catering

- 5.4.4 Airlines and Railways

- 5.4.5 Others

- 5.5 By Distribution Channel

- 5.5.1 Direct (B2B Contracts)

- 5.5.2 Distributors and Wholesalers

- 5.5.3 Online B2B Marketplaces

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 United Arab Emirates

- 5.6.4.1.2 Saudi Arabia

- 5.6.4.1.3 Turkey

- 5.6.4.1.4 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Nigeria

- 5.6.4.2.3 Egypt

- 5.6.4.2.4 Rest of Africa

- 5.6.4.1 Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Huhtamaki Oyj

- 6.4.2 Dart Container Corp.

- 6.4.3 Graphic Packaging International

- 6.4.4 Georgia-Pacific LLC

- 6.4.5 Seda International Packaging

- 6.4.6 Kap Cones Pvt Ltd

- 6.4.7 ConverPack Inc.

- 6.4.8 Go-Pak UK Ltd (SCGP)

- 6.4.9 Benders Paper Cups

- 6.4.10 Hotpack Global

- 6.4.11 Tekni-Plex Inc.

- 6.4.12 CEE Schisler Packaging

- 6.4.13 International Paper Foodservice

- 6.4.14 Stora Enso Food-Service Boards

- 6.4.15 Lollicup USA (Karat)

- 6.4.16 Detmold Group

- 6.4.17 F-Bender & Co.

- 6.4.18 Nissin Paper Products

- 6.4.19 Reynolds Consumer Products

- 6.4.20 Pactiv Evergreen

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment