|

시장보고서

상품코드

1690184

미국의 콜드체인 물류 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)US Cold Chain Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

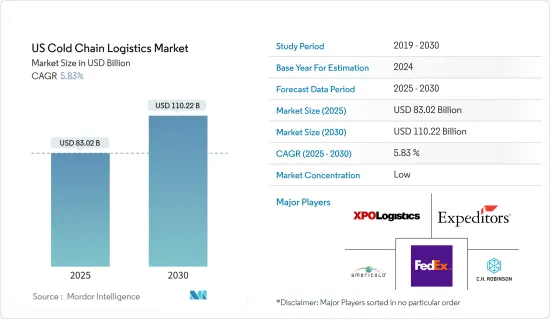

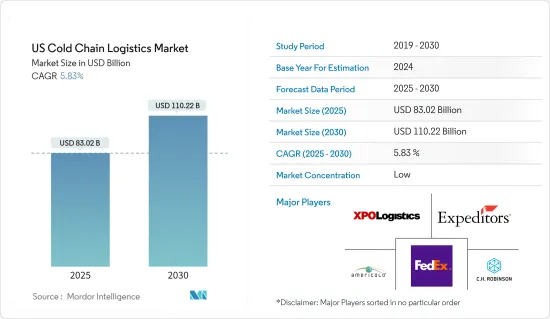

미국의 콜드체인 물류 시장 규모는 2025년에 830억 2,000만 달러, 2030년에는 1,102억 2,000만 달러에 달할 것으로 예측됩니다. 예측 기간(2025-2030년) CAGR은 5.83%를 나타낼 전망입니다.

주요 하이라이트

- COVID-19의 대유행에 의해 국내의 전자 소매 섹터와 가공 식품·식음료의 소비가 크게 늘어나, 냉장 보관 스페이스와 물류 수요를 밀어 올렸습니다.신선 식품이나 냉동 식품의 주문이 큰 비율을 차지하는 온라인 식료품점의 대두도, 시장 수요를 지지하고 있습니다.

- 그러나 운송 및 창고 부문에서의 노동력 부족, 높은 에너지 요건, 콜드체인 물류 업무에 의한 환경에 대한 악영향은 시장의 성장을 제한할 가능성이 있는 과제의 일부입니다.

- 인공지능(AI), 머신러닝, 사물인터넷(IoT), 로봇공학, 웨어, 배송센터 자동화 등의 기술은 업무의 효율화, 운영비용 절감, 보다 좋은 고객체험 제공을 목적으로 진입기업에 의해 도입되고 있습니다.

- 보다 광범위한 산업 물류 시장 전체에서 아웃소싱이 증가하고 있으며, 2021년 동기간의 30%에서 증가하고, 2022년 5월까지 임대 활동 전체의 34%를 제3자 물류(3PL) 프로바이더가 차지하고 있습니다.

- 미국 농무성(USDA)에 따르면 미국의 냉장 창고 용량의 72%는 공개 냉장 창고(PRW) 회사에 위탁되고 있으며, 5년 전의 75%에서 감소하고 있습니다.

- 신선품의 수입, 생물 제제 부문을 포함한 제약 산업의 성장, 냉동 식품의 소비 확대, 의약품의 온도 모니터링 규제 등이 미국의 콜드체인 물류 시장 수요 촉진요인이 되고 있습니다.

미국 콜드체인 물류시장 동향

멕시코에서 신선한 식품 수입 증가

- 미국은 세계에서 연간 220억 달러 상당의 신선식품을 수입하고 있으며, 125개국 이상에서 신선식품을 받아들이고 있습니다.

- 라틴아메리카와 북미를 연결하는 항공화물로 수송되는 상품의 거의 70%는 신선품입니다.

- 멕시코는 미국에 있어서 최대의 농산물 무역 상대국이며, 2022년의 총 수입액은 719억 달러(수입+수출)였습니다., 멕시코로부터의 수입은 434억 달러입니다.

- 미국 농무성(USDA)에 따르면, 2022년 멕시코에서 미국 농산물 수입의 83.6%는 야채, 과일, 음료, 증류주였습니다.

