|

시장보고서

상품코드

1689936

미국의 비디오 감시 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)US Video Surveillance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

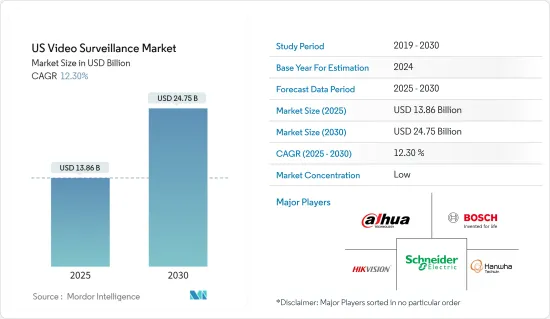

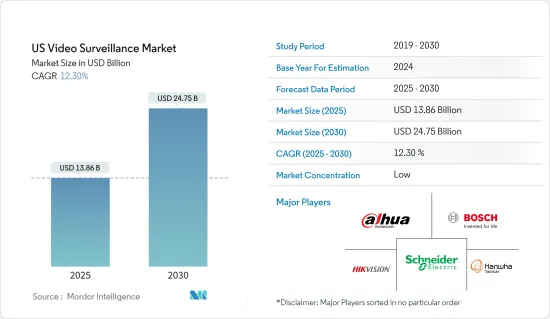

미국의 비디오 감시 시장 규모는 2025년에 138억 6,000만 달러로 추정되고, 시장 예측 기간 2025년부터 2030년까지 CAGR 12.3%로 성장할 전망이며, 2030년에는 247억 5,000만 달러에 달할 것으로 예측됩니다.

미국에서 감시 카메라는 호텔, 레스토랑, 오피스 빌딩 등 민간 소매 및 상업 시설에서 가장 일반적입니다.

주요 하이라이트

- 이 나라에서는 스마트 홈 보안 카메라의 보급이 진행되고 있으며, 시장 조사 대상이 더욱 확대될 가능성이 있습니다. AI 기반의 비디오 분석은 효율성을 더욱 향상시키고, 특히 스마트 시티 용도에서 비즈니스에 보안 관련 이외의 많은 인사이트를 제공합니다. 최근의 동향에서 아마존은 AWS Panorama 기술을 발표했으며 통합업체는 개발자와 협력하여 제조업체에 관계없이 비디오 모니터링을 위해 맞춤형 딥러닝 및 비디오 분석 앱을 손쉽게 제작할 수 있습니다.

- 미국에서는 최근 몇 년동안 비디오 감시의 사용이 확대되고 있습니다. 통합형 비디오 감시에는 사용자가 효율적이고 신속하게 정보를 전송할 수 있는 기술이 탑재되어 있습니다. 그러나 이 기능은 해킹이나 캡처된 시나리오의 기밀성을 위험에 빠뜨릴 수 있습니다. 악의적인 조작은 무단 사용자에게 비디오 영상 및 클립의 부드러운 전송을 통해 이루어집니다.

- 최근 몇 년간 비디오 감시 시스템은 사물 인터넷(IoT)의 일부가 되었습니다. IoT 센서는 종종 공기 중의 오염물질 수준, 소음 수준, 진동 등 인간 이상을 감지할 수 있습니다. 이를 통해 사용자는 위협이 되는 영역을 모니터링할 수 있으므로 많은 카메라 기반 모니터링 솔루션에 통합되는 태세가 있습니다.

- 그러나 다른 IoT 시스템과 마찬가지로 내재된 보안 위험이 사용자의 프라이버시를 크게 침해할 수 있습니다. 주로 딥러닝을 기반으로 한 고급 머신러닝 기술이 연구되어 무기 감지, 화재 감지, 상점 쇼핑, 얼굴 인식 센서, 이상 감지 등 여러 작업을 자동화하기 위해 최신 비디오 감시 시스템에 통합되었습니다.

