|

시장보고서

상품코드

1690960

엔지니어링 서비스 아웃소싱 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Global Engineering Services Outsourcing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

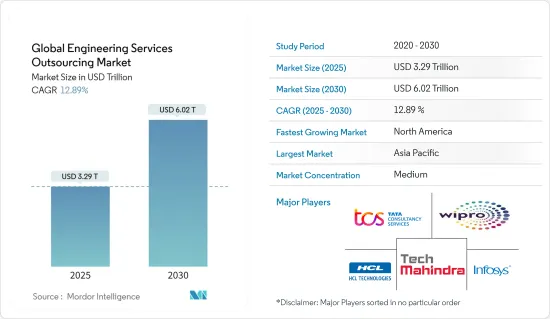

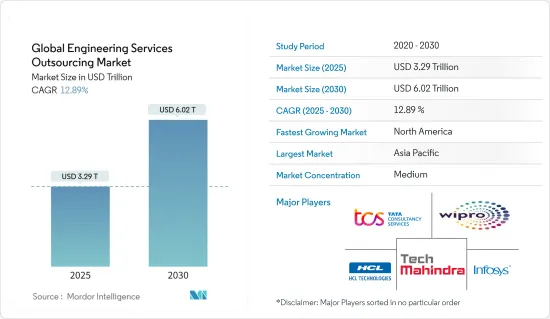

세계의 엔지니어링 서비스 아웃소싱 시장 규모는 2025년에 3조 2,900억 달러로 추정되고, 예측 기간 2025년부터 2030년까지 CAGR 12.89%로 성장할 전망이며, 2030년에는 6조 200억 달러에 달할 것으로 예측됩니다.

주요 하이라이트

- 연구개발 활동의 세계화, 제품제공에 있어서 최신기술 통합 수요 증가, 제품 수명주기의 단축 및 비용절감 요구 증가가 시장의 성장에 기여할 것으로 예상됩니다.

- COVID-19 팬데믹의 발생과 이어지는 세계 각국에서의 봉쇄 영향은 최종 이용 산업이나 업종에 따라 다릅니다. 산업시설, 제조공장, 대중교통은 감염 확대를 막기 위한 노력의 일환으로 일시적으로 폐쇄되었습니다.

- 폐쇄 규제 완화, 산업 기업 재개, 해외 무역 증가로 엔지니어링 서비스 아웃소싱 부문은 2021년 1분기부터 점차 회복하기 시작했습니다.

- 엔지니어링 서비스 아웃소싱(ESO)의 인기의 주요 요인 중 하나는 주문자 상표 부착 생산자(OEM)와 엔지니어링 서비스 공급자(ESP)의 협력 관계가 확대될 것으로 예상됩니다.

- 제품 수명 주기 단축과 비용 절감에 대한 요구 증가와 최신 기술을 도입한 제품 옵션에 대한 요구 증가는 모두 시장 확대를 뒷받침할 것으로 예상됩니다.

- 비용 절감의 일환으로 다양한 서비스를 아웃소싱하고 싶다는 소비자의 요구가 높아지고 있다는 것이 ESO 시장의 지속적인 성장으로 이어지고 있습니다.

- 자동화의 진전, 디지털화의 움직임, 인더스트리 4.0의 채택으로, 자동화된 엔지니어링 서비스 제공업체의 요구는 최근 극적으로 높아지고 있습니다. 현재 시장의 60% 이상을 차지하는 CNC 기계 시장은 예측 기간 동안 크게 성장할 전망입니다.

- 컴퓨터 지원 설계(CAD)와 제도는 가장 아웃소싱된 엔지니어링 서비스 중 하나입니다. 도면 조립, 전자 설계도 초안, 소프트웨어를 사용하여 상세도 작성, 3D 또는 2D 형식으로 변환 등의 작업이 이러한 서비스에 포함됩니다.

