|

시장보고서

상품코드

1689953

인산 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Phosphoric Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

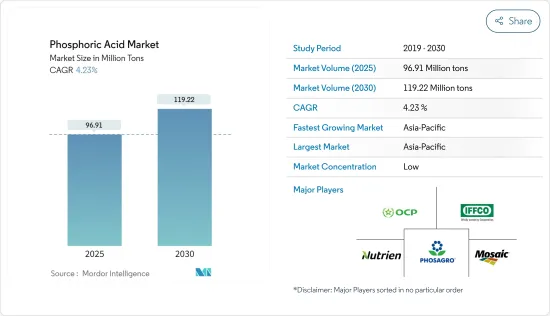

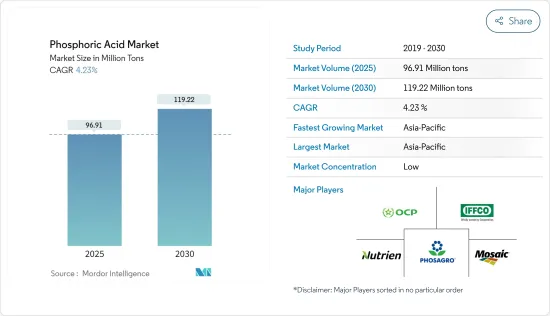

인산 시장 규모는 2025년에 9,691만 톤으로 추정되고, 2030년에는 1억 1,922만 톤에 이를 것으로 예측되며, 예측 기간 2025년부터 2030년까지 CAGR 4.23%로 성장할 전망입니다.

시장은 COVID-19의 대유행에 의해 주요 공급과 제조 라인이 중단되어 심각한 공급 부족에 빠졌기 때문에 부정적인 영향을 받았습니다. 인산의 주요 용도는 비료 생산입니다. 팬데믹은 또한 사람들 사이에 음식과 다른 필수품의 부족으로 작물 생산 감소로 이어졌습니다. 팬데믹 이후 시장은 속도를 높이고 주요 산업이 일을 재개했기 때문에 수요가 증가했습니다.

주요 하이라이트

- 인산의 대부분은 비료의 원료로 사용되기 때문에 비료 업계 수요 증가와 식품 및 식품 업계의 사용량 증가가 시장 수요를 견인할 것으로 예상됩니다.

- 인산염에 의한 건강 피해 및 비료 가격 상승이 시장 성장을 방해할 것으로 예상됩니다.

- 그럼에도 불구하고, 인산으로부터 희토류 원소의 회수 및 촉매로서 키랄 인산의 상업화는 시장에 유리한 기회를 제공할 것으로 기대되고 있습니다.

- 아시아태평양이 가장 높은 시장 점유율을 차지하고 있으며 예측 기간 동안 이 지역이 시장을 독점할 가능성이 높습니다.

인산 시장 동향

시장을 독점하는 비료 산업

- 인산은 기본적으로 비료를 생산하는 중간체입니다. 인산1암모늄(MAP), 인산2암모늄(DAP), 인산3나트륨(TSP) 등의 비료는 인산으로부터 생산됩니다.

- 인산은 식물 영양, pH 조정, 석회 침전에서 관개 설비 정화 등에 사용되는 다기능제이기 때문에 많은 비료의 주요 구성 요소가 되었습니다. 인산은 식물에 풍부한 인공급원입니다.

- 인 비료는 식물에 매우 중요하며 유기 비료보다 더 잘 작동합니다. 인은 식물의 성숙을 촉진하고 뿌리 개발에도 도움이 됩니다. 이것은 건조한 지역에서 특히 중요합니다.

- 에센셜 케미컬 인더스트리(Essential Chemical Industry)에 따르면, 전 세계적으로 연간 4,300만 톤 이상의 인산이 생산되며, 그 중 약 90%가 비료에 사용되고 있습니다.

