|

시장보고서

상품코드

1690785

중국의 데이터센터 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)China Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

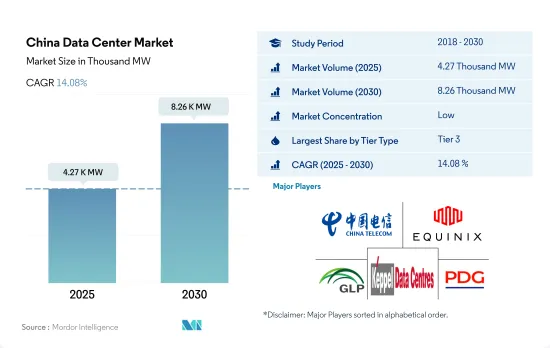

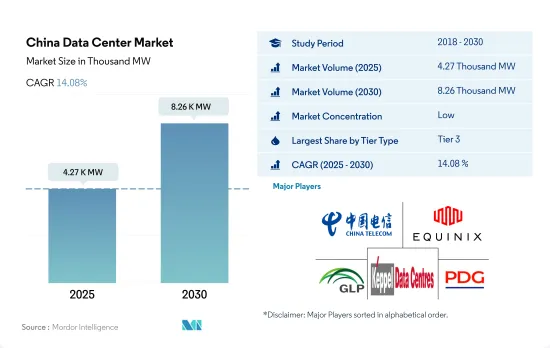

중국의 데이터센터 시장 규모는 2025년에 4,270kW로 추정되고, 2030년에는 8,260kW에 이를것으로 예측되며, CAGR 14.08%로 성장할 전망입니다.

또한 2025년 코로케이션 수익은 40억 1,170만 달러로 추정되고, 2030년에는 97억 660만 달러에 이를 것으로 예측되며, 예측 기간(2025-2030년)의 CAGR은 19.33%를 나타낼 전망입니다.

2023년 티어 3 데이터센터가 규모 면에서 과반수 점유율을 차지, 티어 4는 가장 빠르게 성장하는 부문

- 티어 3 데이터센터는 현장 지원, 전력, 냉각 이중화 등의 기능으로 인해 가장 선호도가 높습니다. 이 부문은 2022년 1,115.1MW에서 2029년 1,874MW로 5.7%의 연평균 성장률(CAGR)로 성장할 것으로 예상됩니다.

- 티어 4 데이터센터는 성능, 낮은 다운타임, 99.99%의 가동 시간으로 인해 대기업이 그 다음으로 선호하는 데이터센터입니다

- 티어 1 및 티어 2 데이터센터는 가동 중단 시간이 길고 전력 및 냉각 이중화, 현장 원격 지원으로 인해 가장 선호도가 낮은 데이터센터입니다.

중국의 데이터센터 시장 동향

Huawei, Apple, Xiaomi, Oppo, Vivo는 고급 기능을 갖춘 저렴한 스마트폰을 제공함으로써 소비자들이 이러한 제품에 더 많이 지출하도록 유도하여 중국 내 스마트폰 수요가 크게 증가하고 있습니다.

- 2022년 중국의 스마트폰 사용자 수는 9억 5,000만명으로 예측기간(2023-2029년) 말에는 18억명에 달할 것으로 예상되며, CAGR은 10.2%를 나타낼 전망입니다.

- 중국 스마트폰 업체들은 고급 기능을 갖춘 합리적인 가격의 스마트폰을 출시하고 있으며, 이는 중국 내 스마트폰 사용자 증가로 이어지고 있습니다. 약 50%의 사용자가 12-18개월마다 휴대폰을 교체하기 때문에 기업들은 휴대폰을 자주 혁신하고 있습니다. 현재 주요 시장 기업은 Huawei, Apple, Xiaomi, Oppo, Vivo입니다.

- 이러한 스마트폰 사용자 증가는 중국 데이터센터 시장의 성장에 긍정적인 영향을 미쳤습니다.

중국 정부의 '광대역 중국 전략'과 광케이블 연결성 증가로 중국 내 데이터 센터 활성화

- 2013년에 초안이 마련되고 2015년에 시행된 중국 정부의 '광대역 중국 전략'은 주로 외딴 지역을 중심으로 중국 전역에 광대역 연결을 확산한 것으로 평가받고 있습니다. 이 전략에 따라 2021년에는 도시의 주거용 광대역 속도가 100Mbps, 농촌 지역의 광대역 속도가 20Mbps에 도달했습니다. 반면 상업용/산업용 광대역 속도는 2015년 평균 100Mbps에서 2021년 1Gbps로 증가했습니다.

- 빠른 데이터 속도를 제공하기 위해 중국 시장은 수년에 걸쳐 광섬유 케이블을 설치하는 거리를 늘렸습니다. 중국 내 광섬유 케이블 네트워크 구축은 2017-2022년 동안 8.5%의 연평균 성장률(CAGR)을 기록했습니다.