- 주요 산업별로는 직원의 행동을 변화시키고 더 나은 결과를 제공하는 더 나은 플랫폼으로 모니터링이 신뢰됩니다. 기업에 의한 감시 전술은 직원들에게 큰 악영향을 미쳤고, 프라이버시 문제의 발생, 스트레스 증가, 정체성의 상실을 초래했습니다. 그러나 어떤 침입 기술도 그렇듯이 공공 캠코더를 도입하는 이점은 비용 및 위험과 균형을 맞추어야 합니다.

미국의 비디오 감시 시장 동향

동영상 분석이 시장을 크게 성장

- 미국에서는 많은 대기업이 보다 정교한 보안 모니터링 시스템을 필요로 하므로 동영상 분석 분야 개발에 가장 기여할 것으로 기대되고 있습니다. 이 업계는 주로 기술적 지식에 대한 접근성, 실시간으로 실용적인 정보에 대한 공개 회사의 필요성 증가, 기술적으로 업그레이드된 공공 보호 인프라에 대한 국가의 필요성 확대에 의해 뒷받침됩니다.

- 혁신적인 능력에 대한 접근은 수많은 중요한 기술 사업의 존재에 의해 촉진되었습니다. 미국은 비디오 감시의 주요 부문을 장악하고 있으며 업계를 전진시키고 있습니다. 게다가 테러 공격의 가능성 때문에 당국은 많은 지역에 고급 감시 장치를 설치할 수 밖에 없습니다. 또한 다양한 업계에서 보안 위협을 파악하기 위해 비디오 분석 시스템을 도입하고 있습니다.

- 미국에서는 감시 카메라가 아날로그 카메라를 대체하는 경우가 늘고 있습니다. 이러한 카메라에는 강력한 얼굴과 피사체 식별 기술이 탑재되어 있어 감시자료를 지속적으로 수집하여 방대한 공개 데이터베이스를 작성하고 있습니다. 게다가 이 나라의 민주주의 틀은 CCTV 시스템의 도입을 강력히 지지합니다. 예를 들어, 국토 안보부는 비디오 보안 카메라를 배포하기 위해 지방 자치 단체에 수십억 달러의 안전 자금을 지불합니다. 연방 정부의 지원은 비디오 분석 수요를 높이고 예측 기간 동안 비디오 감시 장비의 개발을 촉진할 것으로 예상됩니다.

- 주요 기술 기업의 지역 개척 증가는 예측 기간 동안 시장 성장에 기여할 것으로 보입니다. 최근 Cisco Meraki는 Kloudspot과 협력하여 직원과 소비자에게 안전하고 스마트한 작업 공간을 제공할 수 있도록 기업을 지원하고 있습니다.

주택이 큰 시장 잠재력을 가지고 있습니다.

- 주택용 비디오 감시 솔루션은 하나 이상의 녹화 장치를 네트워크에 연결하고 획득한 비디오 및 오디오 데이터를 특정 위치로 전송합니다. 사진은 실시간으로 시청되거나 중앙 스테이션으로 전송되어 녹화 및 저장됩니다. 위협 증가와 범죄 행위로 인한 보안 감시 용품의 필요성 증가는 국내 비디오 감시 시스템 수요를 견인하고 있습니다.

- 스마트 홈의 출현으로 최근 몇 년간 주택 분야에서의 비디오 감시 시스템의 주목도가 높아지고 있습니다. 이 분야에서 구현되는 모니터링 시스템은 모니터링 및 액세스 제어와 같은 다양한 용도를 가지고 있습니다. 이러한 시스템에는 움직임 감지 기능과 야간 암시 기능도 탑재되어 있습니다.

- 이 나라에서는 빈집 발생률이 높기 때문에 최근에는 감시 카메라 등의 보안 시스템의 도입이 증가하고 있어 속도 저하에 도움이 되고 있습니다. 예를 들어 FBI에 따르면 2022년 10월 미국에서 2021년 빈집 발생률은 인구 10만 명당 271.1건이었습니다. 이는 강도 발생률이 인구 100,000명당 308건이었던 전년보다 하락했음을 나타냅니다.

