|

시장보고서

상품코드

1690951

북미의 매니지드 서비스 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)North America Managed Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

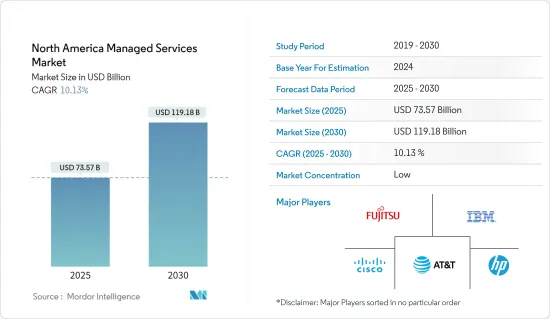

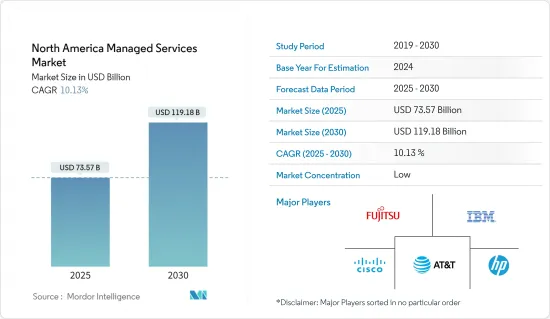

북미의 매니지드 서비스 시장 규모는 2025년에 735억 7,000만 달러로 추정되고, 예측 기간 중 2025년부터 2030년까지 CAGR 10.13%로 성장할 전망이며, 2030년에는 1,191억 8,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

- 북미 시장은 IT 인프라, 특히 사이버 보안 솔루션 아웃소싱에 지속적으로 주력하고 있는 중소기업(SME)의 상황 변화로 인해 성장하고 있습니다. 예를 들어, 미국의 신흥 IT 공급업체 제조 및 판매업체 중 하나인 KPaul Properties LLC는 후지쯔를 도입하여 물리적 서버를 가상화 환경으로 대체했습니다. 이로 인해 회사의 비용은 약 15% 절감되고 가동률은 95%에 달했습니다.

- 솔라 윈즈에 따르면 북미, 특히 미국에서는 서버, 스토리지 하드웨어, 엔드포인트 디바이스, 네트워크 장비에 대한 솔루션 제공이 MSP의 주류가 되고 있습니다. 관리형 보안 제공은 부족할 수 있지만 대부분의 솔루션 제공업체는 네트워크 및 엔드포인트 하드웨어 및 소프트웨어를 통해 보안 포인트 제품을 제공합니다.

- 이 지역에서는 IT 환경을 완벽하게 평가하고 비즈니스 라이프사이클의 각 단계에서 복잡한 비즈니스 과제를 해결하는 데 필요한 솔루션을 제공함으로써 비즈니스 요구에 맞는 IT 솔루션을 통합합니다. 예를 들어, 미국의 매니지드 솔루션은 기술적 기술 세트와 필요한 리소스를 통합하여 과제 발견, 문제 영역 진단, 필요에 따라 종합적인 기술 로드맵을 맞춤 설계, 제공, 실행하며 고객의 안전성, 컴플라이언스 및 효율성을 높입니다.

- 매니지드 서비스에는 여러 가지 장점이 있지만 신뢰성 문제와 같은 특이한 과제가 있어 예측 기간 동안 시장의 성장을 방해할 수 있습니다. 중요한 비즈니스 인프라 호스팅을 MSP에 요청하는 프로세스에는 공급자와의 신뢰 관계가 필수적입니다. 공급업체가 경쟁 시장에서 지속될 수 없는 경우, 공급업체에 의존하는 기업은 웹 호스팅, 이메일, 캘린더 및 기타 중요한 인프라를 완전히 교환해야 할 수 있습니다.

