|

시장보고서

상품코드

1690143

전력 엔지니어링, 조달 및 건설(EPC) - 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Power Engineering, Procurement, And Construction (EPC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

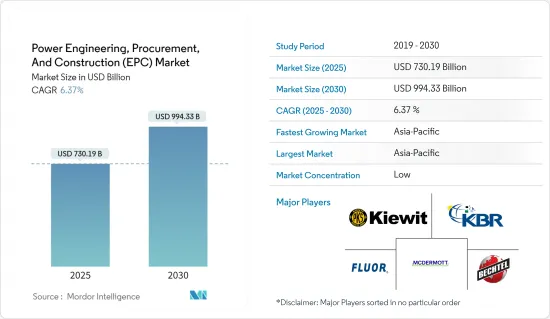

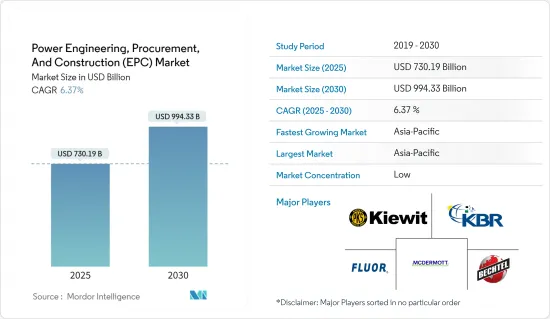

전력 엔지니어링, 조달 및 건설(EPC) 시장 규모는 2025년에 7,301억 9,000만 달러, 2030년에는 9,943억 3,000만 달러에 달할 것으로 예측됩니다. 예측 기간(2025-2030년) CAGR은 6.37%를 나타낼 전망입니다.

주요 하이라이트

- 장기적으로는 발전량 증가, 에너지 소비 수요, 발전 산업의 역학의 변화 등의 요인이 전력 엔지니어링, 조달 및 건설(EPC) 시장 수요를 촉진할 것으로 예상됩니다.

- 한편, 세계 발전에서 큰 점유율을 차지하는 석탄 기반 발전소의 단계적 폐지와 일부 업스트림 프로젝트의 지연으로 이어지는 불안정한 원유 가격은 전력 엔지니어링, 조달 및 건설(EPC) 시장의 성장을 방해할 것으로 예상됩니다.

- 초임계압이나 초임계압의 석탄발전소와 같은 새롭고 효율적인 기술과 재생가능에너지의 점유율을 확대하기 위한 정부의 대처가 향후 전력 엔지니어링, 조달 및 건설(EPC) 시장에 몇 가지 기회를 만들어낼 것으로 예상됩니다.

- 예측 기간 동안 아시아태평양이 가장 큰 시장이 될 것으로 예상됩니다.

전력 엔지니어링, 조달 및 건설(EPC) 시장 동향

시장 세분화는 신재생에너지가 급성장할 전망

- 온실가스 배출과 기후 변화 등 화석연료가 환경에 미치는 악영향에 대한 인식이 세계적으로 높아지고 있습니다. 정부, 조직, 개인은 이산화탄소 배출량을 줄이고 보다 깨끗한 에너지원으로 전환하는 데 점점 더 많은 노력을 기울이고 있습니다. 태양광, 풍력, 수력, 바이오매스 등의 재생가능 에너지는 화석연료를 대체할 수 있는 지속가능하고 저탄소 대체 에너지를 제공하여 재생가능 프로젝트에 대한 수요를 견인하고 있습니다.

- 게다가, 수년에 걸쳐 재생가능 에너지 기술의 비용은 현저하게 저하되고, 종래의 에너지원과의 경쟁이 증가하고 있습니다. 태양전지판의 효율성, 풍력 터빈 기술, 에너지 저장 시스템의 지속적인 발전은 신재생 에너지 프로젝트의 신뢰성, 확장성 및 비용 효과를 향상시켰습니다. 이것은 투자자의 신뢰를 높이고 EPC 기업과 프로젝트 개발자들에게 재생 가능 에너지가 더욱 매력적이었습니다.

