|

시장보고서

상품코드

1690112

금속 인쇄 포장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Global Metal Print Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

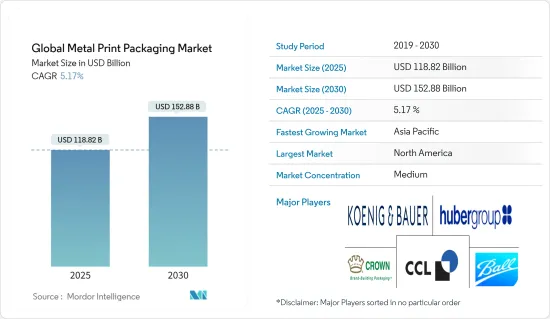

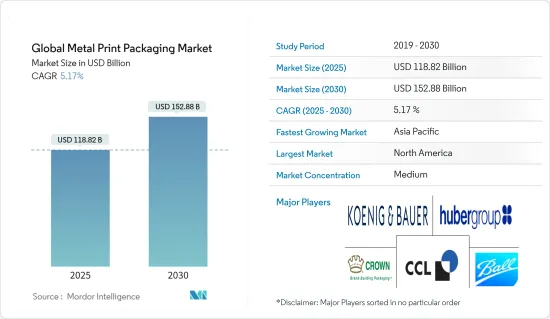

금속 인쇄 포장 세계 시장 규모는 2025년에 1,188억 2,000만 달러, 2030년에는 1,528억 8,000만 달러에 달할 것으로 예측됩니다. 예측 기간(2025년-2030년) CAGR은 5.17%를 나타낼 전망입니다.

주요 하이라이트

- 세계의 금속 인쇄 포장 시장은 커스터마이즈나 프리미엄화, 금속 포장의 채용 확대, 리사이클이나 재이용 가능한 소재에 대한 관심 증가 등의 요인에 의해 상승 기조에 있습니다. 또한, 인쇄 기술의 진보는 시장 벤더에게 기회 확대를 가져오고 있습니다.

- 시각적으로 매력적이고 개인화된 통조림 식품과 식음료에 대한 수요 증가는 예측 기간 중의 금속 인쇄 포장 시장의 성장을 한층 더 촉진할 전망입니다.

- 금속 포장 고유의 장식의 편리성은 특정 시장과 기회에 대응한 다양한 효과와 마무리를 가능하게 합니다.

- 선도적인 음료 제조업체는 선반의 시인성을 높이고 소비자를 매료시키기 위해 맞춤형 포장에 기울이고 있으며, 금속 인쇄 포장의 중요성이 부각되고 있습니다. Ball Corp.에 의하면, 플라스틱 포장에 대한 브랜드의 불안의 고조와 대체품의 추구에 의해 알루미늄캔 수요는 증가할 것으로 예상되고 있습니다.

- 시장은 엄청난 도전에 직면하고 있습니다. 금속 공급자의 가격 상승은 잉크 제조업체에 가격 전략의 조정을 강요하고 있습니다.

금속 인쇄 포장 시장 동향

오프셋 리소그래피는 상당한 성장이 예상된다.

- 오프셋 리소그래피는 포장 인쇄에서 지배적인 기법으로 자리매김하고 있습니다. 보다, 선진 지역, 특히 유럽과 북미에서 특히 지지되고 있습니다. 이 지역에서는 금속캔 인쇄에는 오프셋 리소그래피가 주로 채용되고 있지만, 이것은 소재의 경도와 비흡수성의 성질이 크게 영향을 주고 있습니다.

- 시장을 선도하는 크라운 홀딩스사 등은 2피스와 3피스 금속 패키지 모두에 오프셋 인쇄를 채용하고 있습니다. 이 공정에서는 인쇄판에서 담요로 잉크를 전사한 다음 금속 표면에 도포합니다. 특히 2 조각 캔은 성형 후 인쇄되지만 3 조각 캔은 미리 시트에 인쇄됩니다. 크라운 푸드 유럽은 스낵 과자 산업의 다양한 고객을 지원하며, Bier Nuts사의 바삭바삭하게 코팅된 땅콩용 100% 재활용 가능한 금속 용기를 제조하거나, Satisfied Snacks사의 Salad Crisp 컨셉의 금속 통 인쇄 패키지를 납품하고 있습니다.