- 비디오 분석은 주택용 보안 비디오 감시 기술에서 중요한 역할을 하고, 알람의 오작동을 줄이고, 의심스러운 상황을 감지하는 시스템의 능력을 향상시킵니다. 1만 가구의 광대역 가구를 대상으로 하는 업계 전문가에 의한 소비자 조사에 따르면 미국의 광대역 가구 중 스마트 비디오 도어벨을 구입하려는 26%의 가구에서는 구매할 특정 비디오 도어벨을 선택할 때 인공지능(AI) 또는 고급 분석 기능이 필수적이라고 평가하는 사람이 대부분이었습니다.

미국 비디오 감시 산업 개요

미국의 비디오 감시 시장은 경쟁이 심하고 영향력 있는 기업으로 구성되어 있습니다. 이 시장은 내외 시장세력에 의한 효과적인 압력으로 성장률이 높아지고 있습니다. 시장에 진입하는 주요 기업으로는 Dahua Technology, Hikvision Digital Technology, Hanwha Techwin, Schneider Electric SE, Robert Bosch GmbH 등이 있습니다.

2022년 9월-영상 중심 지능형 IoT 솔루션의 세계 리더인 Dahua Technology USA는 소비자에게 야간 조명 옵션을 늘리는 Lite 시리즈의 참신한 카메라를 발표했습니다. VU-MORE Color 카메라는 적외선과 백색광의 트윈 업라이트를 탑재하고 있어 조도나 장면의 활동에 따라 자동으로 전개됩니다.

2022년 2월-Bosh Security Systems는 완전한 상황 정보를 제공하는 혁신적인 MICIP Fusion 9000i 9mm 카메라를 발표했습니다. 이번에 추가된 MICIP fusion 9000i 9mm 카메라는 기존 MICIP fusion 9000i의 라인업을 보완하는 것으로, 전력 및 유틸리티 시설, 데이터센터, 기타 보호 수준이 높은 시설의 부지 경계를 따라 등 경계 감지 용도에 완전한 상황 정보를 제공합니다. 메타데이터 퓨전이라는 혁신적인 방법을 사용하여 카메라는 열과 광학 스트리밍 비디오의 물체 식별 정보를 결합하여 하나의 이미지에 표시할 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 산업 밸류체인 분석

- 업계의 매력도-Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 시장 성장 촉진요인

- IP 카메라 가격 저하와 분석 및 소프트웨어 기술 진보

- 유효한 상업 모델로서 비디오 감시 서비스(VSaaS)의 출현

- 시장의 과제

- 개인정보 보호 및 보안 문제

- 고해상도 이미지를 위한 대용량 스토리지 필요성

- 미국에서 활동하는 중국 기업에 부과되는 규제

- 시장 기회

- COVID-19가 업계에 미치는 영향 평가

- 시가지 감시의 주된 케이스 스터디 및 도입 사례

- 주요 부문의 주요 기업이 채용하고 있는 베스트 프랙티스

제5장 시장 세분화

- 유형별

- 카메라

- 비디오 관리 시스템 및 스토리지

- 비디오 분석

- 최종 사용자별

- 상업

- 소매

- 국가 인프라 및 도시 감시

- 운송

- 주택

- 기타 최종 사용자

제6장 경쟁 구도

- 기업 프로파일

- Dahua Technology Co. Ltd

- Robert Bosch GmbH

- Hikvision Digital Technology Co. Ltd

- Hanwha Techwin

- Schneider Electric SE

- Honeywell Security Group

- Panasonic Corporation

- NEC Corporation

- Genetec Inc.

- Axis Communications AB(Canon)

- CP Plus International

- Avigilon Corporation

- Allied Telesis Inc.

- Infinova Corporation

- Palantir Technologies

- Cisco Systems Inc.

- Agent Video Intelligence Ltd

- Verint Systems Inc.