- 국제재생가능에너지기구(IRENA)의 보고에 따르면 2023년 세계의 재생가능에너지 설비 용량은 약 3.9테라와트에 달하고, 전년보다 14% 가까이 급증했습니다. 지난 수십년동안 신재생에너지 부문은 기술비용의 급락과 기존의 에너지원에 대한 환경적 우려 증가로 급성장해 왔습니다.

- 또한 세계 각국의 정부는 신재생에너지의 도입을 촉진하기 위한 지원 시책과 인센티브를 실시했습니다. 이러한 조치에는 고정 가격 구매 시스템, 세액 공제, 보조금, 신재생 에너지 포트폴리오 기준 등이 포함됩니다. 이로 인해 신재생에너지 프로젝트에 유리한 비즈니스 환경이 구축됩니다. 안정적이고 장기적인 조치는 예측 가능한 시장 전망을 제공하고 재생 가능 에너지 EPC 프로젝트에 대한 투자를 촉진합니다.

- 예를 들어 인도 정부는 2023년 4월 올해의 첫 2분기에 15GW 프로젝트 경매를 실시할 계획을 발표했습니다. 경매는 인도 정부를 대신하여 Solar Energy Corp. of India Ltd., NTPC Ltd., NHPC Ltd., SJVN Ltd.를 포함한 국영 전력 회사들이 진행합니다.

- WindEurope의 보고에 따르면 풍력발전시장의 성숙한 진입기업인 유럽에서는 2023년에 18.3 GW의 신규 풍력발전 용량이 추가되었습니다. 에너지 목표를 달성하는 데 필요한 용량의 절반에 불과합니다 신규 설비의 79%는 육상 설비였지만, 해양 설비는 과거 최고의 3.8GW에 이르렀습니다.

- 향후, 유럽에서는 2024-2030년까지 260GW의 풍력 발전 용량이 새롭게 추가될 예정입니다. EU-27은 이 중 200GW, 연평균 29GW의 공헌이 전망되고 있습니다. 2030년 기후 및 에너지 목표에 맞추기 위해 EU는 그 페이스를 연간 33GW까지 가속시켜야 합니다.

- 2024년 10월, Mitsubishi Heavy Industries, Ltd.(MHI)의 일부문인 Mitsubishi Power는 풍력 발전의 전력 엔지니어링, 조달 및 건설(EPC) 사업을 개시했습니다. Power는 미야자키현 히나타시에 50메가와트(MW)의 목질 바이오매스 화력발전소를 완성시켰습니다. 휴가 바이오매스 발전소는 MHI가 주도하는 컨소시엄의 제품으로, 엔지니어링, 조달 및 건설(EPC)을 위한 풀 턴키 솔루션입니다. 이 시설은 특수목적회사(SPC)인 휴가 바이오매스 파워(Hyuga Biomass Power Co., Ltd.)가 운영할 예정입니다.

- 이상의 것으로부터, 재생 가능 에너지는 예측 기간중, 시장 조사에 있어서 중요한 역할을 할 것으로 예상됩니다.

아시아태평양이 시장을 독점할 전망

- 중국, 인도, 일본, 한국, 동남아시아 등으로 구성된 아시아태평양은 강력한 경제 성장을 이루고 있습니다.

- Asia-Pacific Population and Development Report 2023에 따르면 아시아태평양에는 세계 인구의 60% 이상과 대도시의 60%가 집중하고 있습니다.

- 예를 들어 BP Statistical Review of World Energy 2023에 따르면 이 지역의 1차 에너지 소비량은 2013년 219.8 엑사줄에서 2023년 291.77 엑사줄로 증가하여 2022년 수준에서 4.7% 증가했습니다.

- 또한 아시아태평양의 많은 국가들은 기후 변화 우려를 해결하고 화석연료에 대한 의존도를 줄이고 에너지 안보를 강화하기 위해 야심찬 신재생에너지 목표를 세우고 있습니다. 발전을 촉진하기 위해 유리한 시책, 인센티브, 규제 프레임워크을 도입하고 있습니다.

- 게다가 인도 정부는 이산화탄소 배출을 억제하기 위해 신재생에너지에 많은 투자를 하고 있습니다. 기용량은 203.22GW에 달하고, 태양광발전(92.12GW)과 풍력발전(47.72GW)이 설비용량에 크게 공헌하고 있습니다.