엔지니어링 서비스 아웃소싱 시장 동향

시장 성장을 견인하는 통합 솔루션 채택 증가

- 엔지니어링 시스템의 분석과 설계를 위한 통합 솔루션의 채택이 증가하고 있는 것 외에도 산업 자동화가 진행되고 있는 것이 시장 성장을 가속하는 주요 요인 중 하나가 되고 있습니다. 게다가 컴퓨터 지원 설계(CAD), 컴퓨터 지원 엔지니어링(CAE), 컴퓨터 지원 제조(CAM), 전자 설계 자동화(EDA) 소프트웨어 등의 엔지니어링 시스템의 이용이 확산되고 있는 것도 시장의 성장을 뒷받침하고 있습니다. 이 소프트웨어는 생산 공정의 전반적인 효율성을 높이는 데 도움이 되며 스마트폰, 노트북 및 태블릿 기기에서 사용자가 조작할 수 있습니다.

- 다양한 기술의 진보와 디지털 변혁 서비스의 도입도 성장을 가속하는 요인이 되고 있습니다. 기타, 자동차, 해양, 해양 분야에서의 전략적 아웃소싱 서비스의 이용 증가와 3D 프린팅 솔루션 시장 개척 등이 시장을 더욱 견인할 것으로 예상됩니다.

- 중소규모의 엔지니어링 서비스 제공업체들 사이에서 엔지니어링 서비스의 아웃소싱에 대한 선호도가 높아지고 있으며, 이러한 서비스에는 개념 설계부터 최종 제품 개발 및 검증에 이르는 신제품 도입, 프로세스 엔지니어링, 자동화, 기업 자산 관리, 전반적인 비즈니스 프로세스 강화 등이 포함됩니다. 이것은 세계 엔지니어링 서비스 아웃소싱 시장이 유리한 성장을 이루는 요인이 되고 있습니다.

- 무수한 유형의 기계 및 장비를 다루는 산업 기업은 그들을 조작하기 위해 상당한 노동력을 고용하는 부담을 가지고 있습니다. 또한 특히 엔지니어링 서비스와 같은 다양한 장비를 다루는 기업의 경우 모든 근로자와의 조정이 매우 복잡합니다.

- 이러한 기업의 경우 자동화는 최상의 솔루션이며 디지털화가 진행되는 세계에서 전진하는 방법입니다. 자동화는 비용을 삭감하고 일의 질을 증가합니다. 인간 작업자는 효율적이지만 실수를 하기 쉽기 때문에 프로세스와 작업을 자동화하여 실수를 방지할 수 있습니다.

- 또한 자동화를 통해 인간의 안전성을 향상시킵니다. 이러한 이점은 산업용 자동화 서비스를 아웃소싱할 가치가 있습니다. 산업용 자동화 서비스는 기업에 더 나은 인프라를 제공하고, 성능을 최적화하고, 보다 효율적으로 안전 문제를 해결하고, 궁극적으로 생산성을 향상시킵니다.

디지털 변혁 서비스와 함께 다양한 기술 개발

- 엔지니어링 서비스 아웃소싱 시장을 지원하는 주요 요인은 모빌리티 및 스마트 제품과 같은 파괴적인 기술의 출현으로 다양한 산업에 걸쳐 기술적 융합이 진행되고 있다는 것입니다. 산업 부문에 걸친 발자국을 가진 ESP는 관련성이 없는 업계 모범 사례와 기술을 채택하는 데 유리한 입장에 있습니다.

- AI, IoT, 디지털 트윈과 같은 디지털 기술은 지난 10년간 빠르게 성장했습니다. COVID-19의 발생은 산업과 지역을 가로지르는 디지털화의 물결을 일으켰습니다. 팬데믹 및 그 후의 영향은 기업의 디지털 변환의 여행을 가속화하는 계기가 되었습니다.

- 신속한 제품 개발, 전사적 커넥티비티, 고객 경험 리엔지니어링, 오퍼레이션 엑셀런스를 통해 자동차 및 항공우주 등 산업 부문 전체의 엔지니어링 프로세스를 최적화할 가능성을 지닌 디지털 인에이블러의 채용을 뒷받침했습니다. 기술 도입의 지연이 급속한 디지털 가속을 대체하는 가운데, 세계 기업은 점차 새로운 생태계에 적응하고 있습니다.

