|

시장보고서

상품코드

1692159

가속도 및 요레이트(Yaw Rate) 센서 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Acceleration And Yaw Rate Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

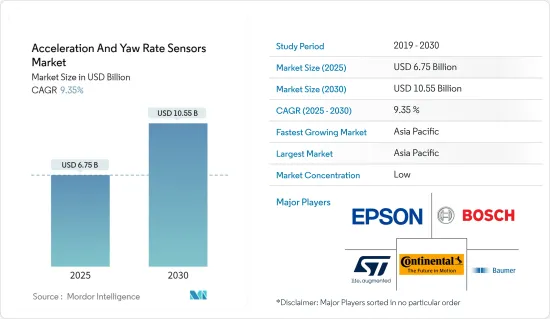

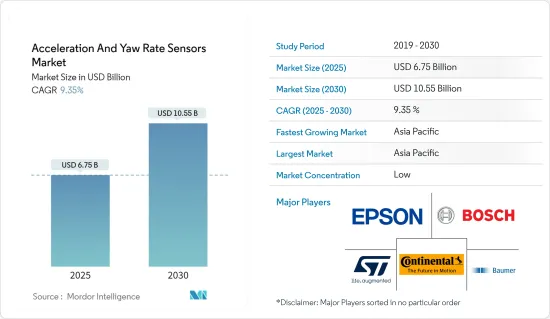

가속 및 요레이트(Yaw Rate) 센서 시장 규모는 2025년에 67억 5,000만 달러, 2030년에는 105억 5,000만 달러에 도달할 것으로 예측됩니다. 예측 기간(2025-2030년)의 CAGR은 9.35%를 나타낼 전망입니다.

요레이트(Yaw Rate) 센서는 차량의 수직축을 중심으로 회전을 측정하는 동시에 주행 방향과 직각 방향의 가속도를 측정합니다. 요레이트는 초당 몇 번 단위로 측정됩니다. 차량이 2초 안에 900회전하면 요레이트(Yaw Rate)은 450이 됩니다. 센서는 측정값을 전자적으로 평가하여 일반 코너링과 차량의 횡방향 미끄러짐 움직임을 구별할 수 있습니다.

주요 하이라이트

- 요레이트(Yaw Rate) 센서는 차량의 수직축 주위의 각도 운동을 감지하는 자이로스코프 가젯입니다. 출력은 보통 초당 도수 또는 라디안 단위로 표현됩니다. 요레이트(Yaw Rate)와 관련된 슬립 각도는 차량의 주행 방향과 자연 방향 사이에 형성된 각도입니다. 이 값을 계산하려면 코리올리 효과가 사용됩니다. 코리올리 효과는 정확한 측정과 결과를 제공합니다. 따라서 시장의 우위를 유지할 것으로 예상됩니다. 코리올리 가속도는 마이크로 기계식 진동 요소의 마이크로 기계식 캡처 가속도 센서를 통해 감지됩니다. 가속도는 요레이트(Yaw Rate)과 진동 속도의 곱에 비례하며 전자적으로 유지됩니다.

- ADAS(선진 운전 지원 시스템)와 커넥티드 차량 기술의 인기가 높아지고 있는 것은 자동차의 안전성, 보안, 쾌적성의 향상을 요구하는 소비자 요구의 높아짐이 배경에 있습니다. ADAS(첨단 운전 지원 시스템)는 센서, 카메라, 통신 시스템을 통합하고 다양한 상황에서 운전자를 지원함으로써 운전 경험의 변화에 기여합니다.

- 수요의 급증은 충돌 회피와 차선 유지 지원 등의 기능으로 안전을 우선시하고, 개선된 네비게이션, 실시간 정보, 개인화된 쾌적성 설정을 위한 커넥티비티를 제공하는 자동차에 대한 집단적 욕구를 반영하고 있습니다. 이러한 추세는 보다 똑똑하고 안전한 운전 환경을 추구하는 소비자의 기대가 진화하고 있음을 돋보이게 합니다.

- 최근 기후 변화와 싸우고 온실가스(GHG) 배출을 줄이려는 소비자의 소원으로부터 대체연료차에 대한 관심과 기호가 현저하게 높아지고 있습니다. 이 교대는 보다 지속가능하고 환경친화적인 교통수단으로 가는 큰 단계입니다.