- 2024년 9월 인도는 해상풍력발전 프로젝트의 입찰을 시작하여 신재생에너지 여행에서 매우 중요한 순간을 맞이했습니다. 신재생에너지부 산하 기관인 인도 태양 에너지 공사(SECI)가 공고한 이번 입찰은 구자라트주 앞바다에 위치한 500MW의 해상 풍력발전소 입찰을 모집하고 있습니다.

- 대규모 재생 가능 에너지 발전 프로젝트의 급증으로 총 발전량에서 차지하는 석탄의 비율은 2020년의 62%에서 2023년에는 49.5%로 감소했습니다. 측량을 3GW에서 4GW로 끌어올렸습니다.

- 따라서 급속한 경제 성장, 도시화, 정부의 이니셔티브, 신재생에너지 도입, 인프라 개발, 산업 수요, 기술진보에 견인되어 아시아태평양이 시장을 독점하게 됩니다.

전력 엔지니어링, 조달 및 건설(EPC) 산업 개요

전력 엔지니어링, 조달 및 건설(EPC) 시장은 세분화되어 있습니다. 시장의 주요 진출기업(특별한 순서 없음)에는 Fluor Corp., KBR Inc., Kievit Corporation, McDermott International Ltd., Bechtel Corporation, Saipem SpA 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 조사의 전제

제2장 조사 방법

제3장 주요 요약

제4장 시장 개요

- 소개

- 2029년까지 시장 규모와 수요 예측(단위: 달러)

- 2029년까지의 설치 용량과 예측

- 1차 에너지 소비량(단위: MTOE, 2023년)

- 최근 동향과 개발

- 정부의 규제와 시책

- 시장 역학

- 성장 촉진요인

- 에너지 수요 증가

- 재생 가능 에너지원의 채용 증가

- 억제요인

- 종래의 전력원의 단계적 폐지

- 높은 초기 투자 비용과 제한된 천연 자원

- 성장 촉진요인

- 공급망 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

- 투자분석

제5장 시장 세분화

- 발전

- 화력

- 원자력

- 신재생에너지

- 송배전(T&D)-(질적 분석만)

- 시장 분석 : 지역별 시장 분석 - 2028년까지 시장 규모 및 수요 예측(지역에 의함)

- 북미

- 미국

- 캐나다

- 기타 북미

- 유럽

- 독일

- 영국

- 이탈리아

- 스페인

- 프랑스

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 나이지리아

- 이집트

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 주요 기업의 전략

- 기업 프로파일

- EPC Developers

- Fluor Ltd

- John Wood PLC

- Kiewit Corporation

- McDermott International Inc.

- Bechtel Corporation

- Saipem SpA

- Larsen & Toubro Limited

- KBR Inc

- Original Equipment Manufacturers(OEMs)

- General Electric Company

- Siemens Energy AG

- ABB Ltd

- Schneider Electric SE

- Eaton Corporation PLC.

- EPC Developers

제7장 시장 기회와 앞으로의 동향

- 송전망의 근대화와 스마트 기술

The Power Engineering, Procurement, And Construction Market size is estimated at USD 730.19 billion in 2025, and is expected to reach USD 994.33 billion by 2030, at a CAGR of 6.37% during the forecast period (2025-2030).

Key Highlights

- Over the long term, factors such as increased electricity generation, energy consumption demand, and changing power generation industry dynamics are expected to drive demand for the power EPC market. Moreover, investments in the power sector, including increased government spending on renewable energy, are further expected to boost the market.

- On the other hand, the phasing out of coal-based power plants, which account for a major share in power generation around the globe, and volatile crude oil prices leading to delays in several upstream projects are expected to hinder the growth of the power EPC market.

- Nevertheless, new and efficient technologies like supercritical and ultra-supercritical coal power plants and government initiatives to increase renewable energy's share are expected to create several opportunities for the power EPC market in the future.

- Asia-Pacific is expected to be the largest market during the forecast period. It is due to the high urbanization growth rate and growing electricity demand, mainly from China and India.