- 미국은 2022년 멕시코에서 신선, 냉동, 가공 과일, 야채, 견과류를 포함한 187억 달러의 농산물을 수입했습니다. 이 수입품의 98% 이상이 멕시코와 텍사스, 뉴멕시코, 애리조나, 캘리포니아 사이의 육로항에서 미국에 입항하고 있습니다.

- 이 수입은 59만 906개의 4만 파운드 트럭으로 출하되었습니다.

냉동 식품의 인기 증가

- 미국 냉동식품협회(AFFI)의 보고에 따르면, 2022년 냉동식품 매출은 8.6% 증가한 722억 달러가 되었으며, 그 사이의 판매 개수는 감소했지만, 유통 전 수준을 5% 웃돌게 되었습니다.

- 2018-2022년 사이에 냉동식품의 달러 매출은 194억 달러나 증가했고, 유통이 이 카테고리의 성장에 미치는 영향을 명확히 했습니다. 일관되게 상승하고 있지만, 판매 개수는 2021년과 2022년 양쪽에서 각각 3.2%와 5.1% 감소하고 있어, 냉동 식품의 비용에 대한 인플레이션의 잠재적 영향이 부각되고 있습니다.

- 감소에도 불구하고, 판매 개수는 유행 전의 수준과 비교하면 여전히 고수준에 있으며, 냉동 식품에 대한 수요가 계속되고 있는 것을 나타내고 있습니다.

- AFFI의 새로운 조사에 의하면, 쇼핑객의 4분의 1 이상이 3년 전보다 냉동 야채 및 과일을 구입하고 있어, 이러한 식품에는 많은 이점이 있다고 인식하고 있습니다. 가정이나 인구층이 농산물의 소비량을 늘려 식품 폐기물을 줄이는 것을 용이하게 합니다.

- 미국의 냉동과일 및 채소 매출은 2022년 6월 26일까지 52주간 71억 달러에 이르렀고, 제품량은 팬데믹 전 수준을 상회하는 2억 7,100만 파운드를 초과했습니다. 이 부문의 상위 제품은 일반 야채, 감자, 양파, 과일로 매출은 각각 29억 달러, 23억 달러, 15억 달러였습니다.

미국 콜드체인 물류 산업 개요

미국의 콜드체인 물류 시장은 매우 세분화되어 있으며, 온도 변화에 민감한 상품의 국내와 국제 운송을 지원하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 성과

- 조사의 전제

- 조사 범위

제2장 조사 방법

- 분석 방법

- 조사 단계

제3장 주요 요약

제4장 시장 역학과 인사이트

- 현재의 시장 시나리오

- 시장 역학

- 성장 촉진요인

- 제약산업의 성장

- 멕시코에서 신선한 식품 수입 증가

- 냉동식품의 인기 상승

- 억제요인

- 콜드체인 작업에 의한 배출

- 노동력 부족

- 기회

- 에너지 효율이 높은 솔루션의 채용

- 온라인 식료품 비즈니스의 상승

- 성장 촉진요인

- 산업의 매력 - Porter's Five Forces 분석

- 구매자, 소비자의 협상력

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 기술 동향과 자동화에 관한 통찰

- 정부의 규제와 대처에 관한 통찰

- 산업의 밸류체인, 공급 체인 분석

- 환경 및 온도 관리된 보관고에 대한 주목

- 배출 기준과 규제가 콜드체인 산업에 미치는 영향

- COVID-19가 시장에 미치는 영향

제5장 시장 세분화

- 서비스별

- 보관

- 수송

- 부가가치 서비스(블라스트 동결, 라벨링, 재고 관리 등)

- 온도 유형별

- 냉장

- 냉동

- 상온

- 용도별

- 과일·야채

- 유제품(우유, 버터, 치즈, 아이스크림 등)

- 생선, 고기, 수산물

- 가공식품

- 의료 의약품

- 베이커리 및 제과

- 기타

제6장 경쟁 구도

- 시장 집중 개요

- 기업 프로파일

- FedEx

- XPO Logistics

- CH Robinson Worldwide

- JB Hunt

- Expeditors

- Total Quality Logistics

- Americold Logistics

- Burris Logistics

- Prime Inc.