- COVID-19의 유행은 미국에서 원격으로 일하는 조직의 수를 증가시켰습니다. ALM Media Properties LLC에 따르면 미국 지식 근로자의 58%가 원격으로 작동하고 있다고 합니다. 이 수치는 COVID-19 이전의 평균에서 30% 이상 증가하고 있으며 미국 민간 직원 1억 4천만 명 중 약 7%가 재택근무로 보고된 이전 수치를 능가하고 있습니다. 이러한 전통적인 직장에서의 대량 유출은 많은 조직에서 고용주들의 기대와 텔레워크 정책에 환영해야 할 변화를 가져옵니다.

북미의 매니지드 서비스 시장 동향

IT 및 통신 분야가 큰 시장 점유율을 차지할 전망

- IT 및 통신 분야는 다양한 기술의 높은 채용률, BYOD 정책의 채용률 증가(업무 운영을 보다 쾌적하고 관리하기 쉽게 하기 위해서), 조직에 있어서 데이터량 급증에 의한 하이엔드 보안의 요구 증가 등으로부터, 매니지드 서비스의 중요한 시장이 되고 있습니다.

- 통신 업계는 지난 몇 년동안 계속 성장하고 있습니다. 경쟁이 치열한 시장에서 고객을 유지하기 위해 통신사는 혁신적인 서비스를 저비용으로 제공해야 하는 압력에 항상 노출되기 때문입니다. 복잡한 경쟁 환경을 수용하기 위해 매니지드 서비스는 통신 사업자의 광범위한 수요가 되고 있습니다.

- 게다가 설득력 있는 경제적 사례로부터 대부분의 통신 캐리어들은 네트워크 하드웨어를 소프트웨어(SDN&NFV)로 대체할 것으로 예상됩니다. SDN과 NFV 수요를 촉진하는 주요 요인으로는 시장 출시까지의 시간 개선, CAPEX와 OPEX의 감소, 비즈니스 관점에서 새로운 수입원의 개척 등이 있습니다. 이 모든 것이 조사된 시장의 성장을 가속할 것으로 예상됩니다. 이러한 노력은 매니지드 네트워크 서비스 수요를 촉진하고 있습니다.

- 북미의 많은 SD-WAN 매니지드 서비스 제공업체는 광범위한 보안을 제공함으로써 차별화를 도모하고 있습니다. 예를 들어, Cato Networks는 NGFW, Secure Web Gateway, Advanced Threat Prevention, Cloud and Mobile Access Protection, Managed Threat Detection and Response 서비스를 포함한 클라우드 네이티브 플랫폼을 제공합니다. 콜트는 레이어 7 방화벽과 DDoS 방어 기능이 있는 레이어 3/4 스테이트풀 방화벽을 제공하며, 센추리 링크는 적응형 네트워크 보안이라는 일련의 보안 서비스를 제공합니다.

급성장이 기대되는 캐나다 시장

- 캐나다의 매니지드 서비스 시장은 주로 신제품의 전개, 인수, 합병, 제휴에 의해 성장하고 있으며, 북미 시장 전체를 형성하고 있습니다. 캐나다에서는 기술 성장이 가속화되어 비즈니스 효율성 향상, 방대한 데이터 활용, 내부 협업, 기업과 고객 간의 교류 등 비즈니스 방식을 계속 바꾸고 있습니다.

- 스타포트는 캐나다에 본사를 둔 매니지드 IT 서비스 제공업체로, 캐나다 전역의 중견 기업에게 최상급 IT 설계, 도입 및 지속적인 네트워크 모니터링을 제공합니다. 고객의 대부분은 그레이터 토론토 지역에 집중되어 있습니다. 투자은행, 제조업, 상업부동산 등 다양한 산업 고객에게 서비스를 제공합니다.

- 또한 캐나다에서는 멀티 클라우드 환경의 적용과 자동화의 도입이 진행되고 있습니다. 이 지역에서 클라우드, 모바일 및 소셜 기술은 기업이 IT 보안에 적극적으로 접근해야 하기 때문에 모든 보안 관리 계층을 제공하는 견고한 매니지드 서비스 전개에 대한 수요가 증가하고 있습니다.

