|

시장보고서

상품코드

1910724

유럽의 소비자용 포장 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Consumer Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

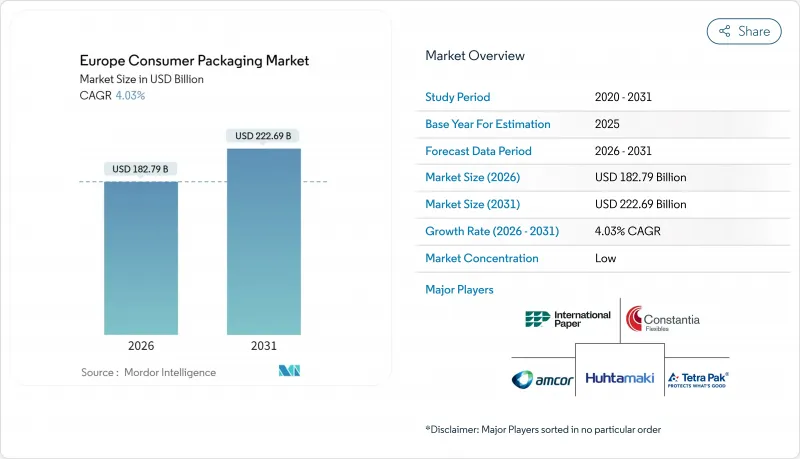

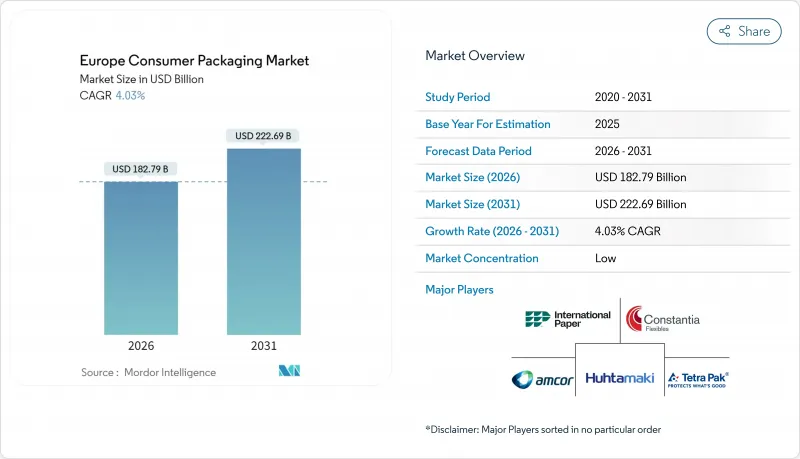

유럽의 소비자용 포장 시장은 2025년에 1,757억 1,000만 달러로 평가되었으며, 2026년 1,827억 9,000만 달러에서 2031년까지 2,226억 9,000만 달러에 이를 것으로 예상됩니다. 예측 기간(2026-2031년)에 있어서 CAGR은 4.03%를 나타낼 것으로 전망되고 있습니다.

성장은 EU 포장 및 포장 폐기물 규제, 폐쇄형 루프 시스템에 대한 브랜드 헌신의 가속화, EC 충진의 지속적인 기세에 의해 견인됩니다. 섬유, 단일 PET, 경량 금속 소재로의 재료 치환이 진행됨으로써 자본 배분이 재구축되는 한편, 에너지 가격의 급등에 의해 컨버터는 조업 규모의 재검토를 강요당하고 있습니다. 디지털 인쇄 기술은 설계부터 발매까지의 사이클을 단축해 SKU의 세분화를 지원, 보증금 반환 제도는 재생 원료를 고부가가치 음료 용도로 이끌어 경쟁 환경을 더욱 변화시키고 있습니다.

유럽의 소비자용 포장 시장 동향과 인사이트

편의성을 추구하는 유연성 플라스틱 포장에 대한 수요

도시 지역의 외출처 소비가 회복됨에 따라 유리 및 금속 용기에서 연포장으로의 전환이 진행되고 있습니다. 휴대성과 신선도를 중시하는 25-45세의 모바일 라이프 스타일에 대응해, 분량 관리된 파우치 포장에 이지 오픈·재봉 가능 기능이 부가되고 있습니다. 가격 변동은 소폭으로 남아 있습니다. 2024년 말에 7미크론 알루미늄박이 4% 상승했지만, 가공업자는 배리어 코팅을 한 경량 필름에 의해 코스트 상승을 상쇄했습니다. 이로 인해 부피가 커지지 않고 보존 기간이 연장됩니다. 현재는 기능성이 형태에의 고집을 웃도고, 소스나 베이비 푸드등의 액체 용도가, 보다 무거운 경질 용기로부터 쏟아부 첨부 파우치로 이행하고 있습니다. 결과적으로 식품 및 개인 관리 분야 모두에서 연포장의 점유율 확대가 지속됩니다.