- Lineage Logistics

- Arc Best

- Stevens Transport

- DHL Supply Chain

- United States Cold Storage

- DB Schenker

- Covenant Transportation Services*

제7장 시장의 미래

제8장 부록

SHW 25.05.09The US Cold Chain Logistics Market size is estimated at USD 83.02 billion in 2025, and is expected to reach USD 110.22 billion by 2030, at a CAGR of 5.83% during the forecast period (2025-2030).

Key Highlights

- The COVID-19 pandemic significantly boosted the domestic e-retailing sector and the consumption of processed foods and beverages, pushing the demand for refrigerated storage spaces and logistics. The rise of online groceries, with a significant share of orders for perishables and frozen foods, is also supporting the market demand. The market has also benefitted significantly from the stringent government regulation toward the production and supply of temperature-sensitive products.

- However, the labor shortages in the transportation and warehousing sector, high energy requirements, and the negative environmental impact of the cold chain logistics operations are some of the challenges that may limit the market growth. To tackle the challenges regarding the high energy requirements and negative environmental impact, some companies are introducing solutions that increase the energy required to run the cold chain infrastructure.

- Technologies like Artificial Intelligence (AI), Machine Learning, Internet of Things (IoT), Robotics, Ware, and distribution center automation are being incorporated by players to increase the efficiency of their operations, reduce operational costs, and provide better customer experience.

- More outsourcing is occurring throughout the broader industrial logistics market, with third-party logistics (3PL) providers accounting for 34% of total leasing activity in 2022 through May, up from 30% in the same period of 2021. This trend is particularly common in the cold storage industry due to costs and more complex technology systems.

- According to the US Department of Agriculture (USDA), 72% of the refrigerated storage capacity in the US is outsourced to public refrigerated warehouse (PRW) companies, down from 75% five years ago. The remaining 28% includes in-house cold chain operators, up from 25% five years ago.

- The perishables imports, pharmaceutical industry growth, including the biologics sector, increasing consumption of frozen foods, pharmaceutical temperature monitoring regulations, etc., are the demand drivers for the cold chain logistics market in the United States.

US Cold Chain Logistics Market Trends

Rising fresh produce imports from Mexico

- The United States imports over USD 22 billion worth of fresh produce annually from all over the globe and receives fresh produce from over 125 countries. Thirty-two percent of the country's fresh vegetables and fifty-five percent of its fresh fruit are imported from other countries.

- Almost 70% of all goods shipped via air freight between Latin America and North America consist of perishable products. Seventy-seven percent of the fresh fruits and vegetables imported by the United S come from Mexico, with an additional 11% from Canada.

- Mexico is the largest agricultural trading partner for the United States, totaling USD 71.9 billion (imports plus exports) in 2022. US agricultural exports to Mexico totaled USD 28.5 billion, while imports from Mexico totaled USD 43.4 billion. The main agricultural products imported from Mexico are fruits and vegetables; in fact, 44% of the fruits and 48% of the vegetables imported by the US are from Mexico.

- In 2022, 83.6% of US agricultural imports from Mexico consisted of vegetables, fruit, beverages, or distilled spirits, according to the US Department of Agriculture (USDA).

- The United States imported USD 18.7 billion of produce from Mexico in 2022, including fresh, frozen, and processed fruits, vegetables, and nuts. Just over 98% of these imports entered the United States through land ports between Mexico and Texas, New Mexico, Arizona, and California. When considering only fresh fruits and vegetables, which constitute nearly 89% of the total produce, imports totaled USD 16.6 billion.

- These imports were shipped in 590,906 forty-thousand-pound truckloads. Approximately 55% of the US fresh fruit and vegetable imports from Mexico entered through Texas land ports, arriving in 325,467 truckloads worth USD 11.6 billion.

Increasing popularity of frozen foods

- The American Frozen Food Institute (AFFI) reported that frozen food sales increased 8.6% to USD 72.2 billion in 2022. Unit sales decreased during that time but remained 5% above pre-pandemic levels.