- 서비스로서의 통합 커뮤니케이션(UCaaS)과 관련 서비스로서의 컨택 센터(CCaaS) 시장은 매니지드 서비스 제공업체에게 비즈니스 기회입니다. 신흥 제공업체가 최소한의 투자로 도입할 수 있는 혁신적인 클라우드 기반 솔루션을 제공하고 있기 때문입니다. 또한 고객은 소비형 종량 과금 모델을 기울입니다.

- 캐나다의 클라우드 서비스 증가는 매니지드 MPLS 시장 수요를 확대할 것으로 예상됩니다. 예를 들어 캐나다 정부는 '클라우드 퍼스트' 전략을 내걸고 있으며 정보 기술에 대한 투자, 이니셔티브, 전략, 프로젝트를 시작할 때 주요 제공 옵션으로 클라우드 서비스를 식별하고 평가했습니다. 또한 클라우드를 통해 캐나다 정부는 민간 제공업체의 혁신을 활용하여 정보기술의 기동성을 높일 수 있을 것으로 기대되고 있습니다.

북미의 매니지드 서비스 산업 개요

매니지드 서비스 시장은 다수의 대기업이 존재하기 때문에 경쟁이 심합니다. 이 시장의 주요 기업으로는 Cisco Systems, IBM, Microsoft, Fujitsu, Wipro 등이 있습니다. 시장 경쟁은 치열해지고 있으며 각 회사는 전략적 제휴와 파트너십을 맺고 있습니다.

- 2021년 5월-Fujitsu Ltd와 Rakuten Mobile Inc.는 세계 시장을 위한 Open RAN 솔루션의 공동 개발에 있어서 협력 관계를 깊게 하기 위한 각서를 체결했다고 발표했습니다. 양사는 4G 및 5G의 Open RAN 솔루션의 개발을 공동으로 실시합니다.

- 2021년 11월 -AT&T는 보안 액세스 서비스 에지(SASE) 포트폴리오에 새로운 제품을 추가했습니다. AT&T SASE with Cisco는 Software-Defined Wide-area Networking(SD-WAN) 기술과 보안 기능을 활용하여 비즈니스 연결과 보호를 실현하는 네트워크와 보안의 통합 관리 시스템입니다.

- 2021년 10월-Citrix는 Managed, Unmanaged, BYO(Bring-Your-Own) 디바이스에서 앱과 데이터 액세스를 보호하는 새로운 클라우드 기반 Zero-Trust Network Access(ZTNA) 솔루션인 Citrix Secure Private Access를 발표했습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업 밸류체인 분석

- 업계의 매력도-Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

- 시장에 대한 COVID-19의 영향 평가

제5장 시장 역학

- 시장 성장 촉진요인

- 하이브리드 IT로의 시프트 증가

- 비용 및 업무 효율 개선

- 시장의 과제

- 통합, 규제 문제, 신뢰성에 대한 우려

제6장 시장 세분화

- 전개별

- 온프레미스

- 클라우드

- 유형별

- 매니지드 데이터센터

- 매니지드 보안

- 매니지드 커뮤니케이션

- 매니지드 네트워크

- 매니지드 인프라

- 매니지드 모빌리티

- 기업 규모별

- 소기업

- 중견기업

- 대기업

- 업계별

- BFSI

- IT 및 통신

- 헬스케어

- 엔터테인먼트 미디어

- 소매

- 제조업

- 정부기관

- 기타 업계별

- 국가별

- 미국

- 캐나다

제7장 경쟁 구도

- 기업 프로파일

- Fujitsu Ltd

- Cisco Systems Inc.

- IBM Corporation

- AT&T Inc.

- HP Development Company LP

- Microsoft Corporation

- Verizon Communications Inc.