Power Engineering, Procurement, And Construction (EPC) Market Trends

Renewable Expected to be the Fastest-growing Market Segment

- There is a growing global awareness of the adverse impacts of fossil fuels on the environment, including greenhouse gas emissions and climate change. Governments, organizations, and individuals increasingly commit to reducing carbon emissions and transitioning to cleaner energy sources. Renewable energy, such as solar, wind, hydroelectric, and biomass, offers a sustainable and low-carbon alternative to fossil fuels, driving the demand for renewable projects.

- Moreover, over the years, the costs of renewable energy technologies significantly declined, making them increasingly competitive with conventional energy sources. The continuous advancements in solar panel efficiency, wind turbine technology, and energy storage systems improved renewable energy projects' reliability, scalability, and cost-effectiveness. It boosted investors' confidence and made renewable energy more attractive for EPC companies and project developers.

- In 2023, global installed renewable energy capacity hit approximately 3.9 terawatts, marking a nearly 14 percent surge from the prior year, as reported by the International Renewable Energy Agency (IRENA). Over the past few decades, the renewable energy sector has witnessed a meteoric rise, driven by plummeting technology costs and growing environmental concerns over conventional energy sources.

- Additionally, governments worldwide are implementing supportive policies and incentives to promote renewable energy deployment. These policies include feed-in tariffs, tax credits, grants, and renewable portfolio standards. It creates a favorable business environment for renewable energy projects. Stable and long-term policies provide a predictable market outlook and encourage investments in renewable EPC projects.

- For instance, in April 2023, the Indian government announced plans to conduct auctions for 15 GW of projects in the first two quarters of the current fiscal year, 2023. Additionally, approximately 10 GW of projects will be offered in subsequent quarters. The auctions will be conducted by state-run power companies, including Solar Energy Corp. of India Ltd., NTPC Ltd., NHPC Ltd., and SJVN Ltd., on behalf of the government.

- In 2023, Europe, a mature player in the wind power market, added 18.3 GW of new wind power capacity, as reported by WindEurope. Of this, the EU-27 accounted for a record 16.2 GW. However, this figure is only half of the capacity needed to meet the EU's 2030 climate and energy targets. While 79% of the new installations were onshore, offshore installations reached a record 3.8 GW. Despite the growth in offshore capacity, projections indicate that two-thirds of installations through 2030 will remain onshore.

- Looking ahead, Europe is set to add 260 GW of new wind power capacity from 2024 to 2030. The EU-27 is expected to contribute 200 GW of this total, averaging 29 GW annually. However, to align with its 2030 climate and energy targets, the EU must accelerate its pace to 33 GW per year. This anticipated surge is poised to significantly energize the wind power EPC market in the coming years.

- In October 2024, Mitsubishi Power, a division of Mitsubishi Heavy Industries, Ltd. (MHI), completed a 50-megawatt (MW) woody biomass-fired power plant in Hyuga, Miyazaki Prefecture. The Hyuga Biomass Power Plant, a product of a consortium led by MHI, is a full turnkey solution for engineering, procurement, and construction (EPC). The facility will be operated by Hyuga Biomass Power Co., Ltd., a special purpose company (SPC).

- Therefore, according to the above points, renewable energy is expected to play a significant role in market studies during the forecasted period.

Asia-Pacific Expected to Dominate the Market

- The Asia-Pacific region, comprising countries such as China, India, Japan, South Korea, and Southeast Asia, is experiencing robust economic growth. This growth increased industrialization, urbanization, and infrastructural development, driving the demand for new power projects and creating a significant market for EPC services.

- According to the Asia-Pacific Population and Development Report 2023, the Asia-Pacific region is home to more than 60% of the global population and 60% of the large cities. In the future, the continent will witness increasing demand for power due to the increasing penetration of renewable energy sources, rising power consumption, and growing access to electricity, expanding and enhancing the power grid infrastructure. Countries like China, India, Japan, and Australia are expected to be the key contributing nations in the region.

- For instance, according to the BP Statistical Review of World Energy 2023, primary energy consumption in the region increased from 219.8 exajoules in 2013 to 291.77 exajoules in 2023, representing a 4.7% increase from 2022 levels.

