|

시장보고서

상품코드

1690901

오프그리드 태양에너지 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Off-Grid Solar Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

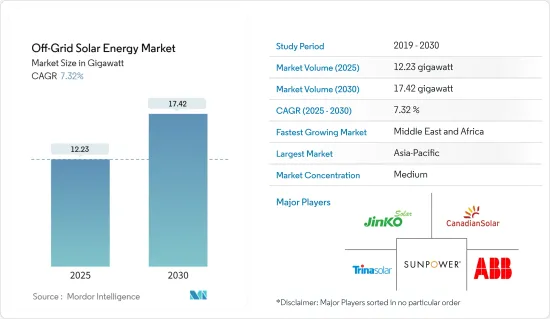

오프그리드 태양에너지 시장 규모는 2025년에 12.23기가와트로 추정되고, 예측 기간인 2025-2030년 CAGR 7.32%로 성장할 전망이며, 2030년에는 17.42기가와트에 달할 것으로 예측됩니다.

주요 하이라이트

- 장기적으로는 솔라 패널이나 배터리의 가격 저하 등이 시장을 견인할 것으로 예상됩니다.

- 한편, 높은 설치 비용과 불충분한 유지 보수가 시장의 성장을 저해하고 있습니다.

- 그러나 미국, 영국, 독일, 중국 등의 국가들은 에너지 믹스에서 신재생 에너지의 비율을 늘리겠다는 야심적인 목표를 내걸고 있습니다. 이들 국가의 정부도 향후 몇 년간 주택용과 오프그리드 태양광 발전 시스템을 도입함으로써 신재생 에너지의 비율을 늘리는 것을 계획하고 있습니다. 이를 통해 오프그리드 태양광 발전 시장에 큰 비즈니스 기회가 생길 것으로 기대되고 있습니다.

- 아시아태평양은 주로 인도와 중국의 중앙 송전망과 신뢰할 수 있는 전력 공급 부족으로 인한 전력 수요 증가로 시장 성장을 지배할 것으로 예상됩니다.

오프그리드 태양에너지 시장 동향

상업 및 산업 부문이 시장을 독점할 전망

- 상업 및 산업 부문에서의 오프그리드 태양에너지 시스템의 이용은 주로 중앙 송전망에 의한 전력 공급이 불안정한 지역의 중소 기업이 견인하고 있습니다. 배터리 일체형의 오프 그리드 솔라 시스템은, 디젤 발전기와 비교해, 상업 및 산업 사업체에 있어서 효과적이고 저렴한 전력 백업 방법이 되고 있습니다.

- 2023년 세계의 오프그리드 설치 용량은 496만 kW로 2022년 455만 kW에 비해 거의 9.01%의 성장률을 기록하고 있습니다. 이 성장률은 예측 기간 중에도 상승할 것으로 예상됩니다.

- 오프그리드 태양광 발전 시스템에는 디젤 공급망의 지연에 의한 번거로움이 없는 소음이나 오염이 적은 정부의 시책이나 보조금이 유리한 등, 상업 및 산업 부문에 있어서 많은 이점이 있습니다.

- 게다가, 일부 산업 사업체에서는 전력이 차단되어 생산이 중단되면 시스템이나 설비를 온라인으로 되돌리는데 몇 시간이 걸릴 수 있어 방대한 다운타임과 경제적 손실로 이어집니다. 따라서 전력 백업은 산업 부문에서 널리 이용되고 있습니다.

- 또한 현재 진행중인 이스라엘 가자 전쟁에서는 전쟁 개시 후 전력망이 급속히 붕괴되어 병원은 디젤 발전기에 의지하게 되었습니다. 이스라엘의 봉쇄를 통과할 수 있는 연료의 공급은 제한되어 있기 때문에 즉시 업무를 수행하고 필수불가결한 의료 서비스를 제공하는 것은 거의 불가능해졌습니다.

- 그러나 오프그리드 신재생 시스템, 특히 태양전지판과 축전지의 조합은 의료 산업을 크게 바꿀 수 있습니다. 오프그리드 태양에너지는 도시지역 병원에서 보다 효율적이고 신뢰성 높은 백업 공급을 제공하는 한편 전력망이 닿지 않는 시설에도 전력을 공급할 수 있습니다.

- 이상과 같이, 예측 기간 중 상업 및 산업 부문이 시장을 독점할 것으로 전망됩니다.

아시아태평양이 시장 성장을 지배합니다.

- 최근 주택용 및 업무용 부문에서는 태양광 발전의 설치가 꾸준히 증가하고 있습니다. 이는 태양광 발전 프로젝트의 자본 비용 절감과 부문 성숙에 따른 경쟁사 간의 경쟁 격화 때문입니다.

- 중국은 세계 최대의 태양광 발전과 태양열 에너지 시장입니다. 2023년에는 중국의 태양에너지의 총 설비 용량이 609GW에 이르렀습니다.

- 이에 따라 2023년까지 기존 주택 및 업무용 건물에는 옥상 태양광 발전 시스템의 설치가 의무화되었습니다. 정부의 의무화로 인해 태양광 발전 시스템을 설치하는 건물의 최저 비율은 필수가 되었습니다. 태양광 발전 옥상 시스템은 약 676개 카운티에 걸쳐 있는 정부 건물(적어도 50%), 공공 건물(40%), 상업 건물(30%), 농촌 지역 건물(20%)에 설치되어야 합니다.

- 태양광 발전은 인도에서 빠르게 개발되고 있는 산업입니다. 이 나라의 태양광 발전 설비 용량은 2023년 12월 31일 7,310만 kW였습니다. 인도의 태양광 발전은 2023년에는 세계 4위가 되었습니다.

- 인도에서는 산업 활동이 활발해지고 있기 때문에 탄소 배출을 완화하는 깨끗한 전력에 대한 수요가 높아지고 있습니다. 그 결과, 옥상 태양광 발전 설비는 기업이 자립하기 위한 견고한 선택이 되어 인도의 옥상 태양광 발전 시장의 확대가 기대됩니다.

- National Solar Mission(NSM)에서는 오프 그리드 태양광 발전 목표를 2GW로 하고 있습니다. 미션 1단계(2010-2013년)에서는 목표는 200MWp였지만 253MWp가 허가되었습니다. 2단계(2013-2017)에서는 목표는 500MWp였지만 713MWp가 허가되었습니다. 오프 그리드 및 분산형 태양광 발전 프로그램의 3단계에서는 PM KUSUM 방식에 설치된 태양광 펌프와 전력부의 'Saubhagya' 방식에 설치된 태양광 홈라이트를 제외하고 118MW의 목표가 유지되고 있습니다.

- 2023년 1월, 이 나라의 통상산업성(MOTIE)은 태양광 모듈의 재활용에 대한 대망의 제도를 승인했습니다. 새 규정은 각국의 주요 지역에서 통일된 데이터 수집 시스템을 구축합니다. 이것은 폐패널의 재활용/재사용률을 80% 이상으로 하는 것을 목표로 하는 것으로, 현재 EU의 수준과 일치하고 있습니다. 이러한 정부의 제도로 국내 태양광 패널 가격은 더욱 낮아져 다양한 오프그리드 제품과의 병용이 가능해질 것으로 예상됩니다.

- 이상으로부터, 이 지역에서는 태양광 발전의 가격 저하와 에너지 가격의 상승이 예측 기간중 시장을 견인할 것으로 보입니다. 또, 정부에 의한 지원 시책이나 인센티브는 오프그리드 태양에너지 시장이 향후 수년간 그 잠재력을 풀에 발휘하는데 도움이 될 것으로 예상됩니다.

오프그리드 태양에너지 산업 개요

오프그리드 태양에너지 시장은 세분화되고 있습니다. 이 시장의 주요 기업으로는, ABBLtd, Canadian Solar Inc., JinkoSolar Holding, SunPower Corporation, Trina Solar Ltd.등이 있습니다.(순부동)

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 범위

- 시장의 정의

- 조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

- 서문

- 설치 용량 및 예측(-2029년)

- 최근 동향 및 개발

- 정부 규제 및 시책

- 시장 역학

- 성장 촉진요인

- 태양전지판의 비용 저하 및 효율 향상

- 성장 억제요인

- 높은 설치 비용 및 유지 보수 비용

- 성장 촉진요인

- 공급망 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 세분화

- 최종 사용자별

- 주택용

- 상업 및 산업

- 시장 규모 및 수요 예측 : 지역별(-2029년)

- 북미

- 미국

- 캐나다

- 기타 북미

- 유럽

- 독일

- 프랑스

- 이탈리아

- 영국

- 스페인

- 노르딕

- 튀르키예

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 한국

- 일본

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 기타 아시아태평양

- 중동 및 아프리카

- 사우디아라비아

- 카타르

- 남아프리카

- 아랍에미리트(UAE)

- 나이지리아

- 오만

- 이집트

- 알제리

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 북미

제6장 경쟁 구도

- M&A, 합작사업, 제휴 및 협정

- 주요 기업의 전략

- 기업 프로파일

- ABB Ltd.

- Schneider Electric Infrastructure Ltd

- Canadian Solar Inc.

- JinkoSolar Holding Co. Ltd

- SunPower Corporation

- Trina Solar Ltd

- LONGi Green Energy Technology Co. Ltd

- JA Solar Holding

- Sharp Corporation

- Tesla Inc.

- 기타 저명한 기업 일람

- 시장 랭킹 분석

제7장 시장 기회 및 향후 동향

- 태양광 발전 제조에서 기술 진보

The Off-Grid Solar Energy Market size is estimated at 12.23 gigawatt in 2025, and is expected to reach 17.42 gigawatt by 2030, at a CAGR of 7.32% during the forecast period (2025-2030).

Key Highlights

- Over the long term, factors like decreasing the price of solar panels and batteries are expected to drive the market.

- On the other hand, high installation costs and poor maintenance practices hinder the market's growth.

- However, countries like the United States, the United Kingdom, Germany, China, and India have set ambitious targets to increase the renewable share in their energy mix. Governments across these nations have also planned to increase the renewable energy share by deploying residential and off-grid solar PV systems in the coming years. These are expected to create enormous opportunities for the off-grid solar energy market.

- Asia-Pacific is expected to dominate the market growth, primarily due to the increasing demand for electricity due to the lack of a central grid and reliable electricity supply, mainly in India and China.

Off-Grid Solar Energy Market Trends

The Commercial and Industrial Segments are Expected to Dominate the Market

- The usage of off-grid solar energy systems in the commercial and industrial segments has been mainly driven by small and medium enterprises in regions with unreliable electricity supply by the central grid system. Battery-integrated off-grid solar systems have become an effective and cheaper method of power backup for commercial and industrial entities compared to diesel generators.

- As of 2023, the global off-grid installed capacity was at 4.96 GW compared to 4.55 GW in 2022, registering a growth rate of almost 9.01%. This growth rate is expected to increase during the forecast period.

- Off-grid solar systems have many advantages for the commercial and industrial segments in terms of no hassle of diesel supply chain delays, less noise and pollution, and favorable government policies and subsidies.

- In addition, once the power is cut off and production is disrupted in several industrial entities, it may take hours to bring the systems and equipment back online, leading to huge downtime and financial losses. Therefore, electricity backup is extensively used in the industrial segment.

- Moreover, with the ongoing Israel-Gaza war, the electricity grid swiftly collapsed after the start of the war, leaving hospitals dependent on diesel generators. With only limited supplies of fuel permitted to pass through the Israeli blockade, it soon became almost impossible to carry out operations and deliver essential healthcare services.

- However, off-grid renewable systems, particularly solar panels combined with battery storage, can be a game changer for the healthcare industry. Off-grid solar offers the promise of bringing power to facilities still out of reach of electricity grids while providing a more efficient and reliable backup supply in urban hospitals.

- As mentioned above, the commercial and industrial segments will dominate the market during the forecast period.

Asia-Pacific to Dominate the Market Growth

- In recent years, there has been a steady increase in solar PV installation in the residential and commercial segments. This is due to reduced capital costs for solar projects and increased competition among competitors as the segments mature.

- China is the world's largest photovoltaics and solar thermal energy market. In 2023, the country had a total installed capacity of 609 GW of solar energy.

- Accordingly, by 2023, the existing residential or commercial buildings were required to install a rooftop solar PV system. Under the government's mandate, a minimum percentage of buildings will be essential to install solar PV systems. The solar PV rooftop systems need to be installed on government buildings (at least 50%), public structures (40%), commercial buildings (30%), and rural buildings (20%) across approximately 676 counties.

- Solar power is a fast-developing industry in India. The country's solar installed capacity was 73.10 GW as of December 31, 2023. Solar power generation in India ranked fourth globally in 2023.

- Due to the rise of industrial activity in India, the demand for clean electricity is increasing to mitigate carbon emissions. As a result, rooftop solar installations would provide a robust option for enterprises to become self-reliant, which is expected to increase the rooftop solar market in India.

- Under the National Solar Mission (NSM), a target of 2 GW was kept for off-grid solar PV applications. During Phase I of the mission (2010-2013), the target was 200 MWp, but 253 MWp was sanctioned. In Phase II (2013-2017), the target was 500 MWp, but 713 MWp was sanctioned. Under Phase III of the Off-grid and Decentralised Solar PV Applications Program, a target of 118 MW has been kept, excluding solar pumps to be installed under the PM KUSUM Scheme and solar home lights taken up under the 'Saubhagya' Scheme of the Ministry of Power.

- In January 2023, the country's Ministry of Trade, Industry, and Energy (MOTIE) approved a long-awaited scheme for solar module recycling. The new regulations set up a uniform system for collecting data in the main regions of each country. It aims to ensure a waste panel recycling/reuse rate of more than 80%, which aligns with current EU levels. Such government schemes are expected to lower the prices of solar panels further in the country, thus making it feasible to use them with different off-grid products.

- Therefore, owing to the above points, declining solar PV prices and increasing energy prices in the region are expected to drive the market during the forecast period. Also, supportive policies and incentives from the government will help the off-grid solar energy market to realize its full potential in the coming years.

Off-Grid Solar Energy Industry Overview

The off-grid solar energy market is fragmented. Some of the key players in the market (in no particular order) include ABB Ltd, Canadian Solar Inc., JinkoSolar Holding Co. Ltd, SunPower Corporation, and Trina Solar Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Installed Capacity and Forecast, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Falling Costs and Rising Efficiencies of Solar Photovoltaic Panels

- 4.5.2 Restraints

- 4.5.2.1 High Installation And Maintenance Costs

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 End-User

- 5.1.1 Residential

- 5.1.2 Commercial and Industrial

- 5.2 Geography [Market Size and Demand Forecast till 2029 (for regions only)]

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 France

- 5.2.2.3 Italy

- 5.2.2.4 United Kingdom

- 5.2.2.5 Spain

- 5.2.2.6 NORDIC

- 5.2.2.7 Turkey

- 5.2.2.8 Russia

- 5.2.2.9 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 South Korea

- 5.2.3.4 Japan

- 5.2.3.5 Malaysia

- 5.2.3.6 Thailand

- 5.2.3.7 Indonesia

- 5.2.3.8 Vietnam

- 5.2.3.9 Rest of Asia-Pacific

- 5.2.4 Middle East and Africa

- 5.2.4.1 Saudi Arabia

- 5.2.4.2 Qatar

- 5.2.4.3 South Africa

- 5.2.4.4 United Arab Emirates

- 5.2.4.5 Nigeria

- 5.2.4.6 Oman

- 5.2.4.7 Egypt

- 5.2.4.8 Algeria

- 5.2.4.9 Rest of Middle East and Africa

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Argentina

- 5.2.5.3 Colombia

- 5.2.5.4 Rest of South America

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 ABB Ltd.

- 6.3.2 Schneider Electric Infrastructure Ltd

- 6.3.3 Canadian Solar Inc.

- 6.3.4 JinkoSolar Holding Co. Ltd

- 6.3.5 SunPower Corporation

- 6.3.6 Trina Solar Ltd

- 6.3.7 LONGi Green Energy Technology Co. Ltd

- 6.3.8 JA Solar Holding

- 6.3.9 Sharp Corporation

- 6.3.10 Tesla Inc.

- 6.4 List of Other Prominent Companies (Company Name, Headquarters, Revenue, Relevant Products and Services, Operating Sector, Recent Trends, Technology or Projects, Contact Details, etc.) (In Brief Tabular Format)

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements in Solar PV Manufacturing