- 오프셋 인쇄는 고품질 출력으로 유명하지만, 그라비아 인쇄 및 포토 그라비아 인쇄와 같은 최첨단 방법과의 까다로운 경쟁에 직면하고 있습니다. 또한, 알루마이트 인쇄판은 산화에 의한 녹의 영향을 받기 쉽고, 철저한 유지 보수가 필요합니다. 이러한 문제는 이 부문의 확장을 방해할 수 있습니다.

- 주석과 알루미늄 시트에 대한 고품질 보호 래커 및 생생한 리소그래피를 전문으로하는 금속 인쇄와 같은 기업은 금속 포장의 광범위한 수요를 수용합니다. 금속 인쇄 제품은 음식 캔에서 화학 용기, 장식 캔까지 다양합니다. 주목할만한 동향은 유기농 식품 산업이 경량 금속 캔을 선호하는 것이며 우수한 장벽 특성과 환경 친화적인 것으로 평가되었습니다.

- 유기 무역 협회 보고서에 따르면 미국의 유기 패키지 식품 시장은 상당한 성장을 이루었습니다. 2019년 소비는 184억 4,180만 달러로, 2025년에는 250억 6,040만 달러로 증가할 것으로 예상됩니다. 이러한 유기농 포장 식품 수요 증가는 식품 포장 업계에서 오프셋 인쇄에 대한 의존도를 높이는 것입니다.

아시아태평양이 큰 성장세 전망

- 아시아태평양은 세계의 금속 인쇄 포장 시장에서 큰 점유율을 차지하고 있는데, 이는 주로 제조업체가 비용 효율적인 포장 및 솔루션을 중시하고 있기 때문입니다. 선진국의 성숙한 시장에서는 디지털 인쇄 패키징 시장이 정체되고 있지만, 중국과 인도에서는 향후 7-8년 사이에 활발한 확대가 전망됩니다.

- 아시아태평양의 금속 인쇄 포장 시장을 견인하는 주요 요인으로는 포장 식품(냉동품과 냉장품 포함)의 매출 증가, 가처분 소득 증가, 라이프 스타일의 변화, 안정된 경제 성장, 알코올 음료와 비알코올 음료 모두 소비 증가 등이 있습니다.

- 맥주 패키지는 맛을 유지하는 뛰어난 능력에서 주로 금속 캔이 선호됩니다.

- 디지털 인쇄 기술에 의해 인쇄 프로세스가 자동화되어 3D 인쇄는 다음의 프론티어로서 대두되고 있습니다.

- 아시아태평양 국가는 최근에 효율적인 금속 가공 기술에 대한 노력을 강화하고 있으며, 금속 가공 산업에서의 CO2 배출량을 삭감하고 있습니다. 타로부터 조형물을 제작할 수 있는 금속 3D 프린터 수요 증가가 전망되고 있습니다.이 프린터는 종래의 제조 공정을 대폭 신속화할 뿐만 아니라, 폐기물을 최소한으로 억제해, 설계의 유연성을 높여, 복수의 부품의 통합이나 전체적인 중량의 경감을 가능하게 합니다.

금속 인쇄 포장 산업 개요

세계의 금속 인쇄 포장 시장은 소규모에서 대규모까지 존재하는 분열된 양상을 보이고 있습니다. 주요 기업으로는 Toyo Seihan Co.Ltd, Ball Corporation, Hubergroup Deutschland GmbH, Envases Group, CCL Container (CCL Industries Inc.의 한 사업부), 그리고 Koenig & Bauer AG가 있습니다. 이러한 기업은 전략적 파트너십, 혁신적인 솔루션에 대한 투자, 신제품 출시를 통해 시장에서의 존재감을 높이고 있으며, 이들은 모두 예측 기간 동안 경쟁력을 획득하는 것을 목적으로 하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 업계의 매력도 - Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 역학