전자상거래의 급성장은 마지막 마일 포장 수요를 창출

소비자 직송 물류에서는 컨베이어로부터의 낙하, 온도 변화, 현관처에서의 검품 등, 포장이 견뎌야 하는 접촉점이 복수 추가됩니다. PPWR(포장 폐기물 규제)은 2030년까지 운송·판매용 포장의 40%를 재이용 가능하게 하는 것을 의무화하고 있어 소매업체에게는 자동화와 지속가능성의 조화가 요구되고 있습니다. 완충성과 체적 효율을 양립시키는 성형 섬유 인서트나 정밀 설계의 골판지 상자에 대한 수요가 급증하고 있습니다. 폴란드와 스페인에서는 EC 보급률이 가장 급격히 상승하고 있으며 유럽의 소비자용 포장 시장에서 지역간 성장 격차가 확대되고 있습니다. 브랜드 오너는 디지털 인쇄를 활용해, 각 소포를 마케팅의 캔버스로 변혁을 창출합니다. 개봉 체험을 코스트 센터에서 수익원으로 승화시키고 있습니다.

다양한 폴리머 및 종이 펄프 가격

원료 가격의 변동은 가공업자의 이익률을 압박하고 분기 지수에 연동하는 고정 가격 계약을 혼란시키고 있습니다. 폴리에틸렌 가격은 2024년 초 하류 수요 침체로 연화되었지만 아시아 공급 라인이 불안정해지면 PET가 희박해 투입자재 가격 동향 예측의 어려움을 보였습니다. 섬유 분야에서는 제지 공장의 유지 보수 정지와 물류 병목 현상으로 인해 2024년 2분기에 코트지 가격이 약 10% 급등한 뒤 침착했습니다. 재활용 및 펄프 자산에 대한 수직 통합이 지지를 받고 있는데, 이는 혁신과 지리적 확대에 충당되어야 하는 자본을 고정화합니다.

부문 분석

종이 및 판지 부문은 EC 물류업체와 외식산업용 일회용 제품을 원동력으로 2025년 매출의 35.22%를 유지했습니다. 유럽의 종이제 소비자용 포장 시장 규모는 규제면에서의 호의와 소비자의식이 지원 재료가 되기 때문에 완만한 확대가 전망됩니다. 그러나, PET의 5.74%라는 CAGR은 보증금 반환 제도의 경제성과 식품 등급 재생재 사용을 내거는 브랜드 공약이 가져온 결정적인 기세 전환을 부각하고 있습니다. 유럽의 소비자용 포장 시장 점유율 확대는 2024년에 평균 24%의 재생 수지 사용률을 달성한 단층 PET 음료 병에 기인하여 클로즈드 루프의 실현 가능성을 실증하고 있습니다. 한편, PE(폴리에틸렌)와 PP(폴리프로필렌)은 새로운 규제에 의해 일회용 캡, 칼집, 얇은 쇼핑백이 시장에서 사라지는 역풍에 휩쓸리고 있습니다.

PET의 우위성은 최적화된 플랜트에서 75%에 달하는 기계적 재활용 수율에 의해 더욱 강화되어 섬유계 카톤과의 탄소 차이를 줄이고 있습니다. 한편, 유리 산업 단체는 노의 전기화에 200억 유로의 투자를 호소하고 있지만, 급등하는 전력 요금이 경쟁력을 흐리게 하고 있습니다. 알루미늄은 순환성에서 여전히 우위를 유지하지만, 사용된 캔 시트의 유통성은 지역 회수율에 따라 달라집니다. 특수 폴리머는 의약품 블리스터 포장이나 퍼스널케어 제품의 펌프 부품 등 균일한 재활용성보다 성능이 중시되는 분야에서 성장 기회를 발견하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 서포트(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 편리성을 중시한 유연성이 있는 플라스틱 포장에 대한 수요

- 전자상거래의 급성장에 의한 라스트마일 포장 수요 창출

- 경량화 및 이지 오픈 포장으로의 이행

- EU의 일회용 플라스틱 지령이 단일 소재의 연구 개발을 촉진

- 보증금 반환 시스템에 의한 재생 폴리에틸렌(rPET) 수요 증가

- 디지털 인쇄 기술에 의한 SKU의 다양화와 소량 생산의 실현

- 시장 성장 억제요인

- 폴리머 및 종이 펄프 가격의 변동성

- 재활용이 곤란한 포장 형태에 대한 EU역내에서의 금지 확대

- 다층 연포장의 리사이클 갭

- 에너지 가격의 급등에 의한 유리·금속 비용의 상승

- 업계 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 소재별

- 플라스틱

- PE(폴리에틸렌)