- Between 2018 and 2022, frozen food dollar sales increased a whopping USD 19.4 billion, underlining the impact of the pandemic on the category's growth. While frozen food dollar sales have consistently climbed since 2018, unit sales decreased in both 2021 and 2022 by 3.2% and 5.1%, respectively, highlighting the potential impact of inflation on frozen food costs.

- Despite the decreases, unit sales remain elevated compared to pre-pandemic levels, indicating continued demand for frozen foods. This is particularly true for frozen processed meat, frozen snacks, and seafood, which have seen double-digit increases in unit sales compared to pre-pandemic levels.

- A new survey from AFFI finds that more than a quarter of shoppers are buying more frozen fruits and vegetables than three years ago and identify many benefits with these foods. Frozen fruits and vegetables help make it easier for households and demographic groups to increase their produce consumption and reduce food waste. Overall, penetration in the United States is high, with 94% of American households buying frozen fruits and vegetables.

- The sales of frozen fruits and vegetables in the United States reached USD 7.1 billion over the 52 weeks ending June 26, 2022, and product volume were 271 million pounds above pre-pandemic levels at 3.9 billion pounds. The top products within the segment were plain vegetables, potatoes, onions, and fruit, with sales of USD 2.9 billion, USD 2.3 billion, and USD 1.5 billion, respectively.

US Cold Chain Logistics Industry Overview

The cold chain logistics market of the United States is highly fragmented, aiding the domestic as well as international transportation of temperature-sensitive goods. It is undergoing developments with the introduction of solar-powered refrigerated units, multi-temperature trucks, and freight optimization software. International and local players like FedEx, XPO Logistics, Total Quality Logistics, Americold Logistics and many such companies are operational in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 PHARMACEUTICAL INDUSTRY GROWTH

- 4.2.1.2 RISING FRESH PRODUCE IMPORTS FROM MEXICO

- 4.2.1.3 INCREASING POPULARITY OF FROZEN FOODS

- 4.2.2 Restraints

- 4.2.2.1 EMISSIONS FROM COLD CHAIN OPERATIONS

- 4.2.2.2 LABOUR SHORTAGES

- 4.2.3 Opportunities

- 4.2.3.1 Adopting energy-efficient solutions

- 4.2.3.2 rise of online grocery business

- 4.2.1 Drivers

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Buyers/Consumers

- 4.3.2 Bargaining Power of Suppliers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Insights on Technological Trends and Automation

- 4.5 Insights on Government Regulations and Initiatives

- 4.6 Industry Value Chain/Supply Chain Analysis

- 4.7 Spotlight on Ambient/Temperature-controlled Storage

- 4.8 Impact of Emission Standards and Regulations on Cold Chain Industry

- 4.9 Impact of Covid-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Services

- 5.1.1 Storage

- 5.1.2 Transportation

- 5.1.3 Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.)

- 5.2 By Temperature Type

- 5.2.1 Chilled

- 5.2.2 Frozen

- 5.2.3 Ambient

- 5.3 By Application

- 5.3.1 Fruits and Vegetables

- 5.3.2 Dairy Products (Milk, Butter, Cheese, Ice Cream, Etc.)

- 5.3.3 Fish, Meat, and Seafood

- 5.3.4 Processed Food

- 5.3.5 Healthcare & Pharmaceuticals

- 5.3.6 Bakery and Confectionary

- 5.3.7 Other Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 FedEx

- 6.2.2 XPO Logistics

- 6.2.3 CH Robinson Worldwide

- 6.2.4 JB Hunt

- 6.2.5 Expeditors

- 6.2.6 Total Quality Logistics

- 6.2.7 Americold Logistics

- 6.2.8 Burris Logistics

- 6.2.9 Prime Inc.

- 6.2.10 Lineage Logistics

- 6.2.11 Arc Best

- 6.2.12 Stevens Transport

- 6.2.13 DHL Supply Chain

- 6.2.14 United States Cold Storage

- 6.2.15 DB Schenker

- 6.2.16 Covenant Transportation Services*