- 시장 성장 촉진요인

- 디지털 인쇄 기술의 급속한 진화

- 시장의 과제

- 인쇄 잉크의 가격 변동

- 대체 패키지 솔루션의 존재

제6장 시장 세분화

- 인쇄 프로세스별

- 오프셋 리소그래피

- 그라비아

- 플렉소 인쇄

- 디지털

- 기타 인쇄 기술

- 지역별

- 북미

- 유럽

- 아시아

- 호주 및 뉴질랜드

- 라틴아메리카

- 중동 및 아프리카

제7장 경쟁 구도

- 기업 프로파일

- Hubergroup Deutschland GmbH

- Crown Holdings Inc.

- CCL Container(CCL Industries Inc.)

- Ball Corporation

- Koenig & Bauer AG

- Toyo Seikan Group Holdings, Ltd

- Envases Group

- Real Pad Printer

- Ardagh Metal Packaging(AMP)

제8장 투자 분석

제9장 시장의 미래

SHW 25.05.09The Global Metal Print Packaging Market size is estimated at USD 118.82 billion in 2025, and is expected to reach USD 152.88 billion by 2030, at a CAGR of 5.17% during the forecast period (2025-2030).

Key Highlights

- The global metal print packaging market is on an upward trajectory driven by factors such as customization and premiumization, the growing adoption of metal packaging, and a heightened focus on recycling and reusable materials. Moreover, advancements in printing technologies are providing market vendors with expanded opportunities.

- The rising demand for visually appealing and personalized canned foods and beverages is poised to further propel the growth of the metal print packaging market during the forecast period. Innovations in printing inks, particularly those tailored for metal packaging, are fueling market demand. The increasing digitization of printing facilities has significantly heightened the appetite for metal print packaging.

- Metal packaging's inherent convenience in decoration enables a diverse range of effects and finishes, catering to specific markets or occasions. To expedite product entry, vendors are increasingly adopting state-of-the-art metal printing technologies. This shift is enhancing vendors' in-house production capabilities, enabling them to adeptly manage scheduling challenges and ensure timely market readiness of their metal-packaged products.

- Leading beverage manufacturers are gravitating toward customized packaging to boost shelf visibility and captivate consumers, underscoring the critical importance of metal print packaging. Pioneering this trend, Coca-Cola rolled out several campaigns centered on digitally inkjet-printed metal cans. According to Ball Corp., a prominent aluminum packaging manufacturer, the demand for aluminum cans is expected to rise owing to brands' growing apprehensions about plastic packaging and their pursuit of alternatives.

- The market faces formidable challenges. Rising prices from metal suppliers are compelling ink producers to adjust their pricing strategies. While many ink manufacturers are attempting to absorb these escalating costs, many have resorted to price hikes and surcharges.

Metal Print Packaging Market Trends

Offset Lithography is Expected to Record Significant Growth

- Offset lithography has solidified its position as the dominant method in packaging printing. It is popular for delivering high-quality prints in bulk with minimal upkeep. This efficiency has made it especially favored in developed regions, notably Europe and North America. In these areas, offset lithography is predominantly employed for printing on metal cans, a choice largely influenced by the material's hard and non-absorbent nature.

- Market leaders, such as Crown Holdings Inc., harness offset printing for both 2-piece and 3-piece metal packaging. The process involves transferring ink from a printing plate to a blanket and subsequently applying it to the metal surface. Notably, while 2-piece cans are printed post-formation, 3-piece cans are printed on sheets beforehand. Crown Food Europe caters to a variety of clients in the snacks industry, producing 100% recyclable metal containers for Bier Nuts' crunchy, coated peanuts and delivering print packaging for Satisfied Snacks' Salad Crisp concept in metal tins.

- Despite its reputation for high-quality output, offset printing faces stiff competition from cutting-edge methods like rotogravure and photogravure. Additionally, the anodized aluminum printing plates, susceptible to rust from oxidation, demand careful maintenance. Such challenges could hinder the expansion of the segment.

