|

시장보고서

상품코드

1689789

혐기성 접착제 시장 : 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)Anaerobic Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

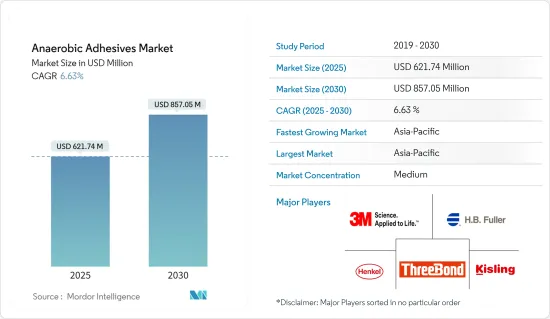

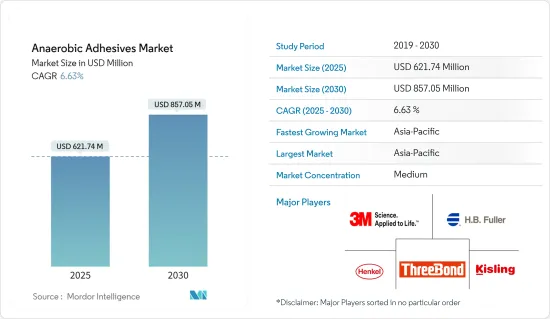

세계의 혐기성 접착제 시장 규모는 2025년 6억 2,174만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR 6.63%로 확대되어, 2030년에는 8억 5,705만 달러에 달할 것으로 예측됩니다.

COVID-19는 2020년 시장에 부정적인 영향을 미쳤습니다.

주요 하이라이트

- 중기적으로는 자동차 산업의 회복과 전기 및 전자 산업에서의 수요 증가가 연구 시장의 성장을 견인합니다.

- 반면, 혐기성 접착제의 고비용이 혐기성 접착제 시장의 성장을 저해하고 있습니다.

- 연구개발과 바이오기반 원료 증가는 재생가능에너지 시장에서의 주목이 높아짐에 따라 조사시장에 있어서 유리한 기회로서 기능할 가능성이 높습니다.

- 아시아태평양은 세계의 혐기성 접착제 시장을 독점하고 예측 기간 동안 가장 높은 CAGR로 성장할 가능성이 높습니다.

혐기성 접착제 시장 동향

자동차 및 운송산업에서의 수요 증가

- 자동차 산업에서는 유지 컴파운드, 파이프 실란트, 개스킷 실란트, 나사록 접착제가 널리 사용되고 있습니다.

- 이들은 엔진 및 방화벽 밀봉, 엔진 모니터 센서, 엔진 플러그 실란트, 나사 호스 커넥터 실란트, 엔진 룸 파이프 및 직선 나사용 나사 호스 니플 실란트, 나사 쿠 나사, 볼트, 너트 내부 실링 용도, 휠 베어링, 자동차 잠금 용도, 자동차 바디/프레임 볼트, 서스펜션 영역, 브레이크, 리어 엔드, 변속기, 기타 많은 용도로 사용되고 있습니다.

- 혐기성 접착제는 또한 나사 잠금, 홀딩, 개스킷, 스레드 씰과 같은 용도에 대한 항공우주 산업의 유지 보수, 수리 및 작동(MRO) 용도에서 사용됩니다.

- 내연기관에서 전기자동차로의 최근의 시프트는 자동화 기술의 기술 혁신을 추진하고 있습니다.

- 접착제는 또한 접촉 부식을 방지하고 전기 모터의 높은 동력을 견디기 위해 필수적인 내충격성을 제공할 수 있기 때문에 기존 접합 방법보다 선호되고 있습니다.

- 세계의 주요 자동차 제조업체는 새로운 제품 라인을 개발해, 기존의 제조 설비를 전환하는 것으로, 전기자동차의 미래를 가속할 계획을 발표하고 있습니다.

- Toyota는 2030년까지 30차종의 배터리 전기자동차(BEV)를 전개한다고 발표했습니다.

- Volvo는 2030년까지 완전한 전기자동차 회사가 될 것을 약속했습니다.

- General Motors는 2025년까지 북미에서 30차종의 EV와 100만대의 생산 능력을 목표로 합니다.

- 2021년에는 세계에서 8,014만대의 자동차가 생산되었습니다. 이것은 2020년 대비 3% 증가입니다.

- 아시아태평양은 2021년에 2020년 대비 6% 증가한 4,673만대, 아프리카는 2021년에 2020년 대비 16% 증가한 93만대로 대폭적인 성장을 보였습니다.

- 2022년에는 합작회사인 GACHonda가 중국 광저우에서 신공장 건설을 시작했습니다.

- 이러한 동향이 혐기성 접착제 시장을 견인하고 있습니다.

시장을 독점하는 아시아태평양

- 아시아태평양은 특히 중국이나 인도와 같은 국가를 중심으로 한 다양한 신흥 시장에 의해 시장을 독점하고 있습니다.

- 중국은 세계 최대의 자동차 제조업체입니다. OICA에 따르면, 2021년의자동차 생산 대수는 2,608만대에 달했고, 2020년 2,523만대에서 3% 증가했습니다.

- 2021년 11월에는 2020년 동시기와 비교해 배터리 내장형 전기차가 106%의 성장을 보였습니다.

- 중국은 또한 최대 항공기 제조업체 중 하나이며 국내 항공 여객의 최대 시장 중 하나이기도 하며, 이 나라의 항공기 부품 및 조립 제조 부문은 급성장하고 있으며 200개 이상의 소형 항공기 부품 제조업체가 혐기성 접착제의 사용량과 수요를 늘리고 있습니다. Boeing Commercial Outlook 2021-2040에 따르면, 중국에서는 2040년까지 약 8,700대가 새롭게 납입되어 시장 서비스액은 1조 8,000억 달러에 이르게 됩니다.

- 게다가 OICA에 따르면, 인도에서는 2021년에 약 4,399만 1,112대의 자동차가 생산되어, 2020년의 생산 대수 338만 1,819대에 비해 30% 증가했습니다.

- 항공우주 부문에서는 India Brand Equity Foundation(IBEF)에 따르면, 이 나라의 항공 산업은 향후 4년간 3,500억 루피(약 49억 9,000만 달러)의 투자가 전망되고 있습니다.

- 인도는 2025년까지 세계 제5위의 소비자용 전자기기 일렉트로닉스 산업이 될 것으로 예상되고 있습니다. 또한 인도에서는 4G/LTE 네트워크의 전개나 사물인터넷(IoT)등의 기술 이행이 전자 제품의 채용을 촉진하고 있습니다.

- 인도의 거대한 건설 부문은 2022년까지 세계 3위의 건설 시장이 될 것으로 예상되고 있습니다. Pradhanmantri Awas Yojana에서는 인도 정부는 주택구입 및 건설에 관한 저소득자층에 대해 1만 2,000루피(약 1만 4,550달러)와 9,000루피(1만 920달러)까지의 대출에 대해 각각 3%와 4%의 이자보급을 실시하기로 결정했습니다.

- 전체적으로, 이러한 요인은 모두, 예측 기간 중에 이 지역에 있어서의 혐기성 접착제 수요에 영향을 준다고 생각됩니다.

혐기성 접착제 산업 개요

세계의 혐기성 접착제 시장은 다양한 지역에 걸친 다양한 세계와 국내 진출기업에 의해 반고체화하고 있습니다. 시장의 주요 기업에는 Henkel AG & Co. KGaA, 3M, H. B. Fuller Company, Kisling AG, and ThreeBond Holdings Co., Ltd 등이 있습니다(특별한 순서 없음).