- 주로 광케이블을 통한 안정적인 광대역 속도는 데이터 센터의 확장과 다른 데이터 센터 및 인터넷 교환(IX)과의 통신에 매우 중요합니다. 기업이 비즈니스의 중요한 데이터를 클라우드, 코로케이션, 사내에 저장하는 것이 일반화되었습니다. 이러한 저장 위치 내에서 다양한 서버를 통해 고객에게 다양한 서비스를 제공합니다. 통신 지점의 수가 증가함에 따라 통신 속도를 최대한 빠르게 유지하는 것이 중요해졌습니다.

중국의 데이터센터 산업 개요

중국의 데이터센터 시장은 세분화되어 있으며 상위 5개 기업에서 17.92%를 차지하고 있습니다. 이 시장의 주요 업체는 China Telecom Corporation Ltd, Equinix Inc. Ltd, Princeton Digital Group(알파벳 순)입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 시장 전망

- IT 부하 용량

- 바닥 공간 증가

- 코로케이션 수입

- 설치 랙 수

- 랙 공간 이용률

- 해저 케이블

제5장 주요 산업 동향

- 스마트폰 사용자수

- 스마트폰 1대당 데이터 트래픽

- 모바일 데이터 속도

- 광대역 데이터 속도

- 광섬유 접속 네트워크

- 규제 프레임워크

- 중국

- 밸류체인과 유통채널 분석

제6장 시장 세분화

- 핫스팟

- 베이징

- 광동성

- 허베이성

- 강소성

- 상하이

- 기타 중국

- 데이터센터의 규모

- 대규모

- 초대규모

- 중규모

- 메가규모

- 소규모

- 티어 유형

- 티어 1 및 2

- 티어 3

- 티어 4

- 흡수량

- 비활용

- 활용

- 코로케이션 유형별

- 하이퍼스케일

- 소매

- 홀세일

- 최종 사용자별

- BFSI

- 클라우드

- 전자상거래

- 정부기관

- 제조업

- 미디어 및 엔터테인먼트

- 통신

- 기타

제7장 경쟁 구도

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- BDx Data Center Pte. Ltd

- Chayora Ltd

- China Telecom Corporation Ltd

- Chindata Group Holdings Ltd

- Equinix Inc.

- GDS Service Co. Ltd

- GLP Pte Limited

- Keppel DC REIT Management Pte. Ltd

- Princeton Digital Group

- Space DC Pte Ltd

- Telehouse(KDDI Corporation)

- Zenlayer Inc.

제8장 CEO에 대한 주요 전략적 질문

제9장 부록

- 세계 개요

- 개요

- Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 세계 시장 규모와 DRO

- 출처 및 참고문헌

- 도표 목록

- 주요 인사이트

- 데이터 팩

- 용어집

The China Data Center Market size is estimated at 4.27 thousand MW in 2025, and is expected to reach 8.26 thousand MW by 2030, growing at a CAGR of 14.08%. Further, the market is expected to generate colocation revenue of USD 4,011.7 Million in 2025 and is projected to reach USD 9,706.6 Million by 2030, growing at a CAGR of 19.33% during the forecast period (2025-2030).

Tier 3 data center accounted for majority share in terms of volume in 2023, Tier 4 is fastest growing segment

- Tier 3 data centers are the most preferred due to features such as on-site assistance, power, and cooling redundancy. The segment is expected to grow from 1,115.1 MW in 2022 to 1,874 MW by 2029 at a CAGR of 5.7%. These data centers are mainly chosen by companies for storing and processing business-critical data to cater to their growing business and scalability needs. There are around 110 Tier 3 data centers in the country, and around 37 upcoming data centers are under construction with Tier 3 specifications.

- Tier 4 data centers are the next most preferred by large businesses due to their performance, lower downtime, and 99.99% uptime. These data centers are relatively costly; however, the performance offered by them outweighs the price and supports the competitive and growing needs of large businesses. In 2022, the country had seven Tier 4 data centers owned by Princeton Digital Group and SpaceDC Pte Ltd.

- Tier 1 & 2 data centers are the least preferred due to their higher downtime durations, power and cooling redundancies, and on-site remote assistance. Since these data centers are relatively cheap compared to Tier 3 and Tier 4, small businesses and startup companies prefer them. Since Tier 1 & 2 data centers are the least preferred, stagnant growth could be seen during the forecast period.

China Data Center Market Trends

Huawei, Apple, Xiaomi, Oppo, and Vivo offer cheap smartphones with high end features which attracts consumers to spend more these products creating a hige demand in smartphones in the country

- The number of Chinese smartphone users was 950 million in 2022, and the figure is expected to reach 1.8 billion by the end of the forecast period (2023-2029), registering a CAGR of 10.2%. The spread of 4G and 5G connectivity across the country has improved mobile communication, making smartphones a basic necessity for people.

- Chinese smartphone companies are offering affordable smartphones with high-end features, leading to an increase in smartphone users in the country. Around 50% of users replace their phones every 12-18 months, making companies innovate their phones frequently. Currently, the major market players are Huawei, Apple, Xiaomi, Oppo, and Vivo.

- This increase in smartphone users has positively impacted the growth of the data center market in the country. During the study period, when the number of smartphone users increased fivefold, the number of racks in data centers increased from around 70k in 2017 to 280k in 2021. This trend is expected to be witnessed during the forecast period as well.

Chinese government's "Broadband China Strategy coupled with increased fiber connectivity, boost the data centers in the country

- The Chinese government's "Broadband China Strategy," drafted in 2013 and implemented in 2015, is accredited for spreading broadband connectivity across the country, primarily in remote locations. In 2021, under this strategy, the broadband speed reached 100 Mbps for residential use in cities and 20 Mbps in rural regions. On the other hand, the broadband speed for commercial/industrial use increased from an average speed of 100 Mbps in 2015 to 1 Gbps in 2021. With further expansion of the fiber connectivity network, average speeds are estimated to rise significantly in the coming years.

- In order to provide high data speeds, the Chinese market increased the distance of laying fiber optic cables over the years. The deployment of optic fiber cable networks in the country registered a CAGR of 8.5% during 2017-2022. The deployment of fiber optic cables spurred last-mile internet connectivity in the country. As these cables offer better connectivity and higher bandwidths, most companies replaced them with traditional copper cables to offer better and upgraded services.

- Stable broadband speed, predominantly via fiber cables, is crucial for the expansion of data centers and their communication with other data centers and internet exchanges (IX). It has become common for companies to store their business's critical data in the cloud, colocation, and in-house. Within these storage locations, various services are provided to their customers across different servers. With the increase in the number of points of communication, it becomes critical to keep communication as fast as possible. Therefore, strong broadband connectivity across the country is expected to support the data centers to maintain 100% uptime during the forecast period.

China Data Center Industry Overview

The China Data Center Market is fragmented, with the top five companies occupying 17.92%. The major players in this market are China Telecom Corporation Ltd, Equinix Inc., GLP Pte Limited, Keppel DC REIT Management Pte. Ltd and Princeton Digital Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 MARKET OUTLOOK

- 4.1 It Load Capacity

- 4.2 Raised Floor Space

- 4.3 Colocation Revenue

- 4.4 Installed Racks

- 4.5 Rack Space Utilization

- 4.6 Submarine Cable

5 Key Industry Trends

- 5.1 Smartphone Users

- 5.2 Data Traffic Per Smartphone

- 5.3 Mobile Data Speed

- 5.4 Broadband Data Speed

- 5.5 Fiber Connectivity Network

- 5.6 Regulatory Framework

- 5.6.1 China

- 5.7 Value Chain & Distribution Channel Analysis

6 MARKET SEGMENTATION (INCLUDES MARKET SIZE IN VOLUME, FORECASTS UP TO 2030 AND ANALYSIS OF GROWTH PROSPECTS)

- 6.1 Hotspot

- 6.1.1 Beijing

- 6.1.2 Guangdong

- 6.1.3 Hebei

- 6.1.4 Jiangsu

- 6.1.5 Shanghai

- 6.1.6 Rest of China

- 6.2 Data Center Size

- 6.2.1 Large

- 6.2.2 Massive

- 6.2.3 Medium

- 6.2.4 Mega

- 6.2.5 Small

- 6.3 Tier Type

- 6.3.1 Tier 1 and 2

- 6.3.2 Tier 3

- 6.3.3 Tier 4

- 6.4 Absorption

- 6.4.1 Non-Utilized

- 6.4.2 Utilized

- 6.4.2.1 By Colocation Type

- 6.4.2.1.1 Hyperscale

- 6.4.2.1.2 Retail

- 6.4.2.1.3 Wholesale

- 6.4.2.2 By End User

- 6.4.2.2.1 BFSI

- 6.4.2.2.2 Cloud

- 6.4.2.2.3 E-Commerce

- 6.4.2.2.4 Government

- 6.4.2.2.5 Manufacturing

- 6.4.2.2.6 Media & Entertainment

- 6.4.2.2.7 Telecom

- 6.4.2.2.8 Other End User

7 COMPETITIVE LANDSCAPE

- 7.1 Market Share Analysis

- 7.2 Company Landscape

- 7.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 7.3.1 BDx Data Center Pte. Ltd

- 7.3.2 Chayora Ltd

- 7.3.3 China Telecom Corporation Ltd

- 7.3.4 Chindata Group Holdings Ltd

- 7.3.5 Equinix Inc.

- 7.3.6 GDS Service Co. Ltd

- 7.3.7 GLP Pte Limited

- 7.3.8 Keppel DC REIT Management Pte. Ltd

- 7.3.9 Princeton Digital Group

- 7.3.10 Space DC Pte Ltd

- 7.3.11 Telehouse (KDDI Corporation)

- 7.3.12 Zenlayer Inc.

- 7.4 LIST OF COMPANIES STUDIED

8 KEY STRATEGIC QUESTIONS FOR DATA CENTER CEOS

9 APPENDIX

- 9.1 Global Overview

- 9.1.1 Overview

- 9.1.2 Porter's Five Forces Framework

- 9.1.3 Global Value Chain Analysis

- 9.1.4 Global Market Size and DROs

- 9.2 Sources & References

- 9.3 List of Tables & Figures

- 9.4 Primary Insights

- 9.5 Data Pack

- 9.6 Glossary of Terms