- 자동차 업계에서는 첨단 센서 기술에 대한 수요가 급증하고 자동차가 스마트 시스템으로 변모하고 있습니다. 선진 경제 국가들은 이러한 진화를 받아들이고 있지만, 신흥 경제 국가의 자동차 센서의 애프터마켓은 가속 및 요레이트(Yaw Rate) 센서의 성장을 방해할 수 있는 독특한 과제에 직면하고 있습니다. 주요 장애물 중 하나는 신흥 국가 애프터마켓 인프라가 개발되지 않은 것입니다. 신흥국 시장은 선진국 시장과는 달리 센서 전문 서비스 제공업체의 견고한 네트워크가 정비되어 있지 않은 경우가 많아, 고품질의 센서 교환이나 적시의 메인터넌스 서비스의 제공이 방해되고 있습니다.

가속 및 요레이트(Yaw Rate) 센서 시장 동향

승용차가 큰 시장 점유율을 차지

- 승용차의 개발이 진행됨에 따라 자동차의 안전기능에 대한 수요가 높아짐에 따라 가속 및 요레이트(Yaw Rate) 센서 수요가 높아지고 있습니다. 이 센서는 가장 어려운 운전 조건 하에서도 보안, 안전성 및 제어성을 향상시키는 자동차 안정 제어의 주요 구성 요소입니다. 이러한 센서는 에어백, 트랙션 컨트롤, ADAS(첨단 운전 지원 시스템), 충돌 회피 시스템 등 수많은 안전 기능에 사용되고 있습니다.

- 승용차의 요 레이트 센서는 차량의 회전 속도(종종 요 레이트라고 함)를 측정하는 데 사용됩니다. 이 데이터는 전자 안정성 제어(ESC) 및 트랙션 제어와 같은 안정성 제어 시스템에 필수적이며 작동의 기초입니다. 또한 차량 성능 문제를 진단하고 운전 지원 시스템에 데이터를 제공하는 데에도 도움이 됩니다.

- 특히 소형 승용차에서는 자율주행이나 자동차의 전동화 등 동향의 도입으로 이 시장은 높은 성장이 전망되고 있습니다. 이러한 수요 증가에 대응하기 위해, 자동차 제조업체의 각 사는 입지를 넓히고 시장 경쟁력을 높이기 위한 투자나 신차종의 투입에 주력하고 있습니다. Scotiabank에 따르면 아시아에서는 2023년 승용차 판매량이 약 3,650만대에 달했고, 북미에서는 1,830만대에 달했습니다.

- 2023년 5월 BYD는 유럽에서 승용차 신공장 설립을 발표했습니다. 또한 성장 전략의 일환으로 태국에 승용차 공장을 건설할 예정입니다.

- 마찬가지로 스즈키 주식회사는 2023년 10월 단독으로 최대 시장인 인도에서 2030년까지 300만대의 승용차 판매를 목표로 한다고 발표하고 향후 10년간 인도에서 생산능력을 400만대로 배가할 계획을 재차 표명했습니다.

- 게다가 세계 정부와 소비자가 전기차에 대한 지출을 늘리고 있으며, 지역 정부는 전기차 도입을 촉진하기 위해 구매 보조금과 면세 조치를 제공합니다. 또한 다양한 정부가 충전 인프라에 지출함으로써 전동화 계획을 가속화하고 완전한 전기자동차의 미래를 목표로 시장의 성장을 지원하고 있습니다.

아시아태평양이 큰 시장 점유율을 차지할 전망

- 중국 자동차 산업은 최근 동향에서 현저한 성장과 개발을 이루고 있습니다. 중국의 자동차 산업은 세계 최대의 EV 시장과 산업을 가지고 있으며, 견고한 공급망과 중요한 연구 개발 활동이 있습니다. 중국 정부는 자동차 부품 부문을 포함한 자동차 산업을 돌출한 산업 중 하나로 간주합니다. 중앙정부는 중국의 자동차 생산량이 2025년까지 3,500만대에 달할 것으로 전망하고 있습니다. 중국은 최근 2030년까지 전기자동차(EV)를 기존 자동차보다 40% 더 판매하도록 자동차 제조업체에 지시했습니다. 자동차 산업의 이러한 발전으로 연구 대상 시장의 성장이 예상됩니다.

- 또한 Industry 4.0과 IoT의 수용을 통한 제조업의 대규모 이동으로 인해 기업은 인간노동을 자동화로 보완 및 확장하고 프로세스 실패로 인한 산업사고를 줄이는 기술로 생산을 진행하기 위한 민첩하고 스마트하고 혁신적인 방법을 채택해야 합니다. 중국의 자동차 부문은 생산량을 늘리고 제품의 적합성과 마무리 수준을 높이고 전반적인 비용을 줄이기 위해 첨단 제조 기술을 크게 채택해 왔습니다. 중국의 자동차 부문 성장은 이 시장의 성장을 지원할 것으로 예상됩니다.