- Companies like Metal-Print, specializing in high-quality protective lacquering and vibrant lithography on tinplate or aluminum sheets, address a wide array of metal packaging demands. Metal-Print's offerings span from food and beverage cans to chemical containers and decorative tins. A prominent trend is the organic food industry's preference for lightweight metal cans, lauded for their excellent barrier properties and eco-friendliness.

- According to a report by the Organic Trade Association, the US organic packaged food market witnessed significant growth. The consumption value was USD 18,441.8 million in 2019, which is expected to increase to USD 25,060.4 million by 2025. This increase in demand for organic packaged food is poised to boost the reliance on offset printing in the food packaging industry.

Asia-Pacific to Witness Significant Growth

- Asia-Pacific commands a significant share of the global metal printing packaging market, primarily due to manufacturers' emphasis on cost-effective packaging solutions. While mature markets in established nations see the digital printing packaging market plateauing, China and India are gearing up for vigorous expansion in the coming seven to eight years. Bolstered by a surge in e-retail sales and a growing appetite for convenient food packaging, the region is on track to experience the most pronounced growth during the forecast period.

- Key factors driving the metal print packaging market in Asia-Pacific include rising sales of packaged foods (encompassing frozen and chilled items), growing disposable incomes, shifting lifestyles, consistent economic growth, and an uptick in beverage consumption, both alcoholic and non-alcoholic.

- Beer packaging predominantly favors metal cans, attributed to their superior ability to preserve taste. Projections from Agriculture and Agri-Food Canada indicate a leap in India's beer consumption from 1.63 billion liters in 2020 to a staggering 3.4 billion liters by 2025. This is expected to increase the demand for printed metal cans.

- With digital printing technology automating the entire printing process, 3D printing is emerging as the next frontier. Countries like Japan, India, China, and Vietnam are witnessing a surge driven by advancements in digital printing technologies. Notably, Mitsubishi Electric recently launched two new AZ600 digital wire-laser metal 3D printer models.

- Asia-Pacific countries have ramped up their efforts on efficient metalworking techniques in recent years, aiming to slash CO2 emissions in the metal fabrication industry. This pivot seeks to curtail energy consumption and safeguard dwindling natural resources. Consequently, there is an anticipated uptick in demand for metal 3D printers, which can craft objects from 3D shape data. These printers not only significantly expedite traditional manufacturing processes but also minimize waste and boost design flexibility, allowing the integration of multiple parts and a reduction in overall weight.

Metal Print Packaging Industry Overview

The global metal print packaging market is fragmented in nature, with the presence of both small and large players. Major players holding significant market shares are actively working to broaden their global consumer base. Key players include Toyo Seihan Co. Ltd, Ball Corporation, Hubergroup Deutschland GmbH, Envases Group, CCL Container (a division of CCL Industries Inc.), and Koenig & Bauer AG. These companies are bolstering their market presence through strategic partnerships, investments in innovative solutions, and new product launches, all aimed at gaining a competitive edge during the forecast period.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rapid Evolution of Digital Print Technology

- 5.2 Market Challenges

- 5.2.1 Fluctuations in the Prices of Printing Inks

- 5.2.2 Presence of Alternate Packaging Solutions

6 MARKET SEGMENTATION

- 6.1 By Printing Process

- 6.1.1 Offset Lithography

- 6.1.2 Gravure

- 6.1.3 Flexography

- 6.1.4 Digital

- 6.1.5 Other Printing Technologies

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Hubergroup Deutschland GmbH

- 7.1.2 Crown Holdings Inc.

- 7.1.3 CCL Container (CCL Industries Inc.)

- 7.1.4 Ball Corporation

- 7.1.5 Koenig & Bauer AG

- 7.1.6 Toyo Seikan Group Holdings, Ltd

- 7.1.7 Envases Group

- 7.1.8 Real Pad Printer

- 7.1.9 Ardagh Metal Packaging (AMP)