|

시장보고서

상품코드

1911453

전기 드라이브 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Electric Drives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

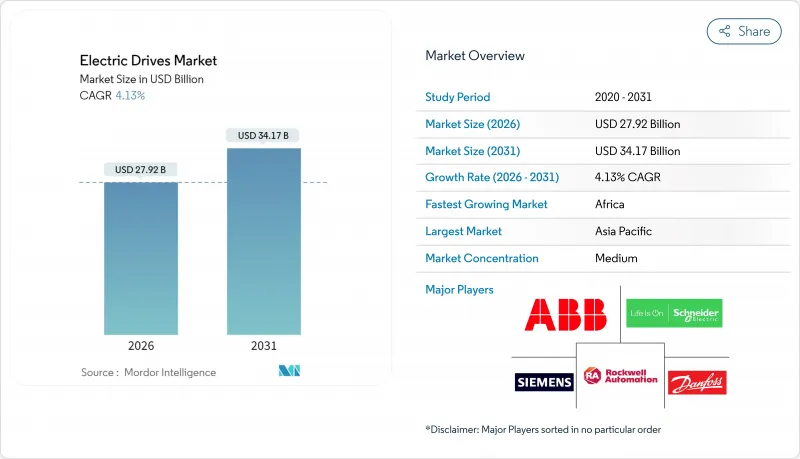

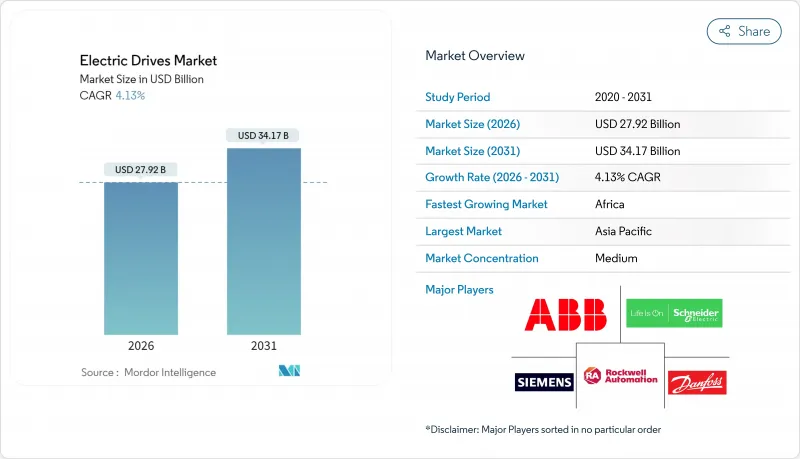

2026년 전기 드라이브 시장 규모는 279억 2,000만 달러로 추정되며, 2025년 268억 1,000만 달러에서 증가한 수치입니다.

2031년까지 341억 7,000만 달러에 달하고, 2026-2031년에 걸쳐 CAGR4.13%로 확대될 전망입니다.

성장은 세 개의 기둥에 의해 지원됩니다. 가변속 채택을 추진하는 의무적인 효율화 규제, 고정밀도의 동작을 요구하는 전동 모빌리티 라인, 광열비 삭감을 목적으로 한 기존 설비의 개수입니다. 아시아태평양은 중국의 공장 규모와 인도의 확대하는 산업 기반으로 2024년 45.64%의 수익 점유율로 선두를 차지했습니다. 한편 아프리카는 광업과 인프라 투자를 배경으로 5.46%라는 가장 빠른 CAGR을 기록하고 있습니다. 출하 대수에서는 교류 유닛이 71.13%의 점유율로 대부분을 차지하지만, 서보 드라이브는 4.47%의 연평균 복합 성장률(CAGR)로 가장 급속하게 성장하고 있어, 이것은 디스크리트 제조업에 있어서의 미크론 단위의 위치 결정 요구를 반영하고 있습니다. 또한 중공업 사업자가 컴프레서나 펌프 설비를 현대화하는 움직임에 따라 중전압 프로젝트도 4.81%의 연평균 복합 성장률(CAGR)로 페이스를 올리고 있습니다.