- 미국 농무부 해외농업국에 따르면 중국, 러시아, 미국, 인도, 캐나다를 합치면 세계 비료영양소의 60% 이상을 생산하고 있습니다. 러시아와 미국은 각각 세계 비료의 10% 미만을 생산하고 중국은 약 25%를 생산하고 있습니다.

- 2022년 9월, 미국 정부는 국내 비료 생산을 촉진하는 5억 달러 상당의 프로그램을 발표했으며, 유럽 연합(EU)도 비슷한 조치를 취하도록 요구되고 있습니다. 이미 세계 최대의 칼리 비료 공급국인 캐나다는 2022년 11월, 타국으로부터의 출하가 멈추고 있는 틈새를 메우기 위해 비료 수출을 연간 20% 늘릴 것으로 발표했습니다.

- 국제비료협회(IFA)에 따르면 중국은 가장 큰 비료 사용자이며 세계 비료 공급량의 1/4 가까이를 소비하고 있습니다. 2022년 중국에서는 총 5,570만 톤의 NPK 비료가 생산되었습니다. 이는 2021년에는 5,544만 톤, 2020년에는 5,496만 톤이었습니다.

- 따라서 세계 각지역의 비료 성장 동향과 생산량을 고려하면 비료 산업이 시장을 독점할 가능성이 높아 예측기간 동안 인산 수요가 높아질 것으로 예상됩니다.

시장을 독점하는 아시아태평양

- 아시아태평양은 2022년 상당한 수량 점유율로 인산 시장을 독점하고 예측 기간 동안에도 우위를 유지할 것으로 예상됩니다.

- 이는 중국이 세계 최대의 비료 생산 및 소비국이기 때문입니다. 중국, 인도, 동남아시아 국가 등에서는 인산 수요가 지속적으로 증가하고 있습니다.

- 중국은 전체 농업 면적의 약 7%를 세계적으로 차지하고 그래서 세계 인구의 22%에게 제공합니다. 국가는 밥, 면, 감자 및 기타를 포함하여 각종 곡물의 가장 큰 생산자, 입니다. 따라서 비료에 사용되는 인산 수요는 일본의 대규모 농업 활동 덕분에 빠르게 증가하고 있습니다.

- 인산은 또한 인산철 리튬 전지의 생산에도 널리 사용되고 있으며, 이 분야에서는 중국이 지배적인 나라가 되고 있습니다. 2022년에는 중국에서 판매된 전기자동차 전체의 44%가 LFP 전지를 사용하고 있으며, 그 다음 유럽의 6%, 미국과 캐나다의 3%가 되었습니다.

- 또 다른 대비료 생산국인 인도는 2위 사용자입니다. 인도 사용량의 대부분은 인도 정부의 비료에 대한 엄청난 보조금으로 충당됩니다. 2022 회계연도에는 4,200만 톤이 넘는 비료가 인도에서 생산되었습니다. 인도의 비료 생산량은 2020 회계 연도에 피크를 맞아 4,600만 톤을 넘어섰습니다. 최근 몇 년동안 공공, 협동 조합, 민간 부문에 대한 투자를 촉진하는 유리한 정책이 취해졌습니다.

- 인산은 또한 다양한 콜라와 잼과 같은 식품 및 음료를 산성화하고 마른 맛과 신맛을 제공하기 위해 음식 식품 산업에서 사용됩니다. 미국 농무부(USDA)에 따르면 인도의 식품 산업은 세계 3위의 식품산업에 랭크되고 있습니다. 이 산업은 지난 몇 년간 꾸준한 성장을 이루고 있으며 인도는 세계 최대의 식품 생산국이 될 것으로 예상되고 있습니다. 이 나라의 식품 및 식료품류(F&G) 소매 시장 매출은 2025년까지 8,500억 달러 이상에 달할 것으로 예측됩니다.

- 따라서 위의 이유는 예측기간에 걸쳐 아시아태평양 인산 시장의 성장을 가속할 가능성이 높습니다.