- 또한 중국 자동차공업협회(CAAM)에 따르면 2022년에는 중국에서 승용차가 약 2,384만대, 상용차가 약 319만대 생산되었습니다.

- IBEF의 자동차 산업 보고서에 따르면 인도에서는 중산 계급 인구가 증가하고 있으며 인구의 상당한 비율이 젊은 층이기 때문에 이륜차 부문이 대수 기준으로 시장을 독점하고 있습니다. 또한, 지방시장 조사에 대한 기업의 관심이 높아지면서 이 분야의 성장을 더욱 강화하고 있습니다. 물류 및 여객 수송 산업의 성장은 상용차 수요를 견인하고 있습니다. 향후 시장 성장은 자동차의 전동화, 특히 소형 승용차 및 삼륜차의 전동화와 같은 새로운 동향에 의해 촉진될 것으로 예상됩니다.

- 인도는 세계 최대의 트랙터 제조업체, 세계 2위의 버스 제조업체, 세계 3위의 대형 트럭 제조업체이기 때문에 세계 대형 자동차 시장에서 강력한 지위를 누리고 있습니다. 22년도 인도의 연간 자동차 생산 대수는 약 2,293만대였습니다.

- 인도는 주요 자동차 수출국이기도 하며 예측기간 동안 수출이 크게 증가할 것으로 예상됩니다. 또한 인도 시장에서의 스크랩 정책, Automotive Mission Plan 2026, 생산에 연동된 인센티브 제도 등 인도 정부의 일부 이니셔티브는 인도를 이륜차 및 사륜차 시장에서 유력한 선수로 만들 가능성이 높습니다.

가속 및 요레이트(Yaw Rate) 센서 시장 개요

가속 및 요레이트(Yaw Rate) 센서 시장은 매우 세분화되어 있으며 Epson Europe Electronics Gmbh(세이코 엡손 주식회사), Bosch Sensortec Gmbh(로버트 보쉬 주식회사), STMicroelectronics NV, Continental AG, Baumer Group 등 주요 기업이 존재합니다. 이 시장의 기업은 제품 라인업을 강화하고 지속 가능한 경쟁 우위를 얻기 위해 제휴 및 인수와 같은 전략을 채택하고 있습니다.

- 2023년 9월 - Intergeo 2023에서 Silicon Sensing 팀은 견고하고 고성능의 관성 시스템 및 미세 전기 기계 시스템(MEMS)을 기반으로 한 다양한 센서의 최신 라인업을 전시했습니다. 게다가 신세대 시장 투입이 가까이 다가온 기술에 대해서도 논의를 나누었습니다. 이러한 최첨단 MEMS 기반 시스템과 센서는 중요한 영역에서 더 크고 무거우며 고가의 광섬유 자이로스코프(FOG) 장치에 필적하는 성능 수준을 제공합니다.

- 2023년 8월 - DTS는 남부 캘리포니아에서 최고급 직장으로 표창됩니다. 이 영광스러운 수상은 DTS의 흔들림 없는 헌신적인 노력과 한 사람 한 사람이 중요한 역할을 하는 협력적인 환경의 양성이 평가된 것입니다. 게다가 이 업적은 사회에 가치를 가져다주는 획기적인 제품 개발, 팀원들 사이의 동료 의식 육성, 개인 성장 촉진, 긍정적인 분위기 양성이라는 DTS의 기본 이념을 더욱 견고하게 하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 업계의 매력도 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

- 업계 공급망 분석

제5장 시장 역학

- 시장 성장 촉진요인

- 자동차의 안전, 보안, 쾌적성에 대한 소비자 수요의 급증

- GHG 배출량 저감을 목적으로 한 대체 연료 자동차에의 소비자의 경사의 고조

- 시장 성장 억제요인

- 신흥국에서의 자동차용 센서의 애프터마켓의 미발달

제6장 시장 세분화

- 유형별

- 압전 유형

- 마이크로 메카니컬 유형

- 용도별

- 항공우주

- 자동차

- 승용차

- 소형 상용차

- 대형 상용차

- 지역별

- 북미

- 유럽

- 아시아

- 호주 및 뉴질랜드

- 라틴아메리카

- 중동 및 아프리카

제7장 경쟁 구도

- 기업 프로파일

- Epson Europe Electronics GmbH(Seiko Epson Corporation)

- Bosch Sensortec GmbH(Robert Bosch GmbH)

- STMicroelectronics NV

- Continental AG

- Baumer Holding AG

- DIS Sensors BV

- Silicon Sensing Systems Ltd

- Xsens Technologies BV

- Diversified Technical Systems Inc.