- Dell Technologies Inc.

- Citrix Systems Inc.

- Rackspace Inc.

제8장 투자 분석

제9장 시장의 미래

AJY 25.04.09The North America Managed Services Market size is estimated at USD 73.57 billion in 2025, and is expected to reach USD 119.18 billion by 2030, at a CAGR of 10.13% during the forecast period (2025-2030).

Key Highlights

- The North American market is growing due to the changing landscape of IT infrastructure, especially in small and medium enterprises (SMEs), which continually focus on outsourcing cybersecurity solutions. For instance, KPaul Properties LLC, one of the emerging manufacturers and distributors of IT supplies in the United States, onboarded Fujitsu to replace a physical server with a virtualized environment. This reduced the company's cost by around 15% and delivered 95% uptime.

- According to SolarWinds, in North America, server and storage hardware, endpoint devices, and networking gear solution offerings dominate among MSPs, especially in the United States. Though managed security offerings may be lacking, most solution providers offer security point products in network and endpoint hardware and software.

- In the region, companies are integrating IT solutions tailored to business needs by providing a full assessment of the IT environment and delivering the solutions needed to solve complex business challenges at every stage of the business lifecycle. For instance, Managed Solution, a US company, integrated technical skillsets and the required resources to discover challenges, diagnose problem areas, and custom design, deliver, and execute a comprehensive technology roadmap based on needs, making customers more secure, compliant, and efficient.

- Although managed services offer various benefits, specific challenges, like reliability concerns, may obstruct the market's growth over the forecast period. The process of hiring an MSP to host critical business infrastructure involves a belief in the providers' business relationship. In case of any failure by providers to sustain in the competitive market, enterprises relying upon them may have to entirely replace web hosting, emails, calendars, and other critical pieces of infrastructure, without which it is not possible to conduct business.

- The COVID-19 pandemic increased the number of organizations working remotely in the United States. According to ALM Media Properties LLC, an estimated 58% of American knowledge workers work remotely. This number is increasing by more than 30% from pre-COVID-19 averages and dwarfs previous figures that reported roughly 7% of the US' 140 million civilian employees worked from home. This mass exodus from the conventional workplace has been a welcome shift in many organizations' employer expectations and telework policies.

North America Managed Services Market Trends

IT and Telecom Sector Expected to Hold a Significant Market Share

- The IT and telecom sector is a significant market for managed services due to the high rate of various technological adoptions, increased rate of adoption of the BYOD policy (in order to make business operations much more comfortable and controllable), and increased need for high-end security due to rapidly increasing data volumes in organizations.

- The telecom industry has observed increased growth during the past few years as telecommunication companies are encountering constant pressure to deliver innovative services at lower costs to retain their customers in the competitive market. In order to address a complex and competitive environment, managed services have become a widespread demand for operators.

- Moreover, because of their compelling economic case, most telecom carriers are expected to replace their network hardware with software (SDN & NFV). Major factors driving the demand for SDN and NFV include improved time-to-market, reduction in CAPEX and OPEX, and opening up new revenue streams from a business standpoint. All these are expected to drive the growth of the market studied. Such initiatives are driving demand for managed network services.

- Many SD-WAN managed service providers in North America differentiate themselves with a broad range of security offerings. For instance, Cato Networks offers a cloud-native platform that includes NGFW, Secure Web Gateway, Advanced Threat Prevention, Cloud and Mobile Access Protection, and a Managed Threat Detection and Response service. Colt offers Layer 7 firewall or a Layer 3/4 stateful firewall with DDoS protection, and CenturyLink provides a suite of security services referred to as Adaptive Network Security.

Canada Expected to be the Fastest-growing Market

- The market for managed services in Canada is growing mainly due to new product roll-outs, acquisitions, mergers, and partnerships, shaping the overall North American market. The accelerated growth of technology in Canada continues to reshape how businesses improve operational efficiencies, leverage massive amounts of data, collaborate internally, and interaction between businesses and customers.

- Starport is a Canada-based managed IT services provider that delivers top-class IT design, implementation, and continuous network monitoring to mid-sized organizations, throughout Canada. Most of its clients are concentrated in the Greater Toronto Area. It offers its services to clients from various industries, including investment banking, manufacturing, and commercial real estate.

- Besides, Canada is witnessing high growth in the application of multi-cloud environments and increased adoption of automation. In the region, cloud, mobile, and social technologies demand that businesses take a proactive approach toward IT security, thus, boosting the demand for the deployment of robust managed services that would deliver in all security management layers.

- Unified Communications as a Service (UCaaS) and related Contact Center as a Service (CCaaS) markets represent a business opportunity for managed service providers. This is because emerging players are offering innovative cloud-based solutions that require a minimum investment and are easy to deploy. Customers are also leaning toward consumption-based, pay-as-you-go models.

- Rising cloud services in the country are expected to augment the demand for the managed MPLS market. For instance, the Government of Canada has a 'cloud-first' strategy, whereby cloud services are identified and evaluated as the principal delivery option while initiating information technology investments, initiatives, strategies, and projects. The cloud is also expected to allow the Government of Canada to harness the innovation of private sector providers to make its information technology more agile.

North America Managed Services Industry Overview

The managed services market is very competitive because of the presence of several major players. Some major players in the market are Cisco Systems Inc., IBM Corporation, Microsoft Corporation, Fujitsu Ltd, and Wipro Ltd. The market players are forming strategic collaborations and partnerships to sustain the intense competition in the market.

- May 2021 - Fujitsu Ltd and Rakuten Mobile Inc. announced a Memorandum of Understanding (MoU) to deepen their collaboration on joint efforts to develop Open RAN solutions for the global market. Both companies will jointly collaborate to develop 4G and 5G Open RAN solutions.

- November 2021 - AT&T added a new offering to its Secure Access Service Edge (SASE) portfolio. AT&T SASE with Cisco is a converged network and security management system that uses software-defined wide-area networking (SD-WAN) technology and security capabilities to connect and protect businesses.

- October 2021 - Citrix launched Citrix Secure Private Access, a new cloud-based Zero-Trust Network Access (ZTNA) solution that safeguards app and data access from managed, unmanaged, and Bring-Your-Own (BYO) devices.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Shift to Hybrid IT

- 5.1.2 Improved Cost and Operational Efficiency

- 5.2 Market Challenges

- 5.2.1 Integration, Regulatory Issues, and Reliability Concerns

6 MARKET SEGMENTATION

- 6.1 By Deployment

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.2 By Type

- 6.2.1 Managed Data Center

- 6.2.2 Managed Security

- 6.2.3 Managed Communications

- 6.2.4 Managed Network

- 6.2.5 Managed Infrastructure

- 6.2.6 Managed Mobility

- 6.3 By Enterprise Size

- 6.3.1 Small Enterprises

- 6.3.2 Medium Enterprises

- 6.3.3 Large Enterprises

- 6.4 By End-user Vertical

- 6.4.1 BFSI

- 6.4.2 IT and Telecom

- 6.4.3 Healthcare

- 6.4.4 Entertainment and Media

- 6.4.5 Retail

- 6.4.6 Manufacturing

- 6.4.7 Government

- 6.4.8 Other End-user Verticals

- 6.5 By Country

- 6.5.1 United States

- 6.5.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Fujitsu Ltd

- 7.1.2 Cisco Systems Inc.

- 7.1.3 IBM Corporation

- 7.1.4 AT&T Inc.

- 7.1.5 HP Development Company LP

- 7.1.6 Microsoft Corporation

- 7.1.7 Verizon Communications Inc.

- 7.1.8 Dell Technologies Inc.

- 7.1.9 Citrix Systems Inc.

- 7.1.10 Rackspace Inc.