- Furthermore, many countries in the Asia-Pacific region set ambitious renewable energy targets to address climate change concerns, reduce dependence on fossil fuels, and enhance energy security. Governments implement favorable policies, incentives, and regulatory frameworks to promote renewable energy development. As a result, there is a surge in renewable energy projects such as solar, wind, and hydroelectric power, creating a thriving market for EPC firms.

- Moreover, the Government of India is investing significantly in renewable energy to curb carbon emissions. This includes launching various large-scale sustainable power projects and championing green energy initiatives. As of October 2024, India's renewable energy capacity reached 203.22 GW, with solar power (92.12 GW) and wind (47.72 GW) majorly contributing to installed capacity. The nation aims for an ambitious target of 500 GW of installed renewable energy capacity by 2031-32, bolstering the growth of the power EPC market.

- In September 2024, India marked a pivotal moment in its renewable energy journey by unveiling its inaugural offshore wind project tender. The tender, issued by the Solar Energy Corporation of India Ltd (SECI) - an entity under the Ministry of New and Renewable Energy - seeks bids for a 500-MW offshore wind farm situated off the coast of Gujarat. The successful bidder will secure a 25-year power purchase agreement (PPA) with SECI and take on the responsibilities of constructing, owning, and operating the wind farm.

- Due to surging large-scale renewable energy projects, coal's share in the total electricity generation dwindled from 62% in 2020 to 49.5% in 2023. In October 2024, The Clean Energy Regulator, responsible for approving new power station capacities under the Renewable Energy Target, upped its forecast for large-scale wind and solar capacity approvals from 3GW to 4GW for 2024. The total new renewable capacity is projected to surpass 7GW in 2024, complemented by an anticipated 3.1GW of small-scale capacity. Following these announcements, the capacity of financially committed renewable electricity generation projects for 2024 (1.6 GW) has eclipsed the total for 2023 (1.3 GW).

- Therefore, driven by rapid economic growth, urbanization, government initiatives, renewable energy deployment, infrastructure development, industrial demand, and technological advancements, Asia-Pacific is set to dominate the market.

Power Engineering, Procurement, And Construction (EPC) Industry Overview

The power engineering, procurement, and construction (EPC) market is fragmented. Some of the major players in the market (in no particular order) include Fluor Corp., KBR Inc., Kiewit Corporation, McDermott International Ltd, Bechtel Corporation, and Saipem SpA, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, Till 2029

- 4.3 Installed Capacity and Forecast, Till 2029

- 4.4 Primary Energy Consumption, in MTOE, 2023

- 4.5 Recent Trends and Developments

- 4.6 Government Policies and Regulations

- 4.7 Market Dynamics

- 4.7.1 Drivers

- 4.7.1.1 Growing Energy Demand

- 4.7.1.2 Increasing Adoption Of Renewable Energy Sources

- 4.7.2 Restraints

- 4.7.2.1 Phasing Out of Conventional Sources of Electricity

- 4.7.2.2 High Initial Investment Cost And Limited Natural Resources

- 4.7.1 Drivers

- 4.8 Supply Chain Analysis

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Consumers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitute Products and Services

- 4.9.5 Intensity of Competitive Rivalry

- 4.10 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Power Generation

- 5.1.1 Thermal

- 5.1.2 Nuclear

- 5.1.3 Renewables

- 5.2 Power Transmission and Distribution (T&D) - (Qualitative Analysis Only)

- 5.3 Geography Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)}

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 Italy

- 5.3.2.4 Spain

- 5.3.2.5 France

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Chile

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 EPC Developers

- 6.3.1.1 Fluor Ltd

- 6.3.1.2 John Wood PLC

- 6.3.1.3 Kiewit Corporation

- 6.3.1.4 McDermott International Inc.

- 6.3.1.5 Bechtel Corporation

- 6.3.1.6 Saipem SpA

- 6.3.1.7 Larsen & Toubro Limited

- 6.3.1.8 KBR Inc

- 6.3.2 Original Equipment Manufacturers (OEMs)

- 6.3.2.1 General Electric Company

- 6.3.2.2 Siemens Energy AG

- 6.3.2.3 ABB Ltd

- 6.3.2.4 Schneider Electric SE

- 6.3.2.5 Eaton Corporation PLC.

- 6.3.1 EPC Developers

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Grid Modernization and Smart Technologies

(주말 및 공휴일 제외)