- MEMSIC Semiconductor(Tianjin) Co. Ltd

- CTS Corporation

제8장 투자 분석

제9장 시장의 미래

SHW 25.04.09The Acceleration And Yaw Rate Sensors Market size is estimated at USD 6.75 billion in 2025, and is expected to reach USD 10.55 billion by 2030, at a CAGR of 9.35% during the forecast period (2025-2030).

A yaw rate sensor measures the vehicle's rotation around its vertical axis while measuring the acceleration at right angles to the driving direction at the same time. The yaw rate is measured in degrees per second. If a vehicle makes a 900 turn in two seconds, it will have a yaw rate of 450. The sensor can differentiate between normal cornering and vehicle skidding movements by electronically evaluating the measured values.

Key Highlights

- A yaw rate sensor is a gyroscope gadget that detects a vehicle's angular motion around its vertical axis. The output is usually expressed in degrees per second or radians per second. The slip angle, related to the yaw rate, is the angle formed between the vehicle's driving and natural direction. The Coriolis effect is used to calculate this value. The Coriolis effect provides precise readings and results. Thus, it is projected to maintain its market dominance. Coriolis acceleration is sensed through a micromechanical capture acceleration sensor on the oscillating element in the micromechanical type. The acceleration is proportional to the product of the yaw rate and the oscillation speed, which is maintained electronically.

- The growing popularity of advanced driver assistance systems (ADAS) and connected vehicle technology is propelled by heightened consumer demand for enhanced safety, security, and comfort in automobiles. As these technologies advance, they contribute to a transformative driving experience by integrating sensors, cameras, and communication systems to assist drivers in various situations.

- The surge in demand reflects a collective desire for vehicles that prioritize safety with features like collision avoidance and lane-keeping assistance and offer connectivity for improved navigation, real-time information, and personalized comfort settings. This trend underscores the evolving expectations of consumers who seek a more smart and secure driving environment.

- In recent years, there has been a notable surge in consumer interest and preference for alternative fuel vehicles, driven by a collective desire to combat climate change and reduce greenhouse gas (GHG) emissions. The shift marks a significant step toward a more sustainable and eco-friendly transportation landscape.

- The automotive industry has witnessed a surge in the demand for advanced sensor technologies, transforming vehicles into smart systems. While developed economies have embraced this evolution, the aftermarket for automotive sensors in emerging economies faces unique challenges that may impede the growth of acceleration and yaw rate sensors. One of the primary hurdles lies in the underdeveloped nature of the aftermarket infrastructure in emerging economies. Unlike their developed counterparts, these markets often lack a robust network of specialized sensor service providers, hindering the availability of quality sensor replacements and timely maintenance services.

Acceleration And Yaw Rate Sensors Market Trends

Passenger Cars to Hold Major Market Share

- The growing developments of passenger vehicles and rising demand for safety features in cars have fueled the demand for acceleration and yaw rate sensors. These sensors are key components in a vehicle's stability control to provide increased security, safety, and control even in the most difficult driving conditions. These sensors are used in numerous safety features such as airbags, traction control, advanced driver assistance systems (ADAS), collision avoidance systems, and others.

- The yaw rate sensor in passenger cars is used to measure the rotational speed of a vehicle, often referred to as the yaw rate. This data is essential for stability control systems, such as electronic stability control (ESC) and traction control, as it provides the basis for their operation. They are also helpful in diagnosing vehicle performance issues and providing data for driver assistance systems.

- The market is expected to witness high growth due to the introduction of trends such as autonomous driving and the electrification of vehicles, particularly in small passenger automobiles. To meet this growing demand, various automaker players focus on investing and introducing new vehicle models to expand their footprint and gain a competitive edge in the market. According to Scotiabank, in Asia, passenger car sales reached around 36.5 million units in 2023, and in North America, it reached 18.3 million units.

- In May 2023, BYD announced the establishment of a new passenger vehicle plant in Europe. The company is also planning to construct a vehicle plant in Thailand as a part of its growth strategy.

- Similarly, in October 2023, Suzuki Motor Corporation announced that it is targeting the sales of 3 million passenger vehicles in India, its single-largest market, by 2030, reiterating its plans to double its manufacturing capacity in the country to 4 million units over the next decade.

- Furthermore, governments and consumers around the globe are increasing their spending on electric cars, and regional governments are also providing purchase subsidies and tax waivers to promote the adoption of electric vehicles. Various governments are also spending on charging infrastructure to accelerate electrification plans and aiming for a fully electric future, thus supporting the market's growth.