세계 전기 드라이브 시장 동향과 인사이트

세계와 각국의 엄격한 에너지 효율 규제

미국, 유럽, 중국의 신규제는 모터의 최저 효율 기준을 인상하고 에너지 집약형 플랜트에 가변속 드라이브 장치의 도입을 사실상 의무화하고 있습니다. 산업 감사는 제조 전력의 최대 70%를 모터가 소비하고 있는 것으로 밝혀졌고, 고정 속도 스타터의 교환에 의해 대폭적인 이산화탄소 배출량 감축과 비용 절감을 실현합니다. 정부는 현재 인증된 드라이브 장치에 대한 개수 실적과 세제우대조치 및 보조금 프로그램을 연동시키고 있으며, 이에 따라 인증제품 수요가 예측 가능해지고 있습니다. 벤더는 이에 대응하고, 3년 이하의 투자 회수를 정량화하는 에너지 평가 소프트웨어를 드라이브에 동고하고 있습니다. 그 결과, 전기 드라이브 시장은 시책 시행에 뒷받침된 지속적인 갱신 사이클을 획득하고 있습니다.

고정밀 드라이브가 필요한 전동 이동성 생산 라인의 가속

전기자동차 공장의 배터리 조립, 모터 권선, 품질 관리 스테이션에서는 0.1mm 이하의 재현성이 요구되고 서보 드라이브가 라인 설계의 핵심을 담당하고 있습니다. 자동차 제조업체는 전동화에 1,000억 달러 이상을 투자하고 있으며, 신규 공장에서는 첫날부터 고도 모션 포장이 지정되어 있습니다. 기존의 내연기관 공장에 있어서의 개수 공사에 있어서도, 기존 컨베이어가 서보 베이스 연질 셀로 옮겨지고 있습니다. 서보 벤더는 통합 안전 기능과 분산형 I/O를 추가하여 협동 로봇 연계를 간소화함으로써 플러그 앤 플레이 도입을 가속화하고 있습니다. 이러한 지속적인 자본 유입으로 인해 전기 드라이브 시장은 전자 이동성 투자의 주요 수혜자로서 확고한 지위를 구축하고 있습니다.

고정 속도 대체품과의 초기 설비 투자액 비교

가변속 드라이브는 컨택터 시동장치의 3-5배의 비용이 들기 때문에 자금 반복이 어려운 공장에서는 설비 투자가 장벽이 됩니다. 3년 이하의 회수기간은 재무에 익숙한 사업자에게는 매력적이지만, 전력이 보조되는 경우, 많은 사업자는 여전히 업그레이드를 선전합니다. 절대 절약액이 겸손한 15kW 이하의 영역에서는 이 우려가 현저하고, 손익 분기점까지의 기간이 장기화합니다. 드라이브리스와 에너지 서비스 등의 자금 조달 수단은 출현하고 있습니다만, 북미와 서유럽 이외에서는 여전히 한정되어 있습니다. 시간이 지남에 따라 반도체 가격 하락과 전력 회사 인센티브가 장벽을 완화하고 전기 드라이브 시장의 잠재 수요를 확대 할 수 있습니다.

부문 분석

2025년 시점에서 AC 드라이브는 전기 드라이브 시장의 70.62%를 차지했고, 세계 공장 자동화의 기반이 되는 펌프, 팬, 컨베이어 라인의 범용성을 반영하고 있습니다. 표준화된 인터페이스, 성숙한 부품 공급망 및 설치업체의 광범위한 지식이 수요를 지원하며, 특히 신뢰성이 최첨단 성능을 능가하는 식품 가공 및 수도 유틸리티 부문에서 두드러집니다. 예측기간동안 전력회사에 의한 원심기기의 효율목표 강화에 따라 전기 드라이브 시장은 기본 모터 제어에 있어서 계속해서 AC 플랫폼에 의존할 전망입니다. 서보 드라이브는 배터리·전자기기·의료기기 조립에 있어서의 서브 마이크로미터 단위의 위치 결정을 필요로 하는 개별 제조 공장 수요에 의해 2031년까지 연평균 복합 성장률(CAGR)4.25%로 가장 성장이 빠른 틈새 시장으로 계속하고 있습니다. 서보 벤더는 현재 통합 안전 기능과 원케이블 네트워크를 번들로 하여 상품화된 AC 유닛과의 차별화를 도모하고 있습니다.