- PP(폴리프로필렌)

- PET(폴리에틸렌 테레프탈레이트)

- PVC(폴리염화비닐)

- 기타 플라스틱

- 종이 및 판지

- 골판지

- 용기용 원판지 및 라이너보드

- 성형 섬유

- 유리

- 금속

- 캔

- 캡 및 마개

- 튜브

- 기타 금속

- 플라스틱

- 포장 형태별

- 경질 포장

- 연질 포장

- 반경질 포장

- 최종 사용자 업계별

- 식품

- 음료

- 의약품 및 헬스케어

- 화장품, 퍼스널케어 및 홈 케어

- 기타 최종 사용자 산업

- 국가별

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 폴란드

- 기타 유럽

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Amcor PLC

- Huhtamaki Oyj

- Mondi PLC

- International Paper Company

- Tetra Pak International SA

- Ardagh Group SA

- Crown Holdings, Inc.

- Constantia Flexibles Holding GmbH

- Sealed Air Corporation

- Sonoco Products Company

- Stora Enso Oyj

- Smurfit Kappa Group Limited

- Ball Corporation

- Berry Global, Inc.

- Greiner Packaging International GmbH

- Albea Group SAS

- Gerresheimer AG

- Vetropack Holding AG

- Massilly Holding

제7장 시장 기회와 향후 전망

KTH 26.01.26The Europe consumer packaging market was valued at USD 175.71 billion in 2025 and estimated to grow from USD 182.79 billion in 2026 to reach USD 222.69 billion by 2031, at a CAGR of 4.03% during the forecast period (2026-2031).

Growth is steered by the EU Packaging and Packaging Waste Regulation, accelerating brand commitments to closed-loop systems, and sustained momentum in e-commerce fulfillment. Material substitution toward fiber, mono-PET, and lightweight metal formats is reshaping capital allocation, while energy-price shocks force converters to reassess operating footprints. The competitive field is further altered by digital printing, which shortens design-to-launch cycles and supports SKU fragmentation, and by deposit-return infrastructure that channels recycled feedstock into high-value beverage applications.

Europe Consumer Packaging Market Trends and Insights

Convenience-driven demand for flexible plastic packs

Flexible formats continue to migrate volume from glass and metal as on-the-go consumption rebounds across urban corridors. Portion-controlled pouches with easy-open reclosable features meet the mobile lifestyle of 25- to 45-year-olds who prize portability and freshness. Price movements remain modest. 7-micron aluminum foil rose 4% in late 2024, but converters offset cost upticks through barrier-coated lightweight films that extend shelf life without adding bulk. Functionality now outweighs format loyalty, drawing liquid applications such as sauces and baby food toward spouted pouches and away from heavier rigid alternatives. The result is sustained share capture for flexibles in both food and personal-care aisles.

E-commerce boom creating last-mile packaging needs

Direct-to-consumer fulfillment adds multiple touchpoints where packs must survive conveyor drops, temperature shifts, and doorstep scrutiny. The PPWR mandates 40% reusable transport and sales packaging by 2030, pressuring retailers to harmonize automation with sustainability. Demand is surging for molded-fiber inserts and precision-engineered corrugated boxes that balance cushioning with dimensional efficiency. Poland and Spain show the steepest e-commerce penetration curves, widening the regional growth gap within the European consumer packaging market. Brand owners also leverage digital print to transform each parcel into a marketing canvas, elevating unboxing to a revenue lever rather than a cost center.

Volatile polymer and paper pulp prices

Feedstock swings erode converter margins and disrupt pricing contracts fixed on quarterly indices. Polyethylene values softened in early 2024 amid weak downstream demand, yet PET tightened when Asian supply lines faltered, demonstrating the difficulty of forecasting input trajectories. On the fiber side, coated paper spiked nearly 10% in Q2 2024 before easing, driven by mill maintenance outages and logistics bottlenecks. Vertical integration into recycling or pulp assets is gaining favor, but it locks capital that could fund innovation or geographic expansion.