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 자동차산업의 회복

- 전기 및 전자 산업에서의 수요 증가

- 성장 억제요인

- 혐기성 접착제의 높은 비용

- 기타 억제요인

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화

- 제품 유형

- 나사록제

- 스레드 실란트

- 유지 컴파운드

- 개스킷 실란트

- 최종 사용자 산업

- 자동차 및 운수

- 전기 및 전자

- 공업용

- 건축 및 건설

- 기타

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 합병, 인수, 합작사업, 제휴, 협정

- 시장 랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- 3M

- Anabond Limited

- Asec Co., Ltd

- HB Fuller Company

- Henkel AG and Co. KGaA

- Hi-Bond Chemicals

- Kisling AG

- Krylex(Chemence)

- Metlok Private Limited

- Novachem Corporation ltd

- Parson Adhesives, Inc.

- Permabond LLC.

- ThreeBond Holdings Co., Ltd

제7장 시장 기회와 앞으로의 동향

- 바이오 원료의 연구 개발과 이용 증가

- 신재생에너지 시장에서의 주목의 고조

The Anaerobic Adhesives Market size is estimated at USD 621.74 million in 2025, and is expected to reach USD 857.05 million by 2030, at a CAGR of 6.63% during the forecast period (2025-2030).

COVID-19 negatively impacted the market in 2020. However, the market recovered significantly in 2021, owing to rising consumption from various end-user industries such as electrical and electronics, building and construction, and others.

Key Highlights

- Over the medium term, recovering the automotive industry and increasing demand from electrical and electronics industries are driving the growth of the studied market.

- On the flip side, the high cost of anaerobic adhesives hinders the growth of the anaerobic adhesives market.

- Nevertheless, increasing research and development and bio-based raw materials, coupled with growing prominence in the renewable energy market, are likely to act as lucrative opportunities for the studied market.

- Asia-Pacific is likely to dominate the global anaerobic adhesives market and is likely to grow with the highest CAGR during the forecast period.

Anaerobic Adhesives Market Trends

Increasing Demand from the Automotive and Transportation Industry

- In the automotive industry, retaining compounds, pipe sealants, gasket sealants, and thread-locking adhesives are widely used.

- They are used in the applications of engine and firewall sealing, engine monitor sensors, engine plug sealants, threaded hose connector sealants, threaded hose nipple sealants for pipes and straight threads of engine compartments, for interior sealing applications of thread-locking screws, bolts, and nuts, wheel bearings, automotive locking applications, automotive body/frame bolts, suspension areas, brakes, rear end, and transmission and many other applications.

- Anaerobic adhesives are also used in aerospace industry maintenance, repair, and operation (MRO) applications for applications including thread-locking, retaining, gasketing, and thread sealing. These adhesives help manufacturers avoid unnecessary machining of a wide range of mechanical components during MRO.

- The recent shift from Internal Combustion Engines to electric vehicles is driving innovation in automation technologies. Anaerobic adhesives replace mechanical fasteners as they may accommodate movements caused by thermal expansion and are not susceptible to corrosion.

- Adhesives are also preferred over conventional joining methods as they can prevent contact corrosion and provide impact resistance that is essential for withstanding the high dynamic forces of electric motors.

- The major automakers globally have announced plans to accelerate their electric vehicle future by developing new product lines and converting existing manufacturing facilities. For example:

- Toyota announced the roll-out of 30 Battery Electric Vehicles (BEV) models by 2030.

- Volvo is committed to becoming a fully electric car company by 2030.

- General Motors aims for 30 EV models and an installed production capacity of 1 million units in North America by 2025.

- In 2021, globally, 80.14 million automobile units were produced. This was an increase of 3% compared to 2020. The production of automobiles in Europe reduced by 4% compared to 2020, to 16.33 million units. The production increased by 3% compared to 2020 in America to 16.15 million units.

- The Asian-Pacific region witnessed a growth of 6% in 2021 compared to 2020 to 46.73 million units, while Africa witnessed a significant growth of 16% in 2021 compared to 2020 to reach 0.93 million units.

- In 2022, the joint venture company GAC Honda started the construction of a new car plant in Guangzhou, China. The plant is expected to have a capacity to produce 120,000 electric vehicles per year and is expected to start production by 2024. The investment amount is expected to be CNY 3.49 billion (~USD 0.5 billion).

- Such trends are driving the market for anaerobic adhesives.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific dominates the market owing to various emerging markets in the region, specifically in countries like China and India.

- China is the largest manufacturer of automobiles globally. In 2021, according to the OICA, the automotive production in the country reached 26.08 million, which increased by 3%, compared to 25.23 million vehicles produced in 2020.

- A growth of 106% in battery-plugged-in electric vehicles was witnessed in November 2021 compared to the same period in 2020. The country's sales of electric vehicles reached around 413,094 units in November 2021. In addition, the market share also increased to 19%, including 15% of all-electric and 4% of plug-in hybrid cars.

- China is also one of the largest aircraft manufacturers and one of the largest markets for domestic air passengers. Moreover, the country's aircraft parts and assembly manufacturing sector has been growing rapidly, with over 200 small aircraft parts manufacturers increasing the usage and demand for anaerobic adhesives. According to the Boeing Commercial Outlook 2021-2040, in China, around 8,700 new deliveries will be made by 2040, with a market service value of USD 1,800 billion. Owing to such new deliveries in the country, the demand for the market studied is likely to rise.

- Furthermore, in India, according to OICA, around 43,99,112 vehicles were produced in 2021, which increased by 30% compared to 3,381,819 units manufactured in 2020.

- In the aerospace sector, according to the India Brand Equity Foundation (IBEF), the country's aviation industry is expected to witness INR 35,000 crore (~USD 4.99 billion) investment in the next four years. The country is projected to have a demand for 2,100 aircraft over the next two decades, amounting to over USD 290 billion in sales. Owing to these factors, the demand for anaerobic adhesives from the aerospace sector is expected to rise in the future.

- India is expected to become the global fifth-largest consumer electronics and appliances industry by 2025. Additionally, in India, technology transitions, such as the rollout of 4G/LTE networks and IoT (Internet of Things), are driving the adoption of electronic products. Initiatives, such as 'Digital India' and 'Smart City' projects, raised the demand for IoT in the country.

- India's huge construction sector is expected to become the global third-largest construction market by 2022. Various policies implemented by the Indian government, such as the Smart Cities project, Housing for all by 2022, etc., are expected to bring the needed impetus to the slowing construction industry. For instance, in the Pradhanmantri Awas Yojana, the Indian government has decided to provide interest subvention of 3% and 4% for loans of up to INR 12 lakhs (~USD 14.55 thousand) and INR 9 lakhs (USD 10.92 thousand), respectively, for the lower strata of society concerning buying and building homes.

- Overall, all such factors will affect the demand for anaerobic adhesives in the region over the forecast period.

Anaerobic Adhesives Industry Overview

The global anaerobic adhesives market is semi-consolidated, with various global and domestic players across different regions. However, the top five players in the market control a majority share of the global market. Key players in the anaerobic adhesives market include Henkel AG & Co. KGaA, 3M, H. B. Fuller Company, Kisling AG, and ThreeBond Holdings Co., Ltd, among others ( not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Recovering Automotive Industry

- 4.1.2 Increasing Demand From The Electrical And Electronics Industries

- 4.2 Restraints

- 4.2.1 High Cost Of Anaerobic Adhesives

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products And Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Threadlockers

- 5.1.2 Thread Sealants

- 5.1.3 Retaining Compound

- 5.1.4 Gasket Sealants

- 5.2 End-user Industry

- 5.2.1 Automotive and Transportation

- 5.2.2 Electrical and Electronics

- 5.2.3 Industrial

- 5.2.4 Building and Construction

- 5.2.5 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Anabond Limited

- 6.4.3 Asec Co., Ltd

- 6.4.4 H.B. Fuller Company

- 6.4.5 Henkel AG and Co. KGaA

- 6.4.6 Hi-Bond Chemicals

- 6.4.7 Kisling AG

- 6.4.8 Krylex (Chemence)

- 6.4.9 Metlok Private Limited

- 6.4.10 Novachem Corporation ltd

- 6.4.11 Parson Adhesives, Inc.

- 6.4.12 Permabond LLC.

- 6.4.13 ThreeBond Holdings Co., Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Research And Development and Usage of Bio-based Raw Materials

- 7.2 Growing Prominence in Renewable Energy Market