인산 산업 개요

인산 시장은 부분적으로 통합되어 있으며, 세계 수준에서도 지역 수준에서도 여러 회사가 활동하고 있습니다. 시장의 주요 기업(순부동)에는 OCP Group, Mosaic, PhosAgro Group of Companies, Nutrien Ltd, IFFCO 등이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 성장 촉진요인

- 비료 산업에 대한 높은 수요

- 식음료 업계에서 사용량 증가

- 시장 성장 억제요인

- 인산에 의한 건강 피해

- 밸류체인 분석

- 업계의 매력도-Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 인산의 가격 동향 분석(2018-2023년)

- 기술 스냅샷

제5장 시장 세분화

- 최종 사용자 산업별

- 비료

- 음식

- 화학제품

- 의약품

- 야금

- 기타 최종 사용자 산업

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 멕시코

- 캐나다

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴 및 협정

- 시장 랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- Aditya Birla Chemicals

- Agropolychim

- EuroChem Group

- ICL

- IFFCO

- Innophos

- JR Simplot Company

- Mosaic

- Nutrien Ltd

- Phosagro

- Sterlite Copper(A Unit of Vedanta Limited)

제7장 시장 기회 및 향후 동향

- 인산으로부터 희토류 원소 회수

- 촉매로서 키랄인산의 상업화

The Phosphoric Acid Market size is estimated at 96.91 million tons in 2025, and is expected to reach 119.22 million tons by 2030, at a CAGR of 4.23% during the forecast period (2025-2030).

The market was negatively impacted by the COVID-19 pandemic as it disrupted the main supply and manufacturing lines, leading to acute shortages. The main use of phosphoric acid is for producing fertilizers. The pandemic also led to a decrease in crop production, accompanied by a shortage of food and other essentials among people. After the pandemic, the market picked up speed, and the demand grew as major industries got back to work.

Key Highlights

- Since most phosphoric acid is used to make fertilizer, the rising demand from the fertilizer industry and increasing usage in the food and beverage industry are expected to drive market demand.

- Health hazards caused by phosphoric acid and the high price of fertilizers are expected to hinder the market's growth.

- Nevertheless, the recovery of rare earth elements from phosphoric acid and the commercialization of chiral phosphoric acid as a catalyst are expected to offer lucrative opportunities to the market.

- Asia-Pacific accounted for the highest market share, and the region is likely to dominate the market during the forecast period.

Phosphoric Acid Market Trends

Fertilizer Industry to Dominate the Market

- Phosphoric acid is basically an intermediate used to produce fertilizers. Fertilizers like monoammonium phosphate (MAP), diammonium phosphate (DAP), and trisodium phosphate (TSP) are produced from phosphoric acid.

- Phosphoric acid forms a key component for many fertilizers as it is a multi-function agent used for plant nutrition, pH adjustment, and cleansing irrigation equipment from lime precipitation. It is a rich source of phosphorus for plants.

- Phosphorus fertilizers are extremely important for the plant and provide better activities than organic fertilizers. Phosphorus accelerates the maturation of the plant and also provides the development of the roots. This is particularly important for dry areas.

- According to the Essential Chemical Industry, annually, more than 43 million metric tons of phosphoric acid are produced worldwide, of which about 90% are used to make fertilizers.

- According to the USDA Foreign Agricultural Service, China, Russia, the United States, India, and Canada produce more than 60% of the world's fertilizer nutrients combined. Russia and the United States each produce less than 10% of global fertilizers, while China produces approximately 25%.

- In September 2022, the US government announced programs worth USD 500 million to boost domestic fertilizer production, and the European Union is being urged to take similar action. Canada, already the world's largest supplier of potash fertilizers, announced in November 2022 that it will boost its fertilizer exports by 20% annually, filling a gap left by blocked shipments from other countries.

- According to the International Fertilizer Association (IFA), China is the largest user of fertilizer, consuming nearly one-quarter of global fertilizer supplies. In 2022, a total of 55.7 million tons of NPK fertilizer was produced in China. This was 55.44 million tons in 2021 and 54.96 million tons in 2020.

- Therefore, considering the growth trends and production of fertilizers in different regions worldwide, the fertilizer industry is likely to dominate the market, which, in turn, is expected to enhance the demand for phosphoric acid during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region dominated the phosphoric acid market in 2022 with a considerable volume share, and it is expected to maintain its dominance during the forecast period.

- This is due to China being the world's largest producer and consumer of fertilizer. In countries like China, India, and Southeast Asian nations, the demand for phosphoric acid has been increasing continuously.

- China accounts for approximately 7% of the overall agricultural acreage globally, thus feeding 22% of the world's population. The country is the largest producer of various crops, including rice, cotton, potatoes, and others. Hence, the demand for phosphoric acid, which is used in fertilizers, is rapidly increasing owing to the large-scale agricultural activities in the country.

- Phosphoric acid is also used extensively in the production of lithium-iron-phosphate batteries, and China is the dominant country in this field. In 2022, 44% of the total electric vehicles sold in China used LFP batteries, followed by 6% in Europe and 3% in the United States and Canada.

- India, another large fertilizer producer, is the second largest user. Much of India's usage is fueled by the Indian government's heavy subsidization of fertilizers. In the financial year 2022, over 42 million metric tons of fertilizers were produced in India. Fertilizer production in India peaked in the financial year 2020 at over 46 million metric tons. During the last few years, there has been a favorable policy facilitating investments in the public, cooperative, and private sectors.

- Phosphoric acid is also used in the food and beverage industries to acidify foods and beverages, such as various colas and jams, providing a tangy or sour taste. According to the US Department of Agriculture (USDA), the Indian food industry ranks as the third-largest food industry globally. The industry has been experiencing steady growth over the past several years, with India anticipated to become the largest food producer in the world. The country's food and grocery (F&G) retail market is projected to surpass USD 850 billion in sales by 2025.

- Hence, the reasons mentioned above are likely to fuel the growth of the phosphoric acid market in Asia-Pacific over the forecast period.

Phosphoric Acid Industry Overview

The phosphoric acid market is partially consolidated, with several companies operating on both global and regional levels. Some of the major players in the market (not in any particular order) include OCP Group, Mosaic, PhosAgro Group of Companies, Nutrien Ltd, and IFFCO, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions

- 1.2 Scope of Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Drivers

- 4.1.1 High Demand for Fertilizer Industry

- 4.1.2 Increasing Usage in the Food and Beverage Industry

- 4.2 Market Restraints

- 4.2.1 Health Hazards Caused by Phosphoric Acid

- 4.3 Industry Value Chain Analysis

- 4.4 Industry Attractiveness - Porters Five Forces Analysis

- 4.4.1 Bargaining Power of Supplier

- 4.4.2 Bargaining Power of Buyer

- 4.4.3 Threat of New Entrant

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Price Trend Analysis of Phosphoric Acid (2018-2023)

- 4.6 Technological Snapshot

5 Market Segmentation (Market Size in Volume)

- 5.1 By End-user Industry

- 5.1.1 Fertilizer

- 5.1.2 Food and Beverages

- 5.1.3 Chemicals

- 5.1.4 Medicine

- 5.1.5 Metallurgy

- 5.1.6 Other End-user Industries

- 5.2 By Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Mexico

- 5.2.2.3 Canada

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle East and Africa

- 5.2.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Merger and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aditya Birla Chemicals

- 6.4.2 Agropolychim

- 6.4.3 EuroChem Group

- 6.4.4 ICL

- 6.4.5 IFFCO

- 6.4.6 Innophos

- 6.4.7 J.R. Simplot Company

- 6.4.8 Mosaic

- 6.4.9 Nutrien Ltd

- 6.4.10 Phosagro

- 6.4.11 Sterlite Copper (A Unit of Vedanta Limited)

7 Market Opportunities and Future Trends

- 7.1 Recovery of Rare Earth Elements from Phosphoric Acid

- 7.2 Commercialization of Chiral Phosporic Acid as a Catalyst