Other drivers and restraints analyzed in the detailed report include:

- Shift toward lightweighting and easy-open formats

- EU Single-Use Plastics Directive spurring mono-material R&D

- Expanding EU bans on difficult-to-recycle formats

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Paper and board defended 35.22% of 2025 revenue on the strength of e-commerce shippers and foodservice disposables. The Europe consumer packaging market size for paper-based solutions is projected to expand modestly as regulatory goodwill and consumer perception remain supportive. However, PET's 5.74% CAGR underscores a decisive momentum swing driven by deposit-return economics and brand pledges for food-grade recycled content. Europe consumer packaging market share gains accrue to mono-PET beverage bottles that averaged 24% recycled resin in 2024, validating closed-loop viability. In contrast, PE and PP navigate headwinds from single-use caps, cutlery, and thin grocery bags disappearing under new bans.

The PET narrative is reinforced by mechanical recycling yields that reach 75% in optimized plants, narrowing the carbon delta versus fiber-based cartons. Meanwhile, glass lobbies are campaigning for EUR 20 billion in furnace electrification, but elevated electricity tariffs cloud competitiveness. Aluminum retains a strong circularity story, yet the liquidity of post-consumer can sheet fluctuates with regional redemption rates. Specialty polymers hold pockets of growth in pharma blister packs and personal-care pump components, where performance trumps uniform recyclability mandates.

The Europe Consumer Packaging Market Report is Segmented by Material (Plastic (PE, PP, PET, and More), Paper and Board (Cartonboard, Molded Fiber, and More), Glass, and Metal (Cans, Caps and Closures, Tubes, and More)), Packaging Format (Rigid, Flexible, and Semi-Rigid), End-User Industry (Food, Beverage, Pharmaceutical and Healthcare, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Amcor PLC

- Huhtamaki Oyj

- Mondi PLC

- International Paper Company

- Tetra Pak International SA

- Ardagh Group S.A.

- Crown Holdings, Inc.

- Constantia Flexibles Holding GmbH

- Sealed Air Corporation

- Sonoco Products Company

- Stora Enso Oyj

- Smurfit Kappa Group Limited

- Ball Corporation

- Berry Global, Inc.

- Greiner Packaging International GmbH

- Albea Group S.A.S.

- Gerresheimer AG

- Vetropack Holding AG

- Massilly Holding

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Convenience-driven demand for flexible plastic packs

- 4.2.2 E-commerce boom creating last-mile packaging needs

- 4.2.3 Shift toward lightweighting and easy-open formats

- 4.2.4 EU Single-Use Plastics Directive spurring mono-material R&D

- 4.2.5 Deposit-return schemes scaling rPET demand

- 4.2.6 Digital printing enabling SKU proliferation and short-runs

- 4.3 Market Restraints

- 4.3.1 Volatile polymer and paper pulp prices

- 4.3.2 Expanding EU bans on difficult-to-recycle formats

- 4.3.3 Recycling gaps for multilayer flexibles

- 4.3.4 Energy-price shocks inflating glass and metal costs

- 4.4 Industry Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Plastic

- 5.1.1.1 PE (Polyethylene)

- 5.1.1.2 PP (Polypropylene)

- 5.1.1.3 PET (Polyethylene Terephthalate)

- 5.1.1.4 PVC (Polyvinyl Chloride)

- 5.1.1.5 Other Plastics

- 5.1.2 Paper and Board

- 5.1.2.1 Cartonboard

- 5.1.2.2 Containerboard and Linerboard

- 5.1.2.3 Molded Fiber

- 5.1.3 Glass

- 5.1.4 Metal

- 5.1.4.1 Cans

- 5.1.4.2 Caps and Closures

- 5.1.4.3 Tubes

- 5.1.4.4 Other Metals

- 5.1.1 Plastic

- 5.2 By Packaging Format

- 5.2.1 Rigid

- 5.2.2 Flexible

- 5.2.3 Semi-rigid

- 5.3 By End-user Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Cosmetics, Personal and Home Care

- 5.3.5 Other End-user Industry

- 5.4 By Country

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Poland

- 5.4.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor PLC

- 6.4.2 Huhtamaki Oyj

- 6.4.3 Mondi PLC

- 6.4.4 International Paper Company

- 6.4.5 Tetra Pak International SA

- 6.4.6 Ardagh Group S.A.

- 6.4.7 Crown Holdings, Inc.

- 6.4.8 Constantia Flexibles Holding GmbH

- 6.4.9 Sealed Air Corporation

- 6.4.10 Sonoco Products Company

- 6.4.11 Stora Enso Oyj

- 6.4.12 Smurfit Kappa Group Limited

- 6.4.13 Ball Corporation

- 6.4.14 Berry Global, Inc.

- 6.4.15 Greiner Packaging International GmbH

- 6.4.16 Albea Group S.A.S.

- 6.4.17 Gerresheimer AG

- 6.4.18 Vetropack Holding AG

- 6.4.19 Massilly Holding

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment