|

시장보고서

상품코드

1690067

자동차 내부 백미러 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)Automotive Inside Rearview Mirrors (IRVM) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

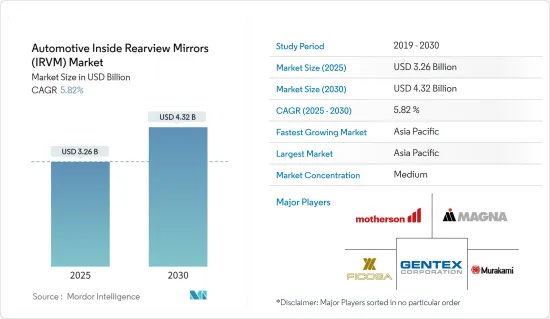

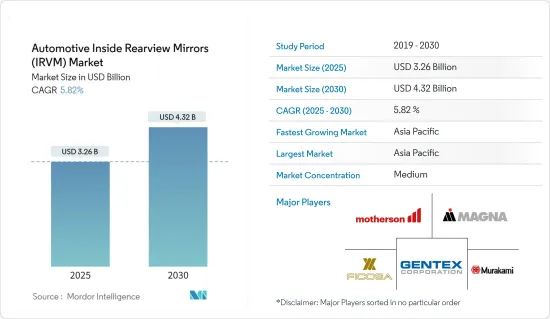

자동차 내부 백미러 시장 규모는 2025년 32억 6,000만 달러에 이르고 예측기간 중(2025-2030년) CAGR은 5.82%를 나타내 2030년에는 43억 2,000만 달러에 달할 것으로 예상됩니다.

자동차 내부 백미러는 유통의 영향을 받아 OEM과 자동차 부품 공급업체의 대부분이 정부의 봉쇄 조치로 생산 거점을 폐쇄하지 않을 수 없게 되었습니다.

게다가 중기적으로는 승무원의 쾌적성과 안전성에 대한 의식의 높아짐과 안전기능을 의무화하는 정부규제를 배경으로 ADAS 기능을 통합한 자동차의 생산대수가 증가하여 시장 수요를 촉진할 것으로 예상됩니다. National Highway Traffic Safety에 따르면, 연간 1만 5,000명이 등을 넘는 사고로 부상을 입었으며, 유아와 노인이 가장 희생되고 있습니다. 또한 미국 도로교통안전국 보고서에 따르면 미국에서는 매년 약 84만 건의 사각지대 사고가 발생한다고 합니다.

카메라와 센서는 다양한 목적을 달성하기 위해 신차에 빠뜨릴 수 없는 부품입니다. 라 시스템은 일반적으로 도로를 달리는 자동차의 안전성을 향상시키는 유용한 도구로 간주되어 왔습니다.

아시아태평양은 인도, 일본, 중국에서 자동차 생산량이 증가함에 따라 세계의 자동차 내부 백미러 시장을 독점 할 가능성이 높습니다. 또한 유럽은 Porsche, AUDI, Volkswagen, BMW 같은 지역의 유명한 진출기업의 존재로 인해 두 번째로 큰 시장을 등록할 가능성이 있습니다.

자동차 내부 백미러 시장 동향

승용차 부문이 시장에서 큰 점유율을 차지할 전망

예측 기간 동안 승용차 부문은 자동차 생산량이 증가하고 세계 주요 지역에서 자동차 판매량이 증가함에 따라 폭넓은 소비자를 매료시키는 혁신적인 제품 투입에 주력하는 주요 OE M이 증가함에 따라 더 빠른 속도로 성장합니다., 자동차 판매를 포함한 세계 경제 활동에 영향을 주고 바이러스의 만연을 억제하기 위해 여러 나라에서 엄격한 봉쇄가 실시되었습니다.

승용차 수요 증가와 전동 이동성에 대한 의식이 높아짐에 따라 주요 기업은 현재 보유 차량의 전동화에 기대하고 있습니다.

- 2022년 3월, Ford Motors는 2024년 말까지 유럽에서 전 전기 승용차를 3차종 투입한다고 발표하고, 2026년까지 유럽에서 연간 60만대 이상의 전기자동차를 판매하는 목표를 설정했습니다.

- 2022년 1월, 제너럴 모터스는 전기자동차 생산 능력을 강화하기 위해 미시간의 2개 공장에 40억 달러 이상을 투자하고자 한다고 발표했습니다.

승용차 부문의 판매량이 증가함에 따라 내부 백미러 수요는 유망한 성장을 이루고 있습니다.

- 2022년 8월, Audi India는 몇개의 신기술을 채용한 신형 Q3를 발표했습니다.

- 2022년 8월, Tata Punch의 인상적인 매출을 확인한 후, Tata Group은 내년, 추가 기능을 포함하는 블랙 버드라고 명명된 크레타 부문의 미드 사이즈 SUV를 발매한다고 발표했습니다.

자동차 내부 백미러 시장은 승용차 부문에서 등장하는 새로운 카메라 기술과의 까다로운 경쟁에 직면 해 있습니다. 주요 자동차 제조업체와 내부 백미러 제조업체는 드라이버의 시야를 확보하기 위해 기존의 미러에 카메라를 통합하고 있습니다. 특정 상황에서는 미러를 통한 차량의 후방 시야가 차단되어 운전자의 시야를 방해합니다.

따라서 내부 백미러 시스템에 카메라를 통합하는 것이 자동차 산업에서는 지금까지 최상의 솔루션이되었습니다. 이러한 개발과 승용차 판매량 증가 요인을 고려하면 내부 백미러 수요는 예측기간 동안 높은 성장률을 나타낼 것으로 예상됩니다.

예측기간 동안 아시아태평양은 크게 성장할 것으로 예상

아시아태평양은 저비용 원료의 가용성, 저렴한 노동력, 현지 생산을 위한 정부 노력 증가로 시장에서 가장 큰 점유율을 차지하고 있습니다. 이 지역에서는 중국이 전기차의 최대 생산국과 소비국 중 하나이며 인도, 일본, 한국 등의 국가에서 승용차 판매 수요가 증가하고 있는 것도 자동차 산업의 내부 백미러 수요를 밀어 올리는 요인이 되고 있습니다.

세계에서 가장 큰 전기자동차 시장인 중국은 정부의 까다로운 지원에 의해 지원되고 있습니다. 중국은 신에너지자동차(NEV) 구매에 대한 우대조치를 2022년까지 연장했습니다. 아시아태평양은 전기자동차의 도입을 적극적으로 지원합니다.

- 2020년 1월, Tesla Motors는 상하이에 20억 달러의 시설을 완성했고, 2020년 3월에는 전기자동차 대기업의 다른 모든 세계 시설이 COVID-19 팬데믹을 위해 폐쇄되었을 때 주 3,000대 근처의 자동차를 조립했습니다.

- 2021년 말, 현대는 3월 세계에서 31만 3,926대를 판매했습니다. 판매 통계는 전년 대비 17% 감소했습니다. 판매량은 2021년 1분기보다 더 적었습니다. 게다가 현대자동차의 자동차 부문은 전기자동차 판매량이 거의 두 배로 급성장했습니다. 그 결과 BEV의 판매 대수는 105% 증가한 1만 1,447대가 되었습니다. 또한 플러그인 전기자동차는 1만 4,693대가 되어 전년대비 58% 증가했습니다.

시장과 미개척 시장의 정부·행정은 그 부의 대부분을 교통과 그 안전성의 향상에 지출하고 있습니다. 그 결과, 자동차의 판매 대수가 늘어남에 따라, 자동차의 안전성의 요구에 맞는 추가 기능이 요구되고 있습니다. 내부 백미러는 자동차 판매에 크게 의존하기 때문에 아시아태평양은 내부 백미러 채용의 중심지가 되어 세계 자동차 판매를 선도하고 있습니다. 이러한 점을 고려하면 내부 백미러 수요는 예측 기간 동안 높은 성장률을 보일 것으로 예상됩니다.

자동차 내부 백미러 산업 개요

자동차 시장은 Gentex Corporation, Magna International Inc., Samvardhana Motherson Reflectec과 같은 많은 지역 및 세계 진출 기업이 존재하기 때문에 적당히 세분화되었습니다.

각 회사는 기존의 거울을 교체하지 않고 자동차 소유자에게 편리하고 안전한 경험을 제공하기 위해 R&D 프로젝트에 대한 투자를 늘리고 있습니다. 기술적 이점을 높이고 내부 백미러 기능을 개선함으로써 시장은 큰 성장을 이루고 있습니다.

- 2022년 8월, Mahindra와 Mahindra는 상승 중 사용자의 안전과 편안함을 개선하기 위해 자동 조광 내부 백미러을 탑재한 신형 Scorpio N 가솔린 차량을 발표했습니다.

- 2022년 7월 SemiDrive는 Chery의 OMODA 5 SUV가 세미 드라이브 X9 시리즈 자동차 System-on-Chip(SoC)를 채용했다고 발표했습니다. X9 시리즈는 기기 패널, 콘솔 컨트롤, 내부 백미러, 후행 탑승자의 엔터테인먼트 등 최대 10개의 HD 스크린을 1칩으로 출력할 수 있습니다. 멀티스크린 공유 및 상호작용을 지원합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 성장 촉진요인

- 시장 성장 억제요인

- 산업의 매력 - Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 차종별

- 승용차

- 상용차

- 파워트레인 유형별

- ICE

- 전기

- 기능 유형별

- 자동 조광

- 프리즘

- 사각지대 표시

- 유통 채널별

- OEM

- 애프터마켓

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 유럽

- 독일

- 영국

- 프랑스

- 기타 유럽

- 아시아태평양

- 인도

- 중국

- 일본

- 한국

- 기타 아시아태평양

- 기타

- 브라질

- 아랍에미리트(UAE)

- 기타 국가

- 북미

제6장 경쟁 구도

- 벤더의 시장 점유율

- 기업 프로파일

- Gentex Corporation

- Samvardhana Motherson Reflectec

- Magna International, Inc.

- Ficosa International SA

- Continental AG

- Murakami Corporation

- Tokai Rika Co., Ltd.

- Mitsuba Corporation

- SL Corporation

- Flabeg Automotive Holding GmbH

제7장 시장 기회와 앞으로의 동향

KTH 25.05.09The Automotive Inside Rearview Mirrors Market size is estimated at USD 3.26 billion in 2025, and is expected to reach USD 4.32 billion by 2030, at a CAGR of 5.82% during the forecast period (2025-2030).

The Automotive inside rearview mirrors was negatively affected by the pandemic, as majority of OEM and auto component suppliers had to close down their production sites with ongoing government lockdown measures. This held the market with low demand from OEMs for IRVM and reduces production volumes from manufacturers. After 2021, market started witnessing a steady demand for the IRVM with rising auto sales across the globe coupled with an improved supply chain network worldwide.

Moreover, over the medium term, growing production of vehicles with integrated ADAS features in wake of rising awareness toward comfort and safety of passengers and government regulations mandating safety features expected to drive demand in the market. For instance, According to Insurance Institute for Highway Safety says 15,000 people are injured annually in back over accidents, with children and elders having been the most victims. Additionally, the National Highway Traffic Safety Administration report says that nearly 840,000 blind-spot accidents occur every year in the United States. This makes its prime utilization for vehicle IRVM to maintain driver comfort and safety.

Cameras and sensors are a vital part of any new vehicle, as they serve many different purposes. They help OEMs to manufacture cars that are safer, more comfortable to drive, and more fuel-efficient. Rear-view cameras and other camera systems for vehicles have generally been seen as useful tools for improving the safety of vehicles on the road. But in some cases, the complex camera and monitor systems that are supposed to increase the driver's visibility become confusing and distracting.

Asia-Pacific region is likely to dominate global automotive rear view mirror market owing to rising production of vehicle in the India, Japan and China. In addition, this is Europe are likely to register second largest market due to the presence of prominent players in the region for instance, Porsche, AUDI, Volkswagen, and BMW. The technological development in these regions is expected to create significant opportunities in automotive mirror market over the forecast period.

Automotive Rear View Mirror Market Trends

Passenger Car Segment Likely to Hold Significant Share in the Market

The Passenger car segment of the market during the forecast period to grow at faster pace owing to rising vehicle production and growing focus of jey OEMs on launching innovative products to attract wide range of consumers in wake of rising vehicle sales across major regions in the world. For instance, In 2021, the global car sales were around 66.7 Million, which in 2020 were 63.8 Million. The global pandemic impacted economic activities all around the world including car sales the globe, and strict lockdowns were enforced in several countries to contain the spread of the virus. Owing to this the number of cars sold in 2020 was 14.8% lower than compared in 2019. But with life returning to normalcy, the number of cars sold globally has increased which will aid the automotive IRVM market to grow in the forecast period.

Owing to the increase in the demand for passenger cars and the growing awareness of electric mobility, major players are looking forward to electrifying their present fleet. For instance,

- In March 2022, Ford Motors announced to include three all-electric passenger vehicles in Europe by the end of 2024 and set a target to sell more than 600,000 electric vehicles annually by 2026 in the Europe region.

- In January 2022, General Motors announced considering investing more than USD 4 billion in two Michigan factories to increase its electric car manufacturing capacity. GM and LG Energy Solution have proposed constructing a USD 2.5 billion battery facility in Lansing.

With rising sales of the passenger car segment, demand for IRVM is witnessing promising growth. Nowadays, all the id-segment and luxury passenger cars are equipped with advanced IRVM which has posed technological dominance over the market. For instance,

- In August 2022, Audi India has introduced its new Q3 which has adopted several new technologies to look at. Audi has added frameless auto dimming IRVM and parking aid plus with rear view camera, which shall improve the driver safety and comfort apart from other added features in complete Q3.

- In August 2022, after witnessing impressive sales on Tata Punch, Tata Group is announced that ist going to launch a Creta segment mid-size SUV named Blackbird next year which shall encompass added features. The car shall be equipped with advance digital instrument console, auto-dimming IRVM, automatic climate control, electrically operated ORVMs and may more other features.

The automotive inside rear-view mirror market is facing tough competition from new camera technologies with are coming in the passenger car segment. Leading automotive OEMs and interior rear-view manufacturers are integrating cameras with conventional mirrors to provide a better view of the drivers. In certain situations, the rear view of the vehicle through a mirror is blocked and causes hindrance to the driver's view.

Thus, camera integration with the rear-view mirror system has been the best solution so far in the automotive industry. Considering these developments and factors with rising passenger car sales, demand for IRVM is expected to witness a high growth rate in the forecast period.

Asia-Pacific Region Anticipated to Grow at Significant Level During the Forecast Period

The Asia-Pacific region accounts for the largest share in the market owing to the availability of low-cost raw materials, cheap labour, and increasing government initiatives toward local manufacturing. In the region, China is one of the largest producers and consumers of electric vehicles as well as increasing demand for passenger car sales in the countries like India, Japan, South Korea, etc., are likely to boost the demand for inside rear-view mirrors in the automotive industry.

China, which is the largest electric vehicle market in the world, has been backed up by generous support from the government. China has extended the incentives related to the purchase of new energy vehicles (NEVs) till 2022. Asia-Pacific region is aggressively supporting the electrical vehicle adoption. For instance,

- In January 2020, Tesla Motors inaugurated a USD 2 billion facility in Shanghai that was assembling nearly 3000 cars per week in March 2020, when all the other global facilities of the electric vehicle giant were shut down due to the COVID-19 pandemic.

- During the end of FY21, Hyundai sold 313, 926 cars globally in March. The sales statistics stood at a drop of 17% compared to previous years. The sales were even less than Q1 2021. Moreover, Hyundai observed that its automotive segment witnessed a sharp rise with almost doubled sales figures for its all-electric cars. This in turn makes the sales figure for its BEV to stood at 11,447 units with a rise of 105%. In addition, the plug-in electric cars increased to 14,693 units to 58% year and year growth.

Governments and administrations in developing and untapped markets are spending a major portion of their wealth on improving transportation and its safety. This will result in the sales growth of vehicles and also calls for additional features to suit the needs of vehicle safety. With IRVM being highly dependent of sales of the vehicles, Asia-pacific has been leading the vehicles sales across the globe making its epicentre for IRVM adoption. Considering these aspects demand for IRVM is expected to witness high growth rate during the forecast period.

Automotive Rear View Mirror Industry Overview

The automotive market is moderately fragmented due to the presence of many local and global players such as Gentex Corporation, Magna International Inc., and Samvardhana Motherson Reflectec amongst others. The market is transforming but the new technologies are right now available mostly in luxury vehicles and in a selected market and near future, it will not replace the conventional mirrors. As the laws are still with conventional mirrors.

Although companies are increasing investment in R&D projects to provide more convenient and safer experience to the car owner without replacing the conventional mirrors. With rising technological dominance and improved IRVM features market has witnessed immense growth. For instance,

- In August 2022, the Mahindra and Mahindra introduced the new Scorpio N petrol variant with the auto dimming IRVM in order to improve user safety and comfort during the rises.

- In July 2022, SemiDrive announced that Chery's OMODA 5 SUV has adopted SemiDrive's X9 series automotive SoC (system-on-a-chip). The X9 series can provide outputs of up to 10 HD screens, such as instrument panels, console control, rearview mirrors, and entertainment for back row passengers, through a single chip. It supports multi-screen sharing and interaction.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value in USD Million)

- 5.1 By Vehicle Type

- 5.1.1 Passenger Car

- 5.1.2 Commercial Vehicle

- 5.2 By Powertrain Type

- 5.2.1 ICE

- 5.2.2 Electric

- 5.3 By Feature Type

- 5.3.1 Auto-Dimming

- 5.3.2 Prismatic

- 5.3.3 Blind spot indicator

- 5.4 By Sales Channel Type

- 5.4.1 OEM

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Rest of the World

- 5.5.4.1 Brazil

- 5.5.4.2 United Arab Emirates

- 5.5.4.3 Other Countries

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Gentex Corporation

- 6.2.2 Samvardhana Motherson Reflectec

- 6.2.3 Magna International, Inc.

- 6.2.4 Ficosa International SA

- 6.2.5 Continental AG

- 6.2.6 Murakami Corporation

- 6.2.7 Tokai Rika Co., Ltd.

- 6.2.8 Mitsuba Corporation

- 6.2.9 SL Corporation

- 6.2.10 Flabeg Automotive Holding GmbH