- FLIR Systems Inc.

- Qognify Inc.

제7장 투자 분석

제8장 시장 기회 및 향후 동향

AJY 25.04.07The US Video Surveillance Market size is estimated at USD 13.86 billion in 2025, and is expected to reach USD 24.75 billion by 2030, at a CAGR of 12.3% during the forecast period (2025-2030).

In the United States, surveillance cameras are most common among private-sector retail and commercial establishments, such as hotels, restaurants, and office complexes.

Key Highlights

- The country is also witnessing the rising adoption of smart home security cameras, which may further expand the scope of the market studied. AI-based video analytics further enhance efficiencies, offering many non-security-related insights for businesses, especially in smart city applications. Recently, Amazon announced the AWS Panorama technology that enables integrators to work with a developer to easily create customized deep learning and video analytic apps for video surveillance cameras, regardless of manufacturer.

- The use of video security cameras has expanded in recent years in the United States. Integrated video security cameras include technology that enables users to send information efficiently and quickly. This capability, however, may jeopardize the confidentiality of the scenario that has been hacked or captured. Malicious operations are performed via the smooth transmission of video footage and clips to unauthorized users.

- Over the past several years, video surveillance systems have become a part of the Internet of Things (IoT). An IoT sensor can often detect even more than humans, such as levels of pollutants in the air, noise level, and vibrations. For this reason, they are poised to be integrated into many camera-based surveillance solutions as they allow users to monitor threatened areas.

- However, like other IoT systems, inherent security risks can lead to significant violations of a user's privacy. Advanced machine learning techniques, primarily based on deep learning, are being researched and integrated within modern video surveillance systems for automating multiple tasks, including weapon detection, fire detection, in-store shopping, sensors of face recognition, and anomaly detection.

- Major industry verticals are trusting surveillance as a better platform for altering the behavior of employees to yield better results. Corporate companies' surveillance tactics had highly adverse effects on employees, resulting in the emergence of privacy issues, increased stress, and the loss of identity. However, like any intrusive technology, the benefits of deploying public video cameras must be balanced against the costs and dangers.

US Video Surveillance Market Trends

Video Analytics to Witness Significant Market Growth

- The United States is expected to provide the most to the development video analytics sector since many significant enterprises there require higher security surveillance systems. The industry is primarily fueled by the accessibility of technological knowledge, companies' increasing need for actionable information in real-time, and the country's expanding need for technically upgraded public protection infrastructure.

- Accessibility to innovative capabilities has been facilitated by the existence of numerous important technology businesses. The United States controls the major sector for video surveillance, propelling the industry forward. Further, the potential of terrorist strikes has forced authorities to install advanced monitoring equipment in a number of areas. Moreover, they have implemented video analytics systems to identify security threats in various industries.

- In the United States, surveillance cameras are increasingly replacing analog cameras. Such cameras have powerful facial and subject identification technology that continuously harvests surveillance material and produces a massive public database. Furthermore, the nation's democratic framework strongly favors implementing CCTV systems. For example, the Homeland Security Department pays local authorities billions of dollars in safety funding to deploy video security cameras. Federal assistance is expected to increase the demand for video analytics, propelling the development of video surveillance equipment over the forecast period.

- Major technology players' increasing regional developments are expected to contribute to market growth over the forecast period. Recently, Cisco Meraki collaborated with Kloudspot to assist businesses in providing safer and smarter workspaces for their workers and consumers.

Residential Addresses a Major Market Potential

- Residential video surveillance solutions connect one or more recording devices to a network and transfer the acquired video or audio data to a specific location. The photos are watched in real-time or sent to a central station for recording and retention. The growing need for security observation goods due to rising threats and criminal operations is driving the demand for video surveillance systems in the country.

- The emergence of smart homes increased the prominence of video surveillance systems in the residential segment in the past few years. The surveillance systems implemented in this sector have varied applications, such as monitoring and access control. These systems are also equipped with motion detection and night vision features.

- The high burglary rate in the country has increased the adoption of security systems such as video surveillance cameras over recent years, which has helped decrease the speed. For instance, according to the FBI, in October 2022, the national burglary rate in the United States was 271.1 incidences per 100,000 people in 2021. This represents a drop from the prior year when the burglary rate was 308 instances per 100,000 people

- Video analytics play a significant role in residential security video surveillance technology, reducing false alarm instances and enhancing the system's ability to detect suspicious situations. The industry expert consumer survey of 10,000 broadband households found that among the 26% of US broadband households that intend to buy a smart video doorbell, most rated artificial intelligence (AI) or advanced analytics capabilities as vital when selecting a specific video doorbell to purchase.

US Video Surveillance Industry Overview

The United States video surveillance market is highly competitive and consists of influential players. The market shows an augmented growth rate due to the effective pressure exerted by the market forces, both internally and externally. Some of the major players operating in the market include Dahua Technology Co. Ltd., Hikvision Digital Technology Co. Ltd, Hanwha Techwin, Schneider Electric SE, and Robert Bosch GmbH.

In September 2022, Dahua Technology U.S.A. Inc., a global leader in video-centric intelligent IoT solutions, introduced a novel camera in its Lite Series that provides consumers with more alternatives for nighttime lighting. The VU-MORE Color camera features twin infrared and white-light uplights that are automatically deployed depending on illumination and activity in the scene.

In February 2022, Bosch Security Systems Inc. introduced its innovative M.I.C. I.P. Fusion 9000i 9mm cameras, which provided complete situational information. The additional M.I.C. I.P. fusion 9000i 9mm camera complements the existing M.I.C. I.P. fusion 9000i line-up by providing complete contextual information to perimeter detecting applications, including along a site boundary at an electricity or utility facility, data center, or other high protective installations. Using an innovative method termed metadata fusion, the cameras can combine object identification information from heat and optical streaming video and show it in a single picture.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Market Drivers

- 4.4.1 Diminishing IP Camera Prices, Coupled with Technological Advancements in Analytics and Software

- 4.4.2 Emergence of Video Surveillance-as-a-Service (VSaaS) as a Viable Commercial Model

- 4.5 Market Challenges

- 4.5.1 Privacy and Security Issues

- 4.5.2 Need for High-capacity Storage for High-resolution Images

- 4.5.3 Restrictions Imposed on Chinese Companies Operating in the United States

- 4.6 Market Opportunities

- 4.7 Assessment of COVID-19 Impact on the Industry

- 4.8 Key Case Studies and Implementation Use-cases for City Surveillance

- 4.9 Best Practices Adopted by Key Players in Key Segments

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Cameras

- 5.1.2 Video Management Systems and Storage

- 5.1.3 Video Analytics

- 5.2 End User

- 5.2.1 Commercial

- 5.2.2 Retail

- 5.2.3 National Infrastructure and City Surveillance

- 5.2.4 Transportation

- 5.2.5 Residential

- 5.2.6 Other End Users

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Dahua Technology Co. Ltd

- 6.1.2 Robert Bosch GmbH

- 6.1.3 Hikvision Digital Technology Co. Ltd

- 6.1.4 Hanwha Techwin

- 6.1.5 Schneider Electric SE

- 6.1.6 Honeywell Security Group

- 6.1.7 Panasonic Corporation

- 6.1.8 NEC Corporation

- 6.1.9 Genetec Inc.

- 6.1.10 Axis Communications AB (Canon)

- 6.1.11 CP Plus International

- 6.1.12 Avigilon Corporation

- 6.1.13 Allied Telesis Inc.

- 6.1.14 Infinova Corporation

- 6.1.15 Palantir Technologies

- 6.1.16 Cisco Systems Inc.

- 6.1.17 Agent Video Intelligence Ltd

- 6.1.18 Verint Systems Inc.

- 6.1.19 FLIR Systems Inc.

- 6.1.20 Qognify Inc.