서보 알고리즘이 하이 엔드 AC 패키징으로 전환하는 기술 크로스 오버로 인해 전기 드라이브 시장은 혜택을 누리고 있습니다. 이로 인해 기존 제품 라인의 경계가 모호해지는 반면 중견 사용자를 위한 비용 곡선은 매력적인 수준을 유지하고 있습니다. 금속 및 광업 부문에서 과거 주류였던 DC 드라이브는 현대의 AC 벡터 제어가 보다 낮은 보수 비용으로 동등한 토크 정밀도를 실현했기 때문에 축소 경향이 있습니다. 그러나 레거시 호환성에서 압연기 사업자의 일부는 여전히 DC 유닛을 지정하고 있으며 소규모 업데이트 수요를 창출하고 있습니다. 단일 랙 내에 AC, 서보, DC 축을 통합하는 멀티 드라이브 플랫폼이 주목을 받고 있습니다. 특히 모션 클래스를 가로 지르는 통합 프로그래밍을 중시하는 기계 제조업체 OEM에서 두드러집니다. 이 융합은 주요 공급업체의 라이프사이클 서비스 수익을 뒷받침하고 전기 드라이브 시장 전체에서 중간 정도의 집중화를 강화하고 있습니다.

1kV 이하의 저전압 시스템은 2025년 수익의 62.98%를 차지했고 공장 펌프, 압축기 및 자재관리 라인의 대부분을 지원합니다. 설치의 간편성, 몰드 케이스 보호장치의 용이한 이용가능성, 기술자의 스킬셋의 보급에 의해 총소유비용이 낮게 억제되고, 전기 드라이브 시장이 표준 제조 부문에서 저전압을 중심으로 하는 것이 보증되고 있습니다. 그러나 성장은 중전압 설비에 편향되어 중공업 사업자가 대형 모터를 가변속 운전으로 업그레이드하는 움직임에 따라 2031년까지 연평균 복합 성장률(CAGR) 4.62%로 확대될 것으로 예측되고 있습니다.

중전압 프로젝트는 보통 기존 설비의 증설(브라운필드)이나 LNG 플랜트, 시멘트 공장, 해수담수화플랜트에 대한 신규투자(그린필드)에 있어서 펌프나 컴프레서의 소비전력이 2MW를 넘는 경우에 부상합니다. 사업자는 여러 개의 저전압 모터를 병렬 운전하는 경우에 비해 역률을 개선하고 케이블 손실을 줄일 수 있으므로 이러한 솔루션을 선호합니다. 준2레벨 인버터 구성, 실리콘 카바이드 디바이스 및 회생 기능은 현재 프리미엄 중간 전압 포장의 차별화 요인이 되어 공급업체가 더 높은 마진을 정당화하는 데 도움이 됩니다. 고조파 억제 및 계통 지원 모드와 같은 전력 회사 연계 기능은 광산 및 원격 유전의 신흥 마이크로그리드 계획과 일치하여 내 장해성의 가치를 높입니다. 그 결과, 모터 시장은 양극화가 진행되고 있습니다. 상용화된 저전압 제품은 규모를 유지하는 반면, 기술적으로 고도의 중간 전압 장치는 불균형한 이익을 창출합니다.

지역별 분석

2025년에도 아시아태평양은 전기 드라이브 시장에서 최대 점유율(45.10%)을 유지했습니다. 이는 중국의 2024년 500억 달러 규모의 자동화 투자와 인도 인센티브를 배경으로 공장 건설 확대에 뒷받침된 것입니다. 중국 기업은 최신 에너지 강도 규제를 충족하기 위해 기존 스타터에서 가변 속도 포장으로 대체를 계속. 나가에 델타 지역의 배터리 기가 팩토리 집적지에서는 서보 채택이 가속하고 있습니다. 인도의 생산 연동형 인센티브 제도는 백색 가전의 현지 생산을 촉진해, 판금 프레스기나 사출 성형기용 중급 서보 수요를 촉진합니다. 일본과 한국은 기술면에서 주도적 입장을 유지하고 협동 로봇 셀과 반도체 공장용으로 고기능인 AI 대응 드라이브를 구입하고 있습니다. 한편, 동남아시아 국가들은 검사적인 자동화 셀에서 본격적인 생산 라인으로 이행을 진행하고 있습니다. 이러한 상승작용 활동은 전기 드라이브 시장에서 지역의 이점을 확고히 합니다.