Asia-Pacific is Expected to Hold Significant Market Share

- The automotive industry in China has experienced significant growth and development in recent years. The Chinese industry has the largest EV market and industry in the world, with a robust supply chain and significant research and development activities. The Chinese government views its automotive industry, including the auto parts sector, as one of the prominent industries. The central government expects China's automobile output to reach 35 million units by 2025. China recently instructed automakers to sell 40% more electric vehicles (EVs) than conventional vehicles by 2030. As a result of these advancements in the automotive industry, there is likely to be growth in the market studied.

- Moreover, massive shifts in manufacturing due to Industry 4.0 and the acceptance of IoT require enterprises to adopt agile, smarter, and innovative ways to advance production, with technologies that complement and augment human labor with automation and reduce industrial accidents caused by process failure. The automotive sector in China has been a significant adopter of advanced manufacturing techniques for increasing their production output, achieving higher levels of fit and finish for their products, and reducing overall costs. The growing automotive sector in China is anticipated to support the growth of the market studied.

- Further, according to the China Association of Automobile Manufacturers(CAAM), in 2022, approximately 23.84 million passenger cars and 3.19 million commercial vehicles were produced in China.

- According to the IBEF automobile industry report, the two-wheelers segment dominates the market in terms of volume due to a growing middle-class population, and a considerable percentage of India's population is young. Moreover, the rising interest of companies in examining the rural markets is further aiding the sector's growth. The growing logistics and passenger transportation industries are driving the demand for commercial vehicles. Future market growth is expected to be fueled by new trends, including the electrification of vehicles, particularly small passenger automobiles and three-wheelers.

- India also enjoys a powerful position in the global heavy vehicles market as it is the largest tractor manufacturer, second-largest bus producer, and third-largest heavy truck manufacturer globally. India's annual production of automobiles in FY22 was approximately 22.93 million vehicles.

- India is also a major auto exporter and has substantial export growth expectations for the forecast period. Additionally, several initiatives by the Government of India, like the scrappage policy, Automotive Mission Plan 2026, and production-linked incentive schemes in the Indian market, are likely to make India a prominent player in the two-wheeler and four-wheeler markets.

Acceleration And Yaw Rate Sensors Market Overview

The acceleration and yaw rate sensors market is highly fragmented, with the presence of major players like Epson Europe Electronics Gmbh (Seiko Epson Corporation), Bosch Sensortec Gmbh (Robert Bosch Gmbh), STMicroelectronics NV, Continental AG, and Baumer Group. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- September 2023 - During Intergeo 2023, the Silicon Sensing team showcased the latest lineup of robust and high-performing inertial systems and a variety of sensors based on micro-electro-mechanical systems (MEMS). Additionally, they engaged in discussions regarding the imminent market-ready technology of a new generation. These cutting-edge MEMS-based systems and sensors provide comparable performance levels to larger, heavier, and more expensive fiber optic gyroscope (FOG) units in crucial domains.

- August 2023 - DTS received the accolade of being acknowledged as one of the top workplaces in Southern California. This acknowledgment serves as a testament to DTS's unwavering dedication to fostering a collaborative environment where every individual has played a significant role in achieving this esteemed recognition. Furthermore, this achievement reinforces DTS's core principles of developing groundbreaking products that bring value to society, nurturing a sense of camaraderie among team members, promoting personal growth, and cultivating a positive atmosphere.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Degree of Competition

- 4.3 Industry Supply Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Surging Consumer Demand for Vehicle Safety, Security, and Comfort

- 5.1.2 Growing Inclination of Consumers Toward Alternative Fuel Vehicles to Reduce GHG Emissions

- 5.2 Market Restraints

- 5.2.1 Underdeveloped Aftermarket for Automotive Sensors in Emerging Economies

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Piezoelectric Type

- 6.1.2 Micromechanical Type

- 6.2 By Application

- 6.2.1 Aerospace

- 6.2.2 Automotive

- 6.2.2.1 Passenger Cars

- 6.2.2.2 Light Commercial Vehicles

- 6.2.2.3 Heavy Commercial Vehicles

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Epson Europe Electronics GmbH (Seiko Epson Corporation)

- 7.1.2 Bosch Sensortec GmbH (Robert Bosch GmbH)

- 7.1.3 STMicroelectronics NV

- 7.1.4 Continental AG

- 7.1.5 Baumer Holding AG

- 7.1.6 DIS Sensors BV

- 7.1.7 Silicon Sensing Systems Ltd

- 7.1.8 Xsens Technologies BV

- 7.1.9 Diversified Technical Systems Inc.

- 7.1.10 MEMSIC Semiconductor (Tianjin) Co. Ltd

- 7.1.11 CTS Corporation