- 디지털 엔지니어링 능력은 기술의 민주화와 5G 네트워크의 출현으로 가속화되고 있습니다. 예를 들어 항공우주 산업에서는 디지털화를 통해 기체의 피팅 시간이 95% 단축되어 품질도 향상하고 있습니다. 인기있는 디지털 협업 도구의 시작은 엔지니어링 서비스 아웃소싱의 또 다른 성장 벡터로 분산을 도입했습니다. 엔지니어링 서비스 제공업체와 OEM의 협업 증가, 연구개발 활동의 세계화로 아웃소싱 활동이 활발해지고 있습니다.

- 엔지니어링 서비스 제공업체(ESP)가 핵심 엔지니어링 업무를 지원하게 됨으로써 기술을 활용한 원격 제품 개발 등의 활동에 특히 중점을 둔 오프쇼어링의 대처가 강화되고 있습니다. 아웃소싱과 관련하여 OEM, 공급업체 및 순수 소프트웨어 기업의 역할과 전문 지식을 결합한 업계 전반의 협력 체제를 수립함으로써 핵심 활동과 비중핵 활동 간의 경계가 모호해지고 있습니다.

- 지난 20년 동안 엔지니어링 서비스의 변화를 고려할 때 기술적 성장의 역할은 과장되지 않습니다. 최근 몇년만이라도 엔지니어링 집약형 분야에서는 IoT, 클라우드, 디지털 트윈 애널리틱스, 증강현실(AR/VR), AI 등 실현 가능한 기술의 등장을 눈에 띄고 있습니다.

- 유럽에서는 자동화, 애널리틱스, 사이버 보안, 서비스 등의 동향이 업계 전반에 걸쳐 관찰되고 있습니다. 제조 현장이 제어 시스템을 통해 엄청난 양의 데이터를 생성하는 동안 더 많은 기업들이 이 정보를 활용하여 복잡하고 충분한 정보를 기반으로 의사 결정을 내리는 이점을 실감하고 있습니다. IIoT는 머신 투 머신(M2M) 시스템, AI, 에지 애널리틱스, PLM/MES 시스템 전체를 호스팅할 수 있는 클라우드 솔루션 등의 기술을 통해 이를 가능하게 합니다.

엔지니어링 서비스 아웃소싱 업계 개요

세계의 엔지니어링 서비스 아웃소싱 시장은 세분화되어 경쟁이 치열합니다. 지난 10년간, 다양한 세계 엔지니어링 기업의 합병 및 제휴가 큰 동향이 되어, 시장에서의 발판을 굳히고 있습니다. 제조업의 신흥기업을 포함한 신흥기업 및 기타 업계 에코시스템 기업와의 제휴는 엔지니어링 서비스 아웃소싱 시장의 성장에 새로운 기회를 제공할 것으로 기대되고 있습니다. 기업은 연구개발 사업에 광범위하게 투자하고 고객에게 맞춤형 서비스를 제공하는 데 주력하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건

- 조사 범위

제2장 조사 방법

- 분석 방법

- 조사 단계

제3장 주요 요약

제4장 시장 인사이트

- 현재의 시장 시나리오

- 기술 동향

- 업계의 밸류체인 분석

- 정부의 규제 및 대처

- 원가계산에 관한 인사이트

- 시장에 대한 COVID-19의 영향

제5장 시장 역학

- 성장 촉진요인

- 성장 억제요인

- 기회

- 업계의 매력도-Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자 및 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제6장 시장 세분화

- 서비스별

- 설계

- 프로토타이핑

- 시스템 통합

- 테스팅

- 기타

- 최종 사용자별

- 자동차

- 산업

- 가전 및 반도체

- 통신

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 태국

- 인도네시아

- 기타 아시아태평양

- 세계 기타 지역

- 북미

제7장 경쟁 구도

- 기업 프로파일

- Tech Mahindra Limited

- Tata Consultancy Services Limited

- Infosys Limited

- HCL Technologies Limited

- Wipro Ltd.

- Capgemini Technology Services India Limited

- Globallogic Inc.

- Accenture

- RLE International Inc.

- ASAP Holding GmbH

- Tata Technologies*

제8장 시장의 미래

제9장 부록

AJY 25.04.09The Global Engineering Services Outsourcing Market size is estimated at USD 3.29 trillion in 2025, and is expected to reach USD 6.02 trillion by 2030, at a CAGR of 12.89% during the forecast period (2025-2030).

Key Highlights

- The globalization of R&D activities, the rising demand for integrating the latest technologies in product offerings, and the growing need to shorten the product lifecycles and cut costs are expected to contribute to the growth of the market.

- The impact of the outbreak of the COVID-19 pandemic and the subsequent lockdowns in various countries across the world varied depending on the end-use industries and industry verticals. Industrial facilities, manufacturing plants, and public transport were shut down temporarily as part of the efforts to arrest the spread of the disease.

- Due to the ease of lockdown restrictions, the reopening of industrial firms, and increased foreign trade, the Engineering Services Outsourcing sector began progressively recovering from the first quarter of 2021.

- One of the primary drivers of the expanding popularity of engineering services outsourcing (ESO) is expected to be the growing cooperation between Original Equipment Manufacturers (OEM) and Engineering Service Providers (ESP).

- The increasing need to shorten product lifecycles and cost-cutting and the rising desire for product options that incorporate the most outdated technology are all expected to support market expansion.

- The increasing desire among consumers to outsource various services as a part of cost-cutting initiatives has led to continuous growth in the ESO market.

- Due to increased automation, a move toward digitalization, and the adoption of Industry 4.0, the need for automated Engineering Service Providers has risen dramatically in recent years. The market for CNC machines, which currently accounts for more than 60% of the market, is expected to grow significantly over the forecast period.

- Computer-aided design (CAD) and drafting are among the most outsourced engineering services. Tasks such as assembling drawings, drafting electronic blueprints, and creating detailed illustrations using software and converting to 3D or 2D formats, are included in these services.

Engineering Services Outsourcing Market Trends

Rising Adoption of Integrated Solutions Driving the Growth of the Market

- Increasing industrial automation, along with the rising adoption of integrated solutions for analyzing and designing engineering systems, represents one of the key factors driving the growth of the market. Furthermore, the widespread utilization of engineering systems, such as computer-aided design (CAD), computer-aided engineering (CAE), computer-aided manufacturing (CAM), and electronic design automation (EDA) software, is also driving market growth. This software aid in enhancing the overall efficiencies of the production processes and can be operated by the user over smartphones, laptops, and tablets.

- Various technological advancements and the incorporation of digital transformational services are acting as other growth-inducing factors. Other factors, including the increasing utilization of strategic outsourcing services by the automotive, marine, and offshore sectors, along with the development of 3D printing solutions, are expected to drive the market further.

- There is a rise in preference for the outsourcing of engineering services among small and medium-sized engineering service providers, these services include, new product induction from conceptual design to final product development and validation, process engineering, automation, enterprise asset management, and overall business process enhancement. This attributes to witness lucrative growth of the global engineering services outsourcing market.

- Industrial firms that handle countless types of machinery and equipment have the burden of hiring a considerable workforce to operate them. It also gets very complicated to coordinate with all the workers, especially for companies that work with different equipment like engineering services.

- For such companies, automation is the best solution and way to advance in an increasingly digitized world.Automation reduces costs and enhances the quality of work. While human workers are efficient, they're prone to making errors that can be avoided when one automates the processes and operations.

- Automation also offers increased human safety. All these benefits make it worthwhile to outsource industrial automation services.Industrial automation and control services that empower companies to have better infrastructure and optimize their performance, address safety concerns more efficiently, and ultimately increase productivity.

Various Technical Developments Along With Digital Transformational Services

- A key factor behind the engineering services outsourcing market is the quantum of technological convergence across varied verticals due to the advent of disruptive technologies like Mobility and Smart Products, which are driving customers to a more connected world. ESPs with a footprint across industry segments are better positioned to adopt best practices and technologies from unrelated industries.

- Digital technologies such as AI, IoT, and digital twins have rapidly grown over the last decade. The onset of COVID-19 gave rise to waves of digitalization that swept across industries and geographies. The pandemic and its subsequent impact have catalyzed enterprises accelerating their digital transformation journeys.

- It boosted the adoption of digital enablers that have the potential to optimize engineering processes across industrial sectors like automotive and aerospace through rapid product development, enterprise-wide connectivity, re-engineering of customer experiences, and operational excellence. With the slow uptake of technology being replaced by rapid digital acceleration, global players are gradually adapting to the new ecosystem.

- Digital engineering capabilities are being accelerated by the democratization of technology and the advent of 5G networks. For example, in the aerospace industry, digitalization reduces fuselage splice times by 95% at a higher quality. The rise of digital collaboration tools during the pandemic has introduced decentralization as another growth vector for outsourcing engineering services. Increasing collaboration between engineering service providers and OEMs and the globalization of R&D activities have increased outsourcing activities.

- The growing involvement of engineering services providers (ESPs) in supporting core engineering practices has reinforced offshoring efforts with a particular focus on activities like remote product development using technologies. When it comes to outsourcing, the blurring of the line between core and non-core activities has been marked by establishing industry-wide collaboration frameworks that combine the role and expertise of OEMs, suppliers, and pure software players.

- When considering the transformation of engineering services during the last twenty years, the role of technological growth cannot be overstated. In the past few years alone, engineering-intensive sectors have witnessed the advent of enablers like IoT, cloud, digital twins, analytics, extended realities (AR/VR), and AI.

- In Europe, automation, analytics, cybersecurity, and servitization are some trends observed across industries. With the manufacturing shop floor generating incredible volumes of data through control systems, more and more organizations realize the benefit of harnessing this information to make complex and informed decisions. IIoT has enabled this with technologies like machine-to-machine (M2M) systems, AI, edge analytics, and cloud solutions capable of hosting entire PLM/MESsystems.

Engineering Services Outsourcing Industry Overview

Global Engineering Services Outsourcing Market is fragmented and competitive. A significant trend of mergers and alliances of various global engineering firms has been seen over the past decade to increase foothold in the market. Partnerships with start-up companies including manufacturing start-ups and other industry ecosystem players are expected to provide new opportunities for the growth of the Engineering Services Outsourcing Market. Companies are extensively investing in R&D operations and are focusing on providing customized services to their customers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Technological Trends

- 4.3 Industry Value Chain Analysis

- 4.4 Government Regulations and Initiatives

- 4.5 Insights on Costing

- 4.6 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Drivers

- 5.2 Restraints

- 5.3 Opportunities

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Consumers / Buyers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION (Market Size by value)

- 6.1 By Services

- 6.1.1 Designing

- 6.1.2 Prototyping

- 6.1.3 System Integration

- 6.1.4 Testing

- 6.1.5 Others

- 6.2 By End User

- 6.2.1 Automotive

- 6.2.2 Industrial

- 6.2.3 Consumer Electronics And Semiconductors

- 6.2.4 Telecom

- 6.2.5 Others

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.1.3 Mexico

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Italy

- 6.3.2.5 Spain

- 6.3.2.6 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 Japan

- 6.3.3.4 South Korea

- 6.3.3.5 Thailand

- 6.3.3.6 Indonesia

- 6.3.3.7 Rest of Asia-pacific

- 6.3.4 Rest of the World

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Overview (Market Concentration and Major Players)

- 7.2 Company Profiles

- 7.2.1 Tech Mahindra Limited

- 7.2.2 Tata Consultancy Services Limited

- 7.2.3 Infosys Limited

- 7.2.4 HCL Technologies Limited

- 7.2.5 Wipro Ltd.

- 7.2.6 Capgemini Technology Services India Limited

- 7.2.7 Globallogic Inc.

- 7.2.8 Accenture

- 7.2.9 RLE International Inc.

- 7.2.10 ASAP Holding GmbH

- 7.2.11 Tata Technologies*