북미에서는 기존 공장의 개수 수요가 안정적으로 발생하고 있으며, 미국 에너지부의 모터 규제 대응 및 수요 반응형 전력 요금 할인 제도의 활용을 목적으로 드라이브 장치의 갱신이 진행되고 있습니다. 5대호 주변에서의 자동차산업회귀의 움직임이 새로운 서보주문을 환기하여 이산제조업에 있어서의 전기 드라이브 시장 규모를 뒷받침하고 있습니다. 캐나다의 광업 섹터에서는 칼륨 및 니켈 확장에 중전압 패키지를 배포하고 있으며, 멕시코의 Tier 1 자동차 부품 제조업체는 트랜스미션 하우징 가공 센터용으로 안전 통합형 서보를 지정하고 있습니다. 병행하는 예지보전 클라우드 플랫폼의 동향은 국내 소프트웨어 에코시스템을 뒷받침해 하드웨어 출하에 디지털 서비스가 출하량의 상위를 차지하도록 보장합니다.

유럽은 성숙하면서도 혁신을 견인하는 영역이며, 인더스트리 4.0 로드맵과 유럽의 그린딜이 가변속 기술의 보급을 뒷받침하고 있습니다. 독일의 자동화 기기 수출 기업은 자석 재료 리스크 저감을 위해 동기 릴럭턴스 드라이브 장치를 요구하고, 이탈리아의 기계 제조업체는 지적 재산 보호를 위해 사이버 안전한 펌웨어를 통합, 북유럽의 프로세스 플랜트는 재생에너지 주체의 전력망 강화를 위해 회생 드라이브 장치를 채택하고 있습니다. 아프리카는 현재 규모가 작지만 남아프리카 광산이 운반 트럭의 전동화를 진행하고 나이지리아 시멘트 프레스가 중전압 인버터를 도입하는 움직임에서 2031년까지 5.26%라는 가장 빠른 CAGR을 기록하고 있습니다. 유럽의 제조업체가 노동 집약적인 프로세스를 북아프리카에 이관하는 움직임도 현지에서의 서보 채택을 뒷받침하고 있습니다. 이러한 동향이 함께 지역 수익원의 다양화가 진행되어 전기 드라이브 시장의 장기적인 성장궤도를 안정화시키고 있습니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 거시경제 요인의 영향

- 시장 성장 촉진요인

- 프로세스 및 불연속(Discrete) 제조 허브의 급격한 산업화

- 엄격한 국제 및 국내적인 에너지 효율 규제

- 고정밀 드라이브를 필요로 하는 전동 모빌리티 생산 라인의 가속

- 디지털 레트로핏-기존 설비의 에너지 절약화를 위한 가변속 드라이브 도입

- AI를 활용한 예지보전에 의한 드라이브 장치의 다운타임 삭감

- 희토류 원소를 사용하지 않는 토폴로지(축 방향 자속형, 스위치 드릴럭턴스형)로의 전환

- 시장 성장 억제요인

- 고정 속도 대체품에 비해 높은 초기 설비 투자액

- 가혹한 사용 환경과 고조파 환경에서의 신뢰성 우려

- 전력 전자 부품과 자석공급 체인 변동성

- 네트워크 접속형 스마트 드라이브에 있어서의 사이버 보안상의 취약성

- 산업 생태계 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품별

- AC 드라이브

- DC 드라이브

- 서보 드라이브

- 전압별

- 저전압 드라이브

- 중전압 드라이브

- 정격 출력별

- 250kW 이하

- 251-500kW

- 500kW 초과

- 최종 사용자 산업별

- 석유 및 가스

- 상하수도

- 화학제품 및 석유화학제품

- 식음료

- 발전

- HVAC

- 펄프 및 제지

- 이산산업

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 이탈리아

- 영국

- 프랑스

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- ABB Ltd.

- Siemens AG

- Danfoss A/S

- Rockwell Automation Inc.

- Schneider Electric SE

- Yaskawa Electric Corporation

- Mitsubishi Electric Corporation

- Nidec Corporation

- SEW-EURODRIVE GmbH and Co KG

- TMEIC Corporation

- WEG SA

- Hitachi Ltd.

- Fuji Electric Co. Ltd.

- Eaton Corporation plc

- Emerson Electric Co.

- Toshiba International Corporation Inc.

- Parker Hannifin Corporation

- Regal Rexnord Corporation

- Johnson Electric Holdings Limited

- Bonfiglioli Riduttori SpA

제7장 시장 기회와 장래의 전망

SHW 26.02.05electric drives market size in 2026 is estimated at USD 27.92 billion, growing from 2025 value of USD 26.81 billion with 2031 projections showing USD 34.17 billion, growing at 4.13% CAGR over 2026-2031.

Growth rests on three pillars: mandatory efficiency rules that push variable-speed adoption, e-mobility lines demanding high-precision motion, and brownfield retrofits aimed at slashing utility bills. Asia Pacific leads with 45.64% revenue share in 2024 because of China's factory scale and India's expanding industrial base, while Africa registers the fastest 5.46% CAGR on the back of mining and infrastructure spending. AC units deliver the bulk of shipments at 71.13% share, yet servo drives advance the quickest at a 4.47% CAGR, mirroring discrete manufacturing's need for micron-level positioning. Medium-voltage projects also pick up pace, logging a 4.81% CAGR as heavy-industry operators modernize compressor and pump assets.

Global Electric Drives Market Trends and Insights

Stringent Global and National Energy-Efficiency Mandates

New U.S., European and Chinese rules elevate minimum motor efficiency levels, effectively compelling variable-frequency drive adoption in energy-intensive plants. Industrial audits show motors consuming up to 70% of manufacturing electricity, so replacing fixed-speed starters yields sizable carbon and cost savings. Governments now link tax incentives and grant programs to verified drive retrofits, creating predictable demand for certified products. Vendors respond by packaging drives with energy-assessment software that quantifies payback in under three years. As a result, the electric drives market gains a durable replacement cycle anchored in policy enforcement.

Acceleration of E-Mobility Production Lines Needing High-Precision Drives

Battery assembly, motor winding and quality-control stations in electric-vehicle plants require sub-0.1 millimeter repeatability, placing servo drives at the heart of line design Automotive OEMs have committed more than USD 100 billion toward electrification, and each greenfield factory specifies advanced motion packages from day one. Brownfield retrofits of internal-combustion plants also replace legacy conveyors with servo-based flexible cells. Servo vendors add integrated safety and decentralized I/O to simplify robot collaboration, accelerating plug-and-play deployment. This continuous capital flow cements the electric drives market as a primary beneficiary of e-mobility investment.

High Initial Capex Versus Fixed-Speed Alternatives

Variable-frequency drives cost three to five times more than contactor starters, making capex a hurdle in cash-constrained plants. Payback periods under three years appeal to financially savvy operators, yet many still defer upgrades when electricity is subsidized. The objection is acute in sub-15 kW ranges where absolute savings are modest, extending breakeven timelines. Financing options such as drive-leasing or energy-as-a-service are emerging but remain scarce outside North America and Western Europe. Over time, falling semiconductor prices and utility incentives may ease the barrier, widening addressable demand in the electric drives market.

Other drivers and restraints analyzed in the detailed report include:

- Digital Retrofits - Variable-Speed Drives for Brownfield Energy Savings

- AI-Enabled Predictive Maintenance Reducing Downtime of Drive Systems

- Cyber-Security Vulnerabilities in Network-Connected Smart Drives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

AC drives held a dominant 70.62% electric drives market share in 2025, reflecting their versatility in pumps, fans and conveyor lines that underpin global factory automation. Standardized interfaces, mature component supply chains and broad installer familiarity sustain demand, particularly in food processing and water utilities where reliability trumps cutting-edge performance. Over the forecast horizon, the electric drives market will continue to rely on AC platforms for baseline motor control as utilities tighten efficiency targets in centrifugal equipment. Servo drives remain the fastest-growing niche with a 4.25% CAGR through 2031 thanks to discrete manufacturing plants that require sub-micrometer positioning in battery, electronics and medical-device assembly. Servo vendors now bundle integrated safety functions and one-cable networks, distinguishing their premium offerings from commoditized AC units.

The electric drives market benefits from a technology crossover as servo algorithms migrate into high-end AC packages, blurring historic product lines while keeping cost curves attractive for mid-tier users. DC drives, once favored in metals and mining, now occupy shrinking pockets because modern AC vector control replicates their torque fidelity at lower maintenance cost. Yet some rolling-mill operators still specify DC units for legacy compatibility, providing a modest replacement stream. Multi-drive platforms that combine AC, servo and DC axes in a single rack are gaining attention, especially among machine-builder OEMs that value unified programming across motion classes. This convergence supports life-cycle service revenues for top suppliers, reinforcing moderate concentration in the broader electric drives market.

Low-voltage systems below 1 kV accounted for 62.98% of 2025 revenue, underpinning most factory pumps, compressors and material-handling lines. Installation simplicity, ready availability of molded-case protection gear and widespread technician skill sets keep total ownership cost low, ensuring that the electric drives market retains a low-voltage core in standard manufacturing. Growth nonetheless skews toward medium-voltage equipment, which is projected to advance at a 4.62% CAGR through 2031 as heavy-industry operators upgrade large motors to variable-speed duty.

Medium-voltage projects typically surface during brownfield capacity expansions or greenfield investments in LNG, cement and desalination plants, where pumps or compressors exceed 2 MW. Operators favor these solutions for improved power factor and reduced cable losses relative to running multiple low-voltage motors in parallel. Quasi-two-level inverter topologies, silicon-carbide devices and regenerative capabilities now differentiate premium medium-voltage packages, helping suppliers justify higher margins. Utility-interactive features such as harmonic mitigation and grid-support modes align with nascent microgrid programs in mining and remote oilfields, adding resilience value. As a result, the electric drives market sees a bifurcation: commoditized low-voltage volumes sustain scale while technologically sophisticated medium-voltage units generate disproportionate profit pools.

The Electric Drives Market Report is Segmented by Product (AC Drives, DC Drives, and Servo Drives), Voltage (Low-Voltage Drive, and Medium-Voltage Drive), Power Rating (Less Than 250 KW, 251-500 KW, and More Than 500 KW), End-User Industry (Oil and Gas, Water and Wastewater, Chemical and Petrochemical, Food and Beverage, Power Generation, HVAC, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific retained the largest share of the electric drives market in 2025 at 45.10%, sustained by China's USD 50 billion 2024 automation spend and India's incentive-backed factory build-out. Chinese enterprises continue to replace legacy starters with variable-speed packages to satisfy the country's latest energy-intensity mandate, while servo adoption accelerates in battery-gigafactory clusters along the Yangtze River Delta. India's Production Linked Incentive scheme drives localized manufacturing of whitegoods, spurring mid-range servo demand in sheet-metal presses and injection-molding machines. Japan and South Korea remain technology front runners, purchasing premium AI-enabled drives for collaborative robot cells and semiconductor fabs, whereas Southeast Asian nations advance from pilot automation cells to full production lines. These combined activities cement regional primacy in the electric drives market.

North America delivers steady replacement demand as brownfield plants retrofit drives to meet U.S. DOE motor rules and leverage utility rebates for demand-response. Automotive reshoring initiatives around the Great Lakes trigger fresh servo orders, underscoring the electric drives market size within discrete manufacturing. Canada's mining sector deploys medium-voltage packages in potash and nickel expansions, while Mexico's tier-one automotive suppliers specify safety-integrated servos for transmission-housing machining centers. A parallel trend toward predictive-maintenance cloud platforms favors domestic software ecosystems, ensuring that digital services layer atop hardware shipments.

Europe represents a mature yet innovation-driven arena where Industry 4.0 roadmaps and the European Green Deal reinforce variable-speed penetration. German automation exporters demand synchronous-reluctance drives to trim magnet material risk, Italian machinery OEMs embed cyber-secure firmware to protect intellectual property, and Nordic process plants adopt regenerative drives to bolster renewable-heavy grids. Africa, although holding a smaller base today, records the fastest 5.26% CAGR to 2031 as South African mines electrify haul trucks and Nigerian cement presses install medium-voltage inverters. European manufacturers relocating labor-intensive stages to North Africa also lift localized servo uptake. Collectively, these patterns diversify regional revenue streams, stabilizing the long-term trajectory of the electric drives market.

- ABB Ltd.

- Siemens AG

- Danfoss A/S

- Rockwell Automation Inc.

- Schneider Electric SE

- Yaskawa Electric Corporation

- Mitsubishi Electric Corporation

- Nidec Corporation

- SEW-EURODRIVE GmbH and Co KG

- TMEIC Corporation

- WEG S.A.

- Hitachi Ltd.

- Fuji Electric Co. Ltd.

- Eaton Corporation plc

- Emerson Electric Co.

- Toshiba International Corporation Inc.

- Parker Hannifin Corporation

- Regal Rexnord Corporation

- Johnson Electric Holdings Limited

- Bonfiglioli Riduttori S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors

- 4.3 Market Drivers

- 4.3.1 Rapid industrialisation in process and discrete manufacturing hubs

- 4.3.2 Stringent global and national energy-efficiency mandates

- 4.3.3 Acceleration of e-mobility production lines needing high-precision drives

- 4.3.4 Digital retrofits - variable-speed drives for brownfield energy savings

- 4.3.5 AI-enabled predictive maintenance reducing downtime of drive systems

- 4.3.6 Shift toward rare-earth-free topologies (axial-flux, switched-reluctance)

- 4.4 Market Restraints

- 4.4.1 High initial capex versus fixed-speed alternatives

- 4.4.2 Reliability concerns in harsh-duty, high-harmonic environments

- 4.4.3 Supply-chain volatility for power-electronic components and magnets

- 4.4.4 Cyber-security vulnerabilities in network-connected smart drives

- 4.5 Industry Ecosystem Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product

- 5.1.1 AC Drives

- 5.1.2 DC Drives

- 5.1.3 Servo Drives

- 5.2 By Voltage

- 5.2.1 Low-Voltage Drive

- 5.2.2 Medium-Voltage Drive

- 5.3 By Power Rating

- 5.3.1 Less than 250 kW

- 5.3.2 251-500 kW

- 5.3.3 Above 500 kW

- 5.4 By End-User Industry

- 5.4.1 Oil and Gas

- 5.4.2 Water and Wastewater

- 5.4.3 Chemical and Petrochemical

- 5.4.4 Food and Beverage

- 5.4.5 Power Generation

- 5.4.6 HVAC

- 5.4.7 Pulp and Paper

- 5.4.8 Discrete Industries

- 5.4.9 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 Italy

- 5.5.3.3 United Kingdom

- 5.5.3.4 France

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level overview, Market level overview, Core segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ABB Ltd.

- 6.4.2 Siemens AG

- 6.4.3 Danfoss A/S

- 6.4.4 Rockwell Automation Inc.

- 6.4.5 Schneider Electric SE

- 6.4.6 Yaskawa Electric Corporation

- 6.4.7 Mitsubishi Electric Corporation

- 6.4.8 Nidec Corporation

- 6.4.9 SEW-EURODRIVE GmbH and Co KG

- 6.4.10 TMEIC Corporation

- 6.4.11 WEG S.A.

- 6.4.12 Hitachi Ltd.

- 6.4.13 Fuji Electric Co. Ltd.

- 6.4.14 Eaton Corporation plc

- 6.4.15 Emerson Electric Co.

- 6.4.16 Toshiba International Corporation Inc.

- 6.4.17 Parker Hannifin Corporation

- 6.4.18 Regal Rexnord Corporation

- 6.4.19 Johnson Electric Holdings Limited

- 6.4.20 Bonfiglioli